Life & Health: General Insurance

1/56

Earn XP

Description and Tags

General Insurance

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

57 Terms

What is insurance?

A contract that transfers the risk of financial loss from an individual or business for certain losses if they occur.

What is risk?

Uncertainty about whether a loss will occur.

• If a loss is certain to occur, it does not involve risk.

• Insurance is designed to cover only losses that involve risk.

• Death is certain, the timing of the loss is uncertain.

What is speculative risk?

Speculative risk has the possibility of a loss or a gain, like gambling - loss is not insurable.

What is pure risk?

Pure risk has the possibility of a loss and can be covered by insurance, like the chance of being in a car accident.

What is loss?

Reduction in the value of an asset.

• To determine the amount of loss, value of the asset is measured before and after loss.

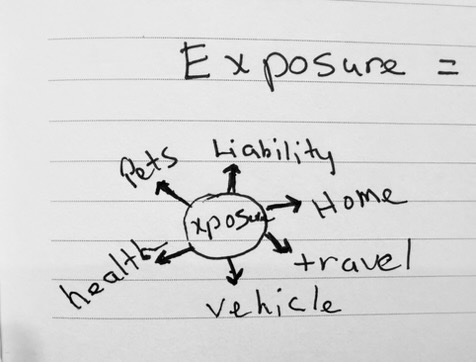

What is exposure?

Risks for which the insurance company would be liable.

• The risk assumed by an insurer and the amount they are responsible to pay out a any give time.

What is peril?

The cause of a loss.

life insurance = death

health insurance = accidents or illness

property & casualty = fire, lightning, etc.

What are the 3 types of hazards?

physical = wet floor

moral = moral character (dishonesty)

morale = carelessness (leaving door unlocked)

What are the 5 methods of handling risk?

STARR

Sharing = share the risk to pay the loss

Transfer = insurer agrees to pays if the individual or business has a loss. The individual/business has a cost in the form of a premium payment.

Avoidance = eliminate risk - don’t drive

Reduction = lessen the chance - wear seatbelt

Retention = Individual pays for the loss

What is The Law of Large Numbers?

The larger the group—the more accurate losses can be predicted

What are the 6 elements of insurable risk?

CANHAM

Calculable

Affordable

Non-catastrophic

Homogeneous (risks must all be similar in regard to factors that affect the chance of loss)

Accidental

Measurable (dollar amount - insurance covers the financial loss of unexpected death or medical bills from sickness)

What is adverse selection?

Higher-risk individuals. Underwriter evaluates risks that have a greater than average chance of loss.

What is reinsurance?

Transfers some or all risk from one insurer to another insurer. Protects the insurance company from catastrophic losses in certain geographical areas.

ceding insurer = company reducing its risk

reinsurer = company assuming the risk

facultative reinsurance = the reinsurer considers each risk before allowing the transfer from the ceding company. Facultative “Oh F*ck!, big risk”

treaty = the reinsurer accepts the transfer.

TYPES OF INSURERS

Stock Insurers

Stock insurer is a business formed as a public or private corporation.

• Owned by S/S (stockholders/shareholders).

• Board of directors chosen by S/S.

• If company makes money, taxable dividend from profits may be paid to S/S.

• Issues non-participating (non-par) policies.

TYPES OF INSURERS

Mutual Insurers

Mutual insurer is owned by its policyholders/policyowners.

• Owned by the policyholders (customers).

• Board of directors chosen by policyholders.

• If company is profitable, excess premiums can be returned to its policyholders-nontaxable dividend.

• Issues participating (par) policies.

TYPES OF INSURERS

Fraternal Benefit Societies (Fraternal Insurer)

Fraternal benefit societies exist for the benefit of its members, share common bond (e.g., religion or occupation), and offers life insurance as one of the benefits of membership. Must be a member of the society to get the benefits.

• Provide social activities, engage in charitable causes.

• Nonprofit societies organized under a lodge system, receive some income tax advantages.

• Operate their insurance programs under special section of state insurance code.

fraternal policies = called certificates

members who own life insurance = called certificate holders

Certificate holders may be assessed additional charges if premiums don’t cover claims. Policies with this feature are open contracts.

TYPES OF INSURERS

Reciprocal Insurer

Reciprocal insurers are unincorporated groups groups of people that agree to insure each other’s losses under a contract.

“you reciprocal me, and I’ll reciprocal you"

• Known as subscribers.

• If subscriber suffers a loss covered by the reciprocal insurance agreement, each subscriber pays equal amount to pay the claim.

• Administration, underwriting, sales promotion = handled by an attorney-in-fact.

• Attorney-in-fact often controlled & overseen by advisory committee or subscribers.

TYPES OF INSURERS

Risk Retention Group (RRG)

A risk retention group formed for the sole purpose of providing liability insurance to its policyholders.

• Must all be member of the same type of business or industry.

car dealers, transportation, manufacturers, colleges or universities

i.e. home health for medical malpractice

TYPES OF INSURERS

Lloyd’s Association

Lloyd’s Associations, named in reference to the famous underwriting group Lloyd’s of London.

• Not an insurance company.

• Insurance provided by individual underwriters, or groups pool to underwrite risks.

• Insure unusual risk, e.g., hole-in-one contests, body parts of celebrities.

TYPES OF INSURERS

Self-Insurance

Self-insurance retains risk rather than transferring risk.

• A business that pays its own claims.

e.g., Costco, Wal-mart

• Big companies often self-insure employee health benefits (stop loss insurance) for catastrophic claims instead of group health policies.

What is Residual Market?

Residual Market is insurance from the state or federal government.

• Federal gov’t = social security benefits, military life insurance etc.

• Feds also provides, supports, or subsidizes insurance programs for catastrophic risks. e.g., war, flood, crop losses.

• State gov’t = unemployment insurance, workers’ comp, disability, etc.

“Think residual as ongoing and continuing, like social security.”

Define Domestic, Foreign, and Alien Insurers

Domestic = the state where an insurer is incorporated, state of domicile. Incorporated in AZ, does business in AZ.

Foreign = the insurer writes business in states other than where they are domiciled. Insurer located in TX, but selling insurance in MI.

Alien = Insurer incorporated in any country other than USA.

What is a Certificate of Authority?

State license for an insurance company.

What is it called when a state requires the insurance company to have a Certificate of Authority?

Admitted, authorized, or approved.

Licensed = authorized

What is it called when an insurance company is not required to have a Certificate of Authority from the state?

Non-admitted, unauthorized, or nonapproved.

Not licensed = unauthorized

What are surplus lines insurers?

An unauthorized/non-admitted agent or broker that covers specialized risk not covered by a licensed insurer.

What are surplus lines?

Insurance sold by unauthorized/non-admitted insurers - if on the states approved list of surplus funds insurers.

• can only be sold to certain high risk insureds

• can’t be sold just for a cheaper rate than licensed/admitted insurers

• regulated by the state, covers high risks like gaming, casino, skyscrapers, etc.

What is the financial strength rating?

A report card of the company.

What is an Independent Insurance Agent?

individuals that sell the insurance products of several companies.

• independent contractors, not employees of the insurer.

• own the renewals of the policies they sell.

What is an Exclusive or Captive Agent?

Represent only one company.

• captive agents are independent contractors, not employees of the insurer.

• insurance company owns the renewals of the policies sold on their behalf.

What is a General Agent (GA) or Managing General Agent (MGA)?

Recruits other agents in a certain area who actually sell the insurance to the customer.

• GAs and MGAs receive overriding commissions (overrides) on the business produced by the agents they manage.

What are Direct Writing Companies?

The company sells the insurance through salaried employees of the company.

• producer not usually paid a commission

• business owns all the business produced

What is Direct Response Marketing?

Marketing with no producer/agent.

• policies sold directly to the public by the insurer.

• mail, newspaper ads, radio, etc.

What is Agency?

Insurance agent acts on behalf of the principal (insurance company)

• Agent = the person authorized to act on behalf of the insurer (sales rep/producer)

• Principal = person on whose behalf the agent acts (insurer)

What is the law of agency?

Contracts made by the agent are considered to be contracts of the principal. The principal is liable for the statements and actions of their agents.

What are the three types of Agent Authority?

Express, Implied, Apparent

Regarding Agent Authority, what is “express” authority?

What the agents written contract with the company states.

Regarding Agent Authority, what is “implied” authority?

Not written, but are the actions agents normally do to sell insurance.

• power that the agent believes they have b/c it’s necessary for the agent to conduct business of the insurer. i.e. printing business cards.

Regarding Agent Authority, what is “apparent” authority?

The actions the agent does that a reasonable person would assume as authority, based on the agents’ actions and statements.

• whatever the agent does, says, or writes, they represent/act as the insurer (principal).

What is a fiduciary?

A person in a position of financial trust.

Fiduciary = trust. What are the four responsibility of fiduciary trust?

• promptly send premiums to insurer

• knowledge of products

• comply with laws and regulations

• no commingling of funds (personal & insured’s premiums)

What is a legal contract?

legal agreement b/w two competent parties that promises a certain performance in exchange for a certain consideration.

What are the 6 elements of a legal contract?

CLOCAC

Consideration = giving something of value

• insured gives information & money (premium) to the insurance company.

• Insurance company gives a promise to pay (policy) to the insured.

Legal purpose = risk transfer does not violate the law

Offer (made by insured) =insured submits application & 1st month’s premium

Counteroffer (made by insurer) = agrees to issue policy but w/ higher premium or restrictions/exclusions. Insured accepts new conditions or withdraws application.

Acceptance = insurer accepts risk as presented

Competent parties = insured age 18 and sane

What is adhesion?

Insurance policies are contracts of adhesion. Insurance policies are written by one party (insurance company) and the other party (insured) is required to adhere, or stick, to them.

• policy written by the insurance company

• if contract language is not clear, the court will take the side of the insured.

What is aleatory?

Insurance policies are aleatory contracts.

Aleatory = not equal value; small premium for a large amount of coverage.

What is Utmost Good Faith?

The insured and insurance company have a right to expect honesty from each other.

What is unilateral?

Unilateral = only one promise made

• insurance company promises to pay for a covered loss

• insured does not promise to pay the premium

What is a personal contract?

Personal contracts can’t be assigned to someone else.

• auto & homeowner insurance are personal b/c terms are based on personal risks.

• life insurance contracts are not w/ the insured, but w/ the policyowner, so it is not a personal contract. i.e. a wife can apply for a policy on her spouse and/or transfer ownership to her spouse or trust.

What is conditional?

Insurance policies are conditional contracts b/c they require certain conditions to be met in order for contract to be enforced.

• conditonal = insured must pay the premium for coverage and file a claim if a loss occurs

What is indeminity?

Indemnity = make whole, restore to the insured’s original pre-loss condition—no better, no worse!

• indemnification is the principle of restoring an insured to their pre-loss financial state.

• principle applies to health insurance but not life insurance.

What is representation, misrepresentation, and material misrepresentation?

• representation = a statement that is believed to be true, to the best of one’s knowledge at the time it is given.

• misrepresentation = information given that is not true, but would not affect the insurance company’s decision. i.e. wrong digit in their address.

• material misrepresentation = information given that is not true, but does affect the insurer’s decision. i.e. a DUI could avoid coverage.

What is a warranty?

warranty = promise

• a statement that is guaranteed to be true. If not kept, there is a a breach of warranty that voids the contract.

What is concealment?

concealment = failure to disclose

• if intentional and information is material (important), coverage could be voided.

• if not in intentional, coverage cannot be voided.

What is fraud?

fraud = intentional act to cheat another

• voids the policy

What are the penalties of fraud?

• fine and/or imprisonment( 10 - 15 years)

• including embezzlement and/or misappropriate of funds

• imprisonment may be up to 15 years if the false statements jeopardized the safety and soundness of an insurer, and a significant cause of them being in conservation, rehabilitation, or liquidation by the courts.

What is a waiver?

Voluntarily giving up a right.

What is estoppel?

Actions reasonably relied on by one party can’t be denied by the party that accepted same previously.

• i.e. if an insurer accepts late payments, they can’t cancel a policy for late payments later.