Topics E&F - Banking and credit markets + Financial Crises

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

28 Terms

Why study financial systems?

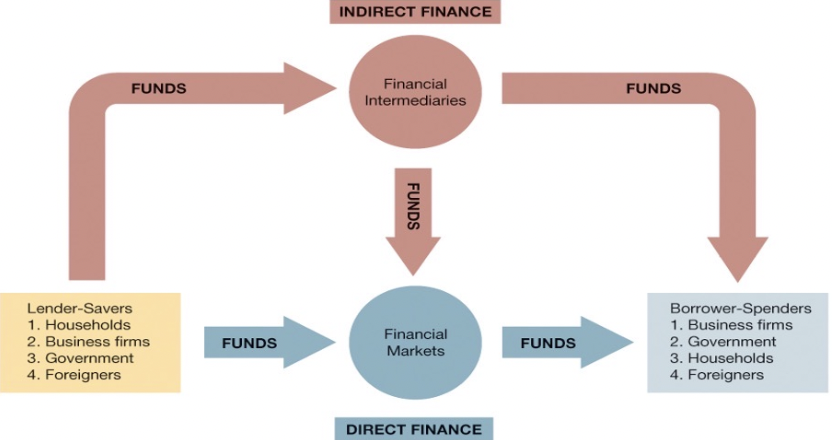

Financial systems are markets in which funds are transferred from people and firms who have an excess of available funds to people and firms who have a need of funds.

A healthy and vibrant economy requires a financial system that moves funds from people who save to people who have productive investment opportunities.

We are interested in an economic analysis of how the financial structure is designed to promote economic efficiency.

Describe the flow of funds through the financial system

What is a financial intermediary?

Financial intermediaries: institutions that borrow funds from people who have saved and in turn make loans to people who need funds.

Banks: accept deposits and make loans

Other financial institutions: insurance companies, finance companies, pension funds, mutual funds and investment companies

What is the function of financial intermediaries?

Indirect finance

Financial intermediaries have evolved to reduce transaction costs: they allow “small” savers and borrowers to benefit from the existence of financial markets.

Economies of scale: reduces transaction cost and enhances liquidity services

Risk sharing/asset transformation: reduces risk exposure by spreading returns earned on risky assets. Diversification and pooling of assets into new assets safer assets for investors

Expertise: developed expertise in dealing with asymmetric information problems:

Adverse Selection (before the transaction): try to avoid selecting the risky borrower by gathering information about them

Moral Hazard (after the transaction): ensure borrower will not engage in activities that will prevent him/her to repay the loan.

Using a contract with restrictive covenants.

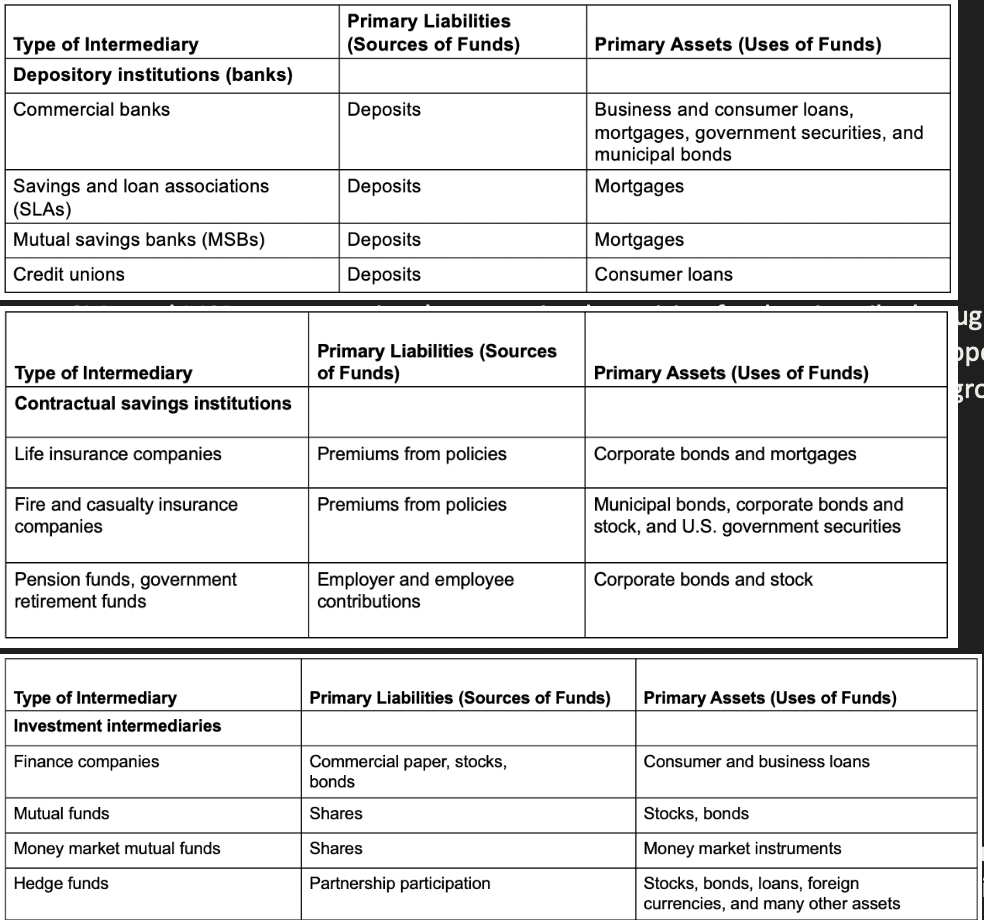

What are the different types of financial intermediaries?

SLAs and MSBs were previously constrained to raising funds primarily through savings deposits (i.e., shares), time and checkable deposits. Over time, loosening restrictions mean they now operate like commercial banks.

Credit Unions are cooperative lenders organised by unions and employee groups that use share (deposits) to create consumer loans.

Essentially, contractual savings institutions are insurance companies and pension funds that acquire funds at periodic intervals on a contractual basis to invest primarily in long-term securities such as corporate bonds, stocks, and mortgages.

Commercial paper: unsecured short-term money market debt instrument issued by large banks and well-known corporations (often 30 days) to fund payroll, accounts payable, etc. Sold at a discount from face value, difference is interest return for investor.

Money market: financial market in which only short-term debt instruments (generally maturity terms < one year) are traded.

Capital market is the market in which longer-term debt instruments (generally original maturity terms of one year or greater) and equity instruments are traded.

How does Adverse Selection affect financial structure (Lemons problem)?

If quality cannot be assessed, the buyer is willing to pay at most a price that reflects the average quality.

Sellers of good quality securities will not want to sell at the price for average quality.

The buyer will decide not to buy at all because all that is left in the market is poor quality equities.

How does Moral Hazard affect the choice between debt and equity contracts?

Seller of securities may have incentives to hide information and engage in undesirable activities for stockholder. Has consequences for whether a firm finds it easier to raise funds with debt than with equity contracts

What tools can help solve moral hazard in debt contracts?

Net worth and collateral

Incentive compatibility (participant with more information is motivated to act in the interest of other party(ies). E.g., manager’s employment contracts incorporates a bonus system to align their interests with those of the shareholders.

Monitoring and enforcement of restrictive covenants

Discourage undesirable behavior (e.g., mandates to use funds for specific assets)

Encourage desirable behavior (e.g., life insurance mandates for mortgage)

Keep collateral valuable (e.g., car/home insurance + sale restrictions until loan paid off)

Provide information (e.g., periodic reporting such as quarterly income reports)

What is the principal-agent problem?

Principal: less information (stockholder)

Agent: more information (manager)

Separation of ownership and control of the firm:

Managers pursue personal benefits and power rather than the profitability of the firm.

What tools can help solve the principal-agent problem?

Monitoring (“Costly State Verification”, e.g., audits)

Free-rider problem (decreases amount of private information to tackle moral hazard)

Govt. regulation to increase information(e.g., standard accounting principles, stiff penalties)

Financial Intermediation (e.g., venture capital: participants as board members)

Debt Contracts (fixed periodic payments without demand to know exact profit)

What is the Bank Balance Sheet

To understand how banking works, we start by looking at the bank balance sheet, a list of the bank’s assets and liabilities (this list balances) such that:

Total assets = Total liabilities + Capital

Essentially a list of sources of funds (liabilities and capital) and uses of the funds (assets). Banks obtain funds by borrowing and by issuing other liabilities (e.g., deposits). They then use these funds to acquire assets (e.g., securities and loans).

Banks make profits by earning interest on their asset holdings of securities and loans that is higher than the interest and other expenses on their liabilities.

What is a liability?

These are acquired funds by issuing (selling) liabilities such as

Checkable deposits: checks can be drawn from these accounts that allow the owner of the account to write checks to third parties.

Non-transaction deposits: primary source of funds. Owners cannot write checks on deposits, but the interest rates paid on them are usually higher than for checkable deposits. Two basic types :

Savings accounts: Funds can be added to or withdrawn from savings accounts at any time and transactions/interest payments are recorded in a monthly statement or passbook held owner.

Time deposits (i.e., certificates of deposit, CDs): fixed maturity length (i.e., several months to over five years) with substantial penalties (the forfeiture of several months’ interest) for early withdrawal.

Borrowings: Banks also obtain funds by borrowing from Central Banks (also known as advances). , other banks (borrowing overnight reserves), and corporations (repurchase agreements).

Bank capital: Final category on the right-hand side of balance sheet, the difference between assets and liabilities. Capital is raised by selling new equity (stock) or from retained earnings. It cushions against a drop in asset value, which can lead to insolvency (i.e., bank liabilities > assets = liquidation)

What is an asset?

Banks use acquired funds by issuing liabilities to purchase income earning assets.

Reserves: Part of deposits held in an account with the Central Bank, plus currency physically held by banks (called vault cash stored in bank vaults overnight). Banks hold them for two reasons.

Regulation: required reserve ratio, e.g. 10% of deposits must be kept as reserves with the central bank.

Reserves are the most liquid of all bank assets which can be used to meet obligations when funds are withdrawn, either directly by a depositor or indirectly when a check is written on an account.

Cash items in process of collection: checks written on an account at another bank is deposited in a bank, but funds for this check have not yet been received from the other bank.

Deposits at other banks: small banks hold deposits in larger banks in exchange for a variety of services (e.g. check collection, foreign exchange transactions). This is also called correspondent banking.

Securities: Banks hold securities as key income-earning assets (e.g., government bonds & treasury bills).

Loans: Bank profits primarily from issuing loans (> 50% of revenues). A loan is a liability for the individual or corporation receiving it but an asset for a bank (income to the bank): typically, less liquid than other assets because they cannot be turned into cash until the loan matures. Also, higher default probability than other assets.

Other assets: The physical capital (bank buildings, computers, and other equipment) owned by banks

Explain basic banking and profitability (asset transformation)

Asset transformation: selling liabilities with one set of characteristics and using proceeds to buy assets with a different set of characteristics: banks are in the business of “borrowing short and lending long.”

The bank is making a profit because it holds short-term liabilities (e.g., checkable deposits) and uses the proceeds to fund longer-term assets (i.e., loans) with higher interest rates.

For example, loans have an interest rate of 10% p.a., the bank earns $9 in income p.a. If deposit receives a 5% interest p.a. with service cost of $2 p.a., the cost of the deposit is $7 p.a.

Profit on the new deposits is then $2 per year, plus any interest that it earns on required reserves.

What are the general principle of bank management?

Liquidity Management

Asset Management

Liability Management

Capital Adequacy Management

Credit Risk

Interest-rate Risk

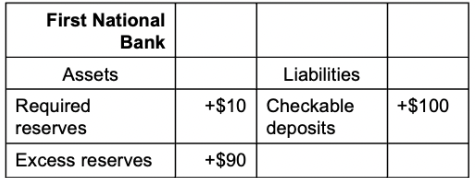

Explain liquidity management and the role of reserves

Suppose a bank’s required reserves are 10% of $100 million, or $10 million. Given that it holds $20 million of reserves, the left panel shows that the bank has ample excess reserves of $10 million.

If a deposit outflow of $10 million occurs (right panel), the outflow does not necessitate changes in other parts of its balance sheet. The bank loses $10 million of deposits and $10 million of reserves.

Excess reserves are insurance against the costs associated with deposit outflows!

Shortfall: Reserves are a legal requirement: shortfalls must be eliminated.

The situation is quite different with insufficient excess reserves (right panel above). If $10 million is withdrawn from deposits and hence reserves, the bank has a problem:

It has a reserve requirement of 10% of $90 million, or $9 million, but it has no reserves! To eliminate this shortfall, the bank has four basic options:

Acquire the reserves needed to meet a deposit outflow by borrowing them from other banks or corporations.

Sell some of its securities to help cover the deposit outflow

Acquire reserves by borrowing from the Central Bank

Reduction of loans

Explain asset management

To maximize its profits, a bank must simultaneously accomplish three goals:

Seek the highest possible returns on loans and securities

Reduce risk.

Have adequate liquidity.

Banks try to accomplish these three goals using four tools:

Find borrowers who will pay high interest rates and have low possibility of defaulting: Banks must decide if potential borrowers are good credit risks who will make interest and principal payments on time (i.e., screening to reduce the adverse selection problem).

Purchase securities with high returns and low risk: High returns are inherently tied to higher risk assets and vice versa. Yet, banks are highly regulated to prevent excessive risk taking. Thus, they must balance the pursuit of profit with the safety of depositors’ funds through careful portfolio management.

Lower risk by diversifying: Banks lower risk by purchasing many different types of assets (short- and long-term) and approving loans to a variety of customers. Overspecialization in making loans to certain sectors (e.g., energy, real estate, farmers) can lead to huge losses due to sectoral shocks.

Balance need for liquidity against increased returns from less liquid assets: manage the liquidity of assets so that they can meet deposit outflows & still satisfy reserve requirements without bearing huge costs. Banks will hold liquid securities even if they earn a somewhat lower return than other assets.

Explain liability management

This is a recent phenomenon due to rise of money centre banks, expansion of overnight loan markets and new financial instruments (such as negotiable certificate of deposit, CDs).

Before the 1960s, liability management was a staid affair: banks took their liabilities as fixed and spent their time trying to achieve an optimality in asset mix. There were two main reasons for these trends:

First, bank funds were mainly obtained through checkable (demand) deposits that by law could not pay any interest. Banks could not compete for deposits by paying interest on them.

Second, large banks (money centre banks) in key financial centres (e.g., New York), began to explore how liabilities could provide reserves and liquidity: expansion of overnight loan market & development of new instruments (e.g., negotiable CDs).

Different (flexible) approach to liability management: aggressively set target goals for their asset growth and try to acquire funds (by issuing liabilities) as they were needed.

Explain capital adequacy management and how capital prevents bank failure

Banks have to decide the amount of capital they need to hold for three reasons:

Bank capital helps prevent bank failure, a situation in which the bank cannot satisfy its obligations to pay its depositors and other creditors and so goes out of business.

The amount of capital held affects returns for the owners (equity holders) of the bank.

A minimum amount of bank capital (bank capital requirements) is required by regulatory authorities.

How Bank Capital Helps Prevent Bank Failure:

When a bank becomes insolvent, government regulators close the bank, its assets are sold off, and its managers are fired. Owners of Low Capital Bank will find their investment wiped out, they clearly would have preferred the bank to have had a large enough cushion of bank capital to absorb the losses, like High Capital

We therefore see an important rationale for a bank to maintain a sufficient level of capital: A bank maintains bank capital to lessen the chance that it will become insolvent

What is the trade-off between safety and returns to equity holders?

Bank capital has both benefits and costs:

Bank capital benefits the owners of a bank in that it makes their investment safer by reducing the likelihood of bankruptcy.

But bank capital is costly because the higher it is, the lower will be the return on equity for a given return on assets.

To determine the optimal level of bank capital, managers must compare the benefit of having higher capital (increased safety) with the cost of higher capital (the lower return on equity for owners).

In more uncertain times (increased possibility of large losses on loans), bank managers might want more capital to protect the equity holders. Conversely, if they have confidence that loan losses won’t occur, they might want to reduce the amount of capital and thereby increase the return on equity.

How can you manage credit risk?

Screening and monitoring for asymmetric information

Adverse selection - collect reliable information

Covenants

Relationship management

Other credit risk management tools

Collateral and compensating balances: property promised to the lender as compensation if the borrower defaults. It lessens the consequences of adverse selection because it reduces the lender’s losses in the case of a loan default. It also reduces moral hazard because the borrower has more to lose from a default.

One form of collateral required when a bank makes commercial loans is called compensating balances: The borrowing firm must keep a required minimum amount of funds in a checking account at the bank. E.g., at least $1 million in its checking account for a $10 million loan, which can be taken by the bank to make up some of the losses if firm defaults.

Credit rationing: Another way to deal with adverse selection and moral hazard by refusing to make loans even though borrowers are willing to pay the stated interest rate, or even a higher rate. It takes two forms:

*Lender refuses to make a loan of any amount to a borrower, even if the borrower is willing to pay a higher interest rate.

*Lender is willing to make a loan but restricts the size of the loan to less than the borrower would like.

What is securitization?

Transforming otherwise illiquid financial assets (e.g., mortgages, auto loans) into marketable capital market securities.

Securitisation played an especially prominent role in the development of the subprime mortgage market in the mid 2000s.