Economics of Regulation - L1+2

1/82

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

83 Terms

What is the Economics of Regulation About?

Using a regulated service, this service is funded by users or taxpayers, and it has to raise enough revenue to ensure it is financially and/or fiscally sustainable.

Revenue cannot be the only dimension against which the prices are assessed, because the prices should also send the right signal to users.

Economics of Regulation provides a conceptual framework for evaluating when and how government intervention is necessary to correct market failures in public services.

Why is Regulation Important?

Economic Importance:

A large portion of household budgets goes to essential services.

This makes them economically important and justifies regulation to ensure fair pricing, efficiency, and accessibility. (e.g., water, electricity, transportation)

Social desirability & risks

Many societies view public services (like water, electricity, transport) as basic rights that everyone should have access to and it should be affordable.

This creates a demand for universal access. (possible risks exclusion & inefficiencies)

If regulator gets it wrong

Bad regulation can lead to high prices for users (households, businesses, industries). At the same time, service providers may make excessive profits, without necessarily improving service quality.

=> regulation: crucial for social fairness & protecting users

what is regulation?

Government regulations is:

• local, federal or state government control

• of individual or firm behavior

• via three main instruments:

control of prices, quantities, and quality of goods/services

Which Services are Regulated?

Public infrastructure (e.g., water, energy, telecoms), Health services, Education & Financial systems are common sectors

=> bc social importance & prone to market failure risks

Why are These Services (public infrastructure, health services, education, financial systems) Regulated?

Unregulated markets typically fail to provide services at the right quality, quantity, or price.

Goal: correct inefficiencies, promote fairness, and safeguard public interest, especially in monopoly or near-monopoly settings

How Does an Economist Approach Regulation?

Economists analyse cost and demand structures to assess market failures.

They recommend government intervention when markets fail to allocate resources efficiently or equitably.

When and How Do Markets Fail?

3 main causes:

• Imperfect competition (e.g., monopolies, technology leads to natural monopoly)

• Information asymmetries (e.g., hidden costs, under-provision, over-consumption)

• Externalities (e.g., pollution)

=> these lead to suboptimal outcomes requiring regulatory correction

Is Regulation Controversial?

YES => Economists accept (im)perfect competition and market failures as justification for regulation, but political actors may resist regulation due to ideological beliefs, risk of government failure, or influence from interest groups.

Regulation ≠ politically neutral, 2 competing political views:

Pro-regulation-view

Skeptical view of Gov

What are the main theories of Regulation? (Eu perspective, understanding over time)

1) Public Interest Theory : Traditional theories

Assumes government acts benevolent and competent actors to fix failures

Assumptions:

• Markets can fail.

• Governments act in the public interest.

Limitations: Overlooks real-world frictions like transaction costs, information asymmetries, and influence from interest groups.

=> somewhat idealistic theory, assuming good intentions and capabilities of public institutions.

2) Private Interest Theory: Criticism of traditional theories

Accounts for self-interest and capture risks as a goal to limit government opportunism + excessive discretion

=> This theory emphasises the risks of regulation being misused or distorted by vested interests.

3) Hybrid Theories: Modern vision

Recognises that both markets & governance can fail

Considers incentives, institutional constraints, non-benevolent actors & limited capacity

=> This theory “incentives matter”

What do we mean by Efficiency as a Driver of Regulation?

Ideal regulator is:

• Benevolent: The regulator wants to serve the public interest.

• Omniscient: Has perfect knowledge of demand (what users want) and supply (production technology).

• Omnipotent: Can implement decisions without legal or institutional barriers.

• Rational: Makes decisions based on logic and consistent objectives.

In such a theoretical world, the regulator would:

Determine the optimal quantity (q*) of a public service to be provided.

Set the price to match the marginal cost of production at that quantity.

=> This ideal point is called the efficient allocation

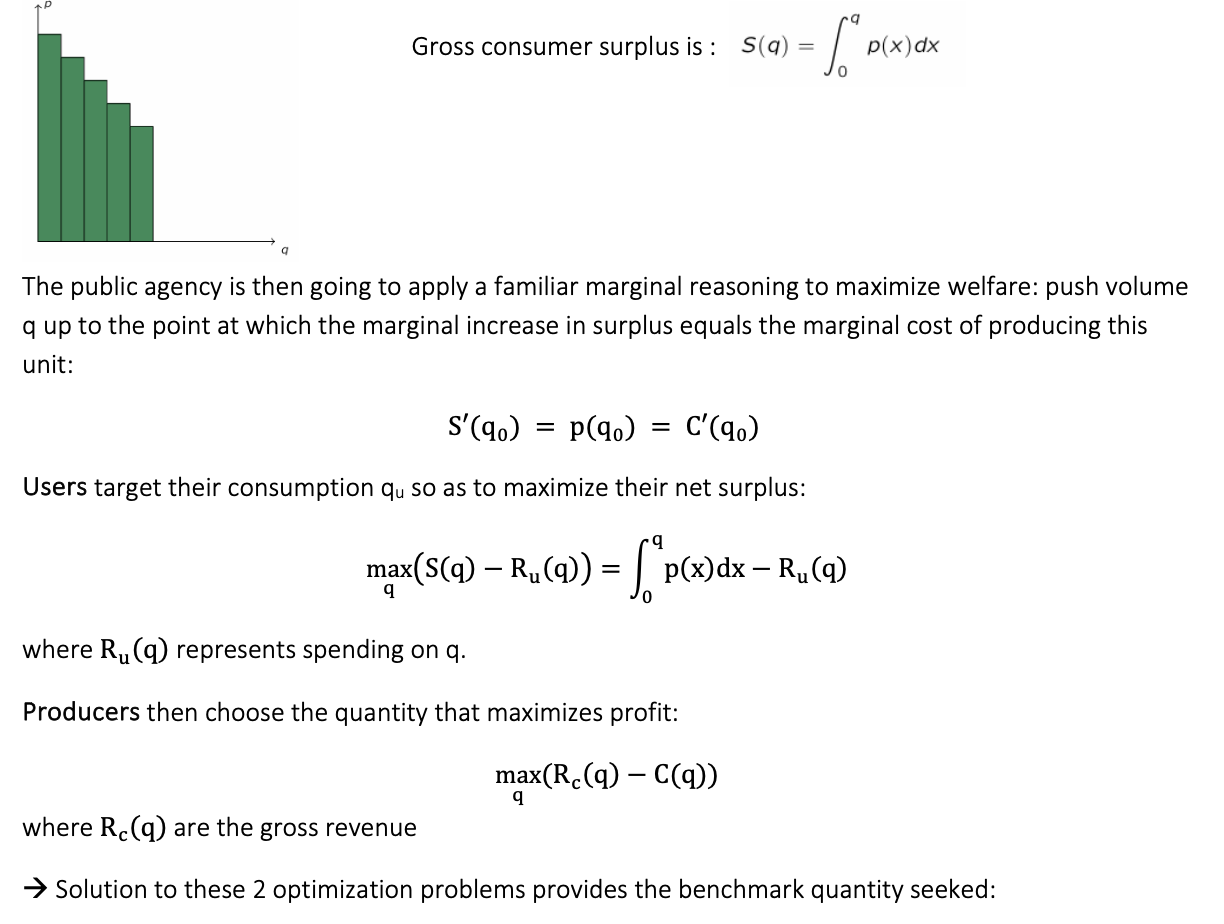

How does the regulator measure Efficiency?

Let’s say, regulator wants to produce & distribute volume q of some good/service:

- S(q) = Social benefit (surplus) of producing quantity q

- C(q) = Total cost of producing quantity q

Then the regulator's goal is to solve:

max S(q) − C(q)

This means the regulator wants to find q where marginal surplus = marginal cost:

S′(q) = C′(q)

Since the derivative of surplus with respect to q is price people are willing to pay for the last unit (p(q)), this condition becomes: p(q) = MC(q)

=> This is the famous marginal cost pricing rule

what are challenges for Efficiency as Driver of Regulation?

Famous marginal cost pricing rule, rarely observed in realty; Practical challenges include imperfect information and institutional constraints

Measuring surplus and demand is hard

Regulators often lack precise information about costs and demand

Political and institutional constraints make implementation imperfect

=> it is a benchmark that serves as a guide for what regulation should aim to approximate

how is the marginal cost pricing benchmark computed?

Solving the user problem, the optimal consumption choice is such that that marginal surplus matches the marginal spending:

S′(q) = p(q) = R’(q)

• Solving the producers problem when their marginal revenue matches the marginal cost of

production:

R’(q) = C′(q)

→ I competition functions properly, the agreement defines the

equilibrium benchmark quantity, where qc= qu, and ensures that resources are allocated efficiently.

How are the impacts of these deviations from the marginal cost pricing benchmark measured?

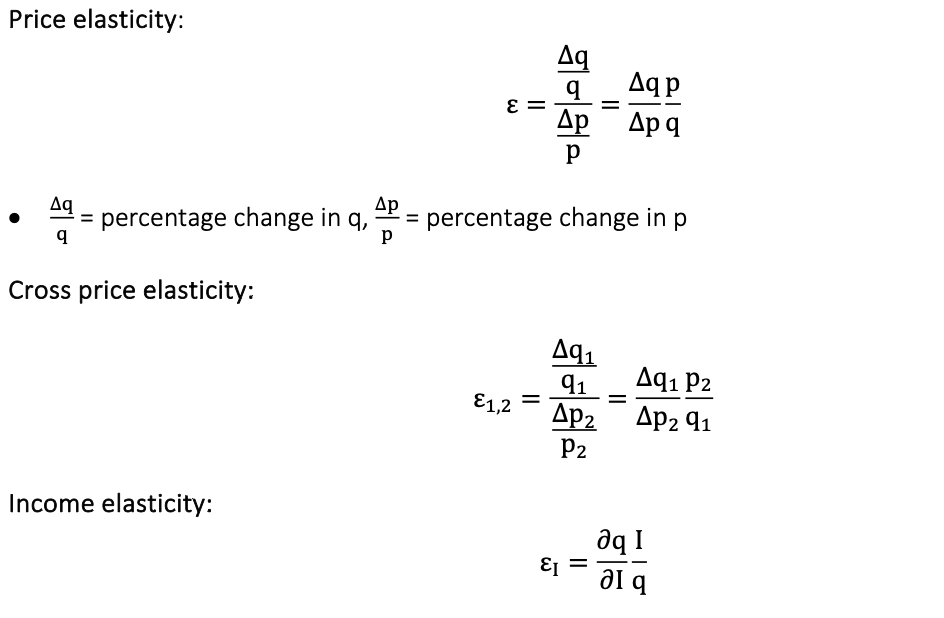

Through elasticities, which determine:

If demand/supply is inelastic, small price changes cause little behavioural change => smaller welfare loss

If elastic, small deviations from the benchmark can lead to large changes in quantity => potentially large welfare impacts (vulnerable groups)

=> elasticities tell us how much real-world harm or benefit arises when markets aren’t perfectly efficient.

what are the different types of elasticities?

Short run / Long run elasticities?

Short run elasticities:

A lot to do on the impact in the short run of spikes in prices

→ especially for low-income socio-economic groups that have low elasticity

• Long run elasticities:

Important for investment decisions

→ they affect the social returns of investing in the provision of the public service

→ users have higher elasticity over the long run than over the short run and a public company must adjust (like markets generally do)

• Think about an example: transportation (slide 35)

Define Income elasticity

= the effect of a 1% change in income on the relative variation of the quantity demanded by households

Income elasticity matters:

• EX: for developing countries, where entire blocks of the society become (relatively quickly) middle class

→ consumption changes with income: Normal goods ; Inferior goods

• Remember that elasticity is a reduced form of the change in demand w.r. to x (where X is usually price), however many factors play a role

(Age, Education, Lifestyle, Factors related to the product/service (e.g., substitutes and complements) etc..)

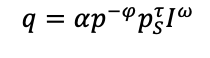

How is Price & Income Elasticity for D of public services estimated?

Empirics? Mostly, regulators and analysts estimate:

• Constant elasticity models, such as:

which can be linearized as: 𝑙𝑛(𝑞) = 𝛼 − 𝜔 𝑙𝑛(𝑝) + 𝜏 𝑙𝑛(𝑝.) + 𝜔𝑙𝑛 (𝐼)

• Non-constant elasticity models, such as: 𝑞 = 𝛼 − 𝜑𝑝 + 𝜏𝑝. + 𝜔𝐼

in this case, remember the difference between:

average marginal effect

marginal effect at the mean

marginal effect at a representative value

→ Approach provides a better sense of the changes in elasticities that take place as prices & incomes change (elasticity changes with the level of consumption)

what risks do regulators face when considering the production side?

Oversimplification of a potentially complex production problem (e.g., how to produce electricity?)

Failing to recognize that information gathering is limited/biased

Details on input matter → how are inputs selected and negotiated?

Technology matters → which technology and under what combination of factors?

Time matters → what if technology evolves rapidly?

Production efficiency can be measured/estimated (vast applied literature on that), but assessing the efficiency of a production technology can be quite hard, even for a well-intentioned regulator

→ cost benchmarking can be a second best (but still good) way to soften this problem

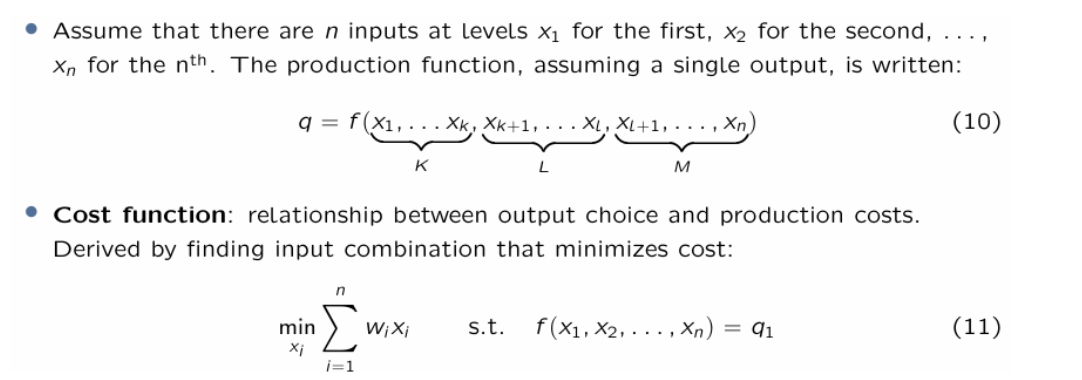

Define the production function (& cost production)

= Technical relationship between inputs & outputs

what causes DWL?

Deviations from the benchmark cause deadweight loss (DWL)

→ DWL w.r. to the ideal benchmark might come both from exploiting market power (and thus elasticity tells us about it), but also from failing to produce efficiently

→production function helps analysing this issue

what is an alternative to estimating production functions?

An alternative to estimating production functions is the cost function!

→ This option is particularly attractive for countries that have good accounting rules and practices (many developing countries do comparatively well on that)

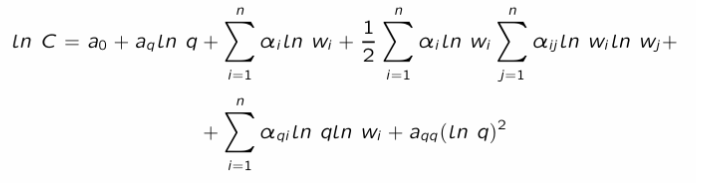

Classic examples of cost functions that are estimated are:

• Cobb-douglas (linearized)

• Translog (which allows for non-constant returns to scale):

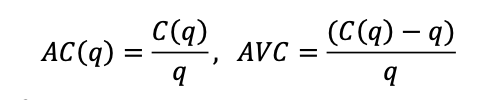

what 3 important quantities are emphasized in the analysis of the cost structure?

Total cost of producing q of output C(q) and which is the sum of:

the total variable cost

the fixed cost

Average cost

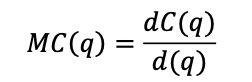

Marginal cost, which is cost of +1 unit

→ important for efficiency to work at the right scale

In decentralised markets, who determines entry decision?

Demand and cost structure (and many other factors) determine entry decision

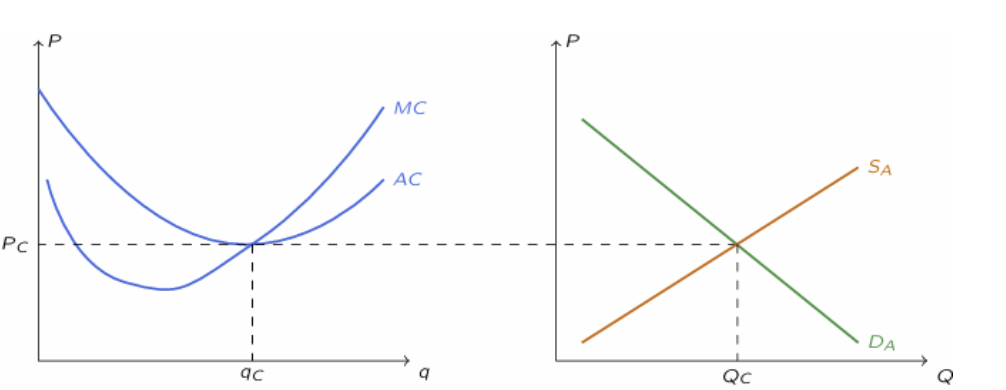

When a market is competitive and there is free entry, marginal cost is equal to average cost (MC = AC),

which correspond to the point where average cost is minimized

What is one of the main focus of regulators? It’s industries where:

Average cost of production is declining over a substantial range of output, so that the marginal cost is below the average cost until production capacity is almost at the maximum.

industries w/ large economies of scale where the fixed component is very relevant & generates an important entry barrier

2 broad types of monopolies?

Legal monopolies:

• An industry enjoying a legal barrier to entry in an activity, and for which there are no close substitutes

• Legal decision granting sole ownership of a resource or service to a specific actor

→Examples: Dutch East India Company in 17-18th centuries, alcohol in Sweden, cannabis in Uruguay, UEFA in European football, ...

Natural monopolies:

• An industry where a single firm can produce a desired output at a lower social cost than two or more firms

• Arise due to cost structure: high fixed costs and low marginal costs

• Common in public utilities (water, electricity, sanitation)

Note: If due to market power, not really to cost structures → competition policy more than regulation?

Bottom line: it is all about cost structures

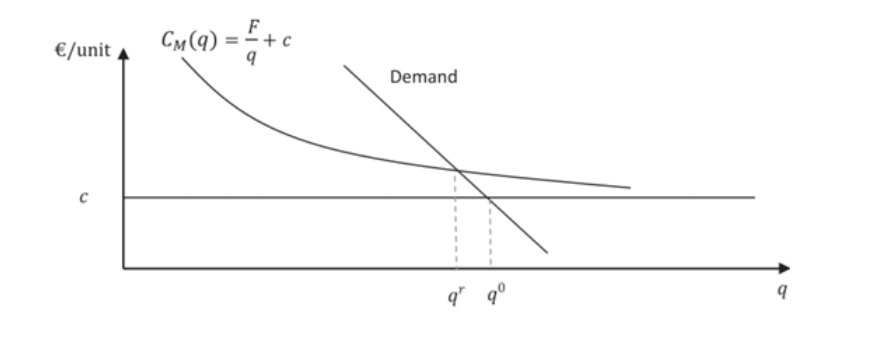

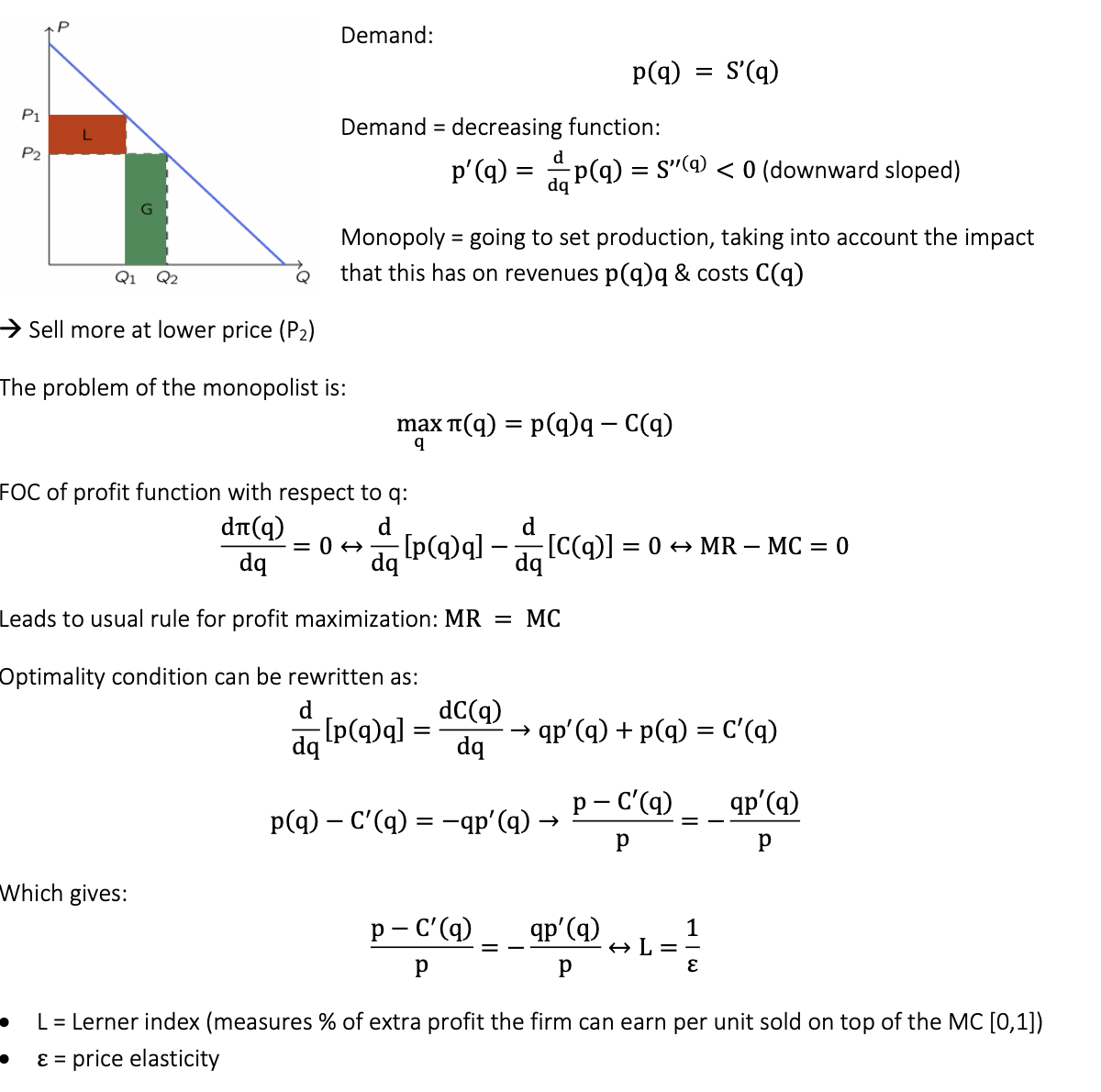

what is the problem of the monopolist?

· Monopolist maximizes profit where MR = MC; charges price from demand curve

· The size of the profit depends on the ATC

· Products or services requiring large investments can have relatively low marginal costs, but high average total costs

Why worry about natural monopolies if they are better than competition in terms of costs for specific industries?

If not regulated, it leads to other forms of inefficiencies:

• Insufficient production and excessive prices

• These problems offset the gains of declining average costs

→ Government worries because in a specific country/region/city/... there is underproduction or underconsumption of these goods and services

→ If we have economies of scale : regulators may want to have a look

Define economies of scale

Economies of scale: average costs falls with increasing output

Represented by the scale economy index:

What is the link between economies of scale and natural monopoly?

Economies of scale: Average costs fall as output increases (AC > MC).

If costs are subadditive, one firm can produce total output cheaper than multiple firms.

This implies a natural monopoly, where it's most efficient for a single firm to serve the market.

Link btw economies of scale and subadditivity

Economies of scale can lead to subadditivity, especially when average cost declines over a broad range of output. Why? Because combining production into one firm reduces the cost per unit, so total cost is lower.

Provide an example of a sector with little economies of scale (and small improvements) in the past and today, and another which had little economies of scale in the past but has dramatically changed in the last 20 years

Market structure is also affected by the presence of network externalities

Willingness to pay by a consumer increases as the number of current consumers increase, because utility from consumption increases when there are more current consumers

→ These markets are likely to contain a small number of firms even if there are limited economies of scale and scope

• Examples: Google, Facebook, telephones, fax

what is the traditional view of monopoly assessing?

To test whether we have a natural monopoly → need to assess the industry’s cost structure; But again demand side is crucial → for efficiency but most importantly, EQUITY issues

Monopolies are potentially good → if they can help cut costs because of scale economies

• Improve productive efficiency by ensuring there is no wasteful duplication of fixed costs without any technological benefits or innovations

Monopolies are potentially bad → if they are allowed to decide how much to produce and to charge, which leads to:

• Inefficient production and excessive prices allowing them to generate and capture economic rents

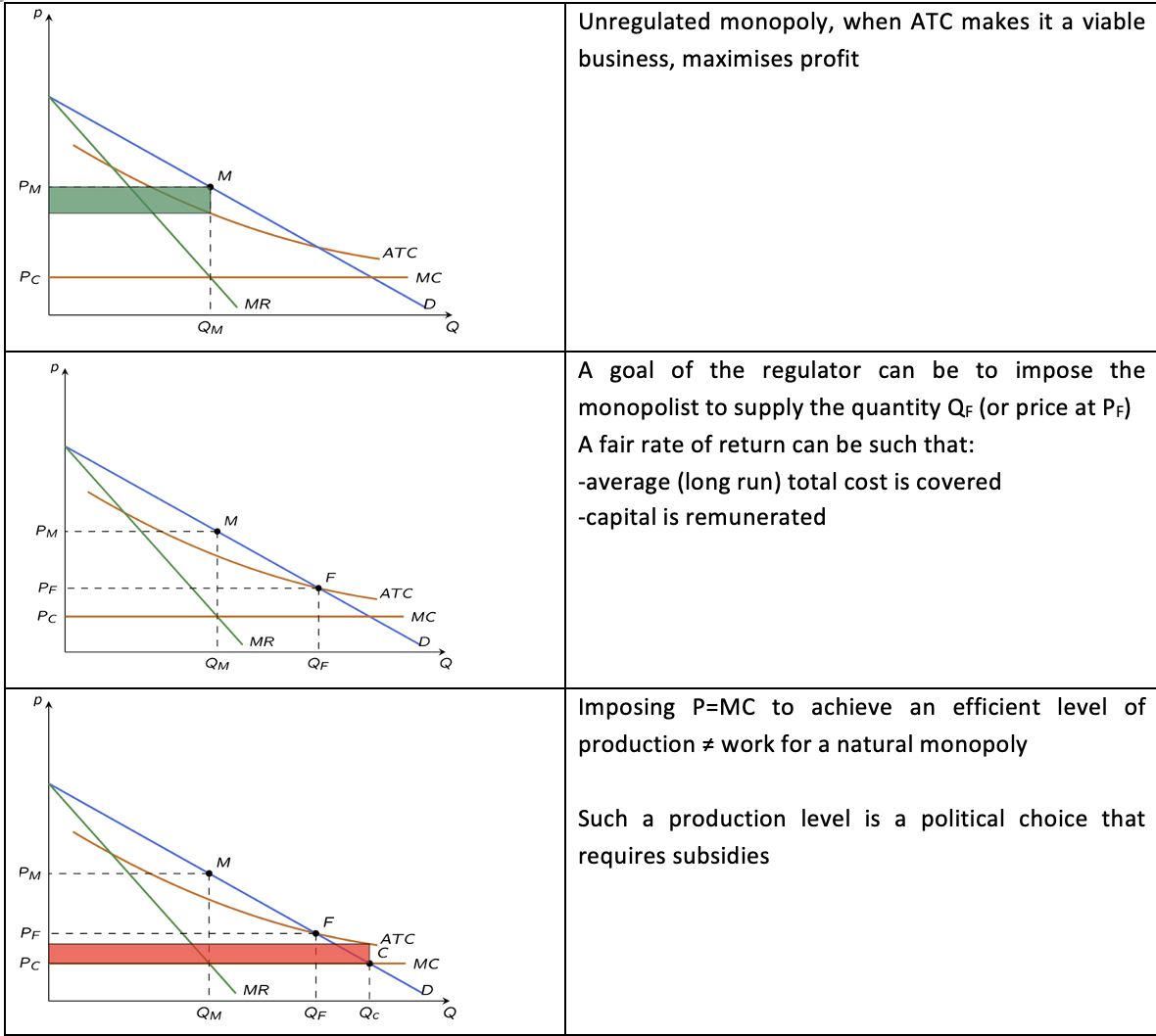

How can a government minimize the efficiency loss related to an unsupervised monopoly?

If technical or political reasons impose a (legal or natural) monopoly

Goal of the government:

• Produce as close as possible to an economically efficient level

• Charge as close as possible to a competitive price

Option 1: Keep the firm in the public sector (or nationalize) to align managers’ choices with users and voters’ preferences

Option 2: Regulate the firm to make sure it does not abuse its market power to increase prices and not meet the demand

Why did countries increase the role of private operators in regulated industries?

Technological and ideological changes → increase scope for competition in some segments of these industries...but keeping a non-competitive segment

e.g. electricity generation is competitive but you need to organize auctions for private operators to compete for the right to enjoy a temporary monopoly

Government failures → can be just as bad as market failures

→ Some evidence (open debate) that ownership is not what matters, rather competition and regulation; Focus of this course is not on ownership, but how to regulate

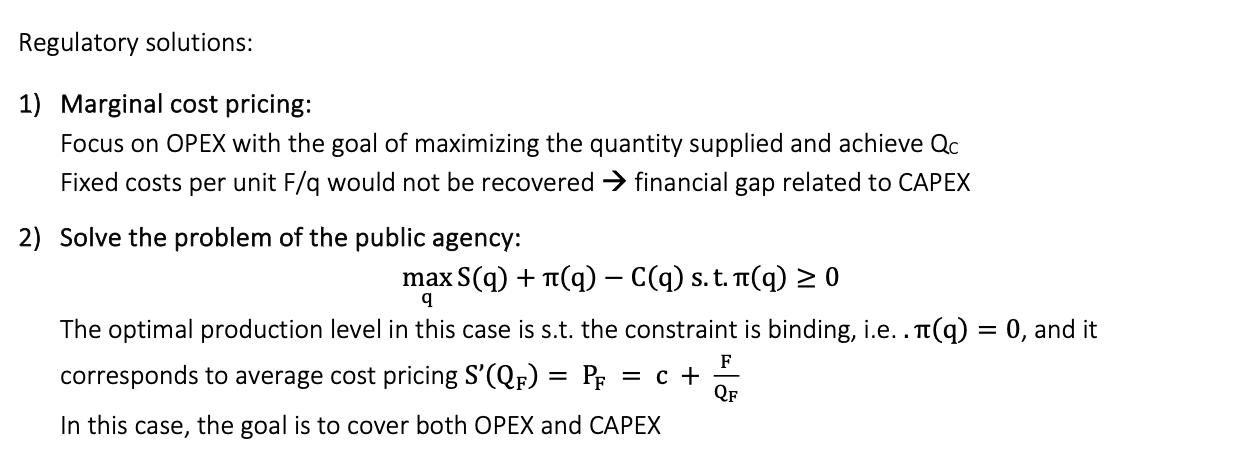

what are 2 obvious options for the regulator to allow the firm to break even?

to set P=MC then subsidise

to set P=AC(average costs)

What happens in practice for the firm to break even?

• The price determined by the regulator

→ allows the firm to obtain a fair rate of return (i.e. a return high enough to cover opportunity costs)

What price allows for this? Average cost pricing can be designed to lead to a fair return

• But the market is still not efficient and provides no incentive to monopolist to optimize capital use (Averch-Johnson effect: over-investment in capital)

how do economists think about distortions?

Compare the size of efficiency gains in monopolistic vs. competitive production:

→ measure the scope for scale economies

→ look at the size of the loss in production associated with poorly regulated or unregulated monopolies

→ measure by how much regulation would increase production and cut prices

→ compare the welfare gains from with and without regulation of the monopoly

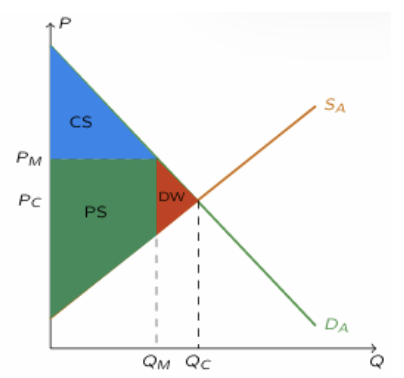

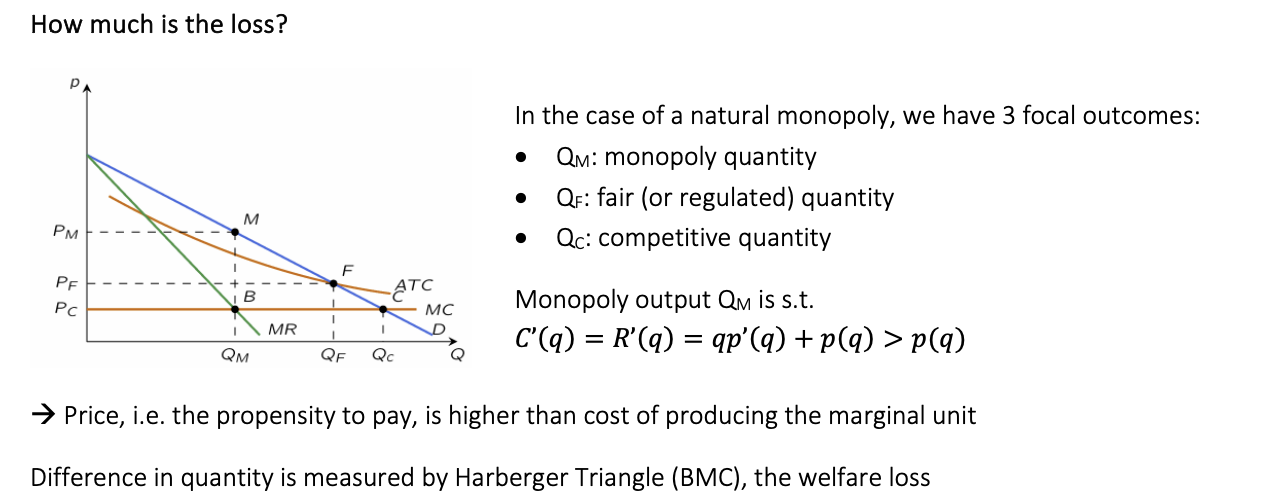

Define the deadweight loss of monopoly

The monopolist sets MR = MC to give output QM and price PM

Consumer surplus reduces but producer surplus increases

Total surplus reduces (deadweight loss of monopoly)

The monopolist produces less surplus than the competitive industry. There are mutually beneficial trades that do not take place: between QM and QC → Inefficiency

what do we need to measure the deadweight loss of monopoly?

The competition: we need to know at least marginal cost and demand

The monopoly: again, we need demand parameters and cost parameters

Then, we can estimate the DWL:

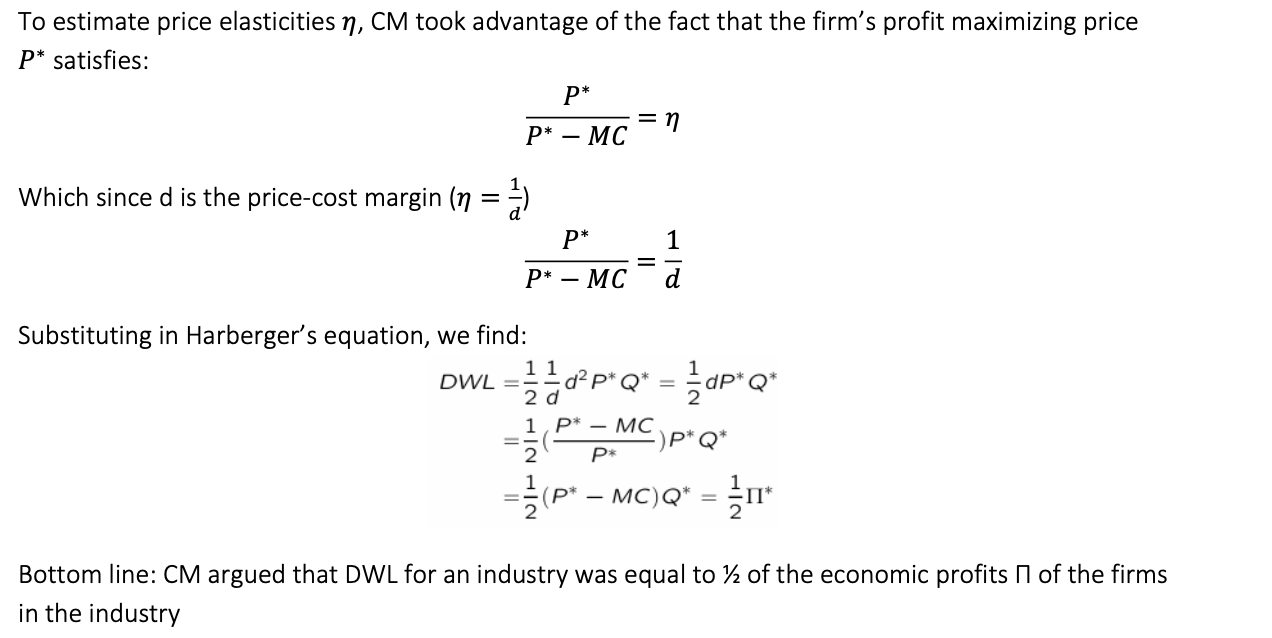

• Harberger’s approach: 𝐷𝑊𝐿 = ½ 𝜂𝑑 ² × 𝑃* × 𝑄*, where d is the price-cost margin 𝑑 = (P* - MC)/P*

→ Q* = the monopoly quantity, and 𝑃* is the monopoly price

• Cowling and Mueller’s approach: 𝐷𝑊𝐿 =½ Π, where Π are the industry economic profits

If the DWL is sufficiently large (or perceived as so): regulate

Note: in reality, the relevant counterfactual might be an oligopoly (see critique of CM and related literature)

Define Harbergers approach in more detail

The dead weight triangle can be approximated as follows:

𝐷𝑊𝐿 = ½ (𝑃M− 𝑃C )(𝑄C− 𝑄M) → 𝐷𝑊𝐿 =½ × 𝜂 × 𝑑2 × 𝑃∗ × 𝑄∗

Where 𝑃∗ = the monopoly price, 𝑄∗ = the monopoly output, 𝜂 is the price elasticity of demand, and d is the price-cost margin

𝑑 = (P* - MC) / P*

• To estimate d, Harberger measured the difference between rate of return for the industry & the average rate of return for all industries

• Harberger (original paper) assumed that, for all industries, 𝜂 = 1

Define Cowling & Mueller’s approach in more detail

How do economists and politicians opinions diverge on monopolies?

Economists and politicians dislike monopolies for different reasons

- Economists: the quantity is not enough!

- Politicians: the price is too high!

In principle, the solution to their concerns should converge: a lower price increases quantity

But in practice, it is not that simple:

- Economists would be happy to allow price discrimination to stimulate production and to push for competition

- Politicians prefer a single price, easier to manage politically, and not necessarily pushing for competition on the ownership of assets that support public services

These issues are very difficult to address in practice (more to come in following lectures)

what are ways in which the government can fail?

Lack of commitment of government and need to renegotiate

How do you deal with these risks? Early rules, separation of powers, sequential processes...

Multi-principal nature of government

In real life, multiple agencies interact with a regulated company on different dimensions (health, environment, economics)

→ If regulated activities are complements; risk or over-regulating!

→ If regulated activities are substitutes; risk or under-regulating due to regulatory competition!

Who has higher authority? Minister or regulator?

Discretion of political principal

Concerns the risk that short term political interests will threaten long-term commitments made to investors and consumers

When in doubt, theory suggests to design regulation so as to tie politicians’ hands

Discretion of regulator

What if a country or a sector has inherited excessive political regulation?

The key is to increase accountability!

→ Obligation to generate information which can be used to increase transparency

→Achieved through established, clear and transparent structures; accounting practices to check compliance with commitments; or simpler pricing rules

what are different actors involved in regulation? what are their objectives?

Regulation involves various actors with differing objectives:

• Regulated firms maximize profits

• Governments seek efficiency and equity

• Consumers aim to maximize net utility

• Regulators in principle benevolent referee, but with self-interest

• Taxpayers want minimize fiscal burdens that distort private profits

• Competing firms maximize their private profits

• Agencies have their own agendas (environmental agency, ministeries…)

what are the constraints of the regulator?

Regulators face constraints:

• Technological & economic

→ Cost & Preferences

• Legal

→ Privatization law, concession law, sector laws, antitrust laws, ...

→Contract design, including duration

→Accounting rules and reporting obligations.

• Institutional

→Who is involved, who decides, and how (e.g. price control, wage control, barriers to entry)

→Enforcement power

→Financing opportunities

• Informational

→ Imperfect by symmetric information

→ Asymmetric information: adverse selection, moral hazard

By pursuing his objectives, what trade-offs does the regulator have to balance?

Regulators must balance:

• Efficiency

→ Cost-reflective prices

→ Optimal investment

→ Minimizing production costs

• Fiscal & Financial viewpoints

→ Fiscal pay-off to the government

• Equity

→ Lowest possible price

→ Highest possible quality

→ Cheapest but well-targeted investments

• Votes

→ Consumers & taxpayers instrument to voice support / discontent

• Governance

→ Ensure accountability of all actors can be enforced

what is the setting of monopolies under full information?

In public services, natural monopolies arise from:

• Large fixed investments (F = large & MC = low)

Trade off, a regulator:

• Wants to exploit the scale economies

• Is worried of the monopoly’s market power

why is the time dimension important?

2 types of costs:

CAPEX = Capital expenditure: Long-term infrastructure investment

OPEX = Operational expenditure: Day-to-day operational & maintenance costs

→ The 2 depend on the scale of production/activity q (the larger scale, the larger CAPEX)

2 problems:

• What the monopoly optimally does in the long run: forecasting demand to set up the right scale

• What the monopoly optimally does in the short run: setting quantity/price for a given capacity

what should the regulator consider when deciding optimal investment in the LR?

Demand forecasts = fundamental for future cost-structure

Forecasts can be underestimating future demand

In many contexts capacity cannot be gradually increased as demand grows (e.g., adding one lane to a highway)

If capacity becomes too small, cost can raise substantially (e.g., social cost of congestion, maintenance of over-stressed infrastructure)

Forecasts can be largely overestimating future demand

In this case capacity = underused

Easy to happen (airports justified by under very optimistic forecasts on projected inflow of tourists) especially because:

Politicians might use exaggerated projections to justify projects that provide short term electoral returns

Private interests of the regulated entity can also distort projection upwards

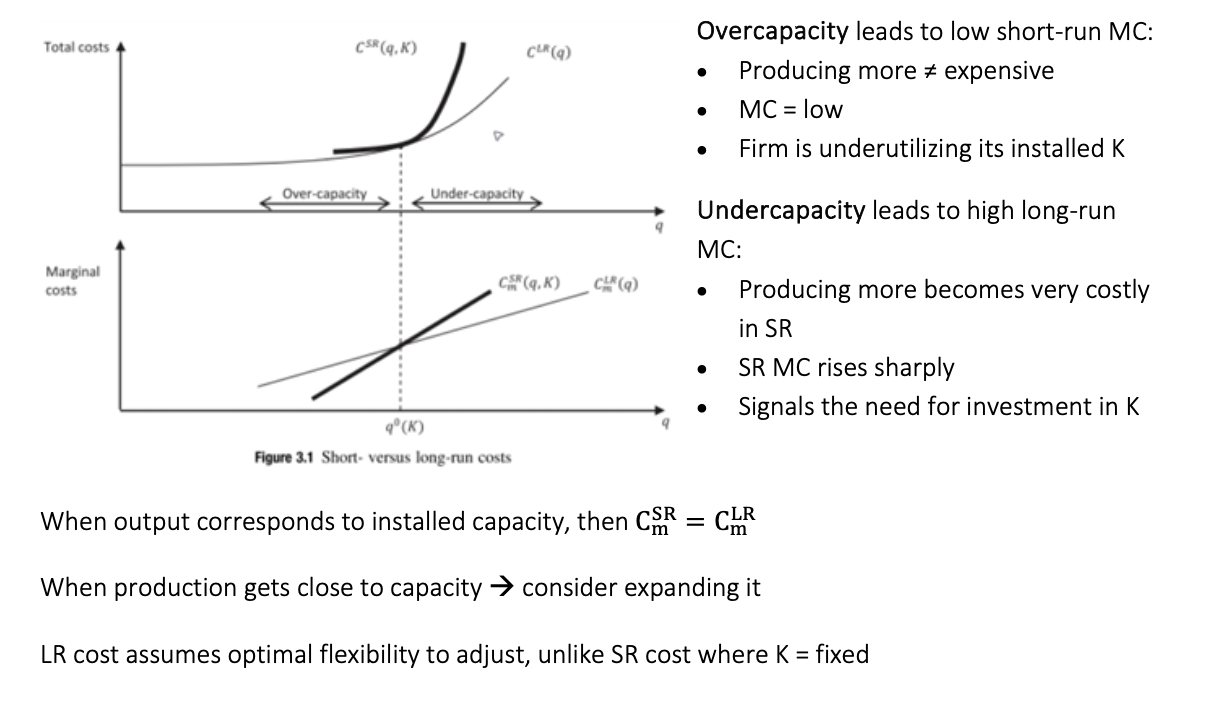

To what do overcapacity & Undercapacity lead?

the problem of the monopolist in the SR?

what are 3 conclusions that can be made from the Monopolist’s problem in SR?

Relevant information for the SR that the regulator needs has to do with demand & cost structure: p(q), C∞0(q),q, ε

Elasticity of demand is related to the markup, i.e. the price-cost margin, which we can measure with the Lerner index

Elasticity of demand reveals the actual ability of the monopoly to raise price over cost

How much is the loss of Monopolist in SR?

what are regulatory solutions to regulating natural monopolies?

what are the pros and cons to these solutions that rgeulators need to take into account (besides informational asymmetries)

Focusing on a very low price benefits consumers (a lot if elasticity is low) but can discourage investors and investments in the infrastructure and its technology depend on their expected returns, plus call for the taxpayer to fill the gap

Higher price reduces direct utility of users, but does not require the taxpayer to step in

Can we find a better solution than the two options PF and PC?

• Pricing ≠ have to be linear (e.g., think about water or electricity tarifs)

• Part of the tariff can be used to recover fixed costs and part (per unit) to charge for consumption (more on this in future class)

→ Or in presence of large economies of scale is not to pursue replicating competition in the market, but to set up competition for the market

what is the rationale for wanting to set up competition for the market, not replicating it?

A regulator can set up a procurement procedure to select a supplier (e.g., an auction where bidders offer output-price combinations)

Competition between potential suppliers can ensure that the most efficient can be selected

With good information on demand and costs, the regulator can select and monitor an efficient public service provide

What can be the pitfalls of such competition for the market?

• Frequency and size of lots to be auctioned have to be carefully assessed

• Projects can be hard to evaluate and complex, which makes the selection criteria of the auction multi-dimensional → auctions awarding a project based on lowest price are less & less adopted

• Risk of regulatory capture and corruption

• Renegotiations can ex-post have high impact on cost-efficiency

what is the goal of the regulator?

Regulator is benevolent and will need to arbitrate between three main goals:

• Efficiency

• Equity (how to trade-off between users and the regulated producer)

• Financial viability of the operation (how much to get the taxpayer to contribute)

In practice, it means to:

• Internalize the profitability constraint of the regulated firm

• Protect the interests of the consumers and the taxpayers

Even more in practice: for public firms, it boils down to deliver the service compatibly with a level of subsidies that is socially optimal (as they reflect the opportunity cost of spending public resources)

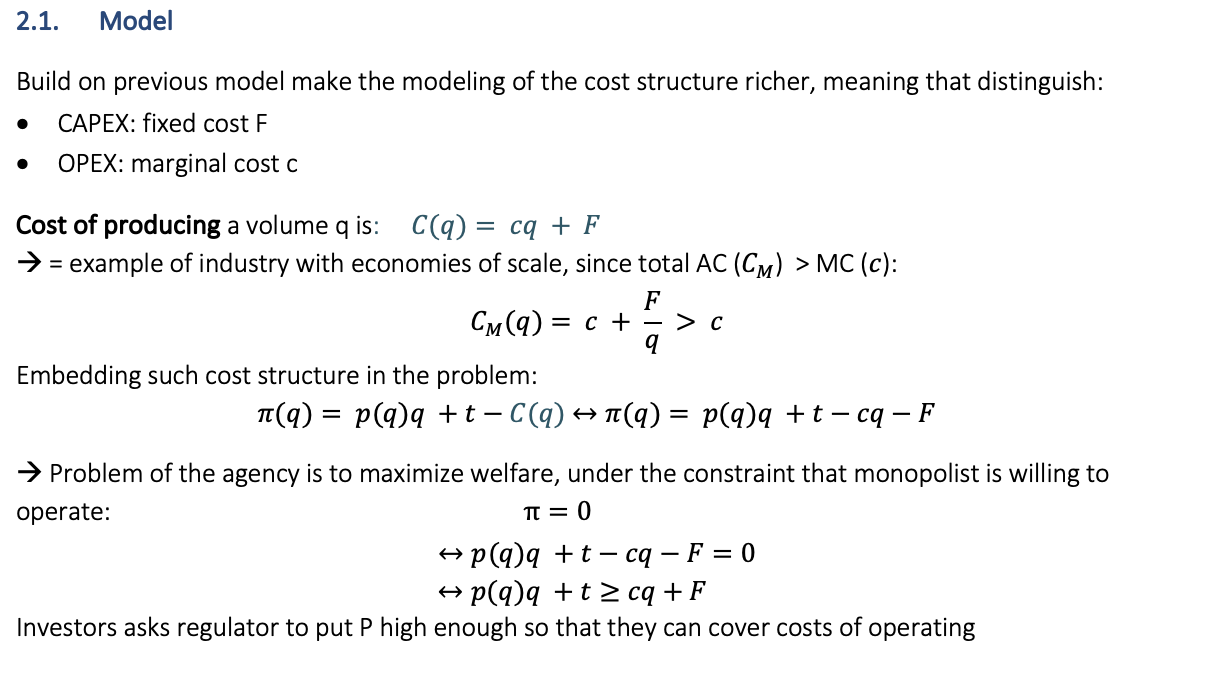

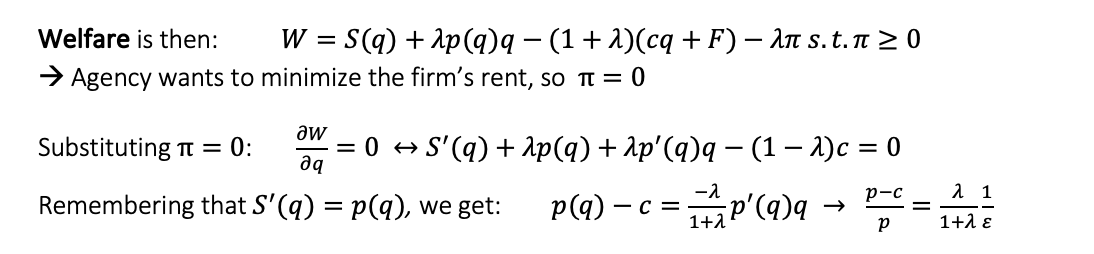

Model- Regulation under full information

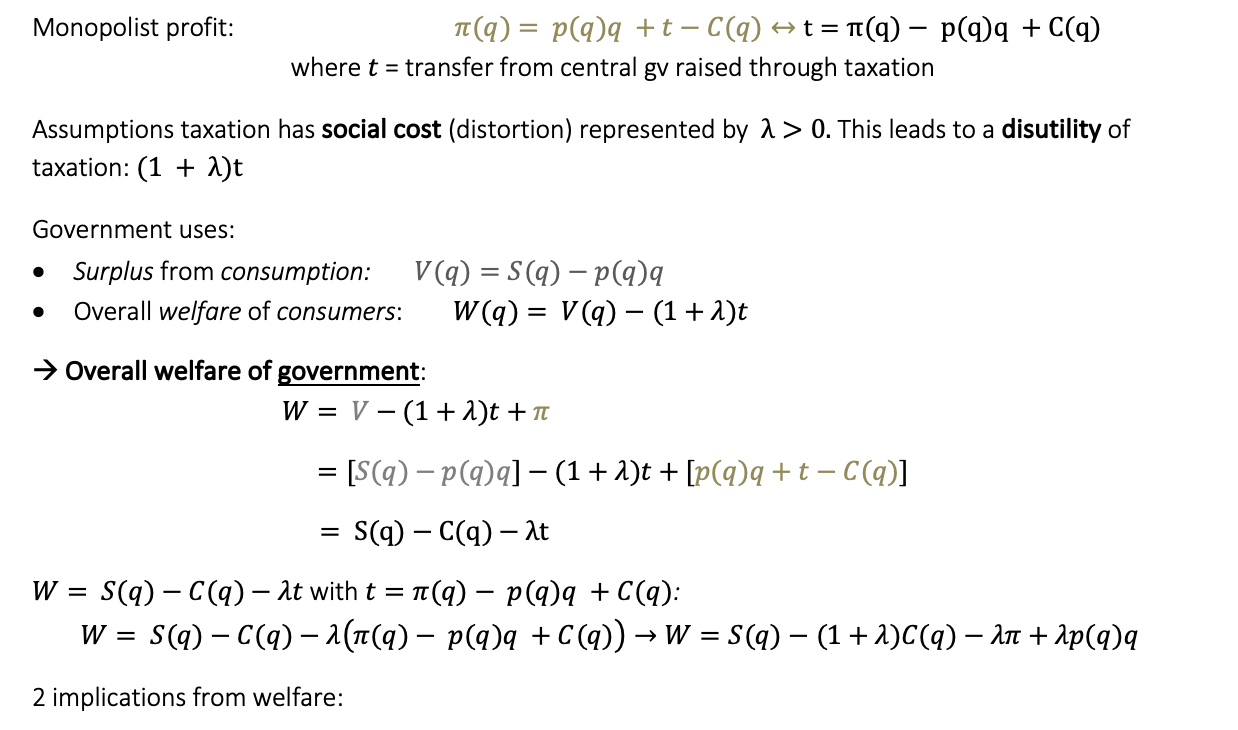

what are the 2 implications of this rewriting of π?

2 implications: W = S(q) − (1 + λ)C(q) − λπ + λp(q)q

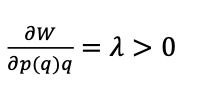

• Welfare increases in the revenues:

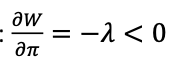

• Bad regulation (high prices or high subsidies), reduce welfare:

Interpretation of model- regulation under full information

Welfare increases revenues:

This is the controversial implication of the analysis, which stems from the fact that taxation is distortionary & from a purely efficiency standpoint (no weighting in the welfare function or equity considerations etc.) the government should refrain from financing the activity with subsidies but should rely on fees

Even more counter-intuitively (or politically palatable): the more taxation is inefficient and distortionary (e.g., developing countries) the more government should refrain from subsidizing a public service company

If instead a country raises taxes with little distortions, then the welfare loss is less of a concern & it is easier to justify public service provision on grounds not modeled in this analysis

Welfare decreases in bad regulation:

If the regulator, either through high subsidies or because it allows the regulated firm to make profit (reducing q or, equivalently, raising p exploiting its market power), then welfare decreases

This is much less controversial, as it clearly shows again that monopoly rents are welfare decreasing

what are the assumptions of Ideal regulation of private monopolies (Baron & Myerson)?

Key assumptions are:

• Welfare function weights everyone the same

• Other objectives of the government are not considered (e.g., environmental concerns)

• Full information

define the model of Ideal regulation of private monopolies '(Baron & Myerson)-PT.1

define the model of Ideal regulation of private monopolies '(Baron & Myerson)-PT.2

Interpretation of the Baron and Myerson Model

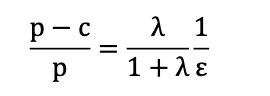

Called the Ramsey-Boiteux formula and is a way to set price in a regulated environment:

It links price cost margin to elasticity of demand & opportunity cost of public funds (their shadow price)

• If 𝛌 = 𝟎 (no distorsions):

Then p = c meaning the optimal price equals marginal cost. In this case, financing the service through public transfers t (another way is to say that taxpayers have 0 weight in the welfare function and all weight is on the users)

• If 𝛌 → ∞:

Then 𝛌 / 1+𝛌 → 𝟏 and the pricing rule converges to the unregulated monopoly price. The regulator avoids subsidies altogether, preferring users to bear the cost.

Depending on value of 𝛌, narrow approach to pricing may lead to underestimation or overestimation of the markup that would produce an optimal price

→ the higher 𝛌 is, the less incorrect the Lerner markup is for a given D elasticity

Bottom line: The Ramsey-Boiteux pricing rule ensures that the price-cost margin reflects both the elasticity of demand (to avoid inefficiencies in consumption) & the distortionary cost of raising public funds (to avoid excessive taxation).

Higher λ → higher markup allowed; higher elasticity → lower markup.

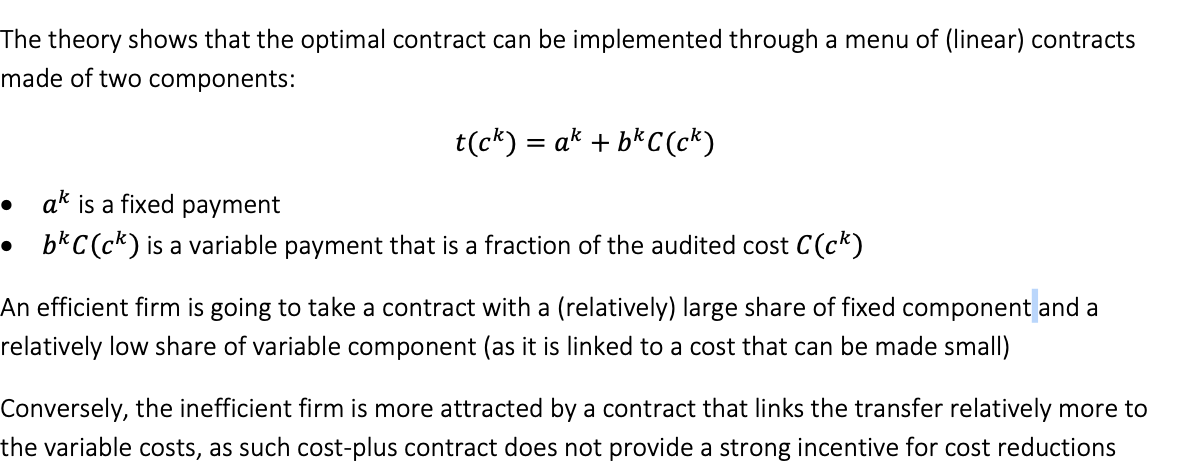

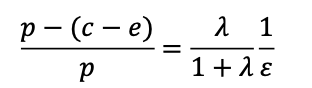

Unified framework to study the “Ideal” regulation of monopolies- Model Laffont -Tirole

Cost function is: C(q, e) = (c − e)q + F

where:

c is the usual cost that depends on the technology adopted

e is the cost that the firm can affect by adopting better operations/practices etc.

F is the usual fixed cost

The efforts to improve the efficiency of the firm generate a cost: Ψ(e) ≥ 0, such that Ψ′(e) > 0 and Ψ′′(e) > 0

Notice that e is not an accounting cost but an organisational cost, as it puts the firm under potential stress, the difference with c is relevant because dealing with c and e requires different approaches from regulatory perspectives:

c is about technology

e is about managers/incentives/practices/efforts etc.

Profit of the monopolist is thus: π = p(q)q − (c − e)q − F − Ψ(e) + t

Welfare function: W = S(q) − (c − e)q − F − Ψ(e) − λt s. t. π ≥ 0

Interpretation of the Laffont-Tirole Model

Analysis follows along the lines of Baron-Myerson:

dW/ dt = −𝜆 < 0: taxes have a social cost due to distortions

𝜋 = 0: constraint on profit is binding

Effort to reduce costs is set optimally: Ψ’(L) = q

which means that the planner (under full info) pushes the regulated firm to increase its effort to the point at which the marginal disutility of the effort = the marginal gain of producing q

Expression for the markup is:

which resembles Baron-Myerson apart from the expression of the marginal cost.

Insight is:

→ regulator (under full info) increases (optimally) the price-cost margin when it is harder to push down costs by the management

NOTE: this is the ideal benchmark under full info, but it’s evident the scope for asymmetric info playing a role here

Regulation under full information conclusions:

The users’ first best of : pricing at marginal cost, which requires subsidies → may create distortions

However, the need to finance OPEX and, importantly CAPEX, leads to a second best solution that maximizes welfare: the Ramsey-Boiteux pricing rule

Thus, the regulator can decide between various source of financing, all with pros and cons:

Subsidies

Higher markups

Capital markets (trade-off, high retruns for LT I)

New modern theory Introduction of independt agencies to supervise SOEs/regulated industries

information rent + implications

Regulator might know the social value of a public service BUT good info on the technology (present and future) DIFFICULT to have

The private information possessed by the regulated firms generates an information rent

→ paid either by the users or by the taxpayers, depending on the financing

→ impacts quality of services + fair prices

what are solutions to avoid rent information?

• Reward truthful reporting (i.e., partially give up and allow for some rent)

• Strict monitoring (potentially costly and not necessarily solving the problem)

what are caveats to the solution for avoiding rent information?

• It can be politically sensitive (the firm should just do its duty)

• We do not consider demand elasticity, this solution my not be feasible

• Solution to the previous problem could be to price at cost and subsidize, but this requires the political will

• Regulator might prefer to eliminate any contract designed for high-cost firms to force a low-cost operator to show up, but this can be a risky strategy (not just because of a strong discouragement, but also because of contract renegotiations)

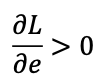

Adverse selection on the Baron-Myerson Model - Assumptions

Assumptions

• 2 types of firms, with low and high cost ci= {cl ch}, with cl < cp

• Surplus from q is S(q), and demand is S’(q) = p(q) which has an elasticity 𝜀

• Fixed cost F is the same for both firms

• Regulator knows cl & cp but does not know actual cost, only info is that the probability of cl is v

Adverse selection on the Baron-Myerson Model PT.1

Adverse selection on the Baron-Myerson Model PT.2

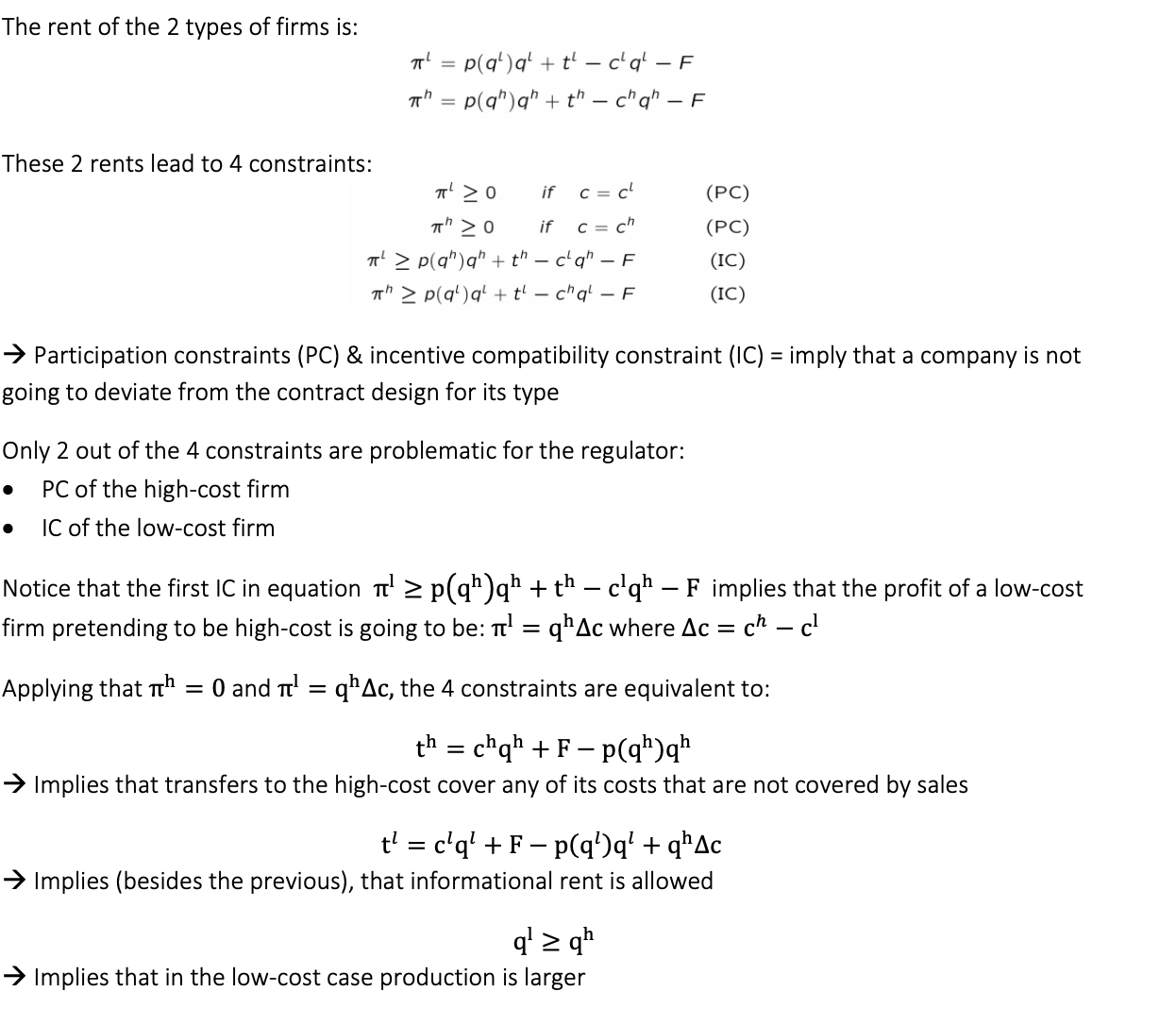

Interpretation of Adverse selection on the Baron-Myerson Model

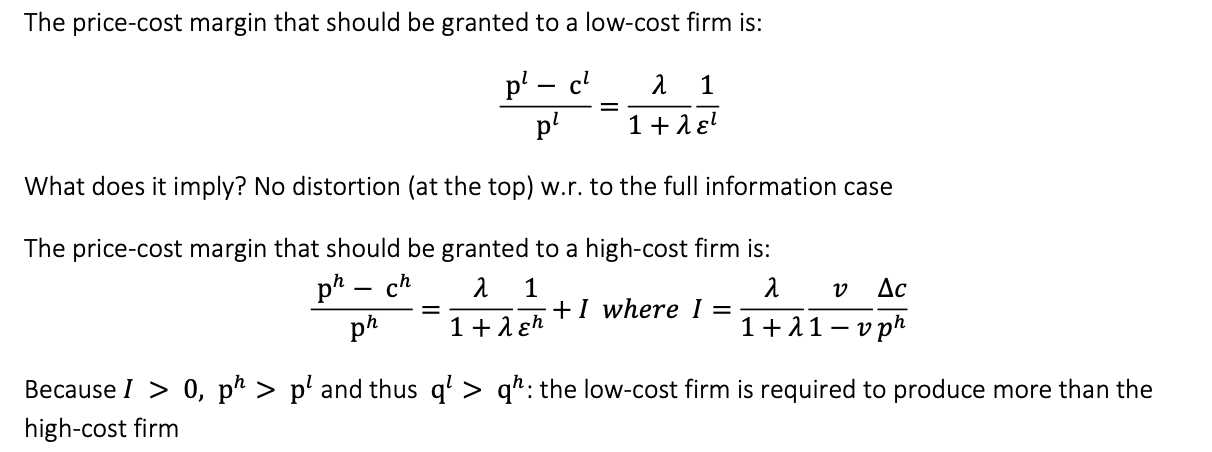

Optimal regulated quantity under symmetric (𝐪𝒉∗, 𝐪𝒍∗) & asymmetric information (𝐪𝒉, 𝐪𝒍)

why is the optimal design of incentives under AS controversial?

The optimal design of incentives under AS implies a rent for the most productive firm:

π(cL) = (cH− cL)qH > 0

However, the bright side of that is:

• The incentive is set for being productive, not the contrary

• There is no distortion in this case

Still, it’s hard for the public to accept regulators to let firms exploit an informational advantage and it’s difficult to quantify how much of the rent comes from good incentives & how much from poor analysis from the side of the regulator (or worse)

→ Because of the political pressure to undertake tough regulatory action, some regulators can be very strict and intrusive in auditing etc.

What do we mean by Regulation under moral hazard?

Problem of the regulator facing an ex-post informational disadvantage: Moral Hazard

→ What do we mean by that? Our full information model had 2 variables influencing marginal cost:

• c: cost that in inherent in the technology adopted etc.

• e: effort to reduce c by the management

Both depend on the choices of the management, but, at least in the short run, c is exogeneous while e(observable action) can be put in place to contain costs

Problem: the regulator has to figure out how much scope there is to contain costs and so how much effort the firm is putting on being efficient, i.e., we have a problem of moral hazard

→ In this case, the perspective is ex-post because generally regulators evaluate reported costs as they enter the reviewing process that defines transfers, future price setting etc.

Assumptions: Information asymmetry by Laffont-Tirole

Before instead the type of the firm was exogenous and the informational problem was only related to learning its type, now type depends on e

New Set of PCs & ICs have to satisfy:

Once again, the high-cost firm receives no rent

The low-cost firm will receive a rent to meet its IC

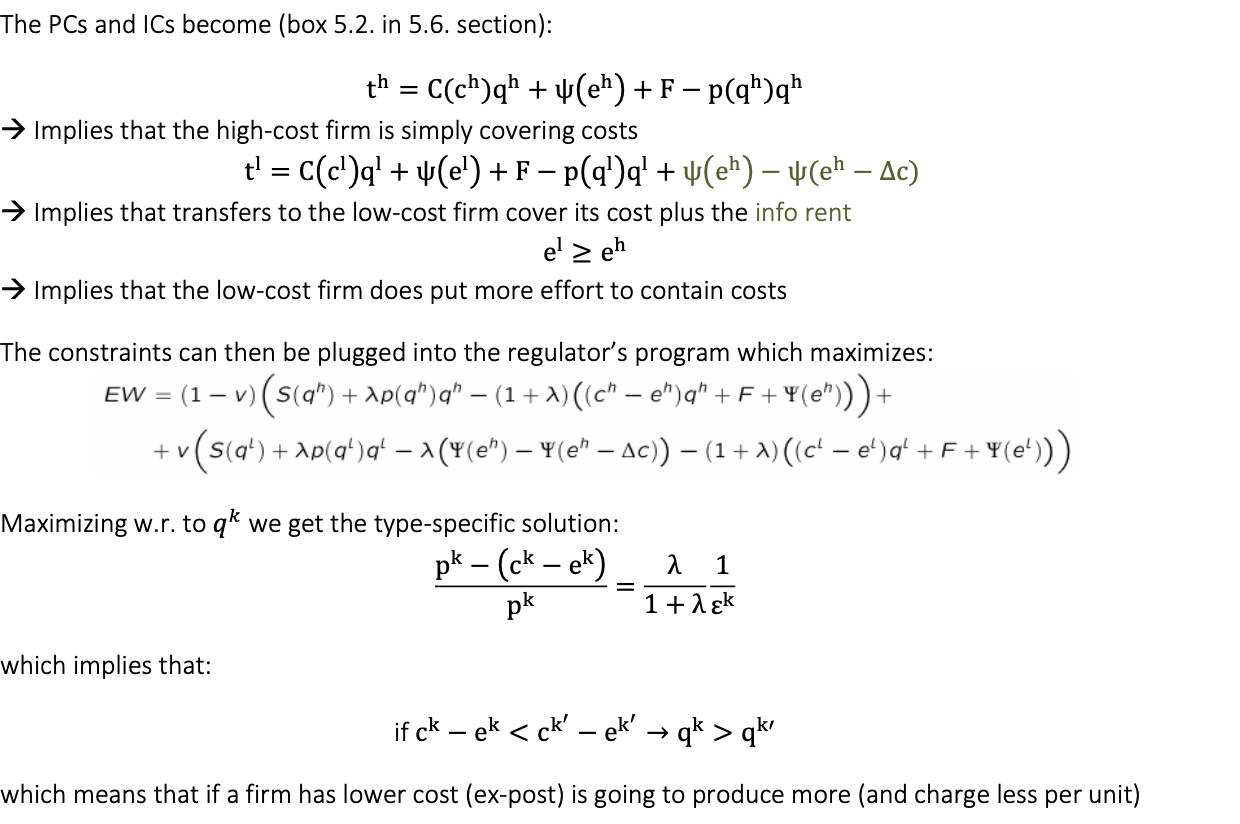

Model Information asymmetry by Laffont-Tirole

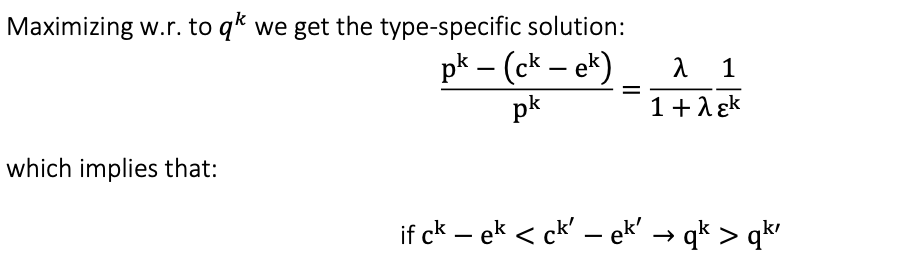

What are the main conclusions from Model MH by Laffont-Tirole?

which means that if a firm has lower cost (ex-post) is going to produce more (and charge less per unit)

The other key points of the solution are:

• No distortion at the top (again): Ψ’(el) = ql

• Distortion for the high-cost firm: Ψ’(eh) = qh - H « qh

→the low-cost firm exerts optimal effort to contain costs, and it produces the same quantity as in the full info benchmark, but in return it enjoys a profit (information rent)

→The high-cost firm exerts less effort than in the full info benchmark, produces less quantity and so final price is higher than in the benchmark

• Again, the information asymmetry generates a distortion which depends on v:

→ If v increases, then the rent increases: higher incentive to put effort in cost reduction (but also increases the distortion if the selected firm is high-cost)

→ If v gets too close to 1, then introducing a significant distortion does not pay anymore