Applied Economics

1/53

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

54 Terms

Applied economics

the application of economic models and theories/concepts in every day living

Scarcity

resources are limited

people have unlimited ____ & _____

needs, wants

Economics

the efficient allocation of available resources

Absolute advantage

the ability to produce more output compared to another entity

comparative advantage

an economy’s ability to produce a specific good/service at a lower opportunity cost

opportunity cost

the benefit you give up because you choose to take one action in favor of another

economic goods

goods and services used extensively in economic discussions (it covers goods, services, products, and the like that have a price and are sold in a market).

WHAT GOODS TO PRODUCE?

HOW TO PRODUCE AND HOW MUCH?

FOR WHOM TO PRODUCE?

Basic economic problems

Factors of production

land

labor

capital

entrepreneurship

Land

available natural resource

typically cultivated or improved for use in production

factor income is rent

Labor

represents human capital like workers and employees

the return on this is wage

Capital

represents physical assets like production facilities, warehouses, equipment, and technology used in the production of goods and services

factor income is interest

Entrepreneurship

represents the factor that decides how much of and in what way the other factors are to be used in production

the return on this is profit

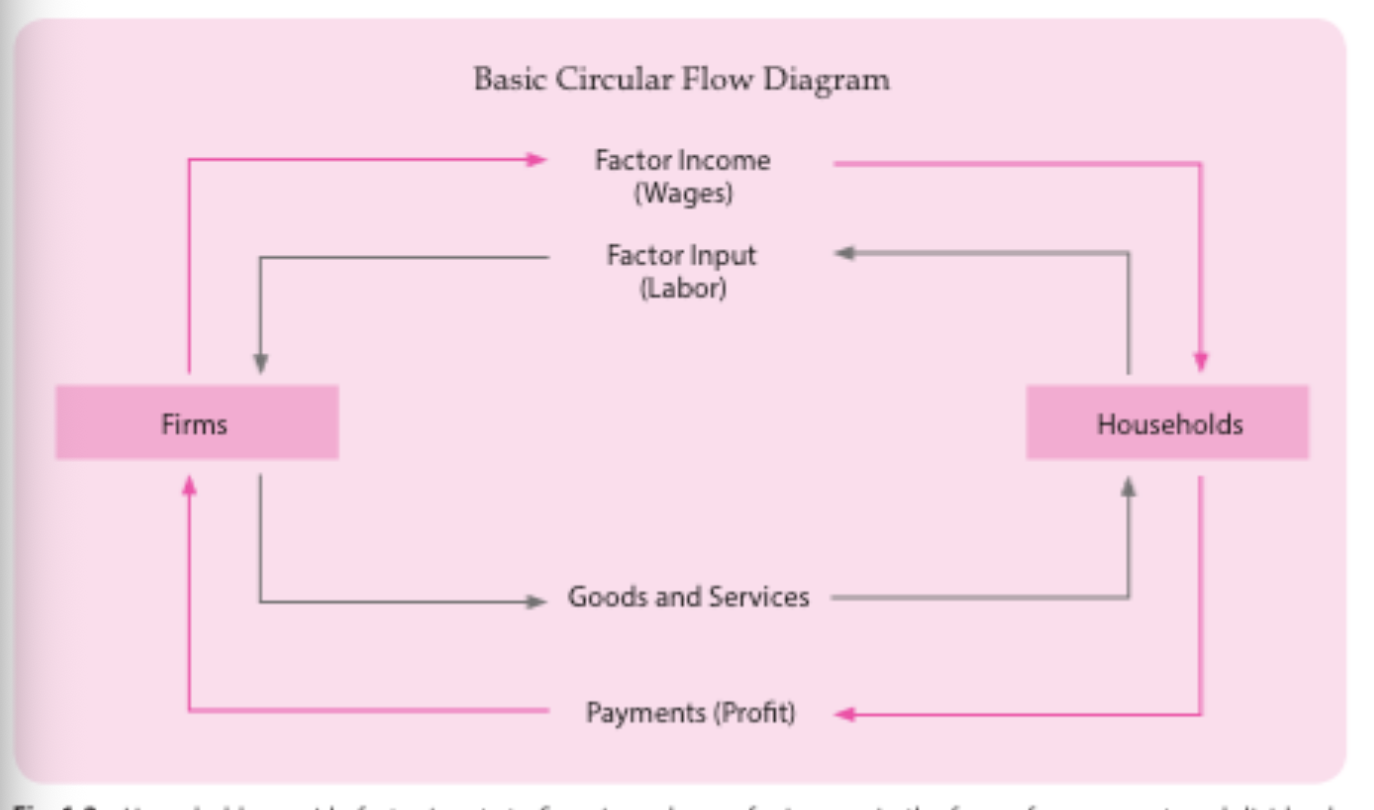

Circular flow diagram

an economic diagram that illustrates the flow of factors of production in the economy.

The circular flow diagram in its most simple form

Production possibility frontier (PPF)

application of the concept of allocation of resources and factors of production

determined by the availability and efficient use of its inputs of production

Qualitative Approach

focuses on directional relationship of different economic variables

often used interchangeably with descriptive analysis

Quantitative approach

involves mathematical and statistical analysis of economic data

complements qualitative analysis by providing figures that support descriptive findings

Economic Variables

used to signify elements in an economic model

a variable is an element that can change in contrast to a fixed one

Functions

explains the relationship between two or more economic variables

Graph

provides visual representation of the relationship between two or more economic variables

Economic theories

simplify economic phenomena

statements or observations on the relationship of variables

Marginal Utility Theory

states that people buy goods that give the highest personal satisfaction

further explains that a rational person will maximize his or her utility given some constraints like budget or income

Economic Models

representations of economic and social phenomena analyzed using research, observations, and testing

Ceteris Paribus Assumption

Ceteris Paribus - a latin term that translates to “all else being the same”

implies that there are other elements which may affect the model but for the pertinent study, the model focuses only on specific variables

a form of acknowledgment of the limitation of the model

Time-series Data

data collected for particular elements for several time periods

Cross-Sectional Data

includes different variables for a single time period

Normative economics

evaluates economic decisions, policies, or outcomes as good or bad

based on opinion and is subjective

Positive economics

evaluates economic scenarios and policies based on qualitative and quantitative analysis

factual and objective

Main branches of economics:

Microeconomics and Macroeconomics

Microeconomics

examines the individual or company level

Macroeconomics

studies the aggregate or country level

Microeconomic Concepts

Utility

Marginal Utility

Law of diminishing marginal utility

upward sloping utility curve

indifference curve

indifference map

budget line

equilibrium position

Utility

refers to the value or satisfaction derived from the consumption of a good

Marginal Utility

the additional satisfaction from the consumption of an additional unit of a good, keeping other things constant

Law of diminishing marginal utility

for every additional consumption your marginal utility or your level of satisfaction is declining

upward sloping utility curve

a scenario where one of the two choices is an economic "bad" (e.g., pollution, commuting time) rather than a good

indifference curve

when the consumer behavior of not being affected by the quantity consumed of a good in favor of another is illustrated by this concept

indifference map

shows a group of indifference curves

budget line

represents the income constraint of a consumer

equilibrium position

represented by the tangency point of the budget line with the highest indifference curve

Disposable income

income after taxes

Discretionary income

income left from disposable income after all other necessary non tax expenses have been deducted

Gross Domestic Product (GDP)

the total value of final goods and services consumed during a given period, usually on year

GDP Growth

the rate of increase in the GDP value from one period to another which is expressed as a percentage

“Final”

emphasized in the value of goods and services derivation of GDP to avoid double counting

Final goods

goods and services are the products bought or consumed by end consumers

Nonproduction transactions

excluded in the GDP value

includes: transfer payments, social security benefits, financial market securities, such as stocks and bonds certificates

Two ways to measure national income

output approach

expenditure approach

Output Approach

looks at output and evaluates what goods and services are factored in

Expenditure Approach

considers the value or expenditure associated with eh purchase of goods and services

Nominal GDP

derived when the value of goods is expressed in current prices

Real GDP

adjusted for inflation and is expressed at constant or base year prices