CFA Level 2 exam questions with complete verified solutions

1/67

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

68 Terms

Heteroskedasticity

What/effects?

How to detect?

How to correct?

Non-constant error variance. Standard errors are unreliable, coefficient estimates are NOT effected, t and F tests are not reliable

Detect with Bruesch-Pagan Test (chi^2 = n * R^2(of residuals))

Correct with White-correct standard errors

Autocorrelation

What/effects?

How to detect?

how to correct?

Correlation among error terms. Coefficient standard errors are too small, est. coefficients are NOT effected, t-stat. too large (type 1 error), unreliable F-test.

Detect with Durbin-Watson statistic (DW = 2(1-r))

Correct with Hansen method (adjusting coefficient standard errors) or improve model specification

DW test

DW=2(1-r) for large sample

if DW=2 homoskedastic

DW<2 positive serial correlation

DW>2 negative serial correlation

if DW

Multicollinearity

What/effects?

How to detect?

how to correct?

High correlation among X's. No effect on slope coefficient but is unreliable, standard error of X's is too high (Type II error).

Detect if t-tests indicate none of the slope coefficients are different than 0, but F-test is significant and R^2 is high.

Correct by omitting variables.

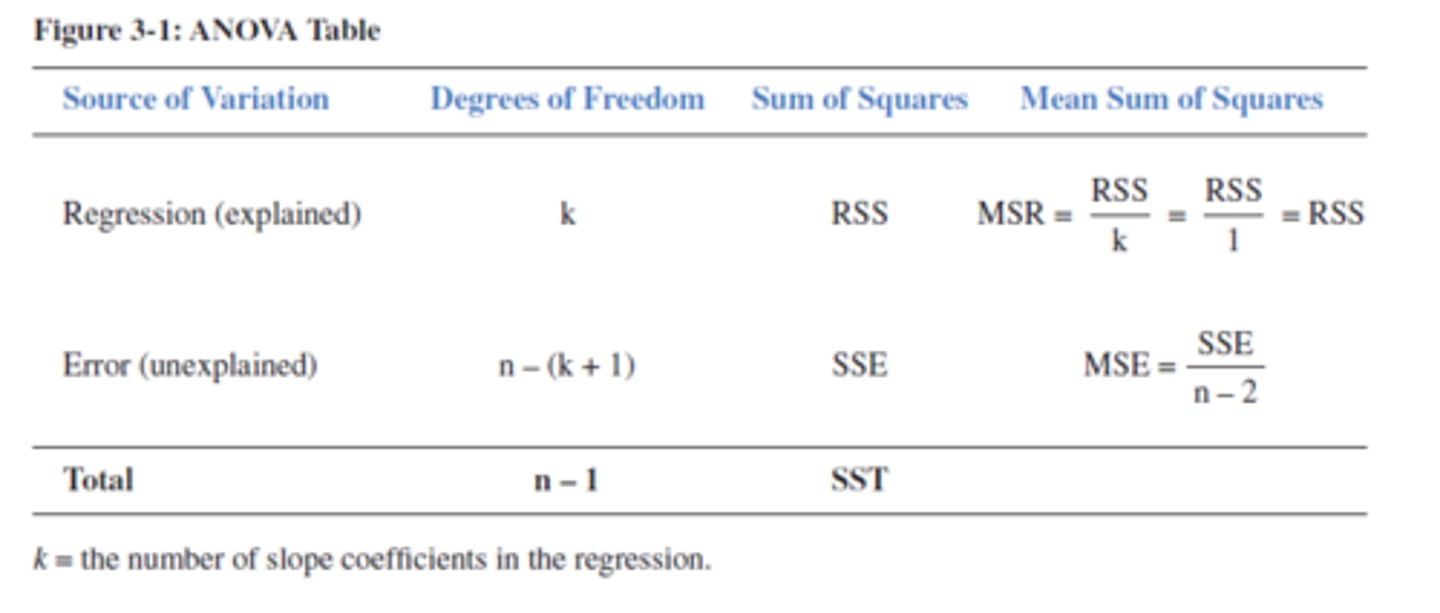

SEE

=sqrt(MSE)

Measures the degree of variability of actual Y to estimated Y

ANOVA table

Adjusted R^2

= 1 - [(n-1)/(n-k-1)](1-R^2)

Mean Reverting Level

= B0/1-b1

Note that this is why Random Walk has unit root where b1 = 1. Therefore Random Walk is NON STATIONARY.

Test for autocorrelation in AR model

t-test where t = correlation of error terms/(1/sqrt(T))

RMSE (root mean squared error)

RMSE is used to compare the accuracy of AR models in forecasting values out-of-sample

Test for unit root for time series model

Run AR model, if residual autocorrelations = 0 at all lags then it is covariance stationary

or

Dicky-Fuller test: Ho: g = b(1) - 1 = 0

if Ho cannot be rejected there is a unit root

First Differencing

This is used to correct AR when it has a unit root. You subtract the previous value from the current value to define NEW DEPENDENT variable. Here you graph the CHANGE in the values which is essential the error term.

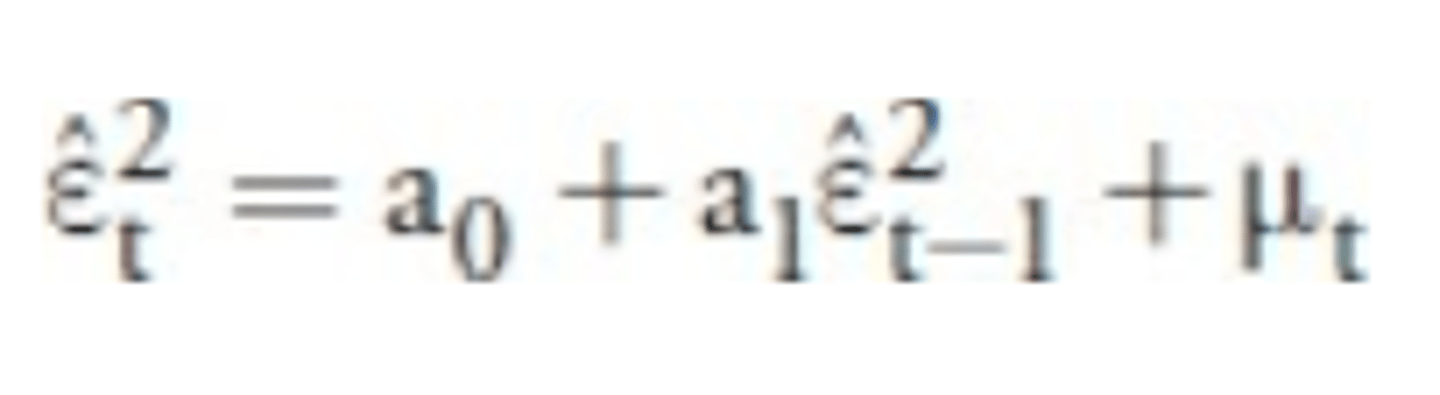

ARCH Model

Used to test for autoregressive conditional heteroskedasticity (ARCH) in AR models.

If a(1) is statistically different than 0, time series has ARCH

bias error

in-sample error, model is a poor fit

Variance Error

out-of-sample error, overfitted models

base error

residual errors due to random noise

If model complexity increases, what happens to variance error and bias error?

Variance error increases and bias error decreases with model complexity

Penalized regressions

Supervised ML algorithm

Penalizes for more variables added in model

ex. LASSO

Support Vector Machine

Supervised learning classification tool that separates data into 1 of 2 possible outcomes

ex. buy vs sell

K-nearest neighbor (K-NN)

A supervised ML technique used to discover associations and sequences when the data attributes are numeric; nonparametric estimator of a function

ex. assigning a bond to a rating class

Classification and regression tress (CART)

Supervised ML algorithm used when target variable is categorical and usually binary, with non-linear relationship

Ensamble Forecasting

Supervised ML

combines predictions from multiple models, results in lower average error

Random Forest

An supervised ML algorithm used for regression or classification that uses a collection of tree data structures trees "vote" on the best model

Principal Component Analysis (PCA)

Unsupervised ML algorithm

variable reduction technique, used when variables are highly correlated. Helps you to figure out which variables matter the most. Categorization technique

Clustering

Unsupervised ML algorithm

Grouping observations into categories based on similarities in attributes

ex. k-means clustering

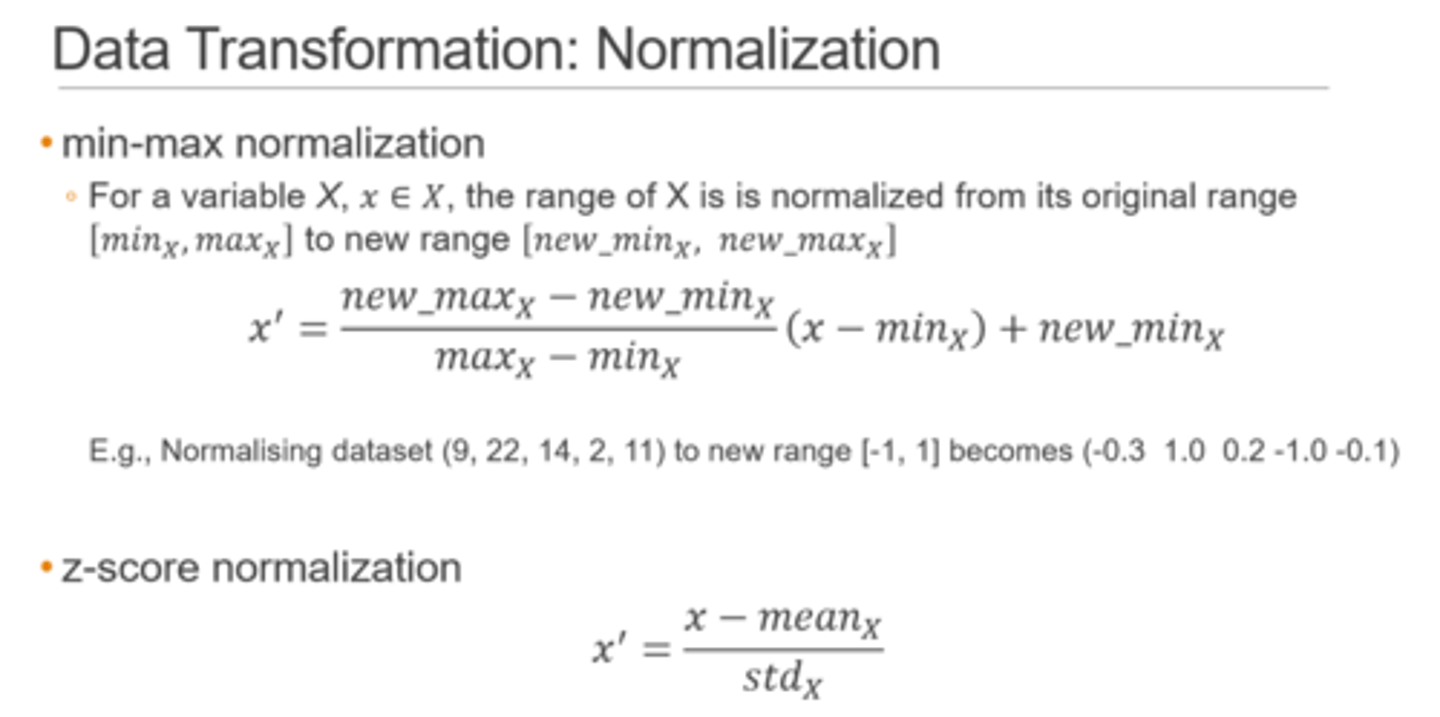

Normalization

puts values between 1 and 0

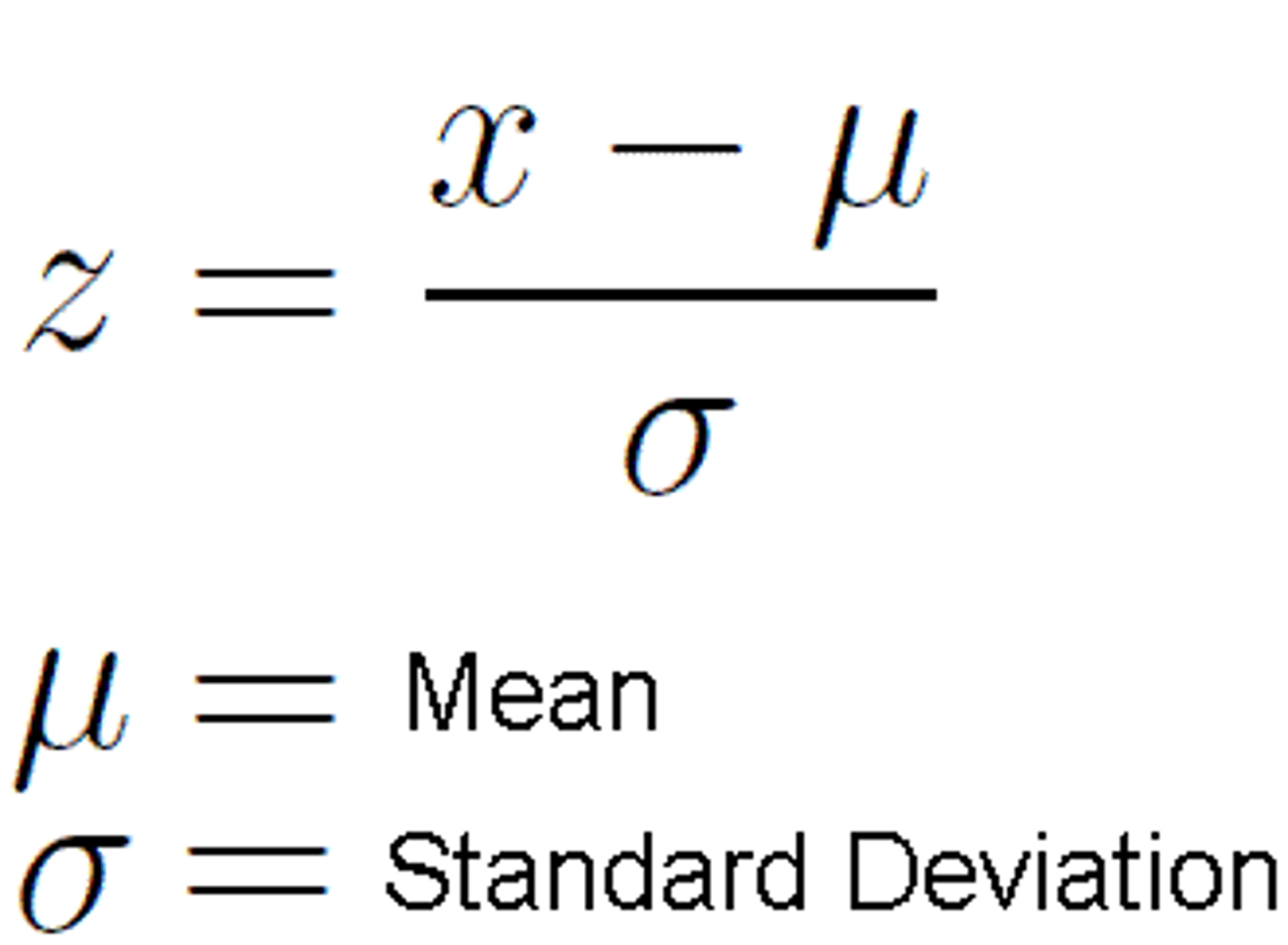

Standardization

Centers variables at 0 and scales them as units of standard deviations from the mean

Assumes data is normally distributed

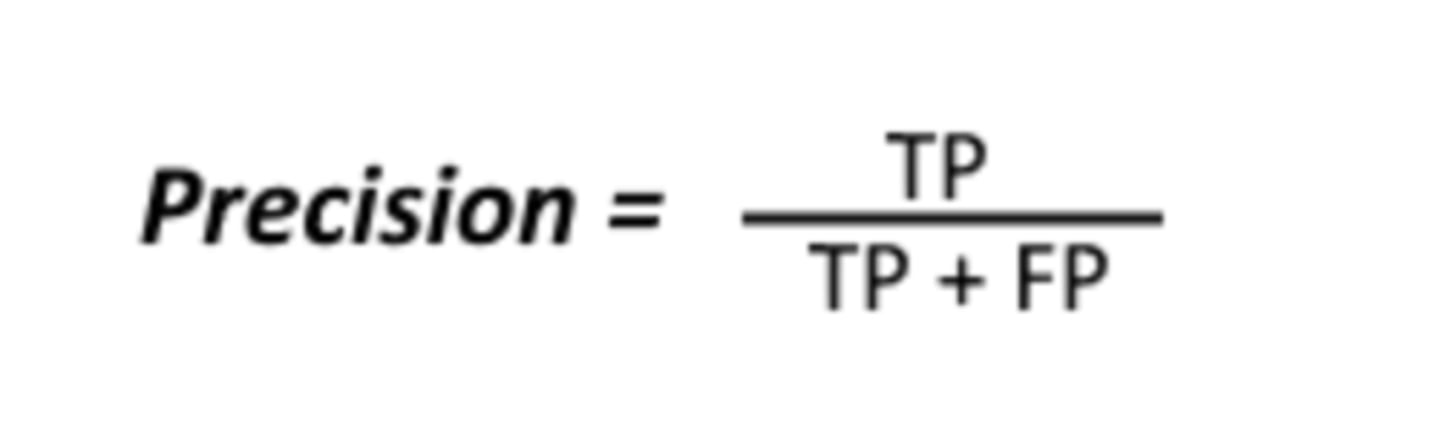

Precision formula

Recall formula

TP/(TP+FN)

Accuracy formula

(TP + TN)/(TP + TN+ FP + FN)

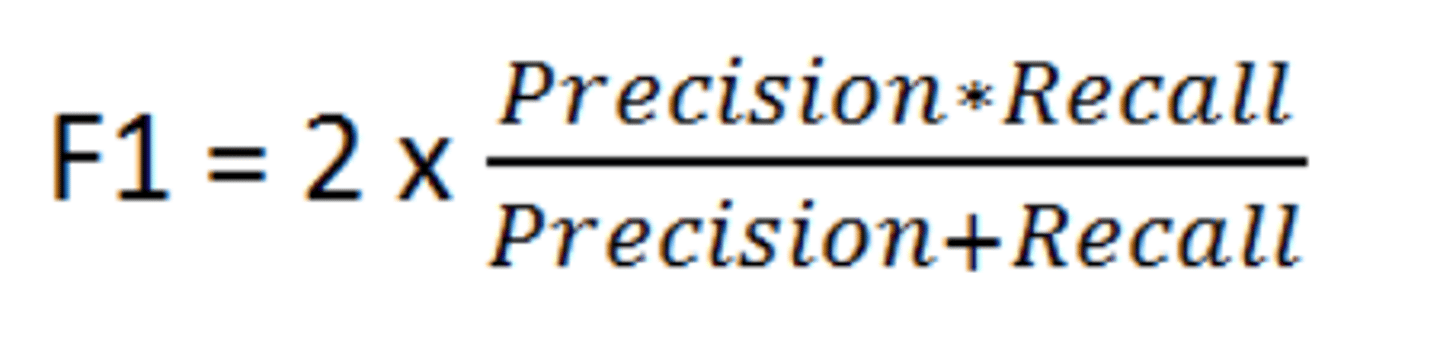

F1 Score

harmonic mean of precision and recall

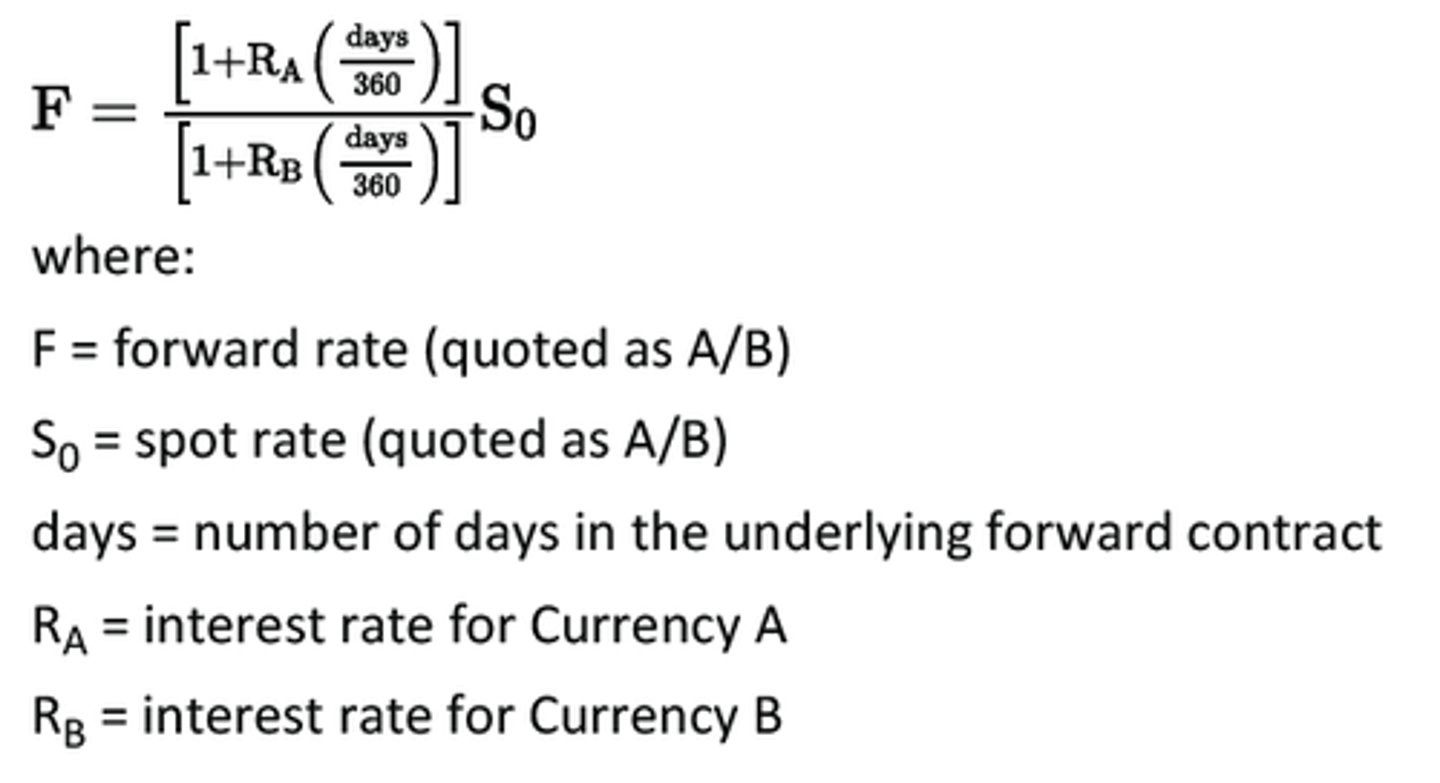

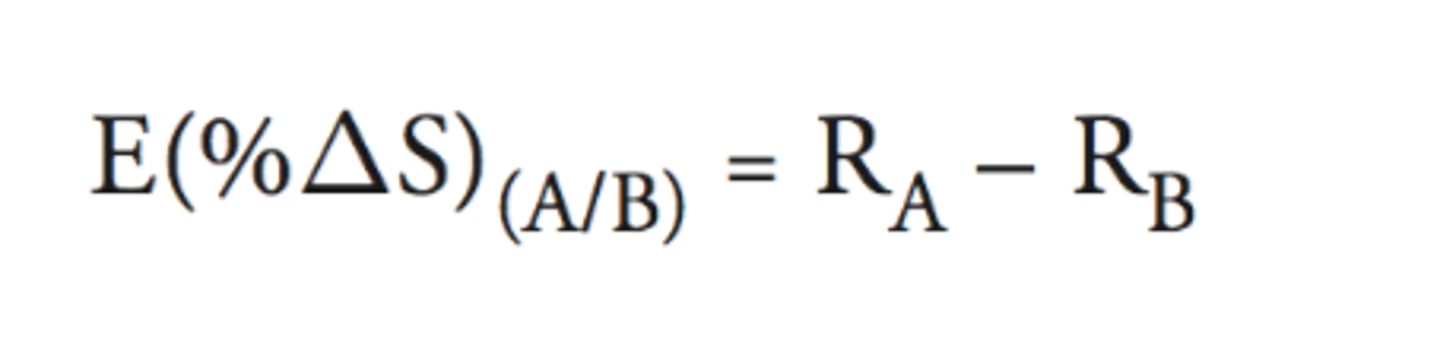

currency arbitrage rule

Up-the-bid-and-multiply, down-the-ask-and-divide

Given a quote for A/B, if trading at a forward premium, we say currency _______ is trading at a forward premium

B

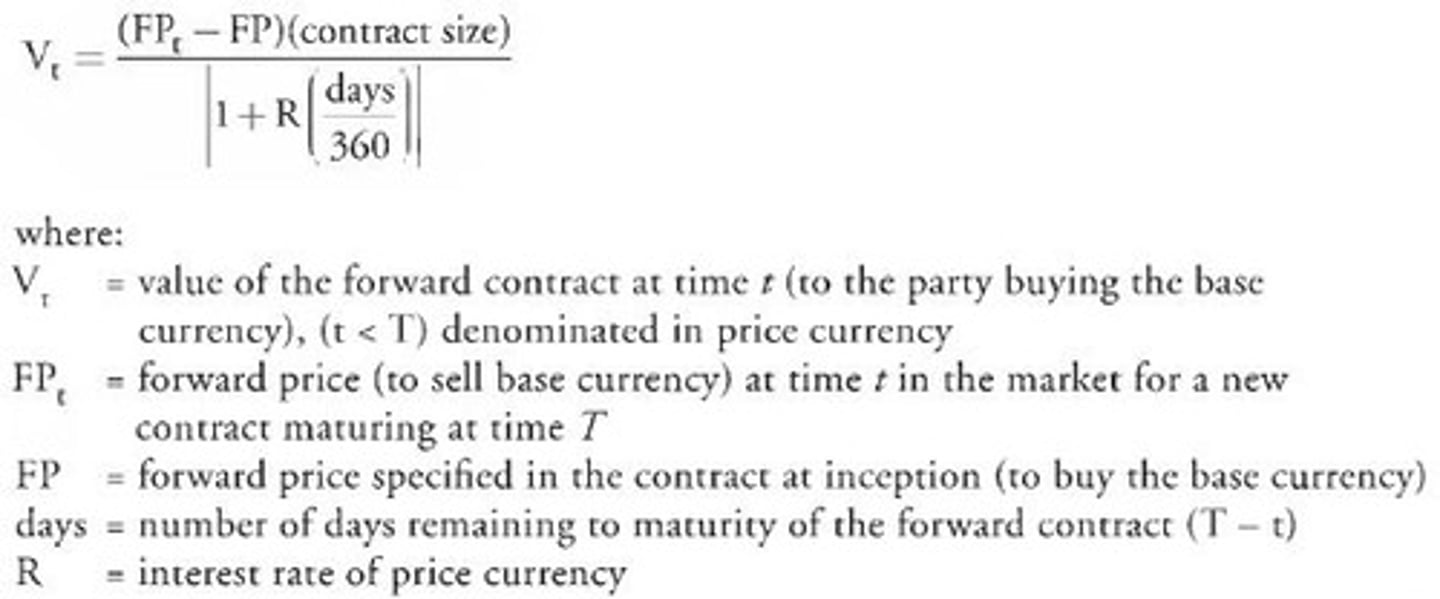

Mark-To-Market Value of Forward Currency Contract

Note FP(t) is calculated based on the need to "unwind" the position

covered interest rate parity

principle implying that forward exchange rates and spot exchange rates set interest rates on bonds in different countries equal to one another

Uncovered Interest Rate Parity

a theory that holds that the forward exchange rate equals the expected future value of the spot rate

assumes investors are risk neutral

Unbiased Predictor

If the forward rate (under covered interest parity) = expected future spot rate (uncovered interest rate parity) then the forward rate is said to be an unbiased predictor of the future spot rate

Fisher Relation and international Fischer Relation

R(nominal) = R(real) + E(inflation)

Ex ante version of PPP

Hypothesis that expected changes in the spot exchange rate are equal to expected differences in national inflation rates. An extension of relative purchasing power parity to expected future changes in the exchange rate

FX Carry Trade

an investment strategy that involves taking on long positions in high-yield currencies and short positions in low-yield currencies

Flow supply/demand mechanism (current account deficit)

Excess supply of currency in the markets causes domestic currency to depreciate.

Amount of depreciation depends on (1) initial deficit, (2) influence of FX rates on domestic import/export prices, (3) price elasticity of demand of the traded goods

Debt Sustainability Mechanism (current account deficit)

When debt gets too high relative to GDP, foreign investors may pull out of positions causing domestic currency depreciation

Excessive capital inflows into emerging markets causes...

1. excessive appreciation

2. asset bubbles

3. increase in debt

4. excessive consumption fueled by debt

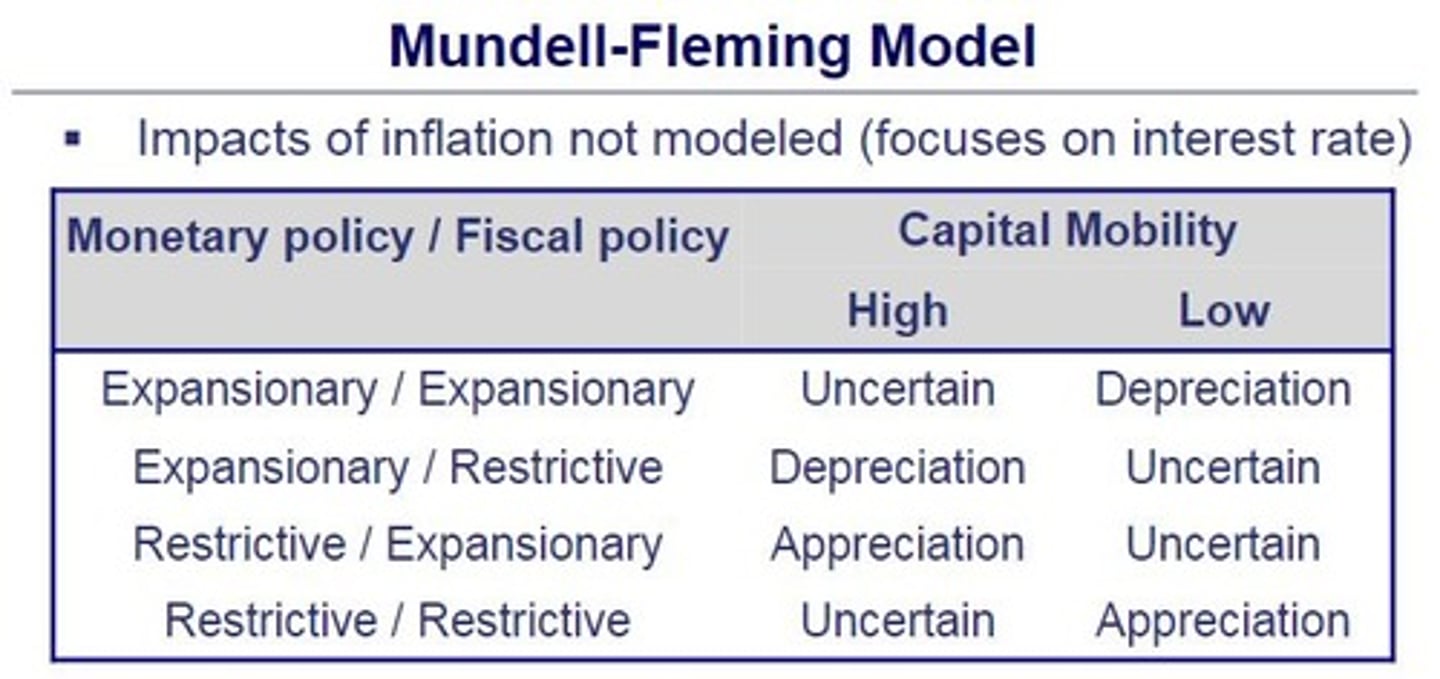

Mundell-Fleming Model

-Evaluates the impact of monetary and fiscal policies on interest rates and exchange rates

-Short-term focus

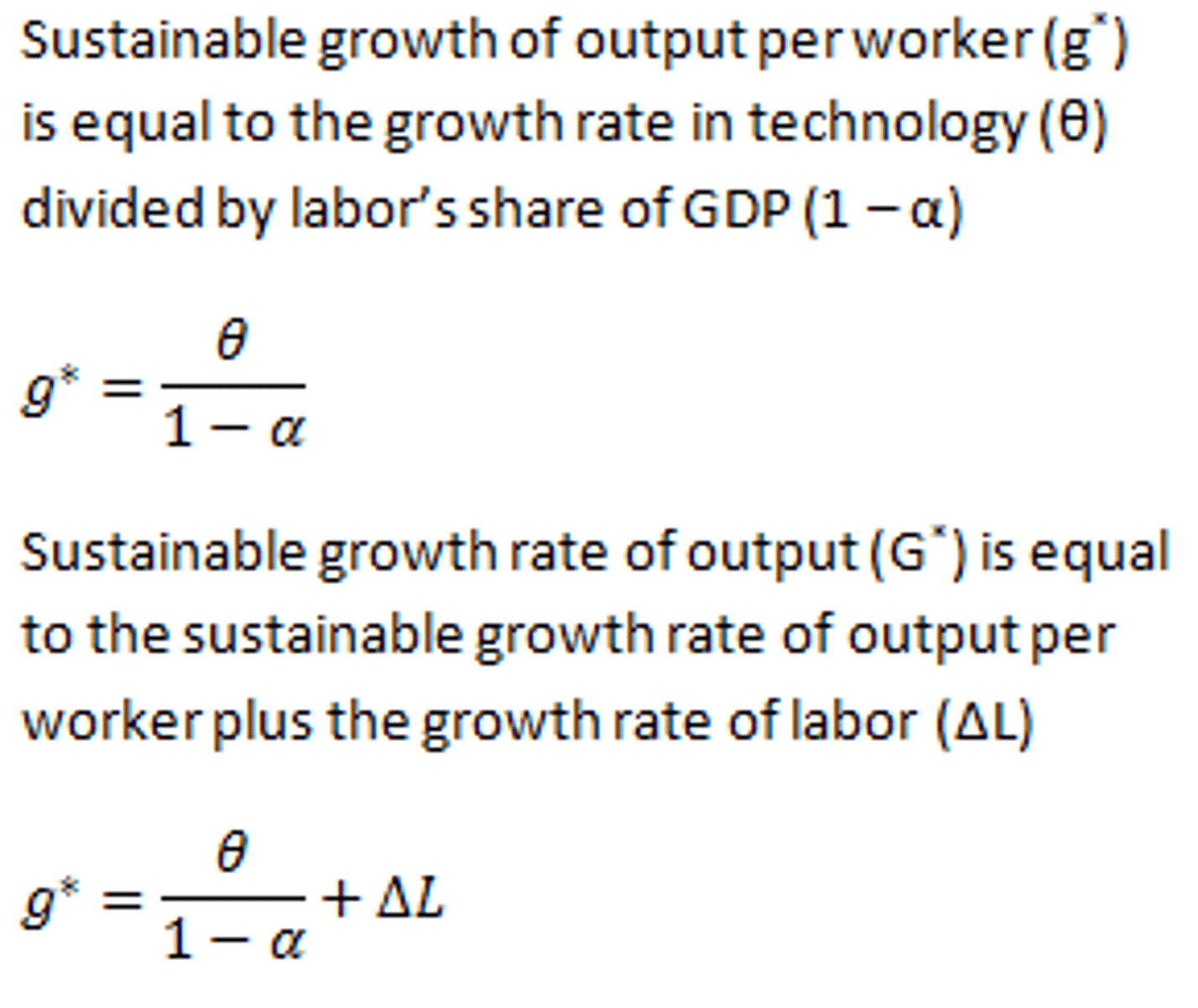

Potential GDP

the amount that can be produced when all of the economy's resources are used fully and efficiently

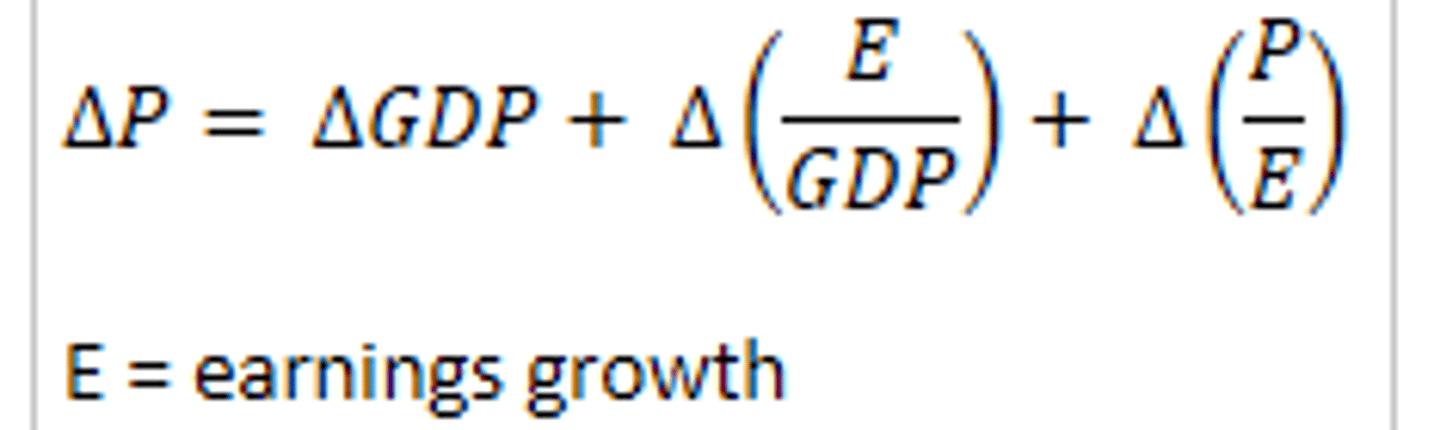

Growth in aggregate stock market equation (as a function of GDP)

In the long term only change in GDP will not be 0

In short-term, what are the effects of actual GPD>potential GDP?

Inflation leading to restrictive monetary policy

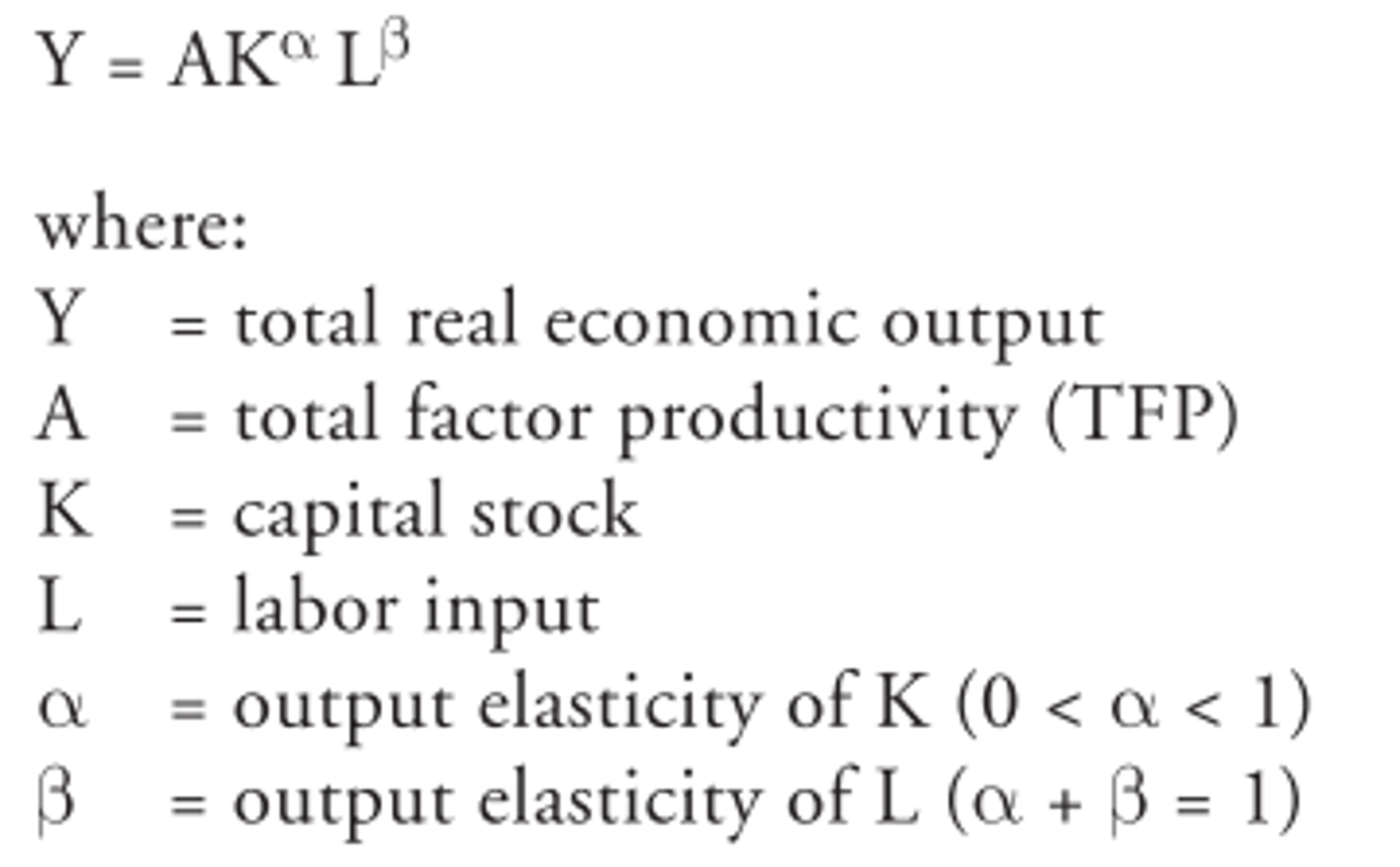

Cobb-Douglas production function

Lower share of output allocated to capital (α) causes the affect of capital deepening to...

decrease

Growth Accounting Equation

Dutch Disease

the negative impact on an economy of anything that gives rise to a sharp inflow of foreign currency, such as the discovery of large oil reserves. The currency inflows lead to currency appreciation, making the country's other products less price competitive on the export market.

Classical Growth Theory

A theory of economic growth based on the view that the growth of real GDP per person is temporary and that when it rises above subsistence level, a population explosion eventually brings it back to subsistence level.

Neoclassical Growth Theory

a theory of economic growth that proposes that real GDP per person grows because technological change. An increase in savings will only temporarily increase economic growth

Effect of capital deepening on growth rate at steady state (neoclassical growth theory)

Capital deepening does NOT effect growth rate

Endogenous Growth Theory

-Technological growth emerges as a result of investment in both physical and human capital

-Increased investment can permanently increase rate of growth

-Returns to capital are constant

-An increase in savings will permanently increase the growth rate

-Capital investment may improve total factor productivity

Regulatory Capture Theory

Regulatory body will at some point be influenced or even controlled by the industry being regulated. Regulators often have experience in the industry and this affects their ability to render impartial decisions

Investments in Financial Assets (IFRS 9) Classifications

For investments <20% with no significant controls

- Amortized Cost (debt): On B/S at amortized cost, interest income from coupon pmts on I/S

- Fair value thru P&L: when held for trading, on B/S at FV with G/L on I/S

- Fair value thru OCI: on B/S at FV, unrealized G/L in OCI, realized G/L on I/S

Investments in Associates (20%-50% ownership)

For investments between 20% and 50% with significant influence. Account for investment using equity method:

- record at cost on B/S as a non-current asset

- in subsequent periods, increase B/S with share of investee's net income and decrease with share of dividends

- share of net income is recognized on I/S, dividends are not recognized on I/S

Impairment on equity method investments

GAAP: if fair value > carrying value AND is not temporary, asset is impaired and written down to fair value

IFRS: asset is impaired if there are 1 or more loss events

Acquisition Method

- used for business combinations or investments >50%

- combine A & L, add minority interest in E

- combine revenue and expenses, add minority interest expense

How is minority interest on B/S adjusted for income and dividends?

Increased for portion of net income not owned by parent and decreased for portion of dividends

Full Goodwill

(Fair value of equity of whole subsidiary) - (fair value of net identifiable net assets of the subsidiary)

#Required under U.S. GAAP; allowed under IFRS

Partial Goodwill

Purchase price - (% owned × FV of net identifiable assets of the subsidiary)

#IFRS only

Non-Controlling Interest (NCI)

Full goodwill: NCI = (% not owned by parent) * (subsidiary's fair value)

Partial Goodwill: NCI = (% not owned by parent) * (FV of net identifiable assets)

Goodwill Impairment

Tested ANUALLY

IFRS: single-step, if carrying value of cash generating unit > recoverable amount; IMPAIRED

GAAP: 2-step, if carrying value of reporting unit > FV; IMPAIRED

impairment loss = (carrying value of GW) - (implied FV of GW)

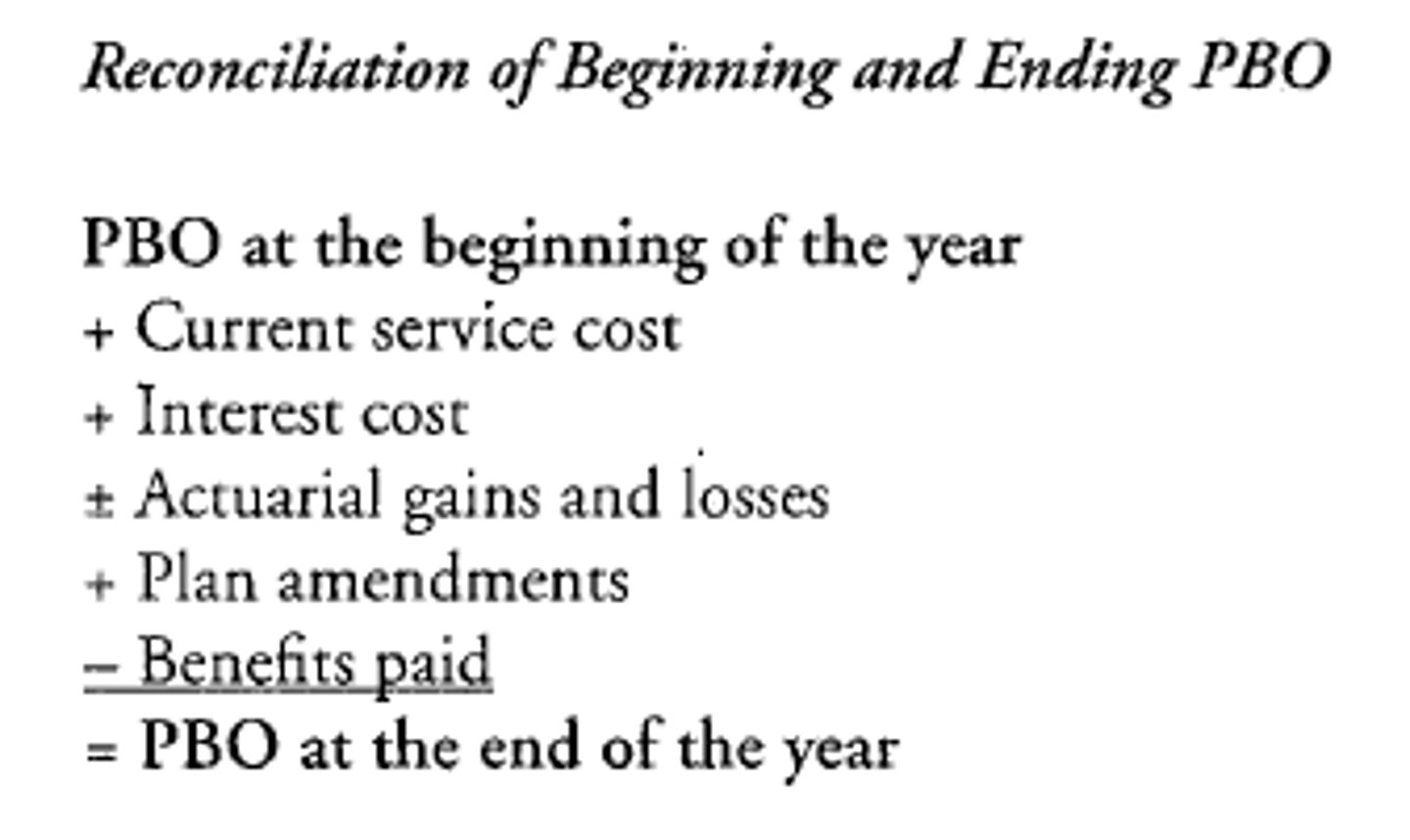

PBO (PVDBO)

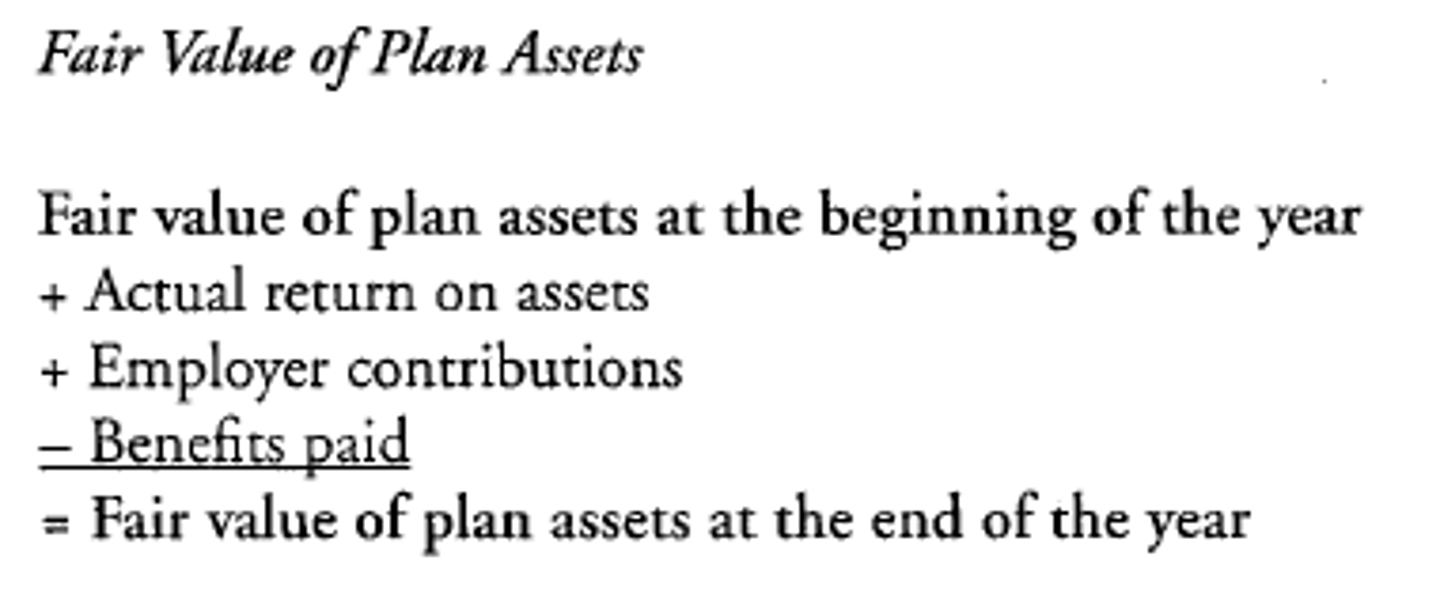

Plan Assets

Total Periodic Pension Cost (TPPC)

Contributions - ∆ funded status

OR

Contributions - (ending funding status - beginning funded status)

OR

Current service cost

+ Prior Service Cost

+ Interest Cost

- Actual return on plan assets

+/- Actuarial losses/gains due to changes in assumptions affecting PBO

OR

(Ending PBO - Beginning PBO)

+ Benefits Paid

- Actual Return on Plan Assets