LO9–3 Understand how leases are recorded.

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

24 Terms

Why do companies lease instead of buy?

Leasing reduces upfront cash, has lower monthly payments, offers flexibility at disposal, and protects against declining asset values.

How does leasing reduce upfront cash needs?

Only the first month’s lease payment is required instead of paying the full purchase price upfront.

Why are lease payments often lower than installment payments?

Lease payments cover only the value used during the lease period, not the full asset value.

How does leasing offer flexibility at the end of the lease?

The lessee can return the asset instead of selling it.

How does leasing protect against declining asset values?

The lessee does not bear the risk if the asset’s fair value decreases.

What does the lessee record at the start of a lease?

A lease asset and a lease liability for the present value of future lease payments.

What were the monthly lease payments in the example?

$352.28 per month for 48 months.

What is the present value of the lease payments in the example?

$15,000.

Why is the lease recorded at $15,000 instead of $16,909.44?

Because accounting records the present value of future payments, not the total cash paid.

$15,000 is the PRESENT VALUE

$16,909.44 is the total cash that will be paid because of interest

What does the extra $1,909.44 represent? —> interest cost

What is the journal entry to record the lease?

Debit Lease Asset 15,000

Credit Lease Payable 15,000

USE THE PRESENT LEASE VALUE

What inputs are needed to calculate the present value of lease payments?

Payment amount, number of payments, interest rate per period, and future value.

What interest rate is used in the example?

0.5% per month (6% annual rate ÷ 12).

How is a down payment recorded in a lease?

Lease Asset = the down payment + the present value of future lease payments.

A down payment is just cash paid upfront at the beginning of the lease.

This cash ALSO gives you the right to use the asset, so it becomes part of the Lease Asset.

But it does NOT reduce the present value calculation — the PV only covers future payments.

Suppose:

Down payment = $2,000

PV of future lease payments = $15,000

Then:

Lease Asset = 17,000

(because you got $17,000 worth of “right to use”)

Lease Payable = 15,000

(you still owe this much in future payments)

Cash = 2,000

(you paid this upfront)

Journal entry:

Debit Lease Asset 17,000

Credit Lease Payable 15,000

Credit Cash 2,000

Why is leasing important?

Leasing is the #1 way U.S. companies finance assets.

4 big reasons why companies lease instead of buy

1. Lower upfront cash

Buying requires paying the full price upfront.

Leasing only requires the first month’s payment.

2. Lower monthly payments

Lease payments are based on the value used, not the full asset value.

Example: If a truck lasts 10 years but you lease it for 4 years, you only pay for 4 years of value.

3. Easier to get rid of

At the end of the lease, you just return the asset.

If you own it, you must sell it — which takes time and money.

4. Protection against declining value

If the asset loses value (like a car), the lessee doesn’t care — they don’t own it.

How are leases recorded?

Even though the lessee doesn’t own the asset, accounting rules say:

The lessee must record:

A lease asset → the right to use the asset

A lease liability → the obligation to make payments

This is why leases show up on the balance sheet.

What happens after recording the lease?

Lease Asset decreases (amortization)

Lease Payable decreases (payments)

Interest expense is recognized each month

This is similar to an installment note — but instead of owning the asset, you’re renting it.

Amortization also means

Paying down a loan in equal installments over time, where each payment includes interest + principal.

This is the same amortization you see in:

Car loans

Mortgages

Installment notes

Lease liabilities

Reduce liability over time

Why do leases use amortization schedules?

Because a lease liability behaves just like an installment loan:

You owe a fixed payment each month

Part of the payment is interest

The rest reduces the liability

Over time, the liability goes to zero

Installment loan

You BUY the asset

You own the asset.

You borrow money to pay for it.

You make equal monthly payments.

Each payment = interest + principal.

The loan balance goes to zero at the end.

What you record:

Asset (Equipment, Truck, Building, etc.)

Notes Payable (loan)

California Coasters buys a truck for $25,000 using a loan.

Journal entry:

Debit Equipment 25,000

Credit Notes Payable 25,000

You own the truck.

Lease

You RENT the asset

You do NOT own the asset.

You pay monthly to use it.

Payments are usually lower than loan payments.

You return the asset at the end.

What you record:

Lease Asset (right to use the asset)

Lease Payable (present value of future payments)

California Coasters leases a truck for 48 months.

Journal entry:

Debit Lease Asset 15,000

Credit Lease Payable 15,000

You do NOT own the truck — you only have the right to use it.

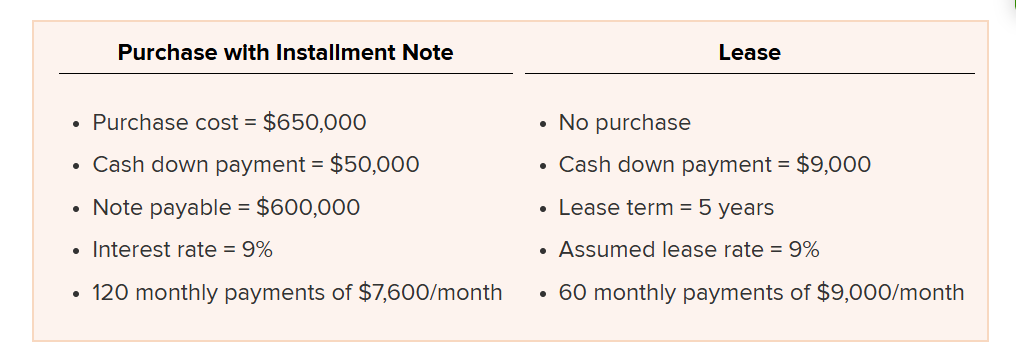

Record the lease with a down payment.

Debit lease asset $442,560

Credit cash (down payment) $9,000

Credit least payable $433,560

If there is a down payment…

It gets added to the lease asset, not liability

When a company leases something and pays a down payment:

✔ Lease Asset = Down Payment + Present Value of Future Payments

✔ Lease Liability = Present Value of Future Payments

✔ Cash = Down Payment