all definitions

1/88

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

89 Terms

Edgeworth box

consists of fitting in thesame graph the indifference curves of both players from opposite origins, where the sizes of the edges of the box represent the total resources of the economy (which we canassume are finite)

Pareto Efficient

an allocation that cannot be improved upon without harming any agent

Contract Curve

The set of Pareto efficient points

Core

The set of Pareto efficient that also improve upon the initial endowment

full insurance

when the agent insures for the whole potential loss (constant wealth)

risk premium

the extra

amount of money an agent is willing to pay with respect to a

risk neutral person. This is quantified by the difference

between E (w ) and the certain equivalent.

adverse selection

the asymmetry in information arises before the contract is

signed

Signaling

the more informed agent might provides

evidence to prove their type

Screening

the less informed agent might ”investigate” to

learn those hidden characteristics

moral hazard

yhe concept that individuals have incentive to alter their behavior when their risk or bad decision making is borne by others

Subgame Perfect Equilibrium

a set of

strategies that constitute a Nash equilibrium in all the

subgames.

Cournot model

Simultaneous quantity setting model.

Bertrand model

Simultaneous price setting model.

Stackelberg model

Sequential quantity setting model. Price is then set

via market demand.

First welfare theorem

in ideal conditions, (perfect markets, no externalities, complete markets, full information) a competitive market equilibrium results in a Pareto efficient allocation.

second welfare theorem

For each allocation in the contract curve, there is a price that supports the desired allocation as a competitive equilibrium. through a suitable redistribution of initial wealth or resources (endowments). Efficiency and distribution can be separated

Nash equilibrium

The Nash equilibrium occurs when each player is playing their best responsive, given the actions that their rivals are playing

pareto optimality

being at an allocation of resources where it is not possible to make one person better off without making someone else worse off.

coase theorem

private parties can efficiently solve externality problems (like pollution) through bargaining, leading to an optimal outcome without government intervention

AS long aS: property rights are clearly defined and transaction costs are low

uncertainty

relates to missing information, in which the link between cause and consequence, choices and outcomes, is not deterministic

Certain Equivalent

the certain lottery which is equivalent to the risky one.

exogenous

having an external cause or origin

club good

excludable but non rivalrous

public good

non excludable and non rivalrous

private good

excludable and rivalrous

Jensens inequality

for a concave function, U(EV)> EU. the utility of the expected value exceeds the expected utility. The individual is risk-averse — they would prefer the certain EV over the gamble.

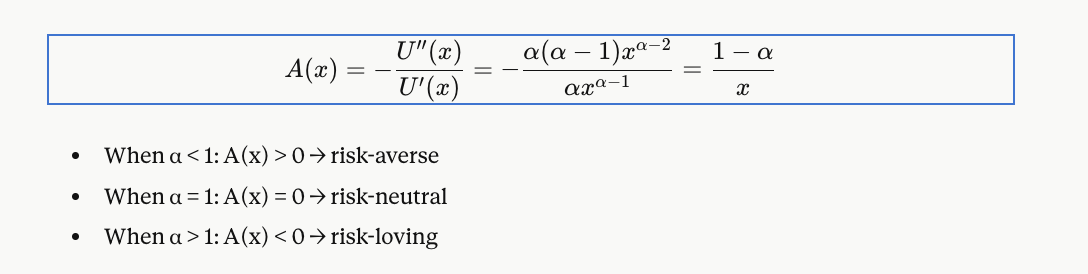

Arrow-Pratt measure of absolute risk aversion:

image

risk neutral

The expected utility is equal to the utility associated with the expected wealth.

risk averse

The expected utility is less than the utility associated with the expected wealth.

risk seeking

The expected utility is greater than the utility associated with the expected wealth.

Completeness

For any two bundles X and Y, either X ≿ Y or Y ≿ X — agents are never indecisive.

Transitivity

If X ≿ Y and Y ≿ Z, then X ≿ Z

Monotonicity

More is always better — for any X and ε > 0, (x₁ + ε, x₂ + ε) ≿ (x₁, x₂).

Continuity

Small changes to bundles do not reverse the preference order.

Convexity

Averages are preferred to extremes — if X ≿ Y then αX + (1-α)Y ≿ Y for α ∈ [0,1]. Implies diminishing MRS. consumers prefer a mix of goods over an extreme amount of one

Utility Function

A numerical representation of preferences. Requires preferences to be complete, transitive and continuous.

Indifference Curve:

The set of bundles giving equal utility

Marginal Rate of Substitution (MRS):

The rate at which a consumer is willing to trade good 2 for good 1 while remaining indifferent. Equal to the slope of the indifference curve.

Homothetic Preferences

If X ≿ Y then tX ≿ tY for all t > 0 — scaling both bundles preserves preferences. Income offer curves are straight lines through the origin.

WARP

if bundle A is chosen over B, B is never chosen over A when both are affordable.

SARP

If a consumer chooses bundle \(A\) over \(B\), and \(B\) over \(C\) (directly or indirectly), they will never choose \(C\) over \(A\) when both are affordable.

Budget Constraint

the set of affordable bundles at given prices and income.

Revealed Preference

if bundle x is chosen when y is affordable, x is revealed preferred to y.

Normal Good:

∂x1∗/∂m>0 — demand increases with income.

Inferior Good:

∂x1∗/∂m<0 — demand decreases with income.

Ordinary Good

∂x1∗/∂p1<0 — demand decreases when own price rises (law of demand holds).

Giffen Good

∂x1∗/∂p1>0 — demand increases when own price rises. Must be inferior, and income effect must outweigh substitution effect

Engel Curve

Plots relationship between income (m) and optimal demand (x*) holding prices fixed. Upward sloping for normal goods, backward bending for inferior goods.

Slutsky Substitution Effect

Change in demand due purely to the change in relative prices, holding purchasing power constant (original bundle still affordable).

Hicksian Demand

optimal demand holding utility constant. Also called compensated demand.

Hicksian Substitution Effect:

Change in demand due to price change holding utility constant. Always larger in magnitude than Slutsky substitution effect.

Compensating Variation (CV)

Income adjustment needed after a price change to restore original utility. Evaluated at new prices. use original utility

Equivalent Variation (EV)

Income adjustment needed before a price change to give the consumer final utility. Evaluated at original prices:

Consumer Surplus

Difference between maximum willingness to pay and actual price paid. Area below demand curve above price.

Risk

Situations where outcomes and their probabilities are known.

Expected Value (EV):

The probability-weighted average of monetary outcomes.

Expected Utility (EU):

The probability-weighted average of utilities — accounts for attitude to risk.

Certainty Equivalent (CE):

The certain amount giving the same utility as the risky lottery:U(CE)=EU

Full insurance

When an agent insures for the whole potential loss (k = A), resulting in equal wealth across all states of the world (w_b = w_g).

problem with adverse selection, a fair premium would be premium=pL probabiloity times loss. individuals know p, insures dont. so they charge an average p. this may be greater than low risk p, so premium is > than fair premium, drives individuals out

Willingness to pay (insurance)

The maximum annual premium an agent will pay for insurance; equal to the difference between wealth in the good state (w_g) and the certainty equivalent.

Pure exchange economy

an economy fully described by a set of traders, their preferences (utility functions), and their initial resource endowments — no production.

Edgeworth box

A graphical tool that fits the indifference curves of two agents from opposite origins into a single box, where the box dimensions represent total economy resources.

Competitive equilibrium

A pair of prices and an allocation such that every agent maximises utility at those prices and all markets clear, under price-taking behaviour.

First Fundamental Welfare Theorem

Every competitive equilibrium allocation is Pareto efficient. Requires only that preferences are monotone.

Second Fundamental Welfare Theorem

For every allocation on the contract curve there exist prices that support it as a competitive equilibrium, provided preferences are convex and a lump-sum redistribution is feasible.

Lump-sum transfer

A costless and immediate redistribution of initial endowments (e.g. via government taxation) used to move the economy to a preferred point on the contract curve.

Market failure

A situation in which competitive markets produce an inefficient outcome.

Dominant strategy

An action that yields a strictly higher payoff than any alternative, regardless of what all other players do.

Best response

The action that maximises a player's payoff given the strategies chosen by all other players.

Prisoners' dilemma

A two-player game whose unique Nash equilibrium is Pareto inefficient; illustrates how individually rational behaviour can lead to collectively suboptimal outcomes.

Backward induction

The technique for finding SPE by solving the game from terminal nodes back to the root, replacing each subgame with its equilibrium payoff.

Non-credible threat

A planned strategy from which a player would want to deviate once the relevant node is actually reached, making the threat strategically irrelevant.

Grim trigger

A repeated-game strategy: cooperate as long as the opponent cooperates; after any deviation, defect forever.

Collusion

An agreement between competing firms to set monopoly prices and share profits rather than compete; its sustainability is a core question in repeated-game analysis.

Externality

A situation where one agent's consumption or production directly affects another agent's utility or costs, outside of any market transaction.

Pigouvian tax/subsidy

A tax (for negative externalities) or subsidy (for positive externalities) set equal to the marginal external cost or benefit at the social optimum, aligning private and social marginal costs.

Tragedy of the commons

The tendency for a shared resource to be over-exploited when individuals, acting in self-interest, fail to account for the negative externality their use imposes on others.

Non-rivalry

A property of public goods: one agent consuming the good does not prevent another from consuming the same unit.

Non-excludability

A property of public goods: agents cannot be excluded from benefiting, making it impossible to charge a market price.

Free riding

The incentive for individuals to under-contribute to a public good, relying on others' contributions; results in underprovision in private markets.

feasible allocation

if the total amount of each good consumed is equal to the total amount available

initial endowment allocation

the allocation that the consumers start with

Price Elasticity of Demand (PED)

the ratio of relative changes, (usually referred to in absolute terms)

tragedy of the commons

explains why externalities cause market failures. concept describing how individuals, acting separately for their own self-interest, deplete a shared resource

consumption externality

if one consumer cares directly about another agent’s production or consumption.

production externality

when the production possibilities of one firm are influenced by the choices of another firm or consumer

Coase theorem

if property rights are clearly defined and transaction costs are zero, and preferences are quasilinear, private parties can negotiate a beneficial trade regardless of initial endowments

Lindahl equilibrium

The state should charge different prices to agents, proportional to their willingness to pay

marshallian demand

the quantity of a good a consumer chooses to buy in order to maximize utility, given their fixed income and the prices of goods