CFA Level 1: Fixed Income

1/224

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

225 Terms

Fixed Income (L1)

A form of debt instrument for a firm, such as loans & bonds as a way of raising finance.

Maturity (L1)

A feature of fixed income securities that focuses on the end date of a security

Principle (L1)

A feature of fixed income securities that focuses on investment securities that offer dividend payments or fixed interest to investors until maturity.

On CFA Level 1 exam $1000 is the default, if value is not given.

Coupon (L1)

A feature of fixed income securities that serves as interest for a fixed income security that is paid regularly.

On CFA Level 1 exam semiannual is the default payment schedule if not given.

Issuer (L1)

A feature of fixed income securities, that focuses on the firm who issues the bond.

Seniority (L1)

A feature of fixed income securities that focuses on the levels of priority of total debt in relation to equity.

Contingency Provisions (L1)

A feature of fixed income securities, a call or put option that is embedded if certain conditions are met.

Yield Curve (L1)

A graph plotting interest rates also know as yields of bonds with equal credit quality but different maturity dates, showing the relationship between time to maturity and yield, typically used for U.S. Treasuries to reflect economic expectations.

Yield to Maturity (L1)

An Internal Rate of Returns (IRR) using all coupon, principle, and current price. Most commonly used and is used as a measure of return on an investments, and focus is when coupons are paid.

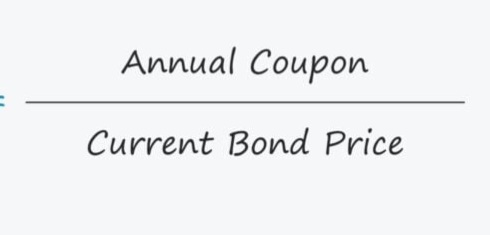

Current Yeild (L1)

A type of yield measurement that shows an investments annual income through a ratio of the annual coupon over the bond price.

Bond Indenture (L1)

The overall rights of the bondholder represented as a contract between the investor and the issuer.

Zero Coupon Bond (L1)

Traded at a discount with all interest earned at maturity, lower the price greater the given value of maturity.

Secured Bond (L1)

A type of bond that has a claim over an asset. Possess high seniority.

Unsecured Bond (L1)

A type of bond that has no claim over a specific asset. Has low seniority.

Covenants (L1)

Any requirement that are required to be met.

Negative Covenant (L1)

A type of covenant that restrict the users actions.

Affirmative Covenants (L1)

A type of covenant that lists the things a user must do.

Collateral (L1)

Also know as a lein or pledge. The asset that is used as a hold in the event of a default, and is used to regain money back to the investor.

Trustee (L1)

A type of administrator that manages the bond indentured, and represents the interest the investor to make sure all obligations are being met. Serves as an independent fiduciary.

Bullet Structure (L2)

Most common type of bond cash flow structure. Coupon payment is paid throughout the life of the bond, but the entire principle (par value) is repaid only at the maturity date.

Carries high risk for the issuer and investor because they concentrate their major cash flow at a single point in time. This creates a "spike" in risk.

Variable Interest (L2)

Has a coupon rate that changes periodically based on a Market Reference Rate (MRR). They have very low interest rates because as the MRR rises, the coupon also rises, thus keeping prices at par.

Amortizing Loans (L2)

Gradually paying off all or part of the principal during the life of the bond

Partial Amortizing Loans (L2)

Only a small partial amount of principal is repaid over the bond’s life, with a bigger lump sum balloon payment made at maturity of the bond.

In essence, it is a hybrid between a fully amortizing and a bullet bond.

Fully Amortizing Loan (L2)

Periodic interest and equal principal repayments are made over the life of the bond, such that the bond is full repaid at maturity.

In essence, the loan is paid little by little over its life.

Deferred Coupon (L2)

Have regular coupon payments but after a period of time.

Zero Coupon Bond (L2)

Pays 0 coupons doesn’t pay any coupons during its life time, only receives payments at the time of maturity.

Sink Fund Provision (L2)

A series of payment made over the life of the bond or after a specific date. by the issuer.

Serves as an element of risk to the investor, by having the issuer redeem some of the principal at random.

A requirement in the bond indenture that forces the issuer to retire a portion of the bond every year.

Waterfall Structure (L2)

Commonly seen with asset backed securities (ABS) & mortgage backed securities (MBS) in which thousands of small loans are bundled together into a one big pool.

Junior tranches (low seniority) will not be repaid until senior tranches (high seniority) will be repaid first.

All tranches will get their own respected coupons.

Payment in Kind (PIK) Bonds (L2)

A type of financing arrangement, with a high degree of risk. Issuer has a choice of pay periodic interest in the form of additional bonds (or sometimes common/preferred stock) rather than in cash.

Green Bond (L2)

A type of variable interest debt, in which environmental terms are set in relation to price increase. If terms are not met coupon payments increase, if terms are met coupon payments are decreased. Used as an incentive for firms to meet environmental goals.

Index Linked (L2)

A type of variable interest debt, is typically linked to an index such as inflation, interest or capital. Inflation index is the most common.

Market Reference Rate + Credit Spread (L2)

The foundation in how variable interest debt is priced and valued.

Step Up Bonds (L2)

A type of variable interest debt, a coupon rate that increases on a predetermined schedule.

Credit Linked (L2)

A type of variable interest debt, in which is determined by the issuers credit rating.

The coupon will increase if poor/ declining rating, due to more risk.

The coupon will decrease if good/ rising rating, due to less risk.

Convertible Bond (L2)

A bond that can be converted into equity, if the choice is given to the investor.

Warrant (L2)

An attached option that entitles the investor to buy stock at a fixed price at a fixed time.

Call Protection Period (L2)

A tool used to prevent early call back & to increase risk for the investor, due to unknown principle return.

American Call Option (L2)

A type of call provision that is also known as a continuously callable option. Specifies can call back after the call date period. Has high flexibility.

European Call Option (L2)

A type of call provision that has one specific date that can be called, has low flexibility.

Bermuda Call Option (L2)

A type of call provision that has a set list of specific dates, with medium flexibility & risk. Has medium flexibility, high risk & high yield.

Embedded Option (L2)

2 types callable & puttable option

A type of contingency provision that is built into the bond’s indenture.

Callable Bond (L2)

A type of bond with embedded option that gives the issuer (the borrower) the right, but not the obligation, to buy back (redeem) the bond before its scheduled maturity date. Has high risk for investor, thus generates a higher yield.

Puttable Bond (L2)

A type of bond with embedded option that gives the bondholder (the investor) the right, but not the obligation, to sell the bond back to the issuer before its maturity date. Has low risk for investor, thus generate a low yield curve.

Conversion Ratio (L2)

How many shares of common stock you will receive if you decide to exercise your option to convert the bond.

Conversion Value (L2)

How much to pay for an outright number of shares.

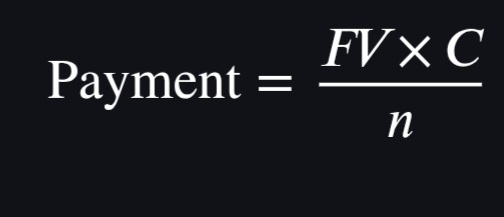

Periodic Coupon Formula (L1)

The coupon payment received each interest payment period.

n = payments per year

C = Coupon Rate

FV= Future Value

Domestic Bond (L2)

Bonds that are classified by having the same issuer, currency and investor.

Foreign Bond (L2)

Bonds that are classified by having a different issuer, but the same currency and investor.

Sukuk Bond (L2)

Bonds made adjusted to sharia law & compliance regards to interest and spending.

Global Bond (L2)

A type of eurobond that is classified by being able to be traded in both foreign and domestic markets.

Original Issue Discount (OID) (L2)

The discount that is considered when a bond is issued at any price below its par value. Usually determined if coupon is below Market Reference Rate (MRR).

Taxation for OID (L2)

Has to declare as taxable interest income each year.

Taxation for Standard Bond (L2)

Taxable interested income for the coupon payments each year. Taxed as capital gains during the sale of the bond.

Market Segments (L3)

Put in different categories such as types of issuers, types of markets, credit quality, ESG factors, currency, geography and etc.

Credit Ratings Provider (L3)

Top 2 providers are Moody’s and S&P

Aggregate Index (L3)

A type of fixed income index with a broad selections, and sectors. Certain fixed incomes are excluded.

Example: Bloomberg Barclay Aggregate Index

Narrower Focus (L3)

A type of fixed income index with a pure based selection, often referred as a pure style index.

Example: JP Morgan Emerging Markets Bond Index Plus

ESG Incorporated Factors (L3)

A type of fixed income index that uses a minimum ESG rating.

Example: Bloomberg- Barclays MSCI Euro Corporate Sustainable SRI Index

Credit Ratings (L3)

A tool that is used to reflect the yield, the poorer the rating is equal to high risk for the investor, but will have a chance for a higher return.

Investment Grade (L3)

A credit quality tier that is reflected by bonds issued by companies or governments that have a high capacity to meet their financial obligations.

Characteristics: Low default risk.

Lower interest rates (coupons) than High Yield.

Highly sensitive to interest rate changes (High Duration)

High Yield (L3)

A credit quality tier that is reflected by bonds with a higher probability of default. Investors are compensated for this extra risk with a significantly higher interest rate. Also known as a junk bond.

Characteristics: * Higher default risk.

Higher coupons to attract investors.

More sensitive to the business cycle and the issuer's specific financial health than to general interest rates.

Behave more like "equities" (stocks) than traditional bonds.

Risk Free (L3)

A credit quality tier that reflects assets with no risk of default and usually no reinvestment risk if it matches the investor's time horizon.

Cut of Point from Investment Grade to High Yield for S&P (L3)

BBB- (Investment Grade) to BB+ (High Yield

Cut of Point from Investment Grade to High Yield for Moody’s (L3)

Baa3 - (Investment Grade) to Ba1 (High Yield

Roll Over Risk (L4)

A type of liquidity and credit risk in which, an issuer will not be able to refinance, their maturing short-term debt with new debt.

Treasury Bill (L3)

A type of fixed income security with a short (1 year ) maturity length and a risk free credit quality.

Highly liquid, short-term instruments used for cash management.

Holds low zero default risk.

Asset Backed Commercial Paper (ABCP), Repo, and Commercial Paper (L3)

A type of fixed income security with a short maturity length (1 year) and a investment grade credit quality.

Highly liquid, short-term instruments used for cash management.

Rated BBB- or Baa3 and higher.

Treasury Notes (L3)

A type of fixed income security with an intermediate maturity length (1 - 10 Year), and a risk free credit quality.

They often serve as a "sweet spot" for yield during times of economic transition or when expecting a flattening yield curve, offering better risk-adjusted returns than longer-dated debt.

Holds 0 default risk.

Unsecured Corporate Bonds and Asset Backed Securities (ABS) (L3)

A type of fixed income security with an intermediate maturity length (1 -10 Years), and an investment grade credit quality.

They often serve as a "sweet spot" for yield during times of economic transition or when expecting a flattening yield curve, offering better risk-adjusted returns than longer-dated debt.

Rated BBB- or Baa3 and higher.

Secured Corporate Bonds and Leveraged Loans (L3)

A type of fixed income security with an intermediate maturity length (1-10 Years), and a high yield credit quality.

They often serve as a "sweet spot" for yield during times of economic transition or when expecting a flattening yield curve, offering better risk-adjusted returns than longer-dated debt.

Much more riskier, due to higher default risk.

Treasury Bonds (L3)

A type of fixed income security with a long maturity length (10+ years), and a risk free credit quality.

Has a long sensitivity to interest rate change,

Holds 0 default risk.

Unsecured corporate bonds & Mortgage Backed Securities (L3)

A type of fixed income security with a long maturity length (10+ years), and an investment grade credit quality.

Has a long sensitivity to interest rate changes.

Rated BBB- or Baa3 and higher.

Primary Market (L3)

The market where newly issued bonds are sold via public/private sales.

Shelf registration

Auctions

Underwritten offering/best efforts

Secondary Market (L3)

Where investors buy and sell previously issued bonds, either on some trading platforms, but mainly through OTC platforms.

Bid/Offer Prices

Low Risk Investor (L3)

Central Banks & Financial Intermediaries

High Risk Investor (L3)

Asset Managers, Hedge Fund Managers, Distressed Debt Funds

Financial Intermediaries & Central Banks Position (L3)

Position: Range of Maturities

Credit Quality: Risk Free

Pension Funds Position (L3)

Position: Long Term

Credit Quality: Risk Free / Investment Grade

Money Market Fund Position (L3)

Position: Short Term

Credit Quality: Risk Free/Investment Grade

Corporate Issuers Position (L3)

Position: Short Term

Credit Quality: Investment Grade

Bond Funds Position (L3)

Position: Intermediate Term

Credit Quality: Investment Grade

Asset Managers, Hedge Fund, Distressed Debt Funds Position (L3)

Position: Intermediate Term

Credit Quality: Gradually moving from Investment Grade to High Yield

Repo Haircut (L4)

The percentage reduction applied to the market value of collateral to determine the amount of cash a lender will provide in a repurchase agreement. It serves as a safety net to protect the lender against potential drops in the collateral's value or the borrower's default.

Expressed as: Security Price - Purchase Price / Security Price

Sovereign Government Issuer (L15)

National government issues bonds to raise funds for public goods and services and investments into public infrastructure.

Non-sovereign Government Issuer (L15)

States, provinces, counties, and entities create & issue bonds to fund & provide services.

Cross Default Clause (L14)

Clauses if issuer defaults on one bond, it will default on all bonds that are issued.

Credit Risk (L14)

The risk the borrower fails to pay these promised payments.

Default (L14)

The consequent of the borrower not paying back the creditor. Usually dependent specifically to the borrower & to general economic conditions.

Expected Loss (L14)

The average amount a firm expects to lose on an exposure.

Loss Severity (L14)

The probable size, dollar lost, or financial magnitude when an incident occurs.

Bottom Up (L14)

Borrower specific factors in the probability of credit risk.

Capacity

Capital

Collateral

Covenants

Character

Capacity (L14)

A bottom up feature that uses the ability to make payments on time, by having enough cash available to make payments.

Dependent on factors such as Sales, or Taxes.

Capital (L14)

A bottom up feature that uses other sources of equity that can be used to service the debt.

More capital means more likely to service the debt.

Collateral (L14)

A bottom up feature that uses the value of such asset that is attached to a debt, and its value in the event of a default.

Covenants (L14)

A bottom up feature that focuses on the terms an conditions of the debt, the stricter the covenants the higher the probability of default.

Character (L14)

A bottom up feature that focuses on personality and integrity of an individual to service debt.

Expected Recovery Rate (L14)

Proportion of a claim an investor will recover, given default.

Expected Exposure (L14)

A credit risk calculation that is determined by the difference of what the investor is owed and the value of collateral available.

Credit Spread: Credit Risk (L14)

Express the credit spread as a function of the risk of default and the expected recovery.

Loss Given Default Percentage (L14)

The percentage of a lender's exposure that is expected to be lost if a borrower defaults, after accounting for any recoveries from collateral, guarantees, or bankruptcy proceedings. A component of calculating expected loss in credit risk analysis.