S2 Topic C&D- Monetary Policy + The Foreign Exchange Market

1/46

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

47 Terms

What is money?

Money is any item that symbolises perceived value which facilitates the exchange of goods in an economy.

What are money’s three key functions?

Regardless of the exact item used as money - be it gold, currency or bank deposits (more on this later) – money fulfils three basic functions:

#1: It is a medium of exchange (money allows us to engage in exchanges with strangers we don’t know or trust! We thus get around the inconvenience of barter, decreases transaction costs as no need for double coincidence of wants)

#2: It is a store of value (money is a convenient way of holding value received from work, sales, trading etc. It allows us to purchase goods & services at later times and in different places)

#3: It is a unit of account (money is used for stating prices and recording transactions, thus forming the basis of record-keeping: profit and loss accounts, assets and liabilities, maintaining records of credit, etc.)

Explain perceived value

Crucially, money is only accepted as a medium of exchange if it is believed that others will also accept it (This has interesting implications for asset pricing – recall the “beliefs about beliefs” discussion from previous topics)

Therefore, high levels of inflation, for instance, are damaging because they erode confidence in money as a medium of exchange and create uncertainty

“Will merchants continue accepting my country’s currency if inflation is at 1000%?”

Of course, this erosion of confidence can have real effects as well – incentives to produce goods & services might be lowered, mutually-beneficial exchange hampered, etc.

Example: Hyperinflation in Post-war Germany

A natural question then follows: how is perceived value assigned to certain items (thus making them ‘money’) in the first place?

A couple of explanations:

#1 Authority: if governments require the use of a specific item as money for payment of taxes/government fees, then it is more likely to be accepted by people in that society

#2 Social custom: and here I have a question for you… ??

Explain Commodity Money

i.e., a real commodity is used as money

While gold and silver are the most well-known / obvious examples, plenty of items have been used as commodity money throughout history

Examples include sea shells, salt, silk, cocoa beans, tobacco and even tea

For instance, a so-called “tea brick” used as a form of currency in certain parts of China, Tibet, Mongolia etc.

Different qualities engraved with different designs were produced and valued accordingly

Regardless of the exact item used, a few characteristics determined whether the commodity would work effectively as money: durability, divisibility, portability, rarity.

Might explain why rare metals were a very popular choice.

Explain Fiat Money

Moving on, we have money which obtains its value by the declaration of government (i.e., a “fiat”)

Prince and kings, parliaments, dictators, etc.

Coins are one of the first examples of fiat money

And it’s not just about establishing perceived value - Fiat currency was a way for government to generate revenue / maintain power!

For example, the English penny was first introduced by King Offa around AD 785

When introduced, it was declared to contain 0.067 ounces of pure silver per coin, whereas in reality it had around 0.053 ounces

Then, a merchant say selling wool and bringing back silver bullion for coinage would lose out on 0.067 – 0.053 = 0.014 of silver per ounce (this amount, the difference, is called 'seignorage' and was profit for the king

Explain Bank Money

Nowadays, bank money – i.e., the “electronic” deposits people hold at commercial banks – is by far the most common form of money

From the Bank of England’s website: 96% of money is held electronically, only 4% is held physically as cash.

Explain Commercial Banking and Money Creation

The role of banks is highly multifaceted when you get into the nitty gritty of it all, but at their core, commercial banks do two key very straightforward things:

Commercial banks accept deposits from the public and give loans to their clients to finance consumption and investment

Now, when it comes to the role of commercial banks in bank money creation, commercial banks can just… create money

And I know this sounds a bit weird, but think about what happens when a commercial bank makes a loan to its client: When a commercial bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money!

Bank money is debt.

In essence, by making a loan to a client, two things happen:

(1) The client owes the bank money (there’s an asset on the bank’s balance sheet)

(2) The bank owes the client money (there’s a liability on the bank’s balance sheet)

If banks can just create money by making out new loans, why don’t banks just expand infinitely by making out an unlimited number of loans (i.e., by creating more and more money)?

#1: No demand for loans – if no one wants to borrow (at a given interest rate – and we’ll come back to interest rates next time), you cannot make new loans

#2: Regulation – banks may not be allowed by regulation to make excessive loans; they might have to comply with liquidity and capital requirements

#3: Risk – loans are inherently risky, they might not be paid back; if a bank starts making lower quality loans for the sake of making more loans… depositors may become very weary of that bank, which can lead to disastrous consequences such as bank runs

Interest rates – which are mainly under the control of central banks – have a great effect on the money creation process, as they influence both the profitability and riskiness of loans.

Explain risk and the role of financial market

A useful way of thinking about financial markets is as markets of information

For economic activity to flourish, funding needs to be allocated efficiently to sound businesses

But many overly-ambitious entrepreneurs (or outright crooks) are out there, promising the earth, moon and stars to obtain funding

Distinguishing between sound and reckless businesses is difficult, however, because of information asymmetries: in particular, moral hazard and adverse selection (which we will discuss at length in the workshop!)

The role of financial intermediaries such as banks is to reduce these asymmetries!

Well-functioning financial markets serve to reduce information asymmetries in the allocation of credit. Via screening and monitoring, financial institutions aim to address adverse selection and moral hazard. Therefore, they allow funding to be allocated to its most efficient uses.

Of course, banks do not “cure” these risks! Banks can still make out bad loans on which clients end up defaulting.

Importantly, this is more likely to be the case when interest rates are high – why? Because higher interest rates inherently attract riskier businesses.

As we shall see next time, interest rates are therefore an important tool which central banks can use to stimulate / cool down the economy.

What is the problem with high levels of inflation?

Money is only valuable as long as perceived value is attached to it

High levels of inflation can therefore erode trust in the system, which is why maintaining monetary stability (i.e., low-ish inflation) is the key mission of most central banks around the world:

This is also why central bank independence is argued to be key – otherwise, political pressures might be too great

What are interbank loans?

In addition to client loans, commercial banks can keep their money as reserves at the central bank or make out (short-term) lending to governments or other banks in the interbank money market.

Why do banks need to bother with interbank payments? Why would they take loans from other banks?

Suppose client A of HSBC makes a £1 transfer to another client of HSBC, client B. What happens to HSBC’s balance sheet?

Nothing happens - payment, so HSBC loses £1 in deposits but then immediately gains it back – no settlement needed!

What if, however, we have an interbank payment, with client C of HSBC making a £1 payment to client D of Barclays. What happens to HSBC’s balance sheet in this case?

Well, the first thing that happens is obviously a reduction in HSBC’s deposits, as £1 was taken out.

This cannot be the end of the story, however, since assets and liabilities are no longer balanced out now!

So, what ends up happening – in first instance – is that the reserves of HSBC also decrease by 1! Why? Because HSBC transfers £1 of reserves to Barclays

What is the problem with this?

If HSBC faces too many transfer requests, it risks running low / out of reserves, which is very, very, very bad!

Having few reserves is equivalent to having very low liquidity: you might start struggling to meet withdrawal / transfer requests and your clients might start becoming very weary, potentially leading to reputation hits and a bank run.

What can HSBC do about this?

Option 1: It can sell one of its assets, typically short-term government bonds (or loans in the money market) and use the revenue to replenish reserves

Option 2: It can borrow from the interbank money market (i.e., from another commercial bank) and use that amount to replenish its reserves

Interbank payments are initially funded with a reduction in reserves, which banks want to replenish. Reserves can be replenished either by liquidating securities or via short-term borrowing in the interbank money market.

Technical details: Handling small vs. large payments

Many payments between banks are quite small and do not have to be settled immediately.

Generally, banks batch up many such “retail payments” and then do a net settlement (i.e., the sum of all the positive and negative settlements between banks) with a single payment known as “Net Deferred Settlement”

When handling large payments (>£100mn. or so), as these involve lots of risk, the central bank may help with immediate settlement schemes known as “Real Time Gross Settlements Schemes” (RTGSS) E.g., CHAPS in the UK; Target 2 in the Euro Area, Fedwire in the US

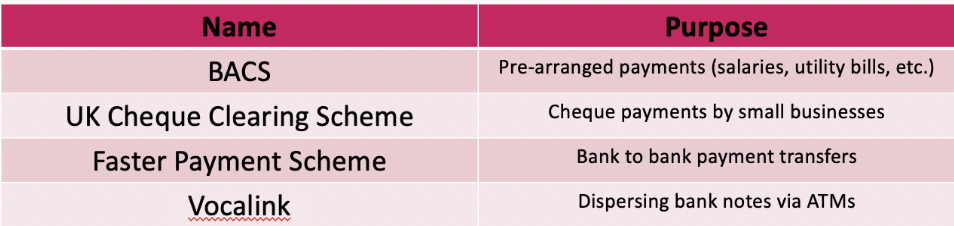

Technical details: Payment scheme examples

Different methods of payment (with different fee structures) are used depending on who pays who – here are some UK examples:

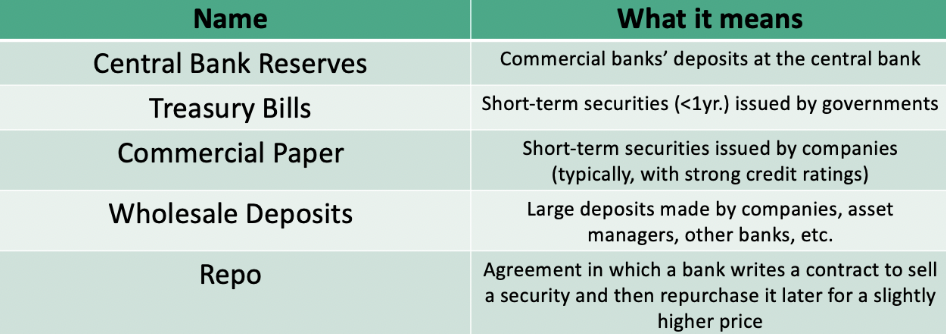

Technical details: Money market instruments

What is the role of the central bank?

Essentially, the central bank can cut interest rates via “expansionary policy” to stimulate growth OR it can increase interest rates via “contractionary policy” to help fight inflation.

As mentioned earlier, the central bank is the “bank of banks”: its main role is to provide reserves to commercial banks which, are needed by commercial banks to make interbank payments

Stretching the intuition a bit, banks use reserves similarly to how households use notes / coin / debit / credit cards to pay businesses!

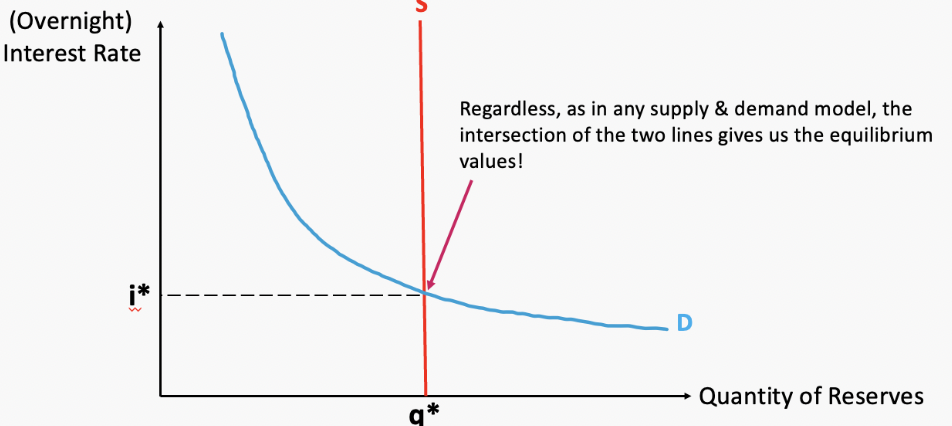

In practice, the policy of providing reserves to (or taking reserves from) commercial banks is known as an open-market operation (OMOs).

And it is best illustrated with a simple supply & demand graph; note: if you understand this graph and are able to explain it intuitively, you basically understand monetary policy!

Graph

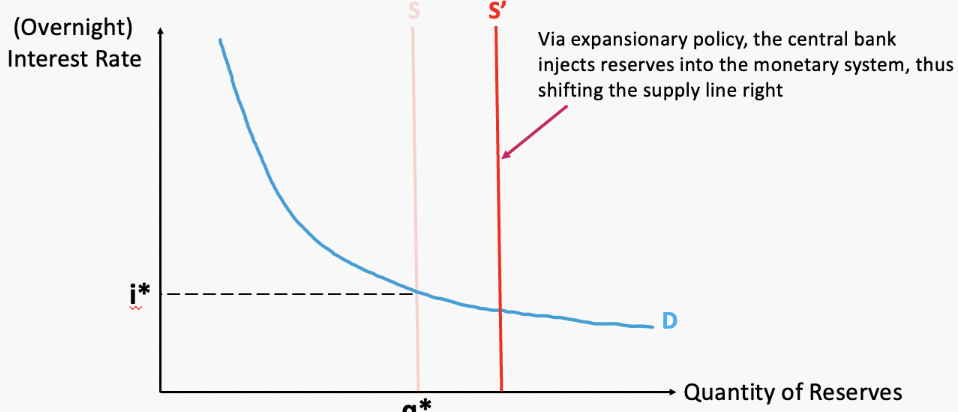

Via expansionary policy, the central bank injects reserves into the monetary system, thus shifting the supply line right

Given this change, the old interest rate i* is no longer the equilibrium value; why?

Because at the old interest rate, we have excess supply of reserves! I.e., banks just have too much liquidity / cash on hand.

Buying bonds raises their price and lowers the yield / interest rate, however, which increases demand for reserves since the opportunity cost falls!

Eventually, we arrive at a lower interest rate where demand is again equal to supply!

What are the key points

The central bank controls overnight money market interest rates via monetary policy

Banks can create new money via lending, but this must be funded in money markets

Therefore, loosening monetary policy reduces the cost of borrowing, increases liquidity and therefore allows more loans to be made

Correspondingly, tightening monetary policy increases the cost of borrowing, lowers liquidity and therefore allows fewer loans to be made

How do central banks increase / decrease the supply of reserves concretely?

Option #1 (Permanent): Outright purchases/sales of securities (OMOs in the strict sense) - the central bank buys or sells and the transaction is done.

Option #2 (Temporary): Repo/reverse repo agreements - the central bank injects or drains reserves but the operation automatically reverses on a set date.

Is there a limit to policy effectiveness?

YES – conventional expansionary policy can only get you so far… at some point, interest rates cannot be pushed further down – something known as the “zero lower bound”

In this case, alternative policies such as Quantitative Easing need to be employed, something you’ll explore in Topic F next Semester

TOPIC D

What is an exchange rate?

The price of one currency in terms of another.

Can appreciate (go up) and depreciate (go down)

Keep in mind that most transactions in the foreign exchange market are not between currencies directly, but rather between bank deposits denominated in different currencies

What are the two different types of exchange rates?

Spot Exchange Rates = immediate / short-run exchange of bank deposits

Forward Exchange Rates = the exchange of bank deposits at some specified future date

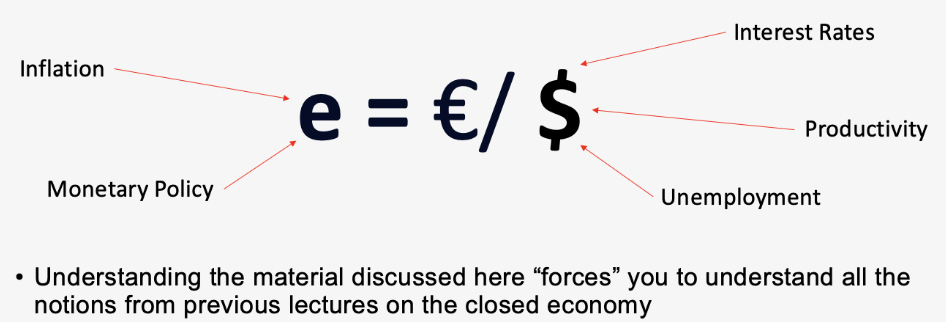

Why do we care about exchange rates?

Reason 1: image attached

Reason 2: Changes in the exchange rate have important trade implications, and trade is a main determinant of economic growth. Generally, a currency appreciation hurts exports & benefits imports.Conversely, a currency depreciation hurts imports & benefits exports.

Reason 3: Foreign exchange illiteracy is often exploited by the politicians and media

What is arbitrage profit?

If two countries produce an identical good, and transportation costs and trade barriers are very low, the price of the good should be the same throughout the world no matter which country produces it.

Otherwise, we have opportunities for arbitrage profit - importing a good from a country where it is produced cheaper, and selling it for the higher price in home country.

What does the Law of one price tell us?

The same good should sell for the same price everywhere (after accounting for exchange rates and transport costs).

What does PPP tell us?

The PPP tells us that, in the long-run, exchange rates adjust to reflect changes in relative price levels between the domestic and foreign countries.

Example: PUS = $100; PFR = € 80 and e = 0.8 € /$ (no arbitrage)

What happens if, say, costs of production fall in France such that PFR = €50? How would the exchange rate change?

Again, it’s all about supply & demand!

Converted to dollars, goods are much cheaper in France now: 50/0.8 = $62.5

We buy in France, sell in the US

This puts downwards pressure on the dollar’s value, which will depreciate until the new exchange rate of e = € 0.5/$

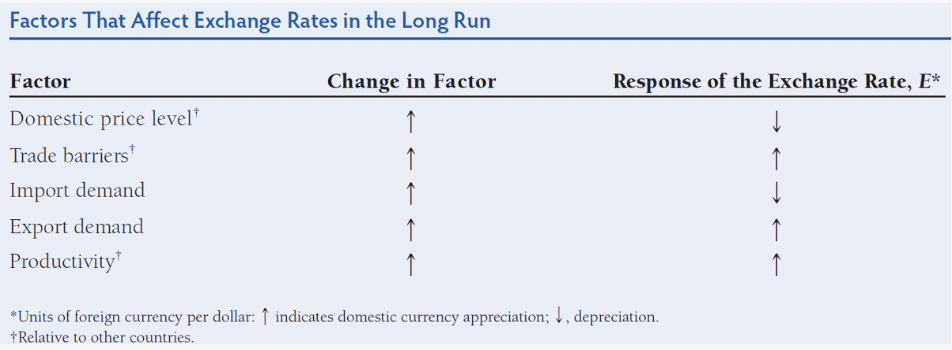

What factors affect exchange rates in the long run?

What factors affect exchange rates in the short run?

When talking about the short-run, we need to introduce the key concept of capital flows.

Like in our long-run discussion, we have agents who must decide whether to invest their money either domestically or abroad.

This time, however, instead of goods such as phones, we’re deciding between domestic or foreign financial assets

E.g., governmental bonds, stocks, bank deposits and so on.

Hence, interest rates play a key role in this decision and therefore have important effects on the short-run exchange rate.

What is interest rate parity?

Interest rate parity is basically the law of one price applied to money/investments across countries.

It says: You shouldn't be able to earn more by investing in one currency vs. another, once you account for exchange rate changes.

Simple example:

US interest rate: 2%

UK interest rate: 5%

"Why not just move all your money to the UK and earn 5%?" - Because the pound is expected to depreciate by roughly 3% against the dollar over that period, wiping out the extra return.

So the higher interest rate in the UK is offset by the expected weakening of its currency. In the end, you earn the same either way.

The arbitrage logic is the same as the law of one price - if a true riskless profit existed from moving money between currencies, traders would flood that trade until exchange rates and interest rates adjusted to eliminate it.

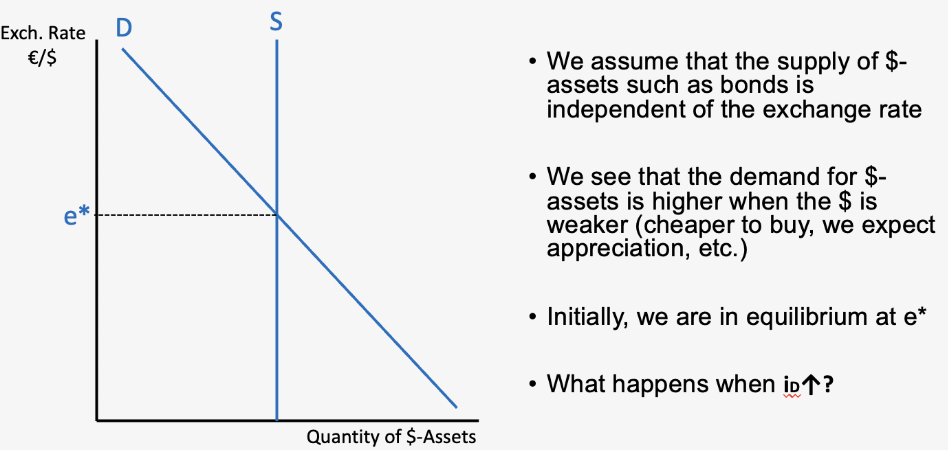

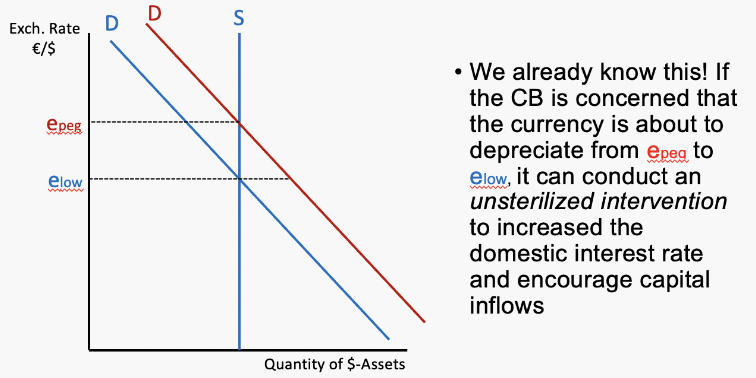

What happens when iD rises?

The setup: the y-axis is the exchange rate (€/$), so a higher value = stronger dollar. Supply of $-assets is fixed (vertical line). Demand slopes down because when the dollar is already strong/expensive, fewer people want to buy dollar assets.

When the US raises interest rates, dollar assets become more attractive - better return for the same risk. So foreign investors rush in to buy dollar assets (capital inflows). This shifts the demand curve right, pushing e* up from e** to a new higher equilibrium. The dollar appreciates.

Why does the opposite happen when i_F ↑? Because now foreign assets become more attractive. Investors sell dollar assets and buy foreign ones instead, capital outflows, demand for $-assets shifts left, and the dollar depreciates.

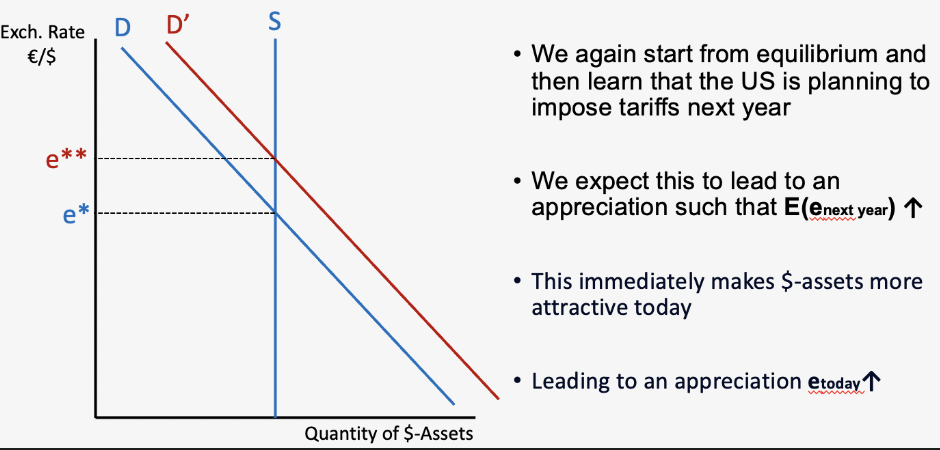

The role of expectations: tariffs next year

This is the more subtle and interesting point. You don't need anything to actually happen today - just the expectation of future appreciation is enough to cause appreciation right now.

The logic: news breaks that the US will impose tariffs next year. From long-run analysis, tariffs → stronger dollar eventually. So investors think "the dollar will be worth more next year." That makes dollar assets attractive today — why invest in euros if you expect to lose on the exchange rate when converting back? So capital flows in now, demand shifts right (D → D'), and the dollar appreciates immediately, even though the tariffs haven't happened yet.

Why do we care about exchange rate interventions?

Reason #1: Last time, we looked at the basics of how the forex market worked and linked exchange rates to policies (e.g., interest rate changes, trade barriers, etc.)

…but these policy changes (a.k.a. “interventions”) don’t just happen out of the blue! Instead, they are decided by institutions with lots of influence such as central banks or governments

We need to look at these interventions to develop a robust understanding of foreign exchange

Reason #2: Since learning how to evaluate economic policy is a major objective of this module, questions relating to foreign exchange interventions often feature in the exam

Central bank interventions in the Forex Market: Say we’re the US Federal Reserve and we believe that the dollar nowadays is too weak – what can we do?

We want to boost the dollar’s scarcity in order to increase its value

To understand how this is done, we need to introduce the concept of international reserves (a term you’ll hear very often in the media and future modules)

Simply put, international reserves are foreign-currency denominated assets on the balance sheets of central banks E.g., €-denominated French bonds owned by the US Federal Reserve

To strengthen the $, the Fed can sell its international reserves (e.g., to other banks, investors) in exchange for $

Why does this work? Higher $ scarcity

How can forex interventions be depicted?

Using T-accounts, simplified balance sheets only listing changes in assets & liabilities from an initial balance sheet position

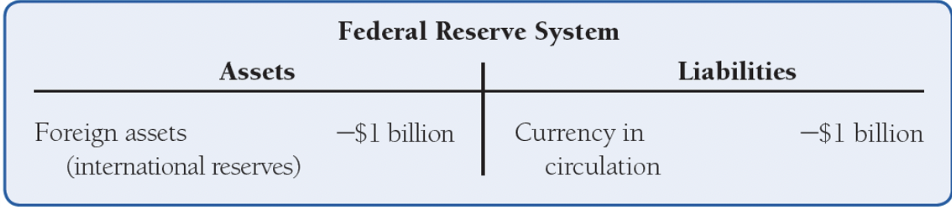

E.g., if the Fed sells $1b. worth of international reserves, the T-account looks like this:

Explain the mechanism for if the dollar is too weak

The Fed sells international reserves (I.R.) - think foreign currencies or foreign assets it holds - in exchange for dollars. This is the intervention.

This triggers a chain reaction:

MB decreases - by buying dollars back, the Fed is pulling dollars out of circulation, shrinking the monetary base

i_US rises - less money supply → tighter money market → higher interest rates (as we'd expect from contractionary monetary policy)

Capital inflows - higher US rates make dollar assets more attractive, so foreign investors buy them

Dollar appreciates - demand for $-assets shifts right (D → D'), pushing the exchange rate up from e* to e**

![<p>The Fed sells international reserves (I.R.) - think foreign currencies or foreign assets it holds - in exchange for dollars. This is the intervention.</p><p class="font-claude-response-body break-words whitespace-normal leading-[1.7]">This triggers a chain reaction:</p><ol><li><p>MB decreases - by buying dollars back, the Fed is pulling dollars out of circulation, shrinking the monetary base</p></li><li><p>i_US rises - less money supply → tighter money market → higher interest rates (as we'd expect from contractionary monetary policy)</p></li><li><p>Capital inflows - higher US rates make dollar assets more attractive, so foreign investors buy them</p></li><li><p>Dollar appreciates - demand for $-assets shifts right (D → D'), pushing the exchange rate up from e* to e**</p></li></ol><p></p>](https://assets.knowt.com/user-attachments/171a9c5d-dfe6-4165-aabb-6f13110e02d2.png)

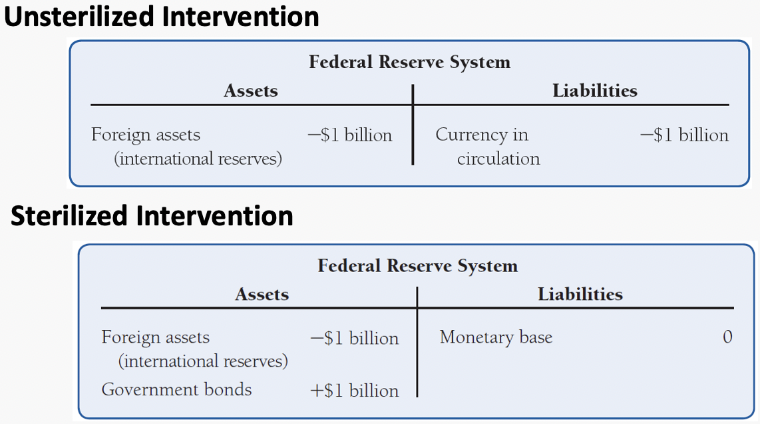

Explain Sterilized vs Unsterilized interventions

When a central bank’s intervention affects the exchange rate, we call that an unsterilized intervention

(Unsterilized interventions are the focus of this course)

Occasionally, however, central banks want to change their asset composition without affecting the exchange rate

In that case, we have sterilized interventions

E.g., in the example discussed previously, if the Fed wants to sell $1b. worth of international reserves without appreciating the $, it can conduct an offsetting operation whereby it purchases $1b. worth of US government bonds – remember it’s all about currency scarcity

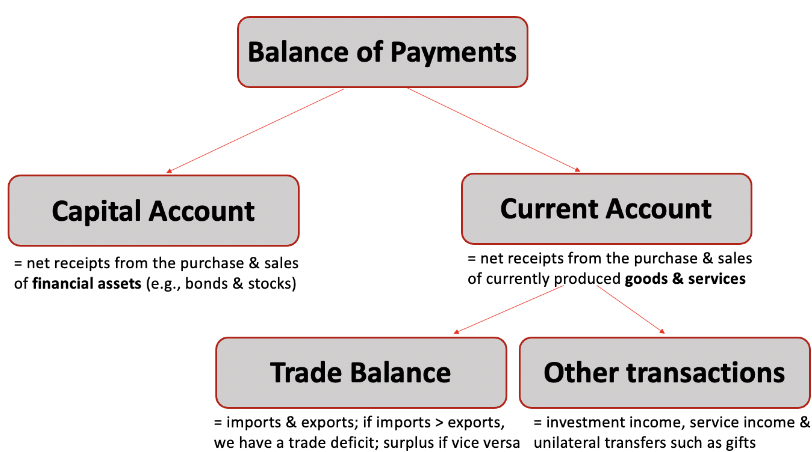

What is the Balance of Payments?

The BoP is simply a bookkeeping system recording all movements of funds between countries.

Capital account + Current account = Official Reserve Transaction Balance (a country's surplus or deficit)

What are the different Exchange Rate Regimes?

Floating - No interventions

'Dirty' Float - Only intervene when it moves a lot

Fixed - Frequent intervention to keep a certain rate e.g. 2£ per $

Explain Fixed Exchange Rate Regimes

The idea is straightforward: in fixed exchange rate regimes, monetary policy is used to ensure that the value of our currency is fixed (or “pegged”) against the value of another:

Noteworthy examples include the Gold Standard, the Bretton Woods System and the European Monetary System

How this works in practice:

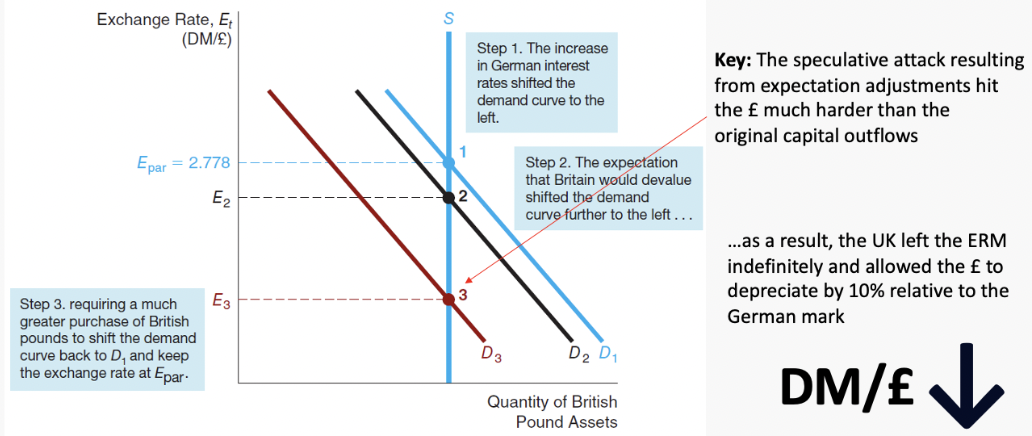

Explain the 1992 UK Forex Crisis and the big problem with fixed exchange rates.

Problem: In 1990, following the reunification, inflation crept up from 3% to roughly 5%, worrying the Bundesbank (historically, very inflation adverse)

→ contractionary policy iGER↑

Dilemma: To fix this problem, the Bank of England would have to, in turn, implement contractionary policy, bringing iGB up.

Unwilling to do so, because unlike Germany, the UL was in a recession at the time… a signal to speculators that the UK is unwilling to protect the peg.

The 1992 Forex Crisis illustrates the key issue with fixing the exchange rate:

To keep the exchange rate fixed, central banks need to design their monetary policy around this objective, which sometimes seriously conflicts with other aims such as fighting inflation or helping the economy recover from recessions.

Particularly problematic for smaller economies, who essentially have to mimic the monetary policy of their anchor economy in order to maintain the peg.

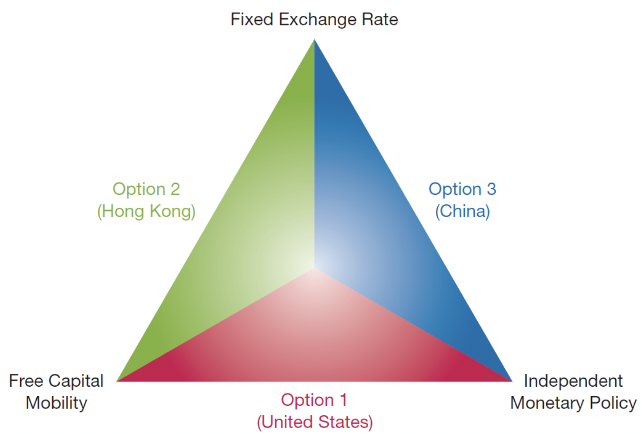

What is the Policy Trilemma

What are the pros and cons of capital controls?

Some economists and policy-makers advocate for capital controls as a way of preventing forex instability and speculative attacks.

There are, however, major problems associated with controls.

If we’re talking about restrictions on capital outflows, these tend to be quite ineffective since outflows are very difficult (and costly) to prevent.

Furthermore, corruption can flourish with politicians bribed to look the other way.

What are some problems with restrictions on capital inflows? Think again about corruption and resource misallocation… biggest issue with controls, however, is that they often target symptoms without addressing root causes such as excessive deficits.

Should countries peg their exchange rates?

Some economists argue that ‘exchange-rate targeting’ is a good rule for the conduct of monetary policy

We’ve already seen some drawbacks, however, including the loss of flexibility in responding to domestic shocks + susceptibility to speculative attacks

E.g., going back to the 1992 Forex Crisis discussion, France was in a similar situation to the UK but instead of abandoning the peg they implemented contractionary policy to prevent a depreciation

…leading to massive unemployment increases and sluggish economic growth (worth it?)

But what are some advantages?

Perhaps the most appealing feature of E.R. targeting is its simplicity, allowing central banks to “sell” contractionary policies to an understandably reluctant populace