accounting final formulas

1/9

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

10 Terms

High-low method formula (variable costs)

Highest in total costs - lowest in total costs/ highest in units produced - lowest in units produced.

Ex: ($14,740-$11,100/ $9,800-$7,000)= $1.30 per unit

High-low method formula (fixed costs)

Highest in total costs - highest in units produced x variable cost

Ex: $14,740 x 12,740→(9,800 x 1.30)= $2,000

Write cost equation using these numbers, $2,000 and $1.30 per unit

Cost = $2,000 + ($1.30 × units produced)

Unit contribution margin equation

Unit Selling Price − Unit Variable Costs = Unit contribution Margin

$500 − $300 = $200

Contribution margin ratio equation

Unit Contribution Margin ÷ Unit Selling Price = Contribution Margin Ratio

$200 ÷ $500 = 40%

Total contribution margin equation

Total sales revenue - total variable costs= total variable costs

Equation for break-even point

Fixed Costs ÷ Unit Contribution Margin = Break-Even Point in Sales Units

$200,000 ÷ $200 = 1,000 units

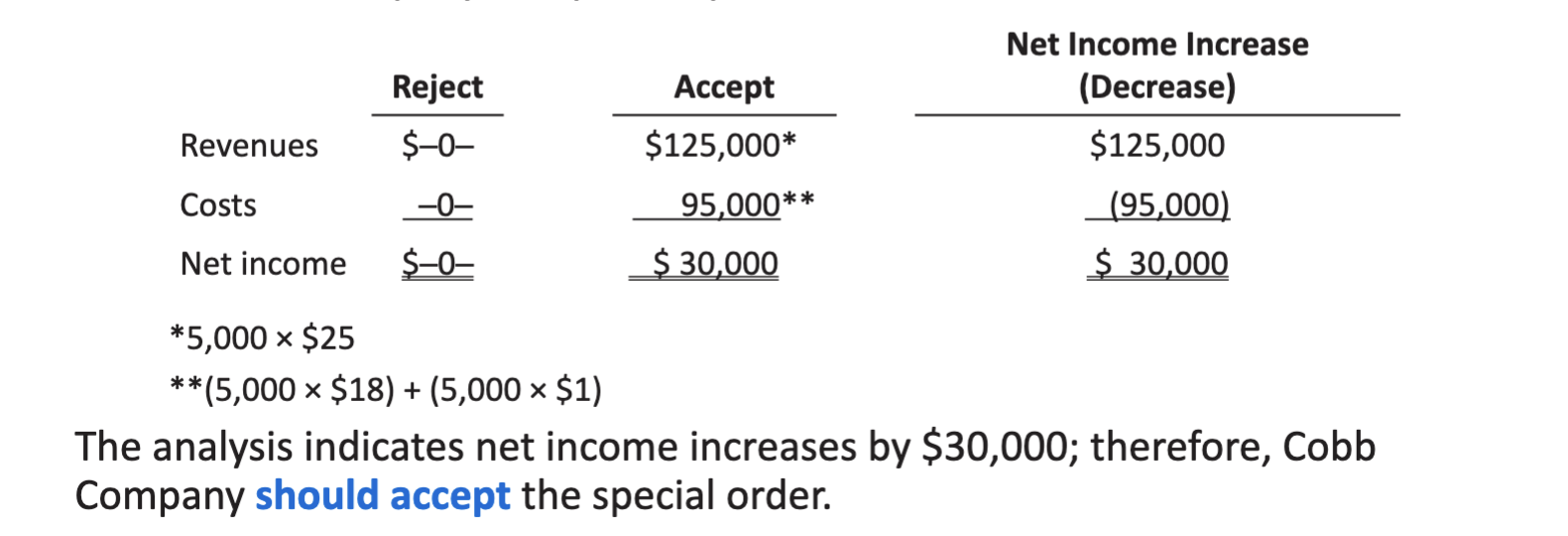

Special Order: Reject or Accept

Cobb Company incurs costs of $28 per unit ($18 variable and $10 fixed) to make a product that normally sells for $42. A foreign wholesaler offers to buy 5,000 units at $25 each. The special order results in additional shipping costs of $1 per unit. Compute the increase or decrease in net income Cobb realizes by accepting the special order, assuming Cobb has excess operating capacity.

Should Cobb Company accept the special?

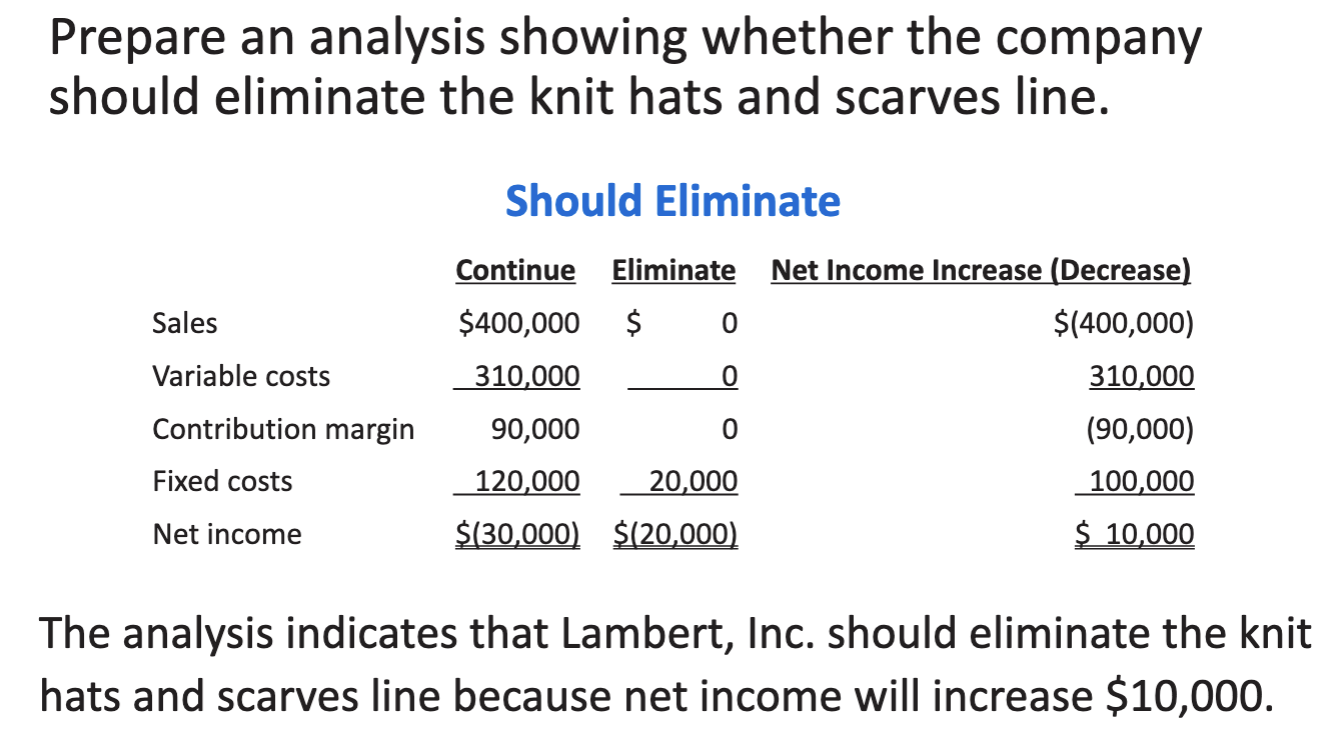

Continue vs. eliminate an unprofitable segment:

Lambert, Inc. manufactures several types of accessories. For the year, the knit hats and scarves line had sales of $400,000, variable expenses of $310,000, and fixed expenses of $120,000. Therefore, the knit hats and scarves line had a net loss of $30,000. If Lambert eliminates the knit hats and scarves line, $20,000 of fixed costs will remain.

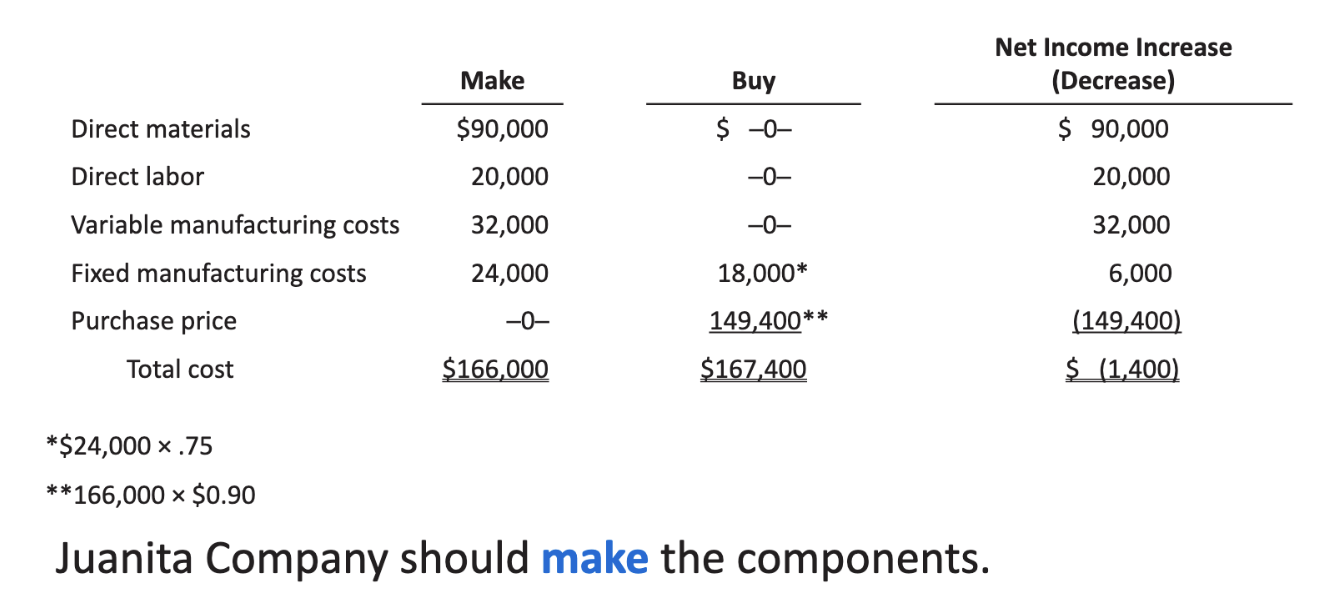

Make or Buy

Juanita Company must decide whether to make or buy some of its components for the appliances it produces. The costs of producing 166,000 electrical cords for its appliances are as follows.

Direct materials: $90,000 Variable overhead: $32,000

Direct labor: 20,000 Fixed overhead: 24,000

Instead of making the electrical cords at an average cost per unit of $1.00 ($166,000 ÷ 166,000), the company has an opportunity to buy the cords at $0.90 per unit. If the company purchases the cords, all variable costs and one-fourth of the fixed costs are

Eliminated. Make or Buy?