FI 301 Exam 3

1/81

Earn XP

Description and Tags

Ch. 6, 9, 17, 19, 23

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

82 Terms

What are money market securities ?

MM securities are debt securities with a maturity of one year or less

What do the yields on MM securities represent ?

Short term-interest rates

Who issues MM securities ?

The treasury, corporations, and financial intermediaries that wish to obtain short-term financing

Who purchases MM securities ?

Households, corporations, and government that have funds available for a short time period

Where can MM securities be sold ?

Sold in secondary market and are liquid

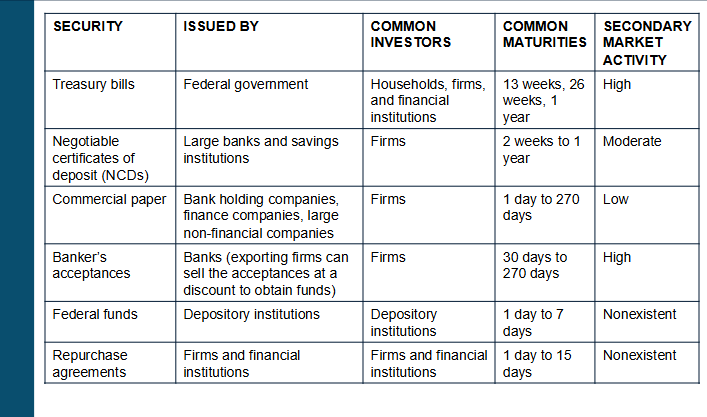

What are the most important MM securities ?

T-bills

Commercial paper

Negotiable certificates of deposit

Repurchase agreements

Federal funds

Banker’s acceptances

T-bills

Issued when the U.S. government needs to borrow funds

issues T-bills with 1-year maturity every 4 weeks

Can periodically issue “cash management bills” when additional cash needs to be raised quickly

maturities of less than 4 weeks

Credit risk of T-bills ?

Backed by Federal government, virtually free of credit risk

Liquidity of T-bills ?

T-bills can be easily liquidated due to short maturity and strong secondary market

Investors in T-bills ?

Depository institutions retain a portion of their funds in T-bills that can be liquidated to accommodate withdrawals

Other financial institutions invest in T-bills in case cash outflows exceed cash inflows

Individuals with substantial savings commonly invest indirectly through money market funds

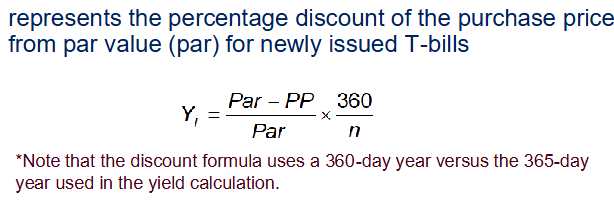

T-bill pricing

Priced at a discount from their par value

Price depends on investor’s required rate of return

T-bills do not offer interest payments to investors

Value of a T-bill is the present value of the par value

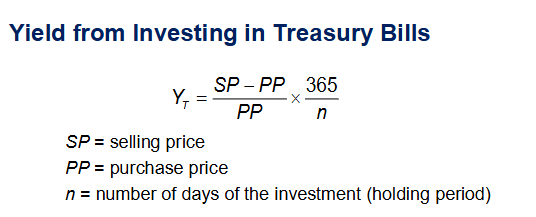

T-bill Yield

T-bill discount

T-bill auctions

Any investor can submit bids online for newly issued T-bills at www.treasurydirect.gov

Competitive bids

Bidders specify maximum price they’re willing to pay, can buy up to 35% of securities being offered

Noncompetitive bids

Bidders guaranteed to receive securities (max $10m per auction per NC bidder), agree to pay whatever price is established by competitive bidders in the auctions

All winning bidders pay the same price in an auction

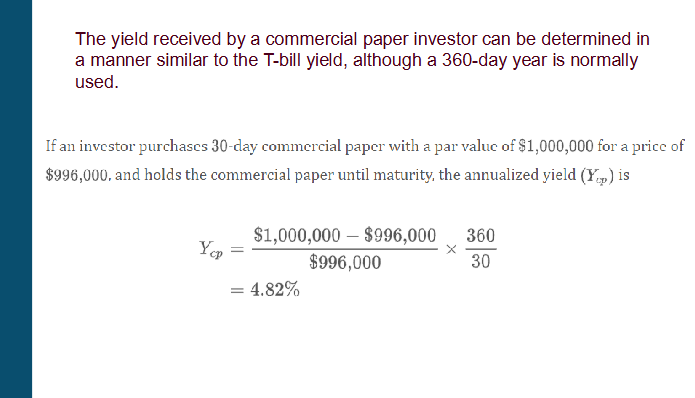

What is Commercial paper

Short-term debt instrument issued by a large, well-known, creditworthy firm

typically unsecured (no collateral)

there is asset-backed commercial paper which is collateralized

Normally issued to provide liquidity or to finance a firm’s investment in inventory and accounts receivable

The issuance of commercial paper is an alternative to short-term bank loans.

is often a cheaper source of funds than borrowing from commercial banks

Basic characteristics of Commercial paper ?

minimum denomination of commercial paper is usually $100k

typically sold in multiples of $1M

Maturities are normally between 20 and 45 days but can be as short as 1 day or as long as 270 days

C paper does not offer interest payment, investors can earn return by buying at a discount from par value

Yield on C paper is close to but higher than T-bill with the same maturity

Higher credit risk and less liquidity

C paper yield ?

C paper credit risk ?

C paper is issued by corporations that may be susceptible to failure,

investors face default risk

risk is affected by issuers financial condition and cash flow

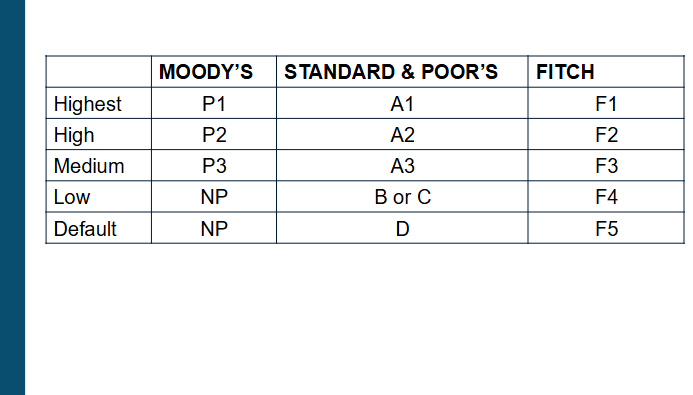

Credit ratings are assigned by agencies such as Moody’s Investors Service, S&P Corporation, and Fitch Investor Service

C paper ratings ?

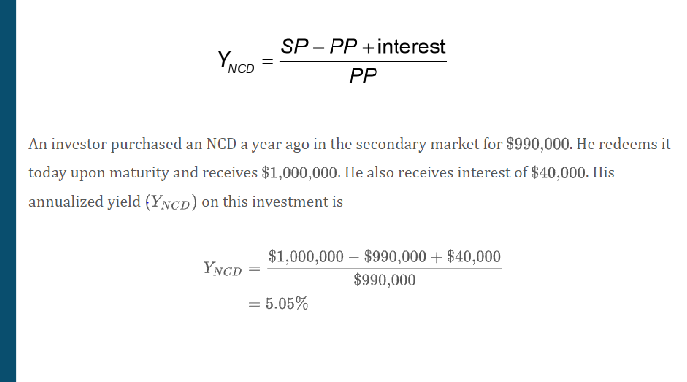

What are Negotiable Certificates of Deposit ?

Certificates issued by large commercial banks and other depository institutions as a short-term source of funds

The minimum denomination is $100k

Maturities on NCDs normally range from 2 weeks to 1 year

Secondary market for NCDs exists, providing investors with some liquidity

Investors in NCDs earn a return from interest payments and capital gains

NCD yields offer a premium above the T-bill yield to compensate for less liquidity and higher credit risk

Formula for NCDs ?

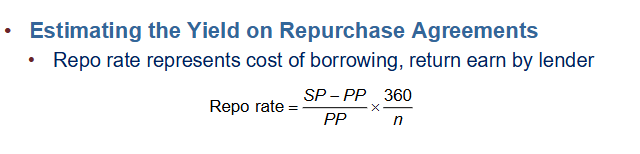

What are repurchase agreements ?

In a repurchase agreement (repo), one party sells securities to another with an agreement to repurchase the securities at a specified date and price.

A reverse repo is the purchase of securities by one party with an agreement to sell them.

A repurchase agreement represents a loan backed by the securities

Financial institutions often participate in repos

Transaction amounts are usually for $10M or more

The most common maturities are from 1 day to 15 days and for one, three, and six months

Impact of Credit Crisis on Repurchase Agreements

Some financial institutions that relied on the market for funding were not able to obtain funds

Investors became more concerned about the securities that were posted as collateral

Estimating yield on Repurchase Agreements

Repo rate represents cost of borrowing, return earn by lender

Federal Funds

Enable depository institutions to lend or borrow short-term funds from each other at the federal funds rate

Federal reserve adjusts the amount of funds in depository institutions to influence the federal funds rate

The rate is normally slightly higher than the T-bill rate at any given time

Loans are normally in excess of $5M

Maturity typically 1 to 7 days (can be longer)

Banker’s Acceptances

Indicate that a bank accepts responsibility to make a payment to a seller of goods

Commonly used for international trade transactions where counterparty risk is difficult to determine

Often sold before maturity, active secondary market

Investors who buy banker’s acceptances in the secondary market earn returns buy buying at a discount to face value

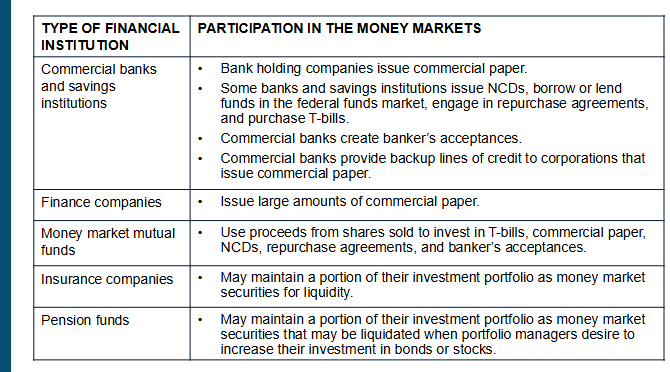

Summary of MM Securities

Institutional Use of MM markets

What is a mortgage ?

A mortgage is a form of debt to finance a real estate investment

What does a mortgage contract specify ?

Mortgage rate (interest rate)

Maturity (years)

Collateral

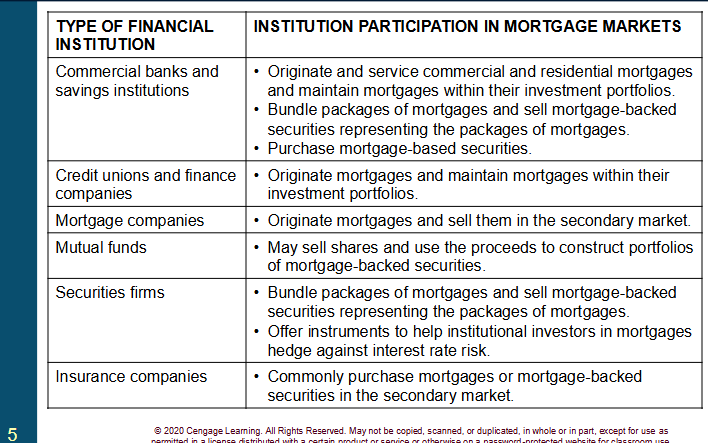

What financial institutions originate mortgages ?

Mortgage companies

Savings institutions

Commercial banks

What financial institutions create and sell mortgage-backed securities ?

Government agencies (Fannie Mae, Freddie Mac)

Commercial banks

What financial institutions invest in Mortgages and MBS ?

Savings institutions

Commercial banks

Insurance companies

Pension funds

Mutual funds

Institutional Use of Mortgage Markets

Criteria Used to Measure Creditworthiness

Level of equity invested by the borrower

Borrower’s income level

Borrower’s credit history

Prime versus Subprime Mortgages

Insured versus Conventional Mortgages

Level of equity invested by the borrower

The lower the down payment, the higher the probability that the borrower will default

Loan-to-value ratio: proportion of the property’s value that is financed with debt. Greater default risk with higher LTV ratio

Borrower’s income level

Borrowers who have a lower level of income relative to the periodic loan payments are more likely to default on their mortgages

Borrower’s credit history

Borrowers with a history of credit problems & low credit scores are more likely to default on their loans

Prime versus Subprime Mortgages

Prime: borrower meets traditional lending standards

Subprime: borrower does not qualify for prime loan

lower income, high existing debt, small down payment

usually higher interest rate

Insured versus Conventional Mortgages

Insured: loan is insured by FHA or VA

FHA - lower income borrowers; VA - veterans

Conventional: loan is not insured by FHA or VA but can be privately insured

Private mortgage insurance (PMI) typically required when down payment is less than 20% of property value

Fixed-rate mortgages

Locks in borrower’s interest rate of the life of the mortgage

Financial institution that holds fixed-rate mortgages is exposed to interest rate risk

value of fixed-rate mortgage decreases when interest rates increase

value of mortgage = PV of remaining payments

lower PV results from higher interest rates

Borrowers with fixed-rate mortgages do not suffer from rising rates, but they do not automatically benefit from declining rates

Borrowers may refinance at lower rates

Results in lower monthly payments, but must pay fees to refinance

Adjustable-rate mortgages (ARMs)

Allows the mortgage interest rate to adjust to market conditions

Contract will specify a precise formula for this adjustment

Some ARMs contain a clause that allow the borrower to switch to a fixed rate within a specific period

Some ARMs are fixed for a period, then adjust once or twice per year

ARMs from a Financial institutions perspective

Mortgages with adjustable rates have values that are more stable, less affected by interest rate increases

Effect of higher discount rates (reduces value of mortgage) offset by adjustment to (increase in) monthly payments when rates increase

Graduated-payment mortgages

Allow the borrower to make small payments initially on the mortgage; the payments increase periodically then level off after 5 or 10 years

Growing-equity mortgages

Monthly payments are initially low and increase over time. The payments never level off but continue to increase throughout the life of the loan

Second mortgages (Home equity loans & HELOCs)

A second mortgage can be used in conjunction with the primary or first mortgage

Offers homeowners opportunity to borrow against home equity

Shared-appreciation mortgages

Allow a home purchaser to obtain a mortgage at a below-market interest rate. In return, the lender will share the price appreciation of the home.

borrower is trading potential upside for lower interest rate

Balloon payment mortgages

Require only interest payments for a 3-5 year period

At the end of the this period, the borrower must pay the full amount of the principal (the balloon payment)

Mortgage Lender Risk

Credit risk

Interest rate risk

Prepayment risk

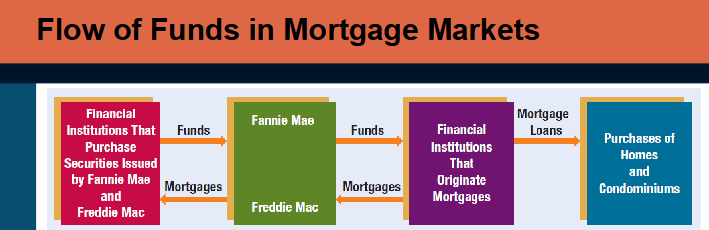

Securitization

The Securitization Process

Credit risk

The risk that the borrower will make a late payment or will default

Interest rate risk

Mortgage values will fall when interest rates rise

Prepayment risk

Borrowers may prepay the mortgage when interest rates fall.

Lenders get capital back all at once, new loans issued will pay lower interest rates

Securitization

The pooling and repackaging of loans into securities

Securities are then sold to investors

The Securitization Process

A financial institution such as a commercial bank or federal agency combine individual mortgages together into packages

Securities are sold to investors

MBS issuer receives interest and principle payments on the mortgages

Transfers (passes through) the payments (minus fees) to investors that purchased the MBS

Flow of Funds in Mortgage Markets

Fannie Mae - Federal National Mortgage Association (FNMA)

Created by the federal gov’t in 1938 to develop a more liquid secondary market for mortgages

Converted into a public, shareholder-owned corporation in 1968

Freddie Mac - Federal Home Loan Mortgage Corporation (FHLMC)

Created by federal gov’t in 1970, converted to public company in 1989

Business Model of Fannie and Freddie

Issue securities to investors, use capital raised to buy mortgages, sell MBS

Purpose is to promote affordable home ownership

Classified as a government-sponsored enterprise

Backed by “implicit” guarantee that federal gov’t would not allow these institutions to fail or default on debts, which reduces their cost of capital and increases their security prices

Implicit guarantee effectively became explicit in 2008

FNMA (Fannie Mae) mortgage-backed securities

Mortgages typically purchased from commercial banks

FHMLC (Freddie Mac) participation certificates

Mortgages typically purchased from smaller savings banks

GNMA (Ginnie Mae) mortgage-backed securities

Guarantees payment to investors buying securitized FHA & VHA loans

Ginnie Mae does not actually issue the MBS, done by private institutions

Private label pass-through securities

Packaged by private financial institutions (“Non-agency”)

More flexibility on what kinds of mortgages to package (jumbo, Alt-A, and other non-traditional mortgages)

‘