MF Unit 1- Introduction to Microfinance

1/20

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

21 Terms

What is Microfinance?

Microfinance refers to the provision of a wide range of financial services—deposit, loans, insurance, payment services, money transfer—to poor and low-income households who lack access to formal banking. It is provided by formal institutions (rural banks, cooperatives), semiformal institutions (NGOs), and informal lenders.

Poor households need microfinance for:

Life-cycle needs: education, marriage, old age, festivals.

Emergency needs: medical shocks, accidents, natural calamities.

Investment needs: business expansion, asset purchase, agriculture.

Why is microfinance important for poverty reduction?

Microfinance helps poor households smooth consumption, manage risks, build assets, improve income, expand microenterprises, and improve quality of life. It supports better resource allocation, technology adoption, and financial inclusion of women.

What are the needs that create demand for microfinance?

Poor households need microfinance for:

Life-cycle needs: education, marriage, old age, festivals.

Emergency needs: medical shocks, accidents, natural calamities.

Investment needs: business expansion, asset purchase, agriculture.

What are the key characteristics of microfinance services?

High ease of access

Low to medium transaction cost

Short lead time for credit

Short & flexible repayments

Medium–high interest rates

Repeat borrowing allowed

Simple loan procedures

Collateral not required

Why is a development strategy needed for microfinance?

Because microfinance grew without a clear framework. A strategy helps improve policy environment, regulate MFIs, address market failures, ensure sustainability, expand outreach, and integrate microfinance into country-level financial systems

What are the core elements of ADB’s Microfinance Development Strategy?

A Development strategy helps improve policy environment, regulate MFIs, address market failures, ensure sustainability, expand outreach, and integrate microfinance into country-level financial systems.

The Asian Development Bank (ABD) is a regional development bank established 19 December 1966 which is headquartered in Philippines.

The Asian Development Bank aims for an Asia and Pacific free from poverty.

Also for social and economic development of the Asian and Pacific countries.

To boost cooperative and regional growth among member countries.

Goal and Purpose:

The goal of ADB’s proposed Microfinance Development Strategy is to ensure permanent access to institutional financial services for a majority of poor and low-income households and their microenterprises.

The purpose is to support the development of sustainable microfinance systems that can provide diverse services of high quality.

Therefore, the strategy focuses on:

(i) creating a policy environment beneficial to microfinance

(ii) developing financial infrastructure,

(iii) building financial institutions,

(iv) supporting pro-poor innovations,

(v) supporting social intermediation

STRATEGIES

POLICY ENVIRONMENT-

Financial sector reform programs have resulted in a general improvement of the policy environment in the Region.

However, in many countries, lack of an enabling policy environment for microfinance continues to be a major constraint.

The policy reforms will focus on interest rate reforms relevant for microcredit and savings within the broader financial sector reforms, creating an environment sufficiently flexible to accommodate a wide range of MFIs and OFIs to meet the diverse demand, and redefining the role of the state and the central banks in microfinance development to facilitate participation of private sector financial institutions.

It is necessary to closely consult with all major stakeholders in formulating microfinance policy reform programs for DMCs.

FINANCIAL INFRASTRUCTURE-

Underdeveloped financial infrastructure continues to constrain the deepening and broadening of microfinance services and participation of private institutions as service providers.

MFIs can develop sustainable commercial services on a permanent basis, and expand their scope of operations and outreach, only if they operate within an appropriate financial infrastructure.

ADB’s assistance will focus on critical elements of financial infrastructure, such as information systems and training facilities necessary for microfinance development.

INSTITUTIONAL DEVELOPMENT -

ADB, in consultation with its DMCs, has identified institutional capacity building as an important requirement for sustainability and expanding outreach.

Financial viability is critical for expanding the outreach.

Only viable financial institutions involved in microfinance can ensure permanency of services to an increasing number of the poor and contribute significantly to poverty reduction.

The institutional development activities also need to encompass:

(i) development of training facilities for the microfinance sector,

(ii) ownership and governance of financial institutions involved in microfinance,

(iii) development of a diversified menu of products and services attractive to the poor

(iv) management information systems and accounting policies and practices,

(v) management of portfolio quality and growth, and

(vi) systems and procedures and financial technology for reducing transaction costs.

PRO- POOR INNOVATIONS-

Private institutions are, in general, reluctant to invest in financial technology and innovative programs oriented to the poor because they tend to believe that the market among the poor is limited and externalities will not allow them to profit from their investments.

Therefore, to ensure that the financial institutions will continue to expand the services to these categories, ADB will support innovative programs and development of financial technology that contribute to breaking these barriers through pilot projects and other measures that aim at establishing sustainable linkages between formal financial institutions and informal service providers.

SOCIAL INTERMEDIATION-

Social Intermediation is necessary to increase the capacity of the majority of the poor to access and productively use microfinance services. The strategy emphasizes supporting investments aimed:-

To improve the capacity of poor to actively participate in microfinance markets,

Awareness building programs on a broad range of microfinance services,

Information dissemination on service providers,

Basic literacy, numeracy, and skills training for women, ethnic minorities,

and other disadvantages groups

Social mobilization for formation of community based organisation.

About the strategy:-

ADB needs a broad strategy because of the diversity of microfinance issues in its DMCs and the flexibility required to address these issues in different country contexts.

Hence, ADB will catalyze expanding the supply of microfinance and strengthen the capacity of the potential clients to access the services.

• On the supply side, the strategy focuses on building financial systems that can grow and provide financial services on a permanent basis to an increasing proportion of the poor, and promotion of pro-poor innovations.

On the demand side, the strategy supports investments in social intermediation.

what is the Strategic focus of development strategy

Policy Environment- Financial sector reform programs have resulted in a general improvement of the policy environment in the Region. However, in many countries, lack of an enabling policy environment for microfinance continues to be a major constraint. The policy reforms will focus on interest rate reforms relevant for microcredit and savings within the broader financial sector reforms, creating an environment sufficiently flexible to accommodate a wide range of MFIs and OFIs to meet the diverse demand, and redefining the role of the state and the central banks in microfinance development to facilitate participation of private sector financial institutions. It is necessary to closely consult with all major stakeholders in formulating microfinance policy reform programs for DMCs.

Financial Infrastructure-

|

Institutional Development-

INSTITUTIONAL DEVELOPMENT

ADB, in consultation with its DMCs, has identified institutional capacity building as an important requirement for sustainability and expanding outreach.

Financial viability is critical for expanding the outreach.

Only viable financial institutions involved in microfinance

can ensure permanency of services to an increasing number of the poor and contribute significantly to poverty reduction.

The institutional development activities also need to encompass:

(i) development of training facilities for the microfinance sector,

(ii) ownership and governance of financial institutions involved in microfinance,

(iii) development of a diversified menu of products and services attractive to the poor

(iv) management information systems and accounting policies and practices,

(v) management of portfolio quality and growth, and

(vi) systems and procedures and financial technology for reducing transaction costs.

pro poor innovations

PRO-POOR INNOVATIONS |

• Private institutions are, in general, reluctant to invest in financial technology and innovative programs oriented to the poor because they tend to believe that the market among the poor is limited and externalities will not allow them to profit from their investments. Therefore, to ensure that the financial institutions will continue to expand the services to these categories, ADB will support innovative programs and development of financial technology that contribute to breaking these barriers through pilot projects and other measures that aim at establishing sustainable linkages between formal financial institutions and informal service providers. |

Social intermediation- It is necessary to increase the capacity of the majority of the poor to access and productively use microfinance services. The strategy emphasizes supporting investments aimed:-

To improve the capacity of poor to actively participate in microfinance markets,

Awareness building programs on a broad range of microfinance services,

Information dissemination on service providers,

Basic literacy, numeracy, and skills training for women, ethnic minorities,

and other disadvantages groups

Social mobilization for formation of community based organisation.

What drives demand for microfinance?

Demand comes from poor households and microenterprises for savings, microcredit, insurance and payment services. Poor households—especially women—need safe deposit services and small, frequent loans for consumption and investment

This demand reflects the importance of savings for these households and microenterprises for a variety of reasons.

The poor need to save for emergencies, investment, consumption, social obligations, education of their children and many other purposes.

They have the capacity and willingness to save. Savings are important for microenterprises and provide them with a major source of investment funds.

The large demand for deposit services among the poor is confirmed by empirical evidence.

The demand for microcredit that originates both from households and microenterprises is also large.

Poor households in the Region require microcredit to finance livelihood activities, for consumption smoothening, and to finance some lumpy nonfood expenses for purposes such as education (e.g., school fees and books), housing improvements, and migration.

Many Asian countries have numerous small farms and their operators also require microfinance services.

The other source of demand is non-farm microenterprises, which cover a wide array of activities such as food.

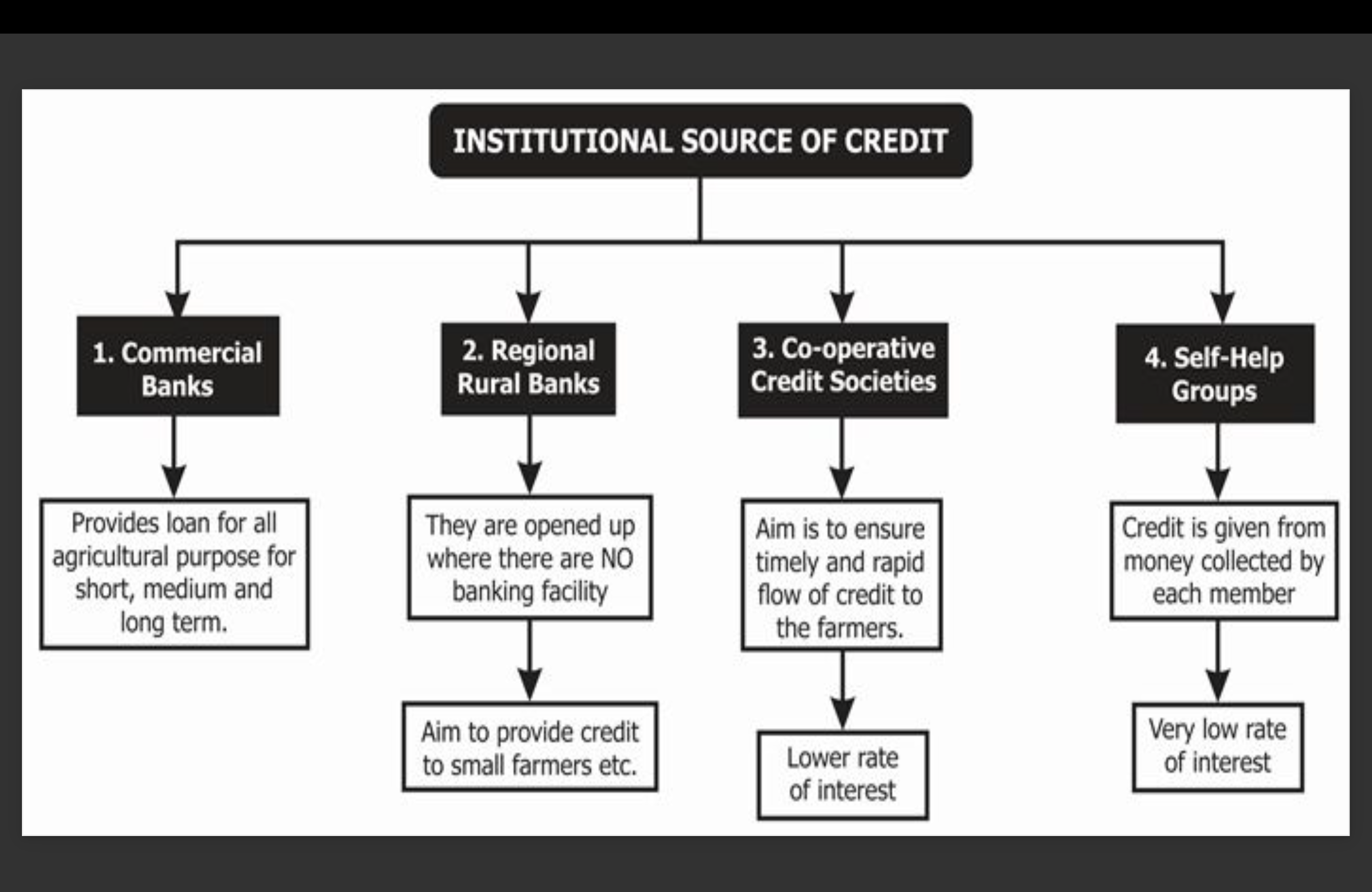

who supplies microfinance service?

supply of microfinance service can be divided into 2 parts:-

institutional sources- NABARD, SIDBI, RRB etc

Non institutional sources- Moneylenders, Relatives, friends etc

Institutional/formal sources

1) NABARD (National Bank for Agriculture and Rural Development) :

NABARD was set up by RBI on 12 July 1982.

NABARD is an apex Development Bank authorised for providing and regulating credit

and other facilities for the promotion and development of agriculture, small-scale industries, cottage and village industries, handicrafts and other rural crafts and other allied economic activities in rural areas with a view to promote integrated rural development and prosperity and for matters connected therewith.

More than 50% of the rural credit is disbursed by the Co-operative Banks and Regional Rural Banks. NABARD is responsible for regulating and supervising the functions of Co-operative banks and RRBs. NABARD works towards providing a strong and efficient rural credit delivery system, capable of taking care of the expanding and diverse credit needs of agriculture and rural development.

2) SIDBI (Small Industries Development Bank of India) :

The SIDBI was established on 2nd April 1999. The SIDBI is subsidiary of IDBI (Industrial Development Bank of India).

SIDBI had entered into microfinance and providing both financial and non financial assitance to microfinance clients.

SIDBI provides Capacity Building Support(CBS) to the MFIs/NGO to expand their microcredit operations.

It targets MFIs who have strong credit and recovery mechanism,MIS and internal control for tracking of credits and support to borrower.

Non institutional/informal sources:-

1) Money Lender:

• Until recent past, the money lenders have enjoyed monopoly in the supply of very

small-scale finance.

• Money lenders provide both production and consumption credits, and these credits are disbursed with customized repayment schedule with high interest.

• Transaction cost and transition period are less relative to formal credit.

2) Friends, Relatives and Neighbors:

They provide credit subjected to their financial strength at a particular time.

Transaction cost and transition period for loan are relatively less.

Like moneylenders, friends and relatives do not provide other microfinance products .

Rate of interest and repayment period are not very rigid, rather the rate and period are determined jointly by the lender and borrower.

Difference between institutional sources and non institutional sources?

non institutional | Insininstitutionaltutiona l Sourcesin | |

|

| |

|

| |

What are the objectives of microfinance?

1) Provide Access to Funds- Typically, the poor acquire financial services like loans through informal relationships. These loans, however, come at a high cost per dollar loaned and can be unreliable. Furthermore, banks have not traditionally viewed poor people as viable clients and often will reject them due to unstable credit or employment history and lack of collateral. MFIs dismiss such requirements and provide small loans at low interest rates, thus providing MFIs the funds they need to continue operation.

2) Encourage Entrepreneurship and Self-Sufficiency- Underprivileged people may have potentially profitable business ideas, but they cannot put them into action because they lack sufficient capital for start-up costs. Microcredit loans give clients just enough money to get their idea off the ground so they can begin turning a profit. They can then pay off their micro-loan and continue to gain income from their venture indefinitely.

3) Manage Risk- Microcredit can give impoverished people enough financial stability to cross from simply surviving to accruing savings. This gives them protection from sudden financial problems that could have been devastating. Savings also allow for educational investment, improved nutrition, better living conditions and reduced illness. Micro-insurance provides people the ability to pay for health care when needed, so they can receive treatment for health conditions before they become grave and more costly to treat.

4) Empower Women- Women make up a large proportion of microfinance beneficiaries. Traditionally, women (especially those in underdeveloped countries) have been unable to readily participate in economic activity. Microfinance provides women with the financial backing they need to start business ventures and actively participate in the economy. It gives them confidence, improves their status and makes them more active in decision-making, thus encouraging gender equality. According to CGAP, long-standing MFIs even report a decline in violence towards women since the inception of microfinance.

5) Community-Wide Benefits- Generally speaking, microfinance institutions seek to reduce poverty worldwide. As they obtain funds and services from MFIs, recipients gain enormous financial benefits which trickle down to others in their families and communities. New business ventures can provide jobs, thereby increasing income among community members and improving their overall well-being. Microfinance services gives hope to people who previously had little or no opportunity to be self-sufficient.

What are the key tools of microfinance? or poverty assessment tools of microfinance?

1)Cashpor Housing Index-Cashpor micro credit is based in Uttar Pradesh carries out poverty assessment to select their client. The objective of the cashpor group is reduction of poverty through the sustainable financial services to poor women. They use an index called housing index.

The CASHPOR Housing Index is a cost effective method to identify poor households through visual inspection from the road or lane outside the house.

It uses a point system that allocates a predetermined number of each main component of house, Example- its size, the material of roof and walls and its structural condition .

The Housing Index has only two indicators:

1) Height of the wall and material used

More than 5 feet and made of brick- 4

More than 8 feet and made of mud -2

More than 4 feet but less than 8 feet and made of mud -1

2) Material of the roof

Concrete/ new tiles-2

Old tiles/GI sheet-1

Plastic/ leaves/straw-0

Maximum score Poverty status- 6

Very poor - 2 OR LESS

Moderate poor- 3

Non poor -4 OR MORE

The scoring method can help in identifying poor clients to segregate the poorest from the poor.

However many donors also like to see the poverty focus of an MFI and therefore want to know the economic profile of clients of an MFI.

This can be done by conducting a poverty-focussed assessment of an MFI called Poverty Audit. CGAP has developed one poverty audit tool.

2) CGAP Poverty Audit- The CGAP poverty audit tool provide transparency on poverty outreach of MFI.

Primarily designed for owners and investors who would require a more

standardized, globally applicable and rigorous set of indicators to make to make

poverty focussed funding decisions.

This tool involves service of 200 randomly selected clients household and 300

non-client household.

Bivariate analysis( relationship between two pairs of variables here are clients and

non-clients.)

The CGAP poverty audit tool concentrates on 5 set of issues:

a) Vision- The stated vision of the program and how leadership commitment and institutional history provides validation for it.

b) Targeting strategy and poverty outreach- The targeting strategy and how it reflects the poverty orientation of the program the depth of outreach of the program that is whether the program has adequate methods to identify the client which the MFI wants to target.

c) Staff client interface- staff client interface and assessment of staff responsiveness to client welfare this is to find out how sensitive the staff are its clients and how is the relationship

d) Product and services- The extent to which the thinking behind product design and changes them from an understanding of poverty and vulnerability.

e) Impact- The extent to which program participation has contributed to changes in client well-being.

3) Social Rating- Social rating is relatively new concept in which the organisations are rated and given a grade on the social performance of the organisation rather than financial performance.

A major concern is whether MFI taking a commercial loan will be able to repay it or not. To make this judgement rating agencies have parameters, which mainly inclined towards financial performance.

Based on the MFI performance on these parameters, a grade is given to the MFI which shows the level of its creditworthiness .

4) Progress out of poverty index(PPI)- PPI is both management and a measurement tool.

It allows microfinance institutions to better determine their client’s need which programs

are most effective, how quickly client leave poverty and what helps them to move out of the poverty faster .

PPI is a unique composite of easy to collect, country-specific, non-financial indicators such as family size, no.of attending school, the type of housing and what the family typically eats.

By using Benchmarks and Standards of measurement that produce reliable information manager can build client profiles and track how they change over time.

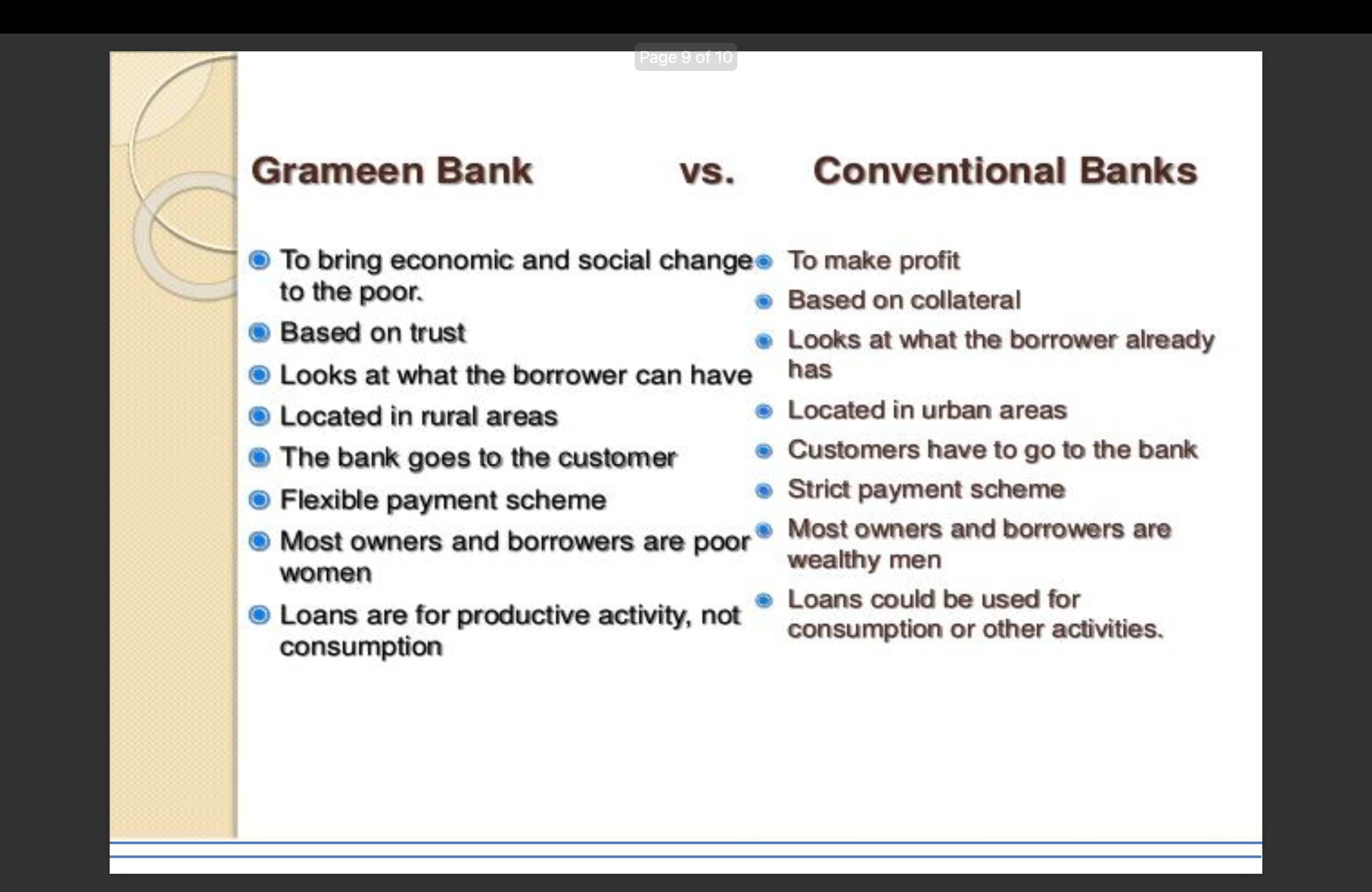

What is the Grameen Bank model? How has Grameen Bank impacted poverty?

Grameen Bank (GB) has reversed conventional banking practice by removing the need for collateral and created a banking system based on mutual trust, accountability, participation and creativity.

GB provides credit to the poorest of the poor in rural Bangladesh, without any collateral.

At GB, credit is a cost effective weapon to fight poverty and it serves as a catalyst in the over all development of socio-economic conditions of the poor who have been kept outside the banking orbit on the ground that they are poor and hence not bankable.

Professor Muhammad Yunus, the founder of “Grameen Bank” reasoned that if financial resources can be made available to the poor people on terms and conditions that are appropriate and reasonable, “these millions of small people with their millions of small pursuits can add up to create the biggest development wonder.”

As of November, 2019, it has 9.60 million members, 97 percent of whom are women. With 2,568 branches, GB provides services in 81,678 villages, covering more than 93 percent of the total villages in Bangladesh.

Objectives of Grameen Bank

To extend the banking facilities to poor men and women

Eliminate the exploitation of the poor by moneylenders

Create opportunities for self employment

Bring the disadvantaged , mostly women from the poorest households

within the fold of an organisational format whhich they could

understand and manage by themselves

Reverse the age – old vicious circle of ‘ low-income,low saving and low

investment’ into a virtuous circle of low-income, injection of credit, investment,more income, more saving , more investment, more income.

Feature of Grameen Bank

The significant feature of the microfinance programme is that it is a tool for empowerment of the poorest women. It is essentially for promoting self employment as the opportunities of wage employment are limited in developing countries. Microfinance increases the productivity of self employment in the informal sector of the economy - generally used for

(a) direct income generation

(b) rearrangement of assets and liabilities for the household to participate in future opportunities and

(c) consumption needs.

It is not just a financing system, but a tool for social change, especially for women. It is aimed at the poorest. Most distinctive feature of Grameen credit is that it is not based on any collateral or legally enforceable contracts. It is based on "trust", not on legal procedures and system.

The tasks performed in Grameen system are:

• Holding weekly meetings which are being supervised by a MFI staff

who maintains the records and savings and repayments are collected and handed over to the MFI office

• Guaranteeing loans to their individual members, by accepting joint and several liability and by accepting that no members of a group are able to take new loan if any default in the group

• Appraising fellow members’ loan applications and ensuring that their fellow members maintain their regular savings contributions and loan repayments.

Based on the assumption of 2:2:1 staggering

grameen bank vs conventional banks

what is group lending?

Group lending generally refers to the arrangements by individuals without collateral who get together and form groups to obtain loans from a lender.

The special feature of the Classic Grameen Bank Model is that the loans are made individually to group members but all the group face consequences if any member runs into serious repayment difficulties.

The large group of villagers is sub-divided into eight,five persons group.

The fundamental idea of group responsibilities( sometimes called joint liability) coupled with regular group meetings is common across approaches.

The weekly group meetings have some advantages for the lender and customers.

Transaction cost are greatly reduced for the loan officer since the multiple savings and loan transactions of 40 people can take place in a short block of time.

Joint liability Clause is used in contract, it can mitigate the moral hazard, adverse selection and enforcement problems that crippled previous attempts at lending to the poor by outside financial institutions

Muhammad Yunus and his associates soon realised that requesting potential borrowers to organise themselves into groups had another advantage.

The cost of screening and monitoring loans and the cost of enforcing that the payments would be substantially reduced.

To Institute this systematically, the bank developed a system in which two members of each 5 person group receive their loans first if all installment are paid on time, the initial loans are followed four to six weeks later by loans to two other members ,and then after another four to six weeks by loan to the group chairperson( This pattern is known as 2:2:1 staggering.)for example: if a member of a group fails to attend a meeting the group leader the pays on her behalf and thus the credit record of the absentee borrower remains clean,and so does the group’s.

• If serious repayment problems emerge, all group members will be cut off from future borrowing.

• If the relationship between Grameen and borrower continuous loan sizes grow over the year and credit histories are built up. Eventually loan may be large enough to build or repair a house or to make lumpy investments like purchasing a rickshaw, sending a child to school.

problems with group lending?

Asymmetric information problems

• Adverse selection: individuals who know they are likely to default select into borrowing pool, raising default rates and interest rates for everyone

– “Hidden type”, “hidden information”

• Moral hazard

– Individuals exert less effort than the lender would desire, raising default rates and interest rates for all

– Ex-ante: less effort is exerted to make the “project” succeed

– Ex-post: even if project succeeds, may voluntarily default

– “Hidden action”

overcoming or mitigating problems of group lending

ADVERSE SELECTION

The adverse selection problem occurs when lenders can't distinguish risky borrows from safer borrowers.

If lenders could distinguish by risk type they could charge different interest rate to different type of borrowers.

But with the poor information options are limited.

They implement Assortative Matching : People are given the choice to choose the second person on their own.

If anyone defaults , the second person is liable to pay the whole amount.

risky borrowers with risky and safe with safe borrowers automatically into homogeneous groups

MORAL HAZARD

take on excessive risks or reduce effort in their projects, knowing the consequences (potential default) will be shared by the entire group.

Moral hazard in lending refers to situations where the bank was tied to an observable choices made by borrowers.

Once loans have been granted , then bank may then face moral hazard problem due to difficulty of monitoring borrower’s actions.

two parts:-

Ex ante Moral hazard related to the idea that unobservable actions or efforts are taken by borrower after the loan has been disbursed but before project returns are realized. These action affect the probability of a good realization of returns.

The term ex-post refers to difficulties that emerge after the loan is made and the borrower has invested and made his decision regarding effort. This is also termed the enforcement problem.

What happens if, after the cashflows are generated, the borrower decides not to pay?

If the cashflows are not observable or it is costly to verify them, the borrower may end up not paying back the loan.

what is stepped lending and repeat loan?

Stepped lending/Progressive lending, in which a borrower begins with a very small loan, repays it, and qualifies for successive loans at higher values.

According to Hulme and Mosley, “Progressive lending is a practice of

increasing the credit limit of borrowers by a proportion dependent on their previous repayment record.”

They visualise the relationship between utility maximising lender and borrower with a game in three stages which may or may not repeat themselves – initial agreement, implementation and decision on whether and on what terms to grant repeat finance.

They referred these three stages as Acts 1, 2 and 3, respectively.

In the first stage, Act 1, the lender gives a loan of standard size X at standard interest rate r.

In stage two, Act 2, the borrower receives returns on the project for which the loan is being used and repays a proportion of the loan; in the event that repayment is not made in full, the lender punishes this behaviour by refusing to provide repeat finance.

In the last stage, in Act 3, borrower does not repay the loan but the lender still provides a loan because the lender’s strategy of ‘lending into the recipient’s arrears’ to pay back the arrears on the previous loan.

Thus, progressive lending schemes expand the opportunity cost of non-repayment and thereby discourage strategic default even further. On the other hand, it is obvious from the figure that the successive repayment of loan will enhance the size of loan through new loan contracts between the lenders and borrowers and further increases the loan cycles.

what are the flexible approaches to collateral?

Collateral is an asset pledged by a borrower to a lender until a loan is paid back. If the borrower defaults, then the lender has the right to seize the collateral and sell it to pay off the loan.

Collateralization is closely linked to loan size i.e the larger the loan, the more likely is a collateral requirement.

There is a close link between loan size and the extent and quality of collateralization: the larger a loan, the more the bank will be inclined to require a form of collateral that retains its value over time and and that can be easily sold, taking into account the respective transaction costs involved.

If bank doesn’t keep collateral , the probability of defaulting will be high. If people know that their collateral is with the bank , they know that it can be seized.

One aspect of microfinance is that most clients are too poor to able to offer collateral. Loans are secured through non-traditional means like group lending but in practice some microfinance lenders do require collateral, the best-known being Indonesia BRI (Bank Rakayat Indonesia).

in rural albania, for example micro lenders require tangible assets rural areas- land, cattle, livestock, housing urban areas- home, business

Bank doesn’t need to take possession of and sell the collateral for this constraint to bind ; it only needs to deny the borrower access to collateral . This also says that at a given interest rate , average default rates will fall , reducing losses for the bank. In the way , adding a collateral requirement can help the bank improve profitabilty without raising interest rates or even while reducing charges.

What is character-based lending?

Lending based on a borrower’s trustworthiness, reputation, social standing, and credit discipline, rather than physical collateral. Group lending embodies this principle by using social collateral.

What is cash-flow-based lending?

Lending decisions based on the borrower’s income flow, repayment capacity, and economic activity, rather than assets. MFIs assess loan cycles, credit usage patterns, savings behaviour, etc.