Week 11

1/30

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

31 Terms

excess burden formula

amount wlerfare is reduced minus the amount of tax collected

objectives of tax

raise revenue, redistrubtion, improve allocation of resources

if all idnivs were identical and were treated for tax purposes identically,

a lump sum would be the only effcient tac

Why impose distoritoonary taxes

gov can only base its decisin on incoem and expenditure

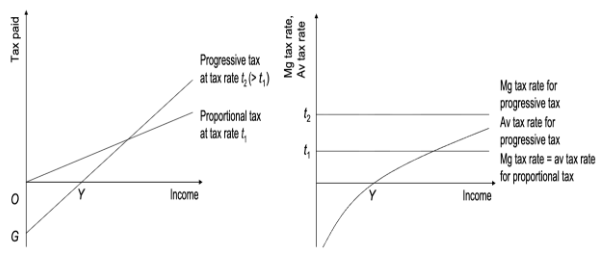

proportional income tax

tax liability is the same percentage of income for all idnivs

simple progressive income tax

imposes a tax at a flat rate on the difference between the individual’s income and some critical level of income

simlairities between propeitional income tax and simple progressive income tax

flat rate taxss, the marginal tax rate is constant, the average tax rate increases with income

what is this

types of taxes

linear tax structure

constant marginal tax rate at all levels of income

non-linear tax structure

varying marginal tax rates

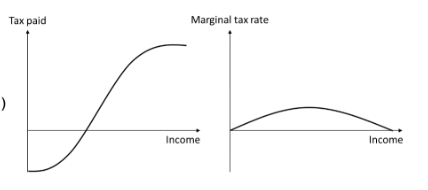

Mirrlees research

marginalta xrate 0 is senstitive to the assumptions about the distribtion of abilities. if you know who the top is then no role for imposing a margianl tax rate bc there is nobody to mimic them

Mirrlees research - shape

inverted u shape

what is this

mirrlees

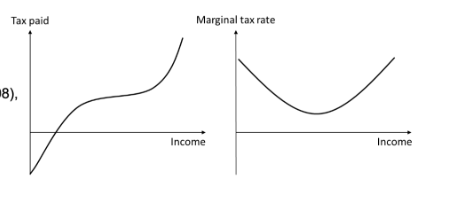

Diamond and Saez research

U-shaped MTR schedule (i.e. current tax schedules may be close to optimal) and that non-linear taxation is significantly more efficient than linear taxation to redistribute income

what is this

diamond and saez research

Diamond and seaz - shape

u shaped

Diamond and seaz - reasong

If you dont know who the top person is, then it could be that marginal tax rates are increasing at the top

What do both Mirrlees and diamond and seaz say

want to impose a large average tax rates with low marginal tax rates, Mirrlees through the flat top for high earners, other for the flatness in the middle

Ramsey rule def

the optimal tax structure is such that the percentage change reduction in the compensated demand for each commodity is the same

What is the additional rule for the ramsey rule

the tax should simply be inversely proportional to the compensated elasticity of demand

Where should high taxes be imposed

commodities with low price elasticities but these goods are usally for low income people which drecreased equality

undesirability of production taxes

Government should not alter the prices that producers face in trades between themselves

optimal tax mix

tax facots or goods with inelastic supply or demand, if no lump sum taxes, the optimal tax depends on the availability and kevels of other taxes

What are the implications of the optimal tax principles

income tax penalises savings but an expenditure tax raises less revenue and is normally more inequitable

when should commodity taxes be used

captures income that may otherwise evade tax and provide a more effciient relief for savings

corlett-hague rule

if income taxes are highly distoritonary, commodity taxes may help to correct that distortion by taxing commodities that are compleemtns of leisure and subsidising commodities that are complements to work

inverse elasticity rule

whe demand elasticities are similar across commodities, for any revenue target, a broad set of low tax rates is preferable

tax reform guidleines efficiency

ncrease taxes on elastic goods and reduce taxes on elastic, broaden tax bases allowing to decrease the marginal tax rate on already taxed items, increase corrective taxes

tax reform guidelines equity

veritcaly equity (redistribution from a well off indiv to a poor) and horizontal equity (broad tax bases and inform tax rates)

whether the should be differnetial commodity taxation

if there is an income tax and its structure

the set of taxes that are feadible dpends on

what variables are observable and verifiable