Math488 flashcards midterm 2 and final

1/85

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

86 Terms

what is the x and y in the PDF graph?

x-results of random variable

y-probabilities

using (α, β), an exponential is a Gamma with what parameters?

alpha = 1 and beta (1/mean) Γ(1,β)

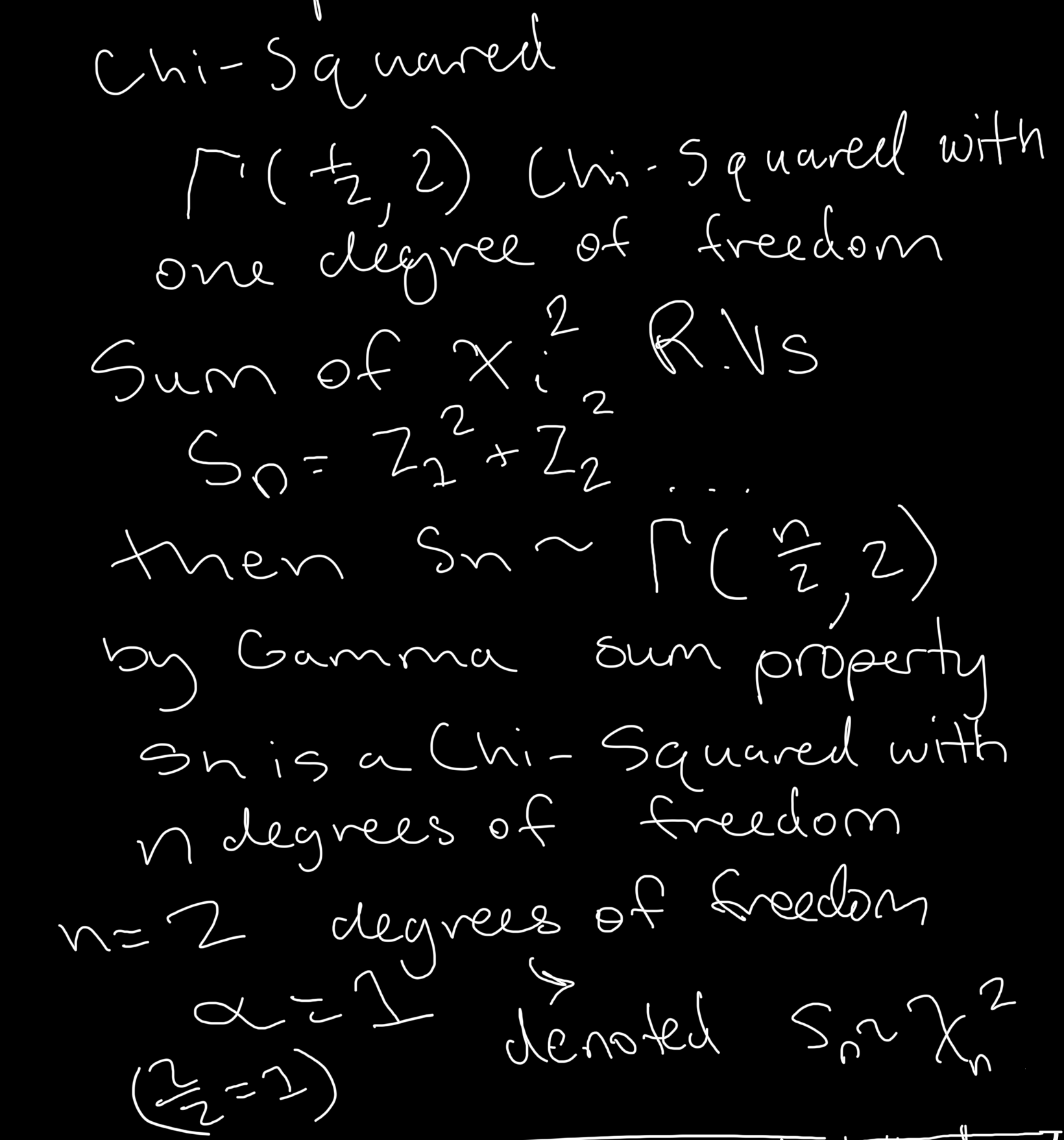

The Chi Squared distribution with one degree of freedom represented as a Gamma with parameters (α, β)

Γ(1/2, 2)

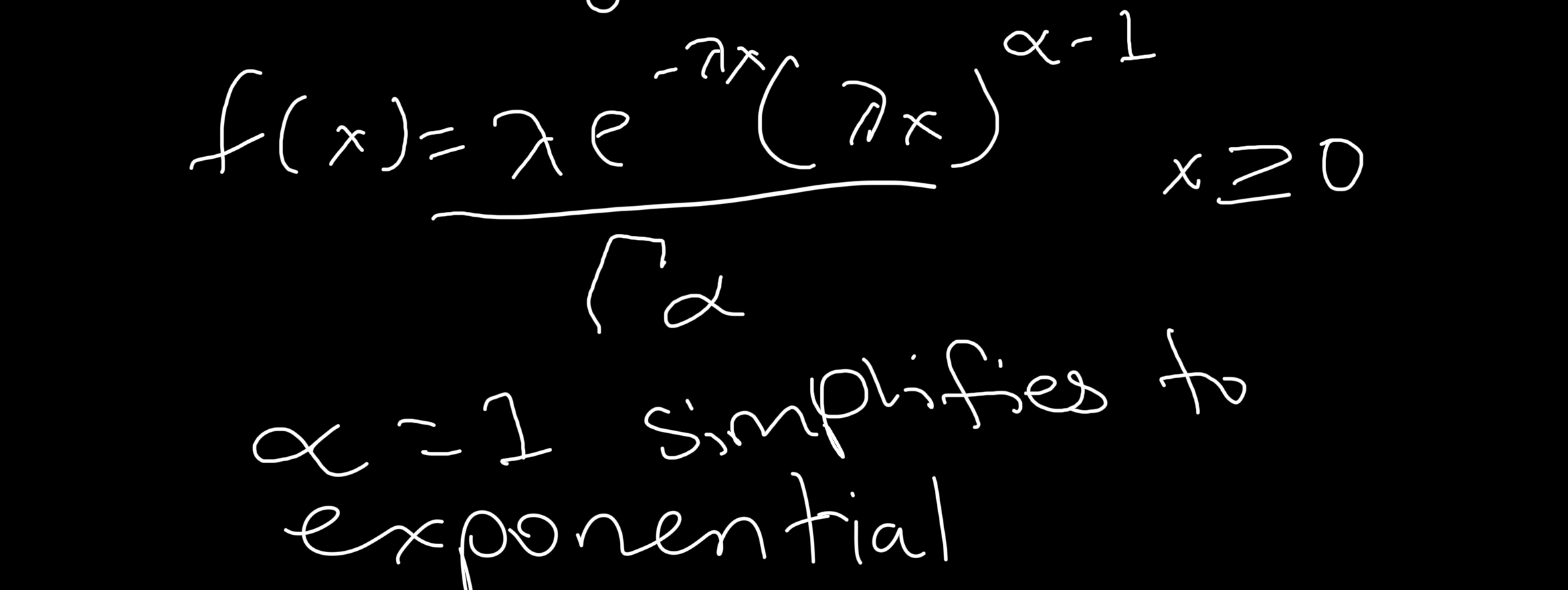

using lambdas, x and alpha, what is the PDF of the gamma?

The sum of Chi-Squared distributions is what as gamma parameters? How many degrees of freedom is from alpha = n/2? What is this denoted?

Alpha is the degrees of freedom over 2. So if n =2 alpha = 1, Sn is a chi-square distribution with n degrees of freedom

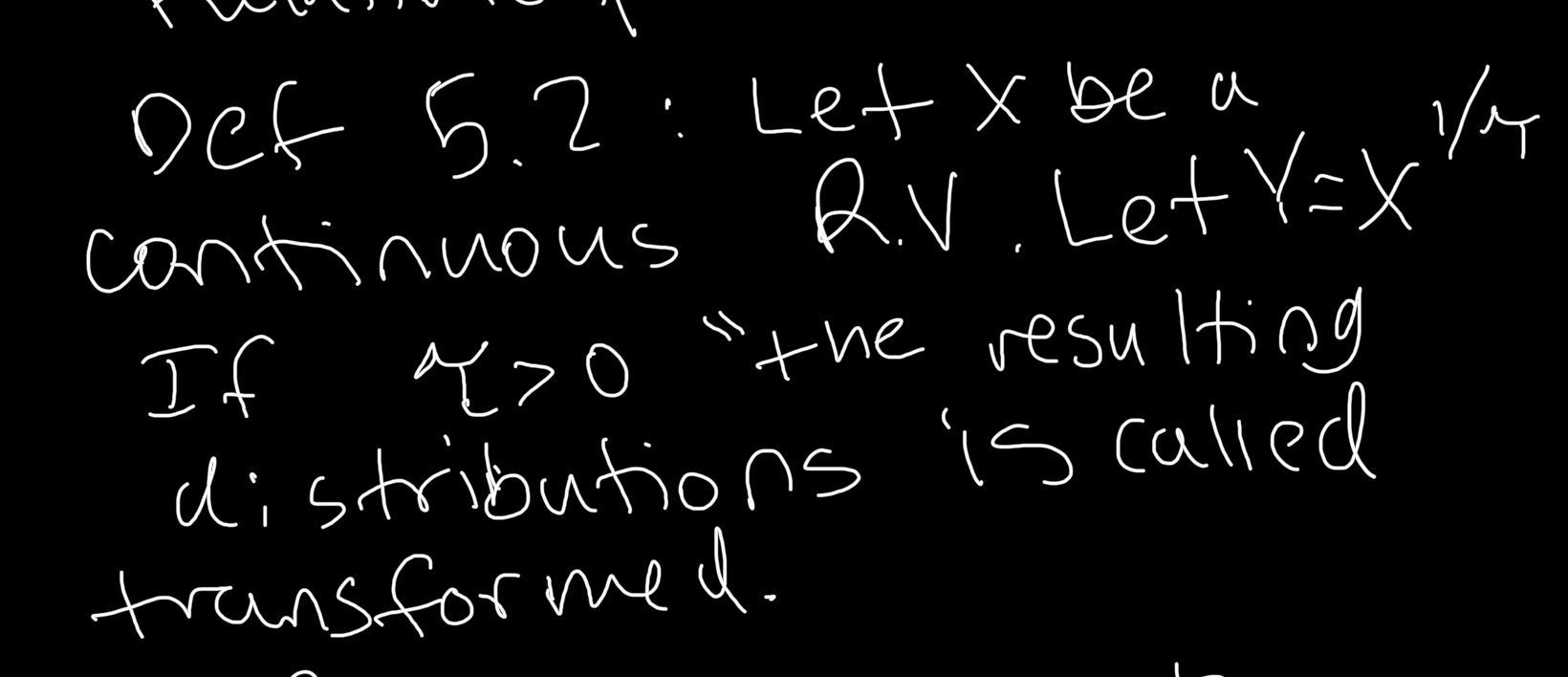

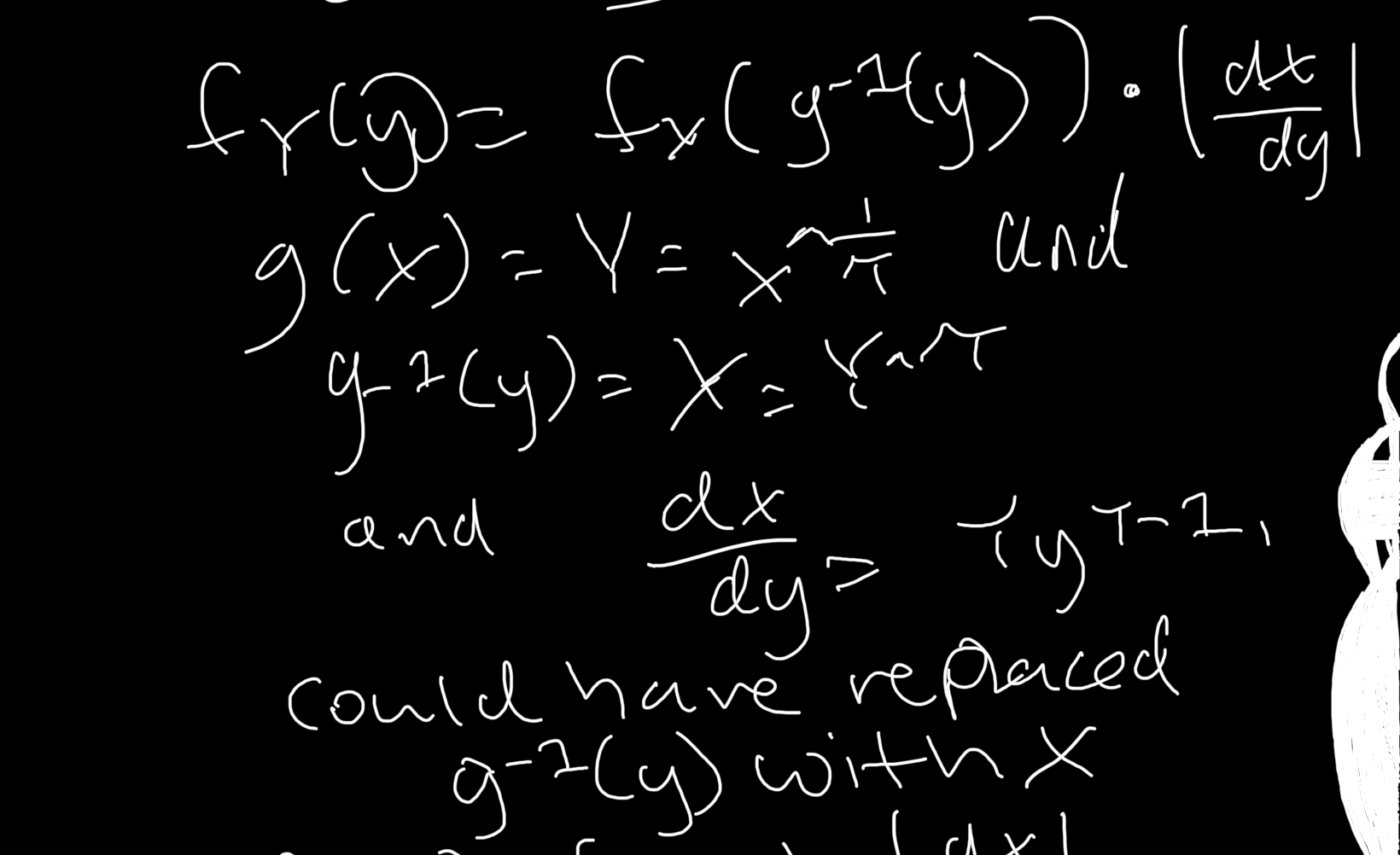

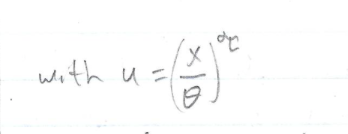

Let X be a random variable. We have a Y random variable involving an equation with X and tao. When is the distribution called transformed and what is this equation?

If τ is -1, then the resulting distribution is called..

the inverse

If τ < 0 but not -1, then the distribution is called?

the distribution is called inverse-transformed or inverse-generalized

For what value of τ is there no transformation?

τ=1

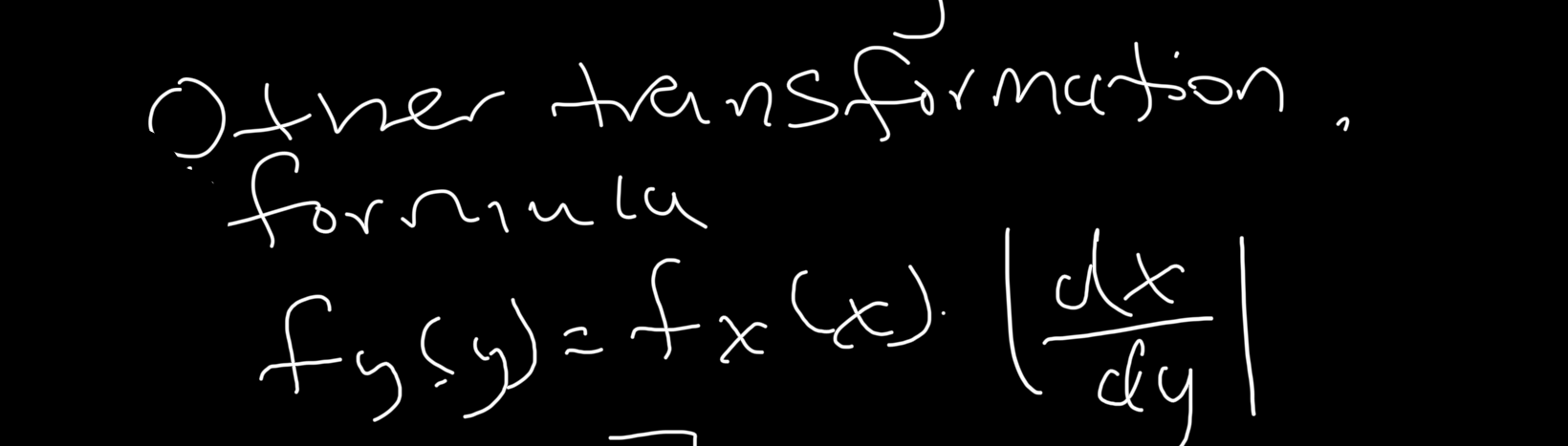

Formual for a transformed random variable fY(y) = …. What are the two formulas with different inputs into that fox?

What is X and Y the same as here?

g-1(y), g(x)

Represent the above X and Y in terms of Tao alongside dx/dy (derivative of X portion with respect to y)

Now go back to our formula with fY(Y)=fX(X)*dx/dy and plug in X and dx/dy

decompose X^(1/τ) now that X = theta subscript x *W

So when intermingling between the Gamma formulas based on our parameters, what is the principle here?

We can transform our random variable to a transformed gamma distribution

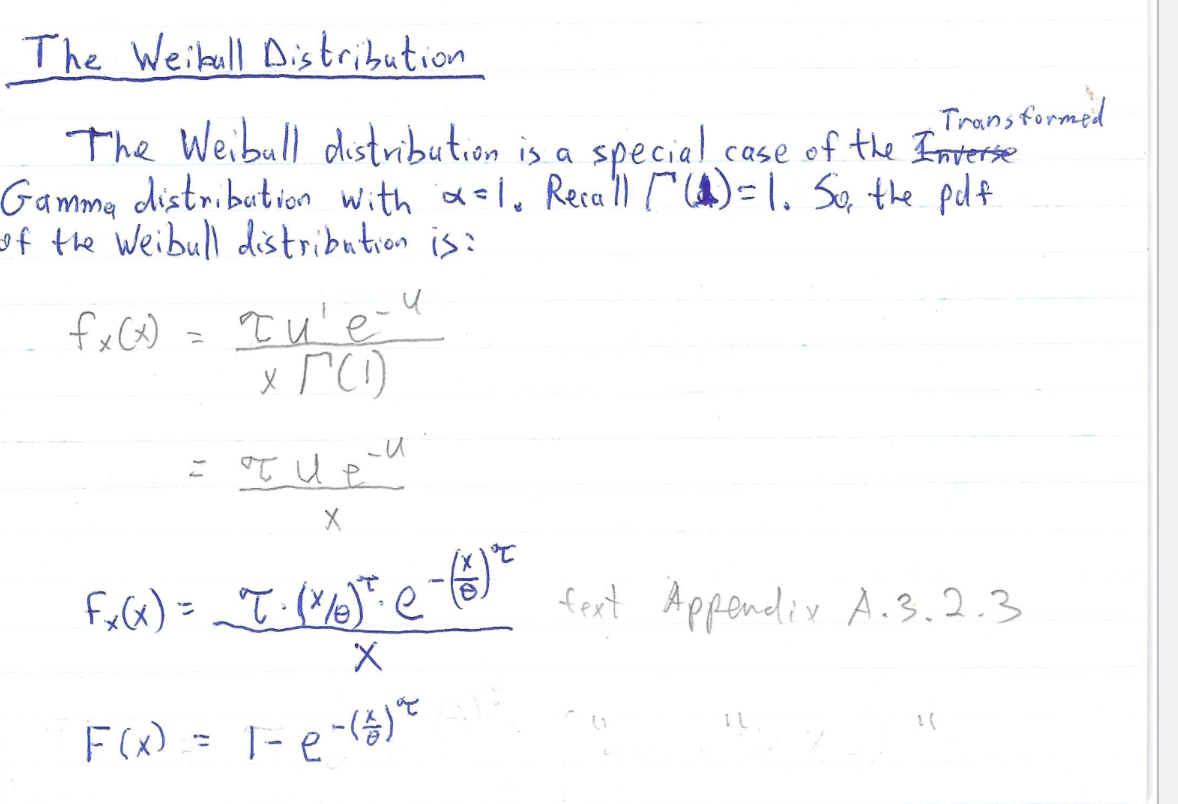

What is the Weibull distribution?

The windell distribution is a special case of the transformed Gamma distribution with alpha =1. For the PDF of the weibull remember that u = x/theta

How does the exponential relate to the Weibull?

The exponential is a special case of the Weibull with τ=1

And the exponential is a special case of the transformed Gamma with what?

τ=1 and alpha =1

Definition of the linear exponential family

the Gamma is a special case of the ___

transformed Gamma with T = 1

The support of a random variable

The set of values where the PMF/PDF is non-zero

Explain the Unsum property

Suppose the number of occurrences N is a Poisson R.V with E[X] lambda. Further suppose each occurrence can be classified into one of m types each with probabilities p1 to pm independent of all other occurrences. N1 .. Nm corresponding to types 1…m respectively are mutually independent poisons with expectations p1* lambda1, p2*lambda 2, and p3 * lambda 3.

If we remove a type that accounts for 10 percent of the claims and the original expectation of all the claims was 0.72, what is the new expectation?

0.72×0.9

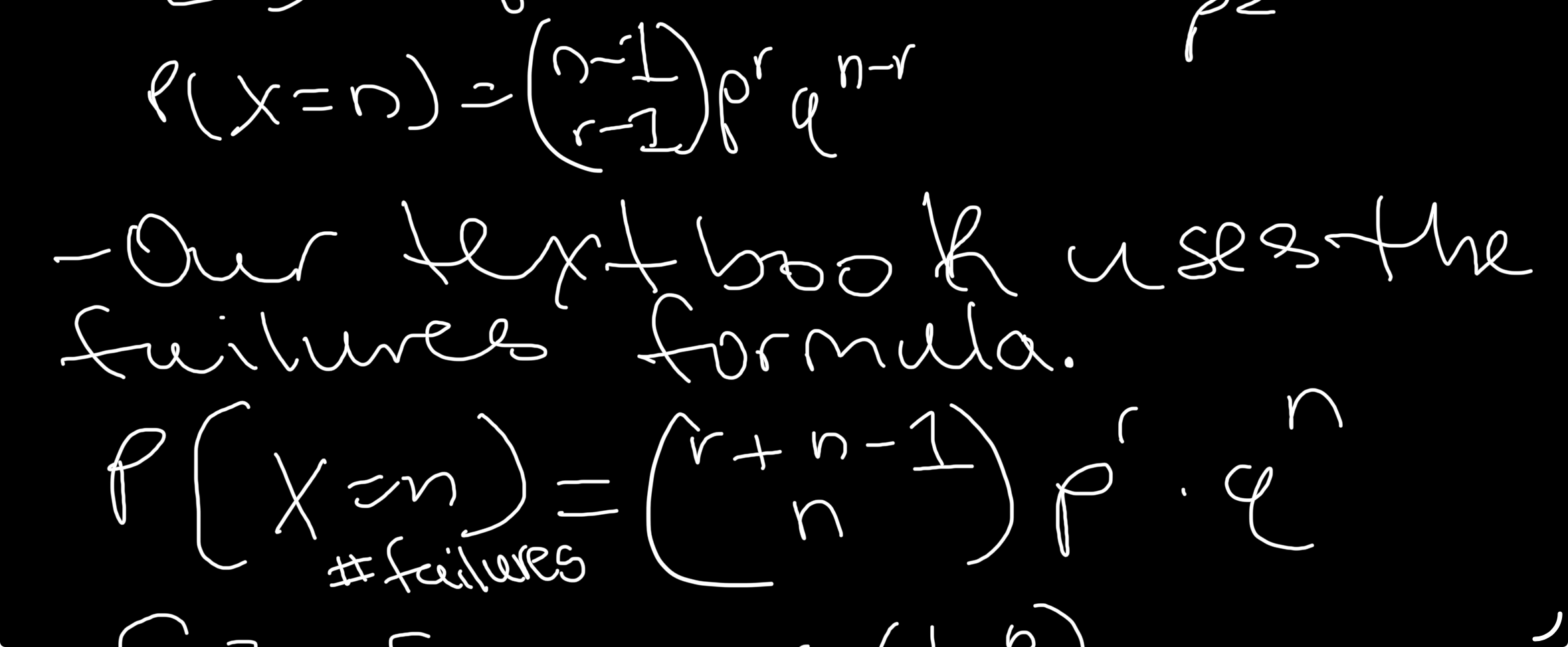

Expectation for trial and variance for negative binomial

r/p and r*q/p²

Two PMFs for negative binomial

Expectation for failure negative binomial

r/p-r

x! relation to gamma

x! = gamma function(x+1)

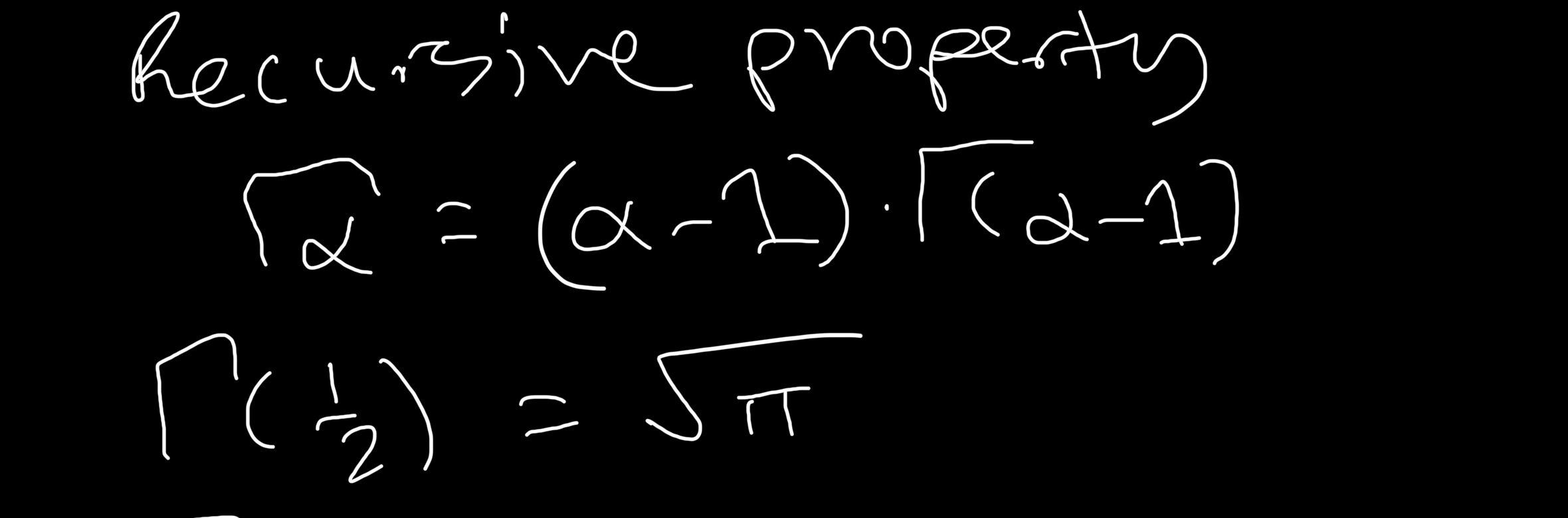

Recursive property of Gamma and gamma of 1/2

Gamma of alpha integral

Explain the properties of teh special case of N.B of 1

-Geometric distribution with r = 1

-Memoryless

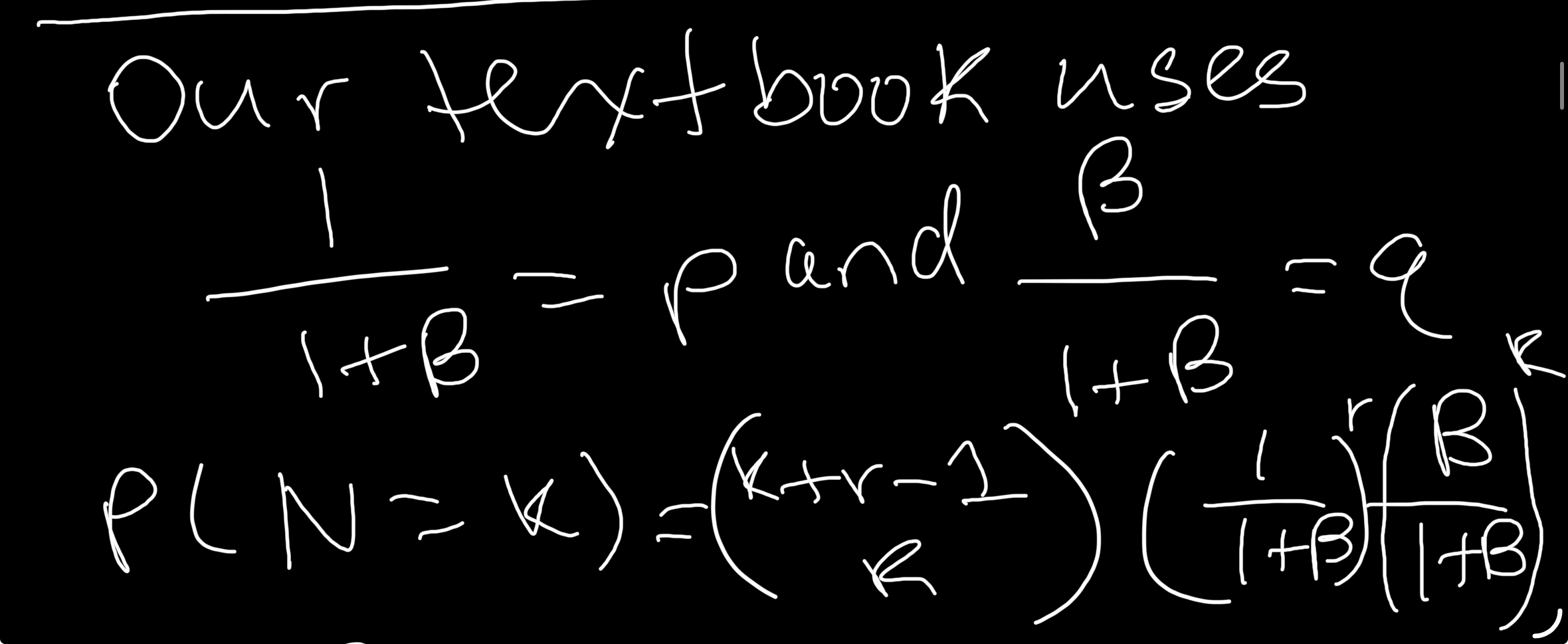

PMF for our textbook with altered values of p and q

Expectation of this Negative Binomial distribution with beta?

r*B

Why does this N.B distribution have ag greater flexibility in shape than the Poisson?

2 parameters r and B

What makes the Poisson a useful tool for modeling the frequency of insurance claims?

The sum property together with its converse

Variance of the Beta N.B distribution?

rB(1+B)

Because B > 0, explain what reflection we can make of the N.B distribution

The variance is greater than the mean. because of this, the actuary might consider the N.B as a better fit for the data than Poisson whenever the data has the variance greater than the mean

In what datasets would Binomial be a good fit for claim frequency data?

In datasets where the variance is less than the mean

In the binomial, values far from the mean may be considered _. Why?

be considered 0 because the variance is small

Under what rules is the binomial a good fit for modeling the number of claims in a portfolio of policies?

-Type of insurance that can have more than 1 claim per year

-A portfolio of n policies

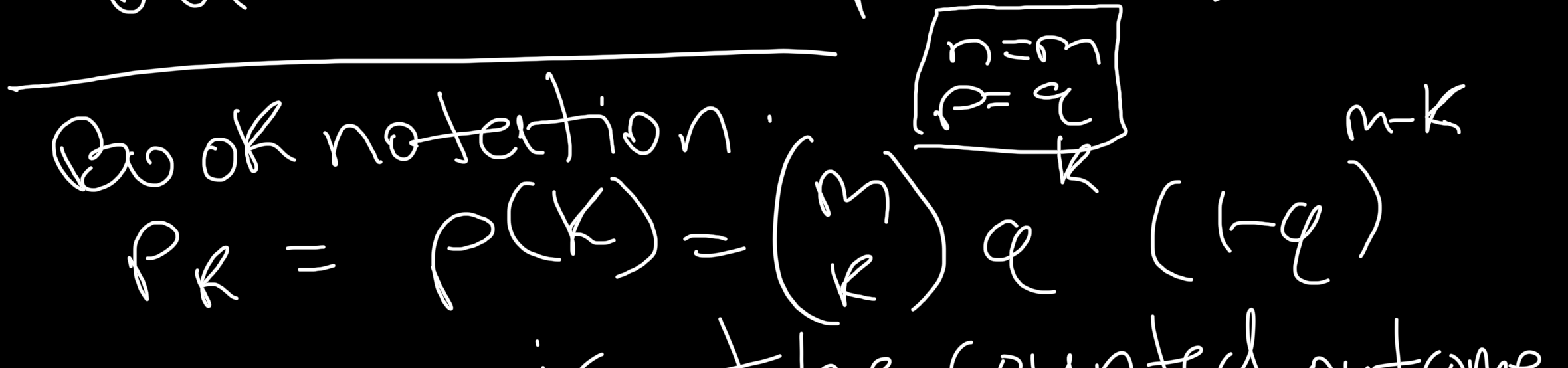

Explain how the binomial distribution now is different from 477?

p now = q

n now = m

New PMF

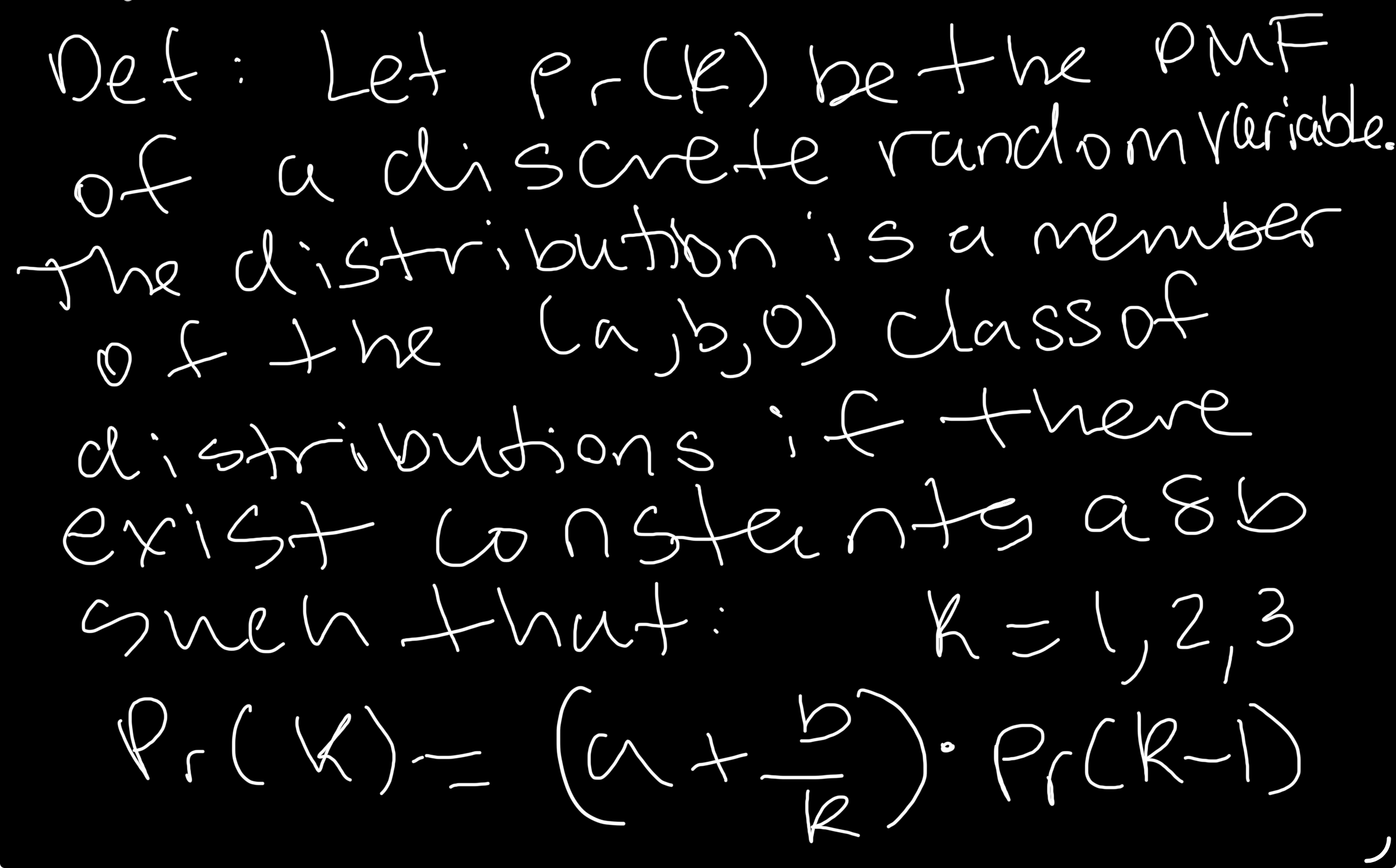

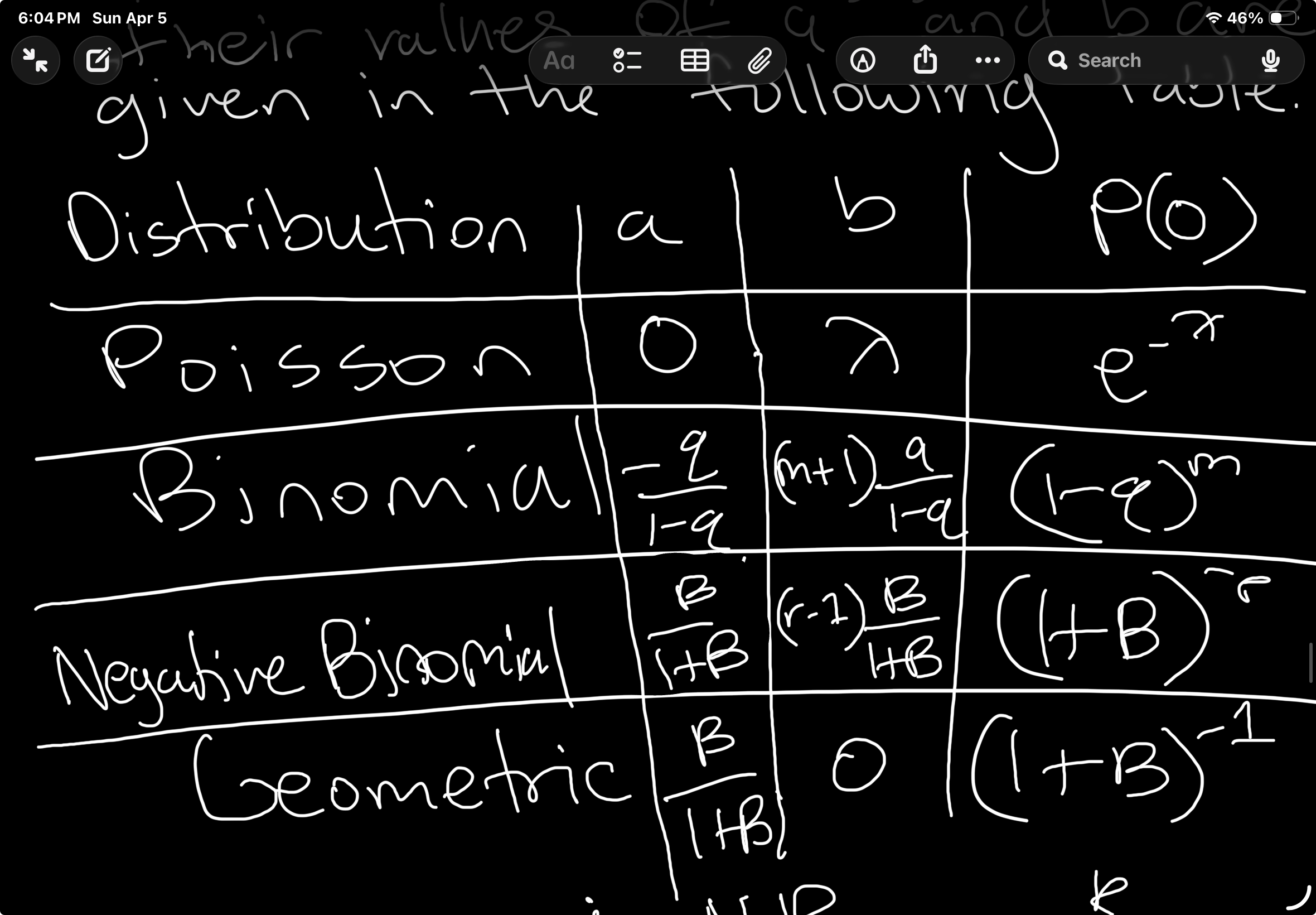

Define the (a, b, 0) class of distributions

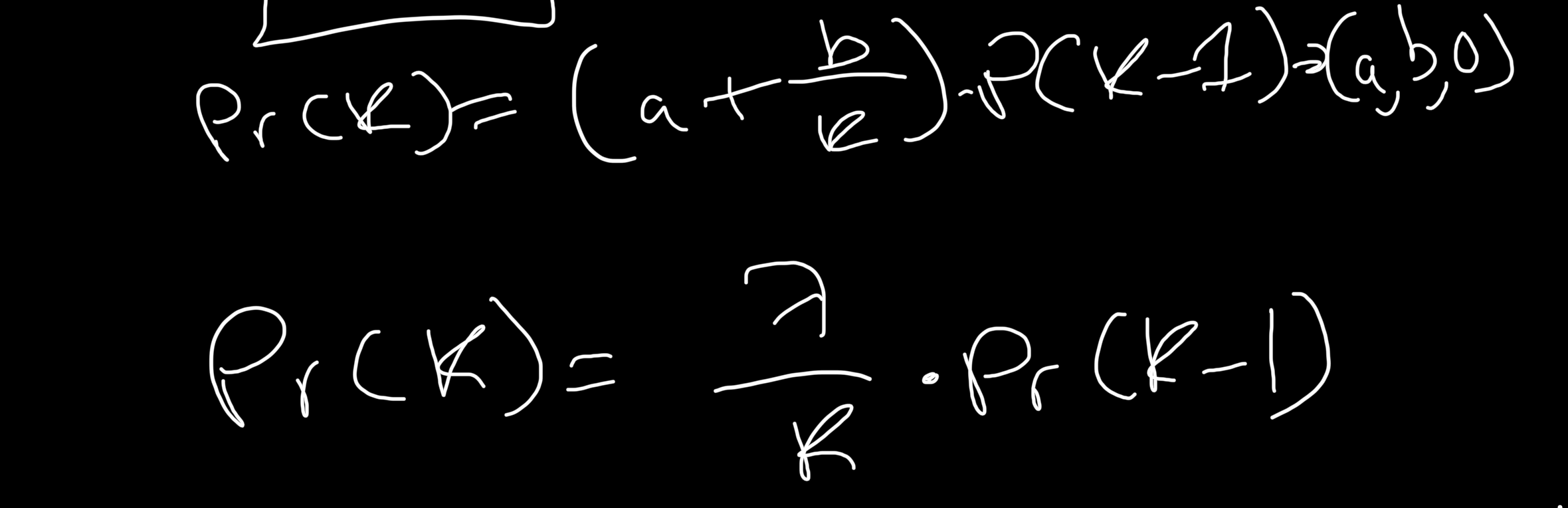

The Poisson is a member of the (a, b, 0) class with what parameters?

a = 0, b= lambda

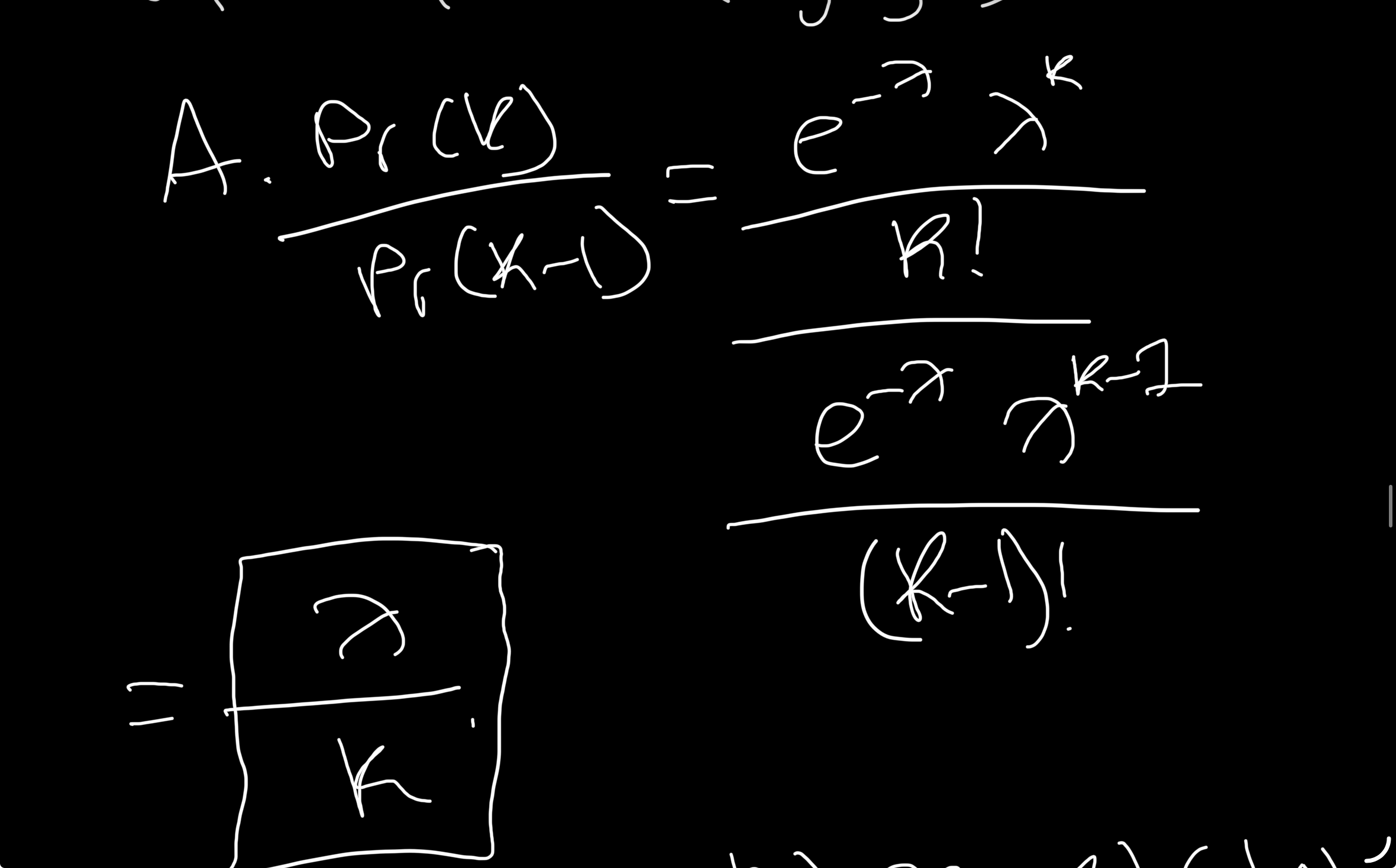

Pr(k)= what in Poisson as it relates to the (a,b,0) class?

what 3 R.Vs belong to the (a,b,0) class of distributions?

N.B, Poisson, Binomial, and Geometric if we count it as part of the N.B

The geometric distribution has what property?

Memoryless property

An actuary faced with data having smaller variance than the mean might consider what distribution?

The Binomial

Write the Binomial PMF in the context of this course and its conventions

Show that the Poisson is a member of the (a, b, 0) class

Write out the a,b, p(0) values for Poisson, Binomial, Negative Binomial, and Geometric

List the range of a values for all the 3 distributions, negative binomial, poisson, N.B

Poisson: a = 0

Binomial: a < 0

Negative Binomial: 0 < a <1

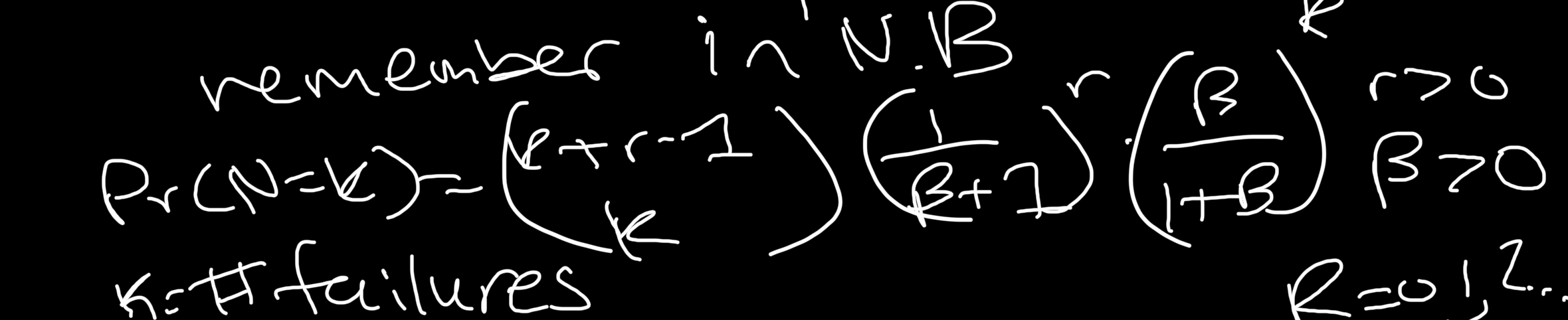

Write out the negative Binomial failures formula with beta

What do we have to remember about solving for Expectation and p(0) for a distribution given a and b?

-Remember use the values for ranges of a to figure out which distribution it belongs to

-In the case of negative binomial, we solved for Beta and r using a and b formulas

-We did not use the recursive formula to find p(0) but rather our normal negative binomial PMF after finding beta and r, which were the two parts we needed to fill in the PMF. Then we set k to 0 and solved for P(0) that way

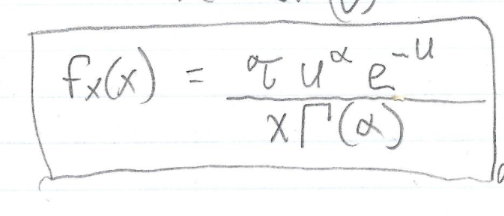

Formula for Transformed Gamma PDF

u = what?

(x/theta)^T

What is useful to find Weibull from transformed Gamma? What is the Weibull PDF and CDF?

The Weibull is a special case of the transformed Gamma with alpha = 1

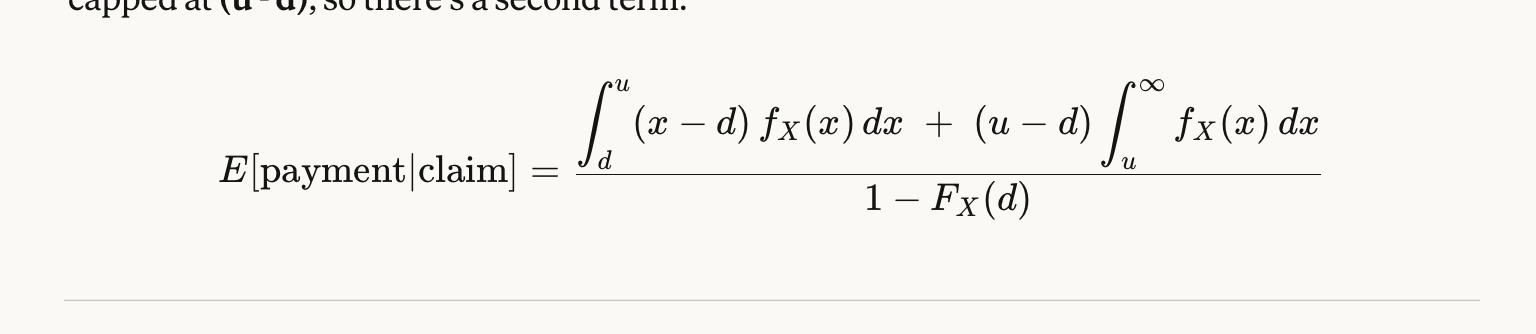

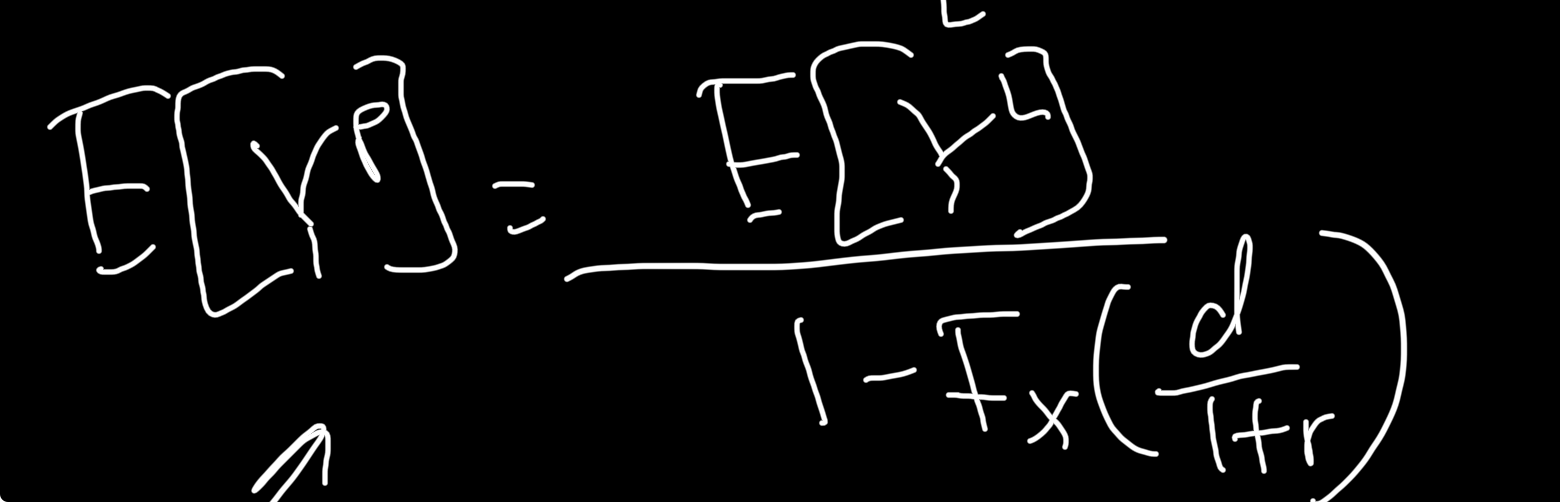

Expected insurance payment given a claim was made with d and u

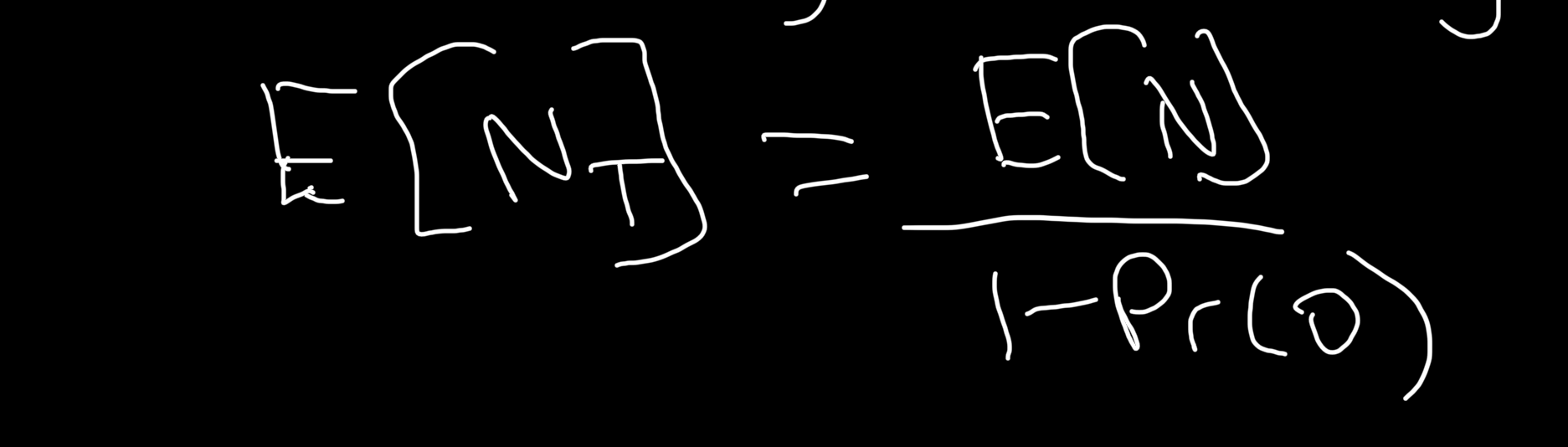

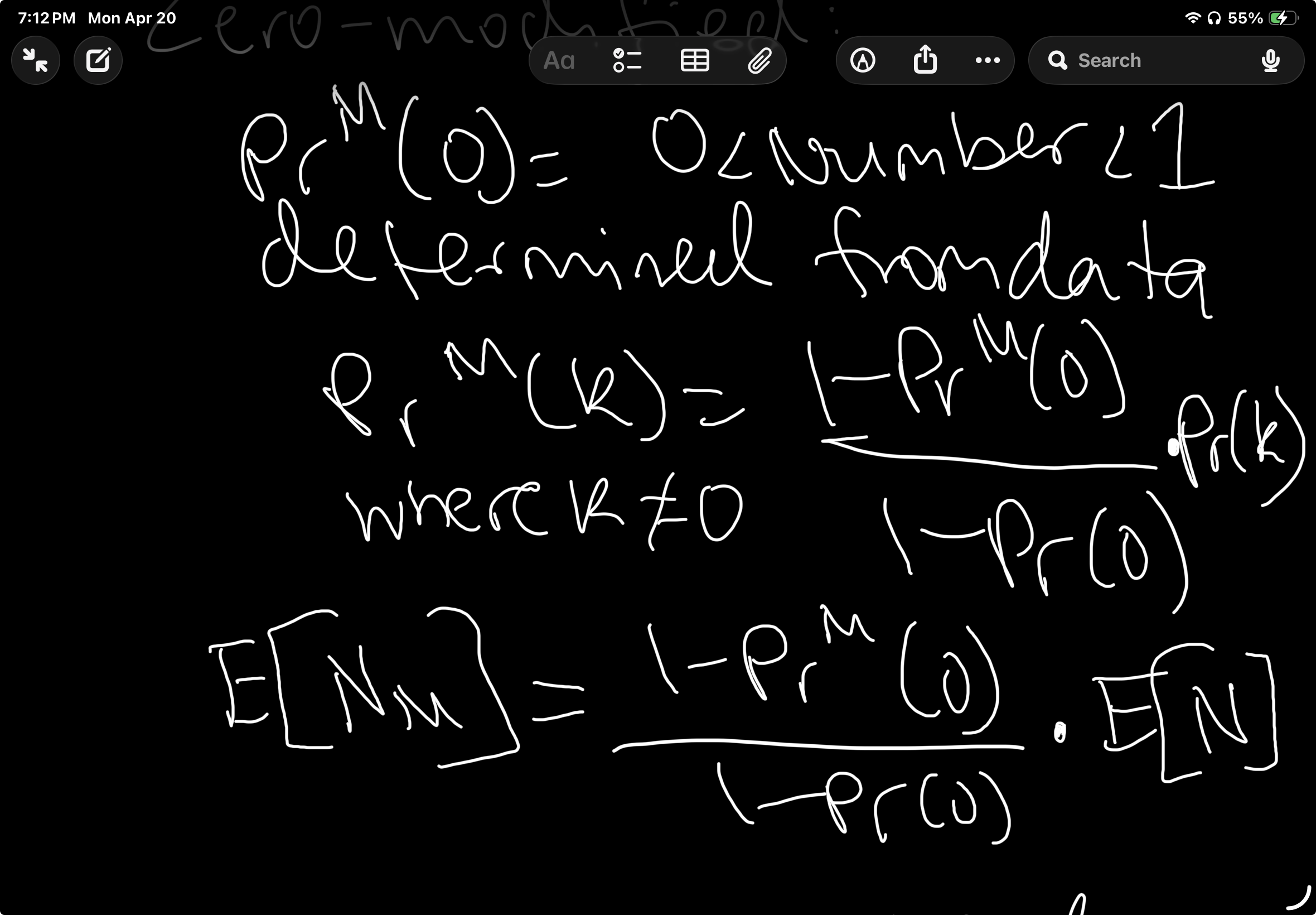

calculate the new Pr T (k) (truncated probability)

Pr(k)/(1-Pr(0))

Likewise calculate the new truncated expectation

Calculate new modified PrM(k) and the new modified E[Nm]

Describe the truncated N.B, its properties

-This is a variation on an N.B distribution which allows the parameter r>-1, as opposed to r>0 for the N.B. It’s a member of the a,b,1 distribution. It has a truncated probability of 0 at PrT(0)=0. For k=2,3,4 the probabilities are generated using recursion with a = B(1+B) and B = (r-1)*a. This is a different distribution from the N.B and when n is negative an and b are identical to the N.B. The normal expectation formulas for N.B will not work.

Franchise Deductible? Difference between Y^L and Y^P pieces?

Pays the full loss when the loss exceeds the deductible. Y^L = 0 if x <=d and x if x>d. Y^P i undefined at x <=d and x at x>d.

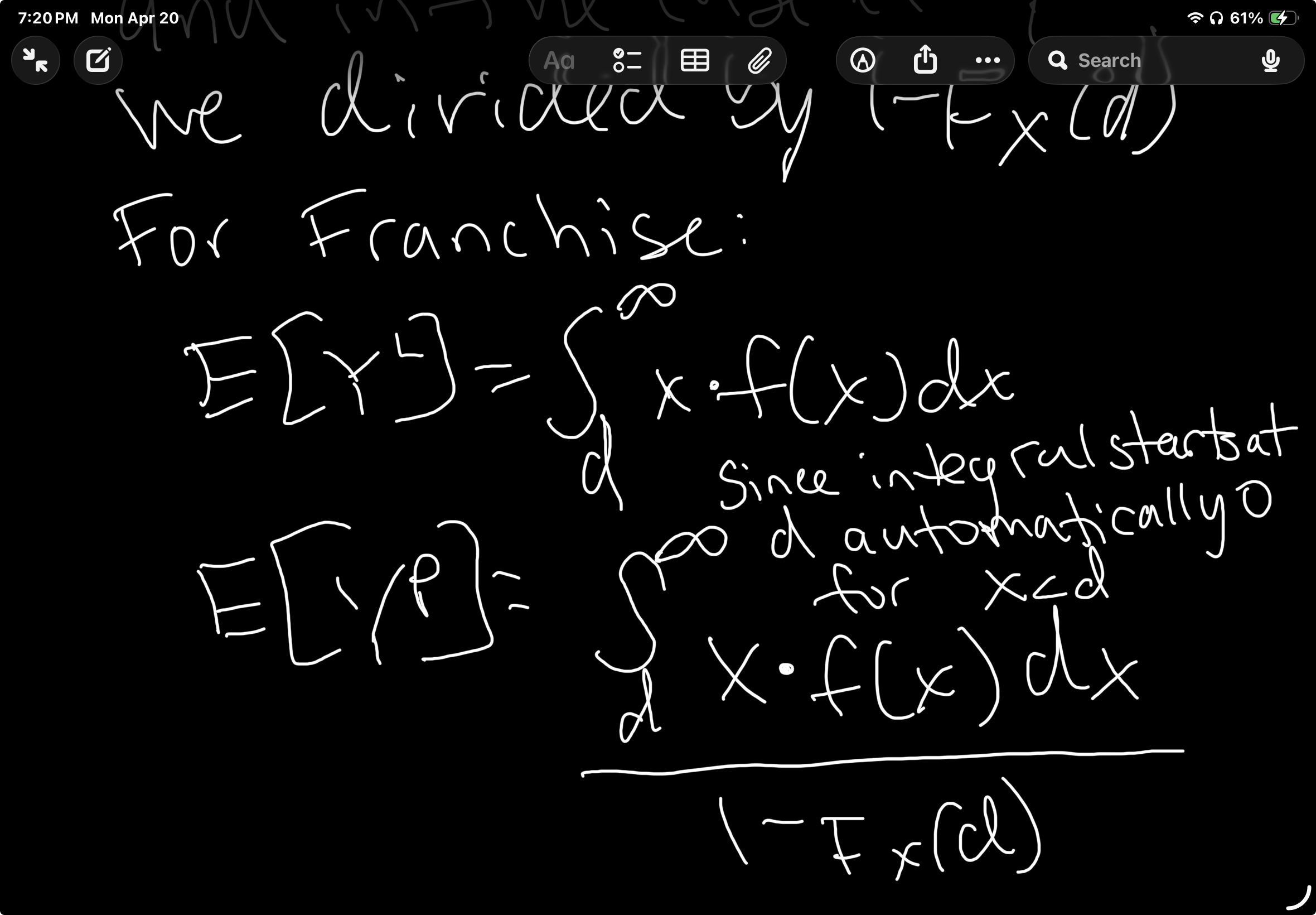

E[Y^L] and E[Y^P] formulas

What does (X-d)+ mean?

It takes X-d when the quantity is positive, and 0 otherwise

so X-d when x >d and

0 when x <=d

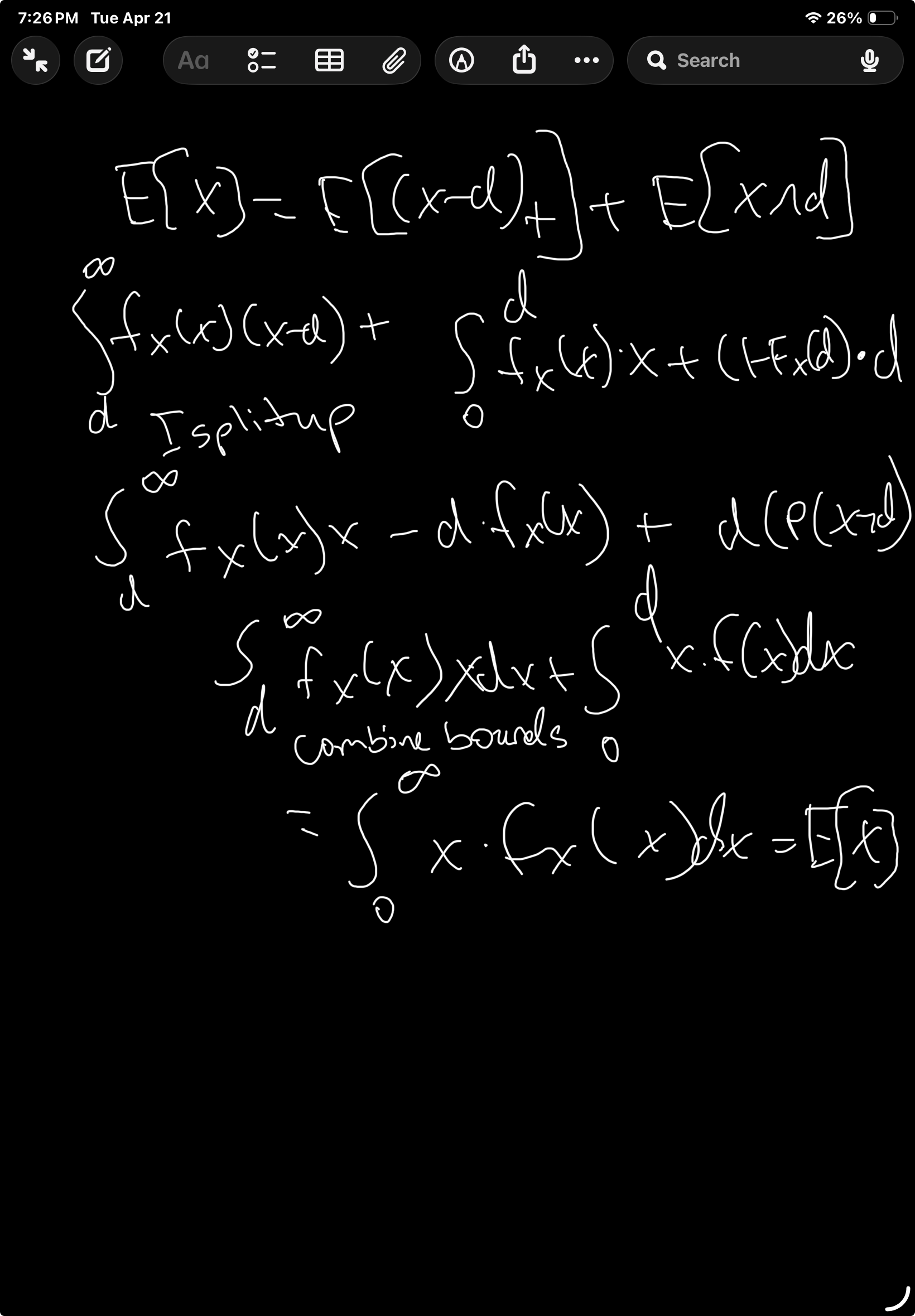

Formula involving 3 expectations for franchise deductible (using last flashcard)

E[X] = E[X-d]+ + E[X^d]

Prove that E[X] = E[X-d]+ + E[X^d]

Now bring E[Yl] into a formula using the previous terms

E[Y^L]=E[X]-E[X^d]+d*(1-F(d))

Define Loss Elimination Ratio and give the formula

Loss Elimination Ratio is the decrease in the expected payment with an ordinary deductible to the expected payment with no deductible.

E[X^D]/E[X]. This is the percentage of the amount of money paid out of total losses in money. What is actually paid as a fraction to the loss

If X has a uniform distribution on (0,100) and d = 10 and it is a franchise deductible, find E[Y^L] and E[Y^P]

49.5, 55

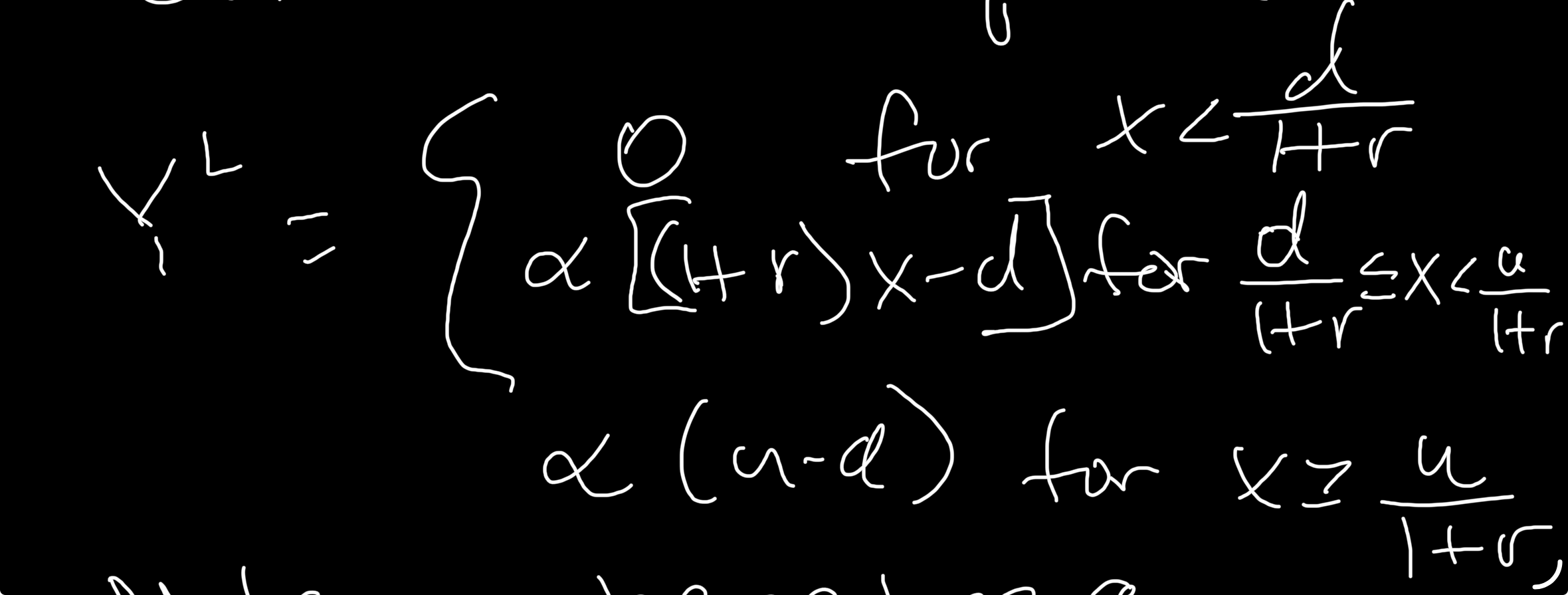

For an ordinary deductible of d after inflation of r, (but not rising d), the expected cost per loss is:

E[Y^L]=(1+r)*(E[X]-E[X^d/(1+r)])

If X has a uniform distribution on (0,100) and d = 10 is an ordinary deductible, what is the LER of this deductible

0.19

Suppose that in the following year there is inflation of 10% on all products and services covered by this policy and the deductible d remains at $10.

-Calculate the new expected cost per loss

-Calculate the new LER

45.454545..

0.157776

Define Policy Limit and give the CDF

This is a limit on an insurer’s payment or a loss. If there are no other modifications we have this cdc

Draw out the new uniform distribution from 0,100 if there is no deductible but there is a policy limit of 90.

What is the new expected cost to the insurer if a policy limit of up to experiences inflation r.

E[Y]= (1+r)*(E[X^u/(1+r)])

Coinsurnace definition

A fraction of the loss covered by the policy, that the policyholder pays. This fraction is an insurance factor alpha, where 0 < alpha < 1. The insurer pays alpha*covered loss and the insured pays (1-alpha)*covered loss.

How much does insurance pay if you have a loss of 50, a deductible of 10, on a uniform distribution from 0 to 100 and there is a coinsurance factor of 90%?

Insurance pays $36

Insured pays $4

Give the cost per loss CDF when there are 4 modifications: deductible, policy limit, inflation, and coinsurance

E[Y^L] when 4 modifications are present

E[Y^P] when 4 modifications are present

Define Collective Risk Model and its properties

S= X1+X2+Xn where each Xi is a claim payment coming from a defined set of insurance contracts. May be from same or different individual insureds. Xis are independent and identically distributed. S = 0 when N = 0

Define Individual Risk Model

S = X1+X2 +XN where n is a fixed number of contracts. n is the number of people in the group that have claims. Xi’s are the total amount of claims/payments for the contract i. Xi may be 0. Xi’s are assured to be independent but not identically distributed.

In creating a compound model for aggregate claims that applies to the collective risk model, what two components do we want?

A frequency model (N) and a severity model (X), we want to create a distribution S.

Find an expression for the value of Fs(x) in the case of conditioning on N

Conditional expectation formula general, discrete case

E[X]=E[E[X|Y]]

![<p>E[X]=E[E[X|Y]]</p>](https://assets.knowt.com/user-attachments/45bec071-006e-4cd4-85bc-34c5e51c90e7.png)