2.2.8 COGNITIVE Bias and Decision

1/43

Earn XP

Description and Tags

Analyse how biases are defined against standards of rationality a) Norms, bounded rationality, adaptive value, ecological rationality Understand the fundamentals of expected utility theory b) Utility vs Value, Expected Utility Theory, E = U*p, uncertainty in decision making Understand how heuristics exploit environmental structure c) Recognition heuristic (and when it works) Critique the idea that biases are flaws in reasoning d) Confirmation bias and positive test strategies, Wason's 2-4-6 task, communicative interpretation of the Linda problem Recognise dual-process theories e) System 1 / System 2

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

rational choice theory (RCT)

several versions of RCT but most indicate that to be rational one will calculate costs and benefits

therefore rational decisions → wld maximise the benefit e.g. economic agents shld maximise value or utility

norms are considered an important aspect of rationality

rationality

is a set of norms

be consistent → coherence

correspond to reality → correspondence

norms = rules of action or thought which define optimality

nobody can agree on a complete set of norms for reasoning

fairness norms + rational choice theory (Opp,2013)

not line with a narrow concept of rational choice theory (Opp, 2013) as they do not maximise benefits rather the benefits rather than the benefit is shared

norms fall short of explaining RCT and so shld norm following be argued as irrational

two biases

availability bias

framing bias

availability bias

over-estimating the frequency of plane crashes (rare or memorable events)

framing bias

switching your decision based on the question framing (e.g. would you buy another ticket if you dropped it on the way to the cinema vs if you dropped £10 on the way to the cinema)

coherence error

correspondence error

violates norms of rationality

which errors correspond to the biases

coherence

correspondence

coherence error corresponds to…

framing bias

correspondence error corresponds to…

availability bias

rationality + probability

to make rational decisions in situations of uncertaintly we may be expected to understand probability

maximise expected value

linda task

linda task:

linda is 31yo, single, outspoken, v bright. she studied philosophy at uni. as a student, she was deeply concerned w issues of discrimination and social justice, and also participated in anti war demonstrations.

which is more likely:

linda is a bank teller

linda is a bank teller and is active in the feminist movement

Tversky et al., (1983)

violation of norm and conjuction fallacy

option two must be less likely than option one bc option 2 is a subset of option 1, and option 2 requires two things to be true whilst option 1 only 1

most ppl intuit option 2 is the answer, in defiance of the norms, specifically the laws of probability.

most Ps make a conjunction fallacy as they have made error in reasoning by assuming that specific conditions are more probable than a single, more general condition

stanford grad school of business error on linda task

made 85% error on linda task despite having taken several advanced courses in probability, stats, and decision theory

conjunction fallacy

an error made where ppl judge that the probability of A + B events occuring is more likely than A occuring, despite that fact adding more info = lower prob

decision calculus

how we shld make rational decisions:

logical

probabilities

systematic consideration of all options

probability and decision making: two key considerations

value and utility

why it is difficult to make decisions

future uncertain

need to assess potential risks and benefits

choose a course of action to increase the chance of a positive outcome

need to use knowledge to estimate probabilities of future events

rationality: probability based on…

value

rationality, probability based on value. in monetary terms:

expected value `(value investment will have in future)

good bet is one for which the expected value is greater than the amount invested

bad bet is one for which the expected value is less than the amount invested

rational choice wld be to maximise expected value

tendency of ppl to accept a sure outcome over a riskier outcome = risk aversion

monetary value NOT always most important factor in dec making

expected utility theory

theory of decision under risk/uncertainty

each option leads to one set of outcomes

where p is known

individuals place subjective value utility on outcomes

EU = weighted avg of satisfaction from possible outcomes

w accumulating evidence, EUT became a theory of norms (model of how ppl ought to choose) and rationality

Bernoulli (1738)

suggests that the value of a gamble to an individual =/= to its expected monetary value

developments in non-expected utility theory

behaviour not always in like w EUT- does that make us irrational decision makers?

expected utility theory + rationality

calculating the option with the highest expected utility is a decision making method

rational decision making = assume choose option that maximises our utilit

value = utility? true or false

value is not utility

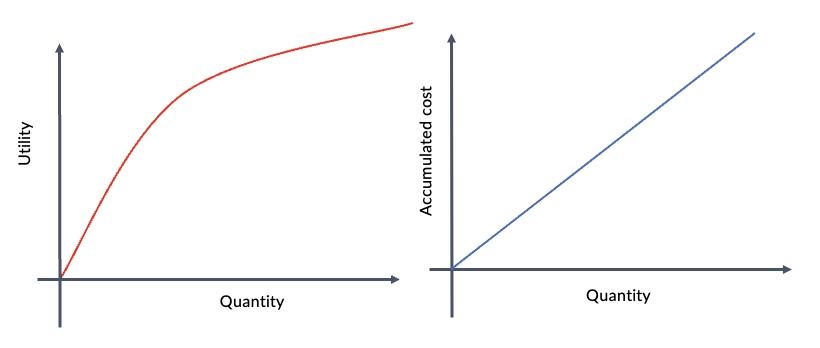

marginal utility

the additional satisfaction gained by a unit of goods/services

the diminishing marginal utility of wealth

as amt of money one has increases, each addition to ones fortune becomes less important, from a personal, subjective pov

an extra 1000 means little to Bill Gates, quite a lot for uni student

why is value not the same as utility?

bc of marginal utility

and

utility is compressed with respect to value (u do not enjoy 10 pizzas 10x more than 1 pizza, altho 10 pizzas costs 10x more than 1 pizza)

utility = how much u enjoy/prefer it- the degree to which it contributes to overall wellbeing/satisfies ur desires

one way of measuring utility is willingness to pay

according to EUT, ppl shld behave to maximise expected utility

utility

how much u enjoy/prefer it- the degree to which it contributes to overall wellbeing/satisfies ur desires

utility =/= value example

option a: coin flip- heads win £1k, tails win 0

option b: no coin flip = £499

expected value b = 499, expected value a = 500, but most will still opt for b

utility attached to first 499 greater than additional 501

what effects expectation?

uncertainty

uncertainty effects expectation- thought example

if wld pay 10 for pizza, how much wld u pay for

10% chance to win a pizza

a pizza which had a 1/100 chance of making u sick

calculating expected utility

E = p x U

Expected Utility (E) =

Probability (P) x Utility (U)

calculating expected utility under multiple options

E = p1 x u1 + p2 x u2, etc

EU (E) needs to exceed cost

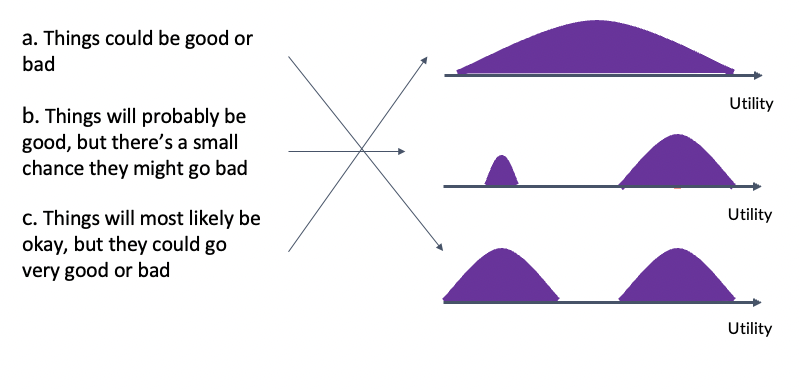

effect of uncertainty

everything is uncertain, question is how much

uncertain neutrally = 2 low and high normal distributions of utility

probably be good, small chance go bad = tiny nd over low, regular nd over high

probably be ok, but cld go very good or bad- giant, flatter nd over whole u graph

do we use norms, probabilities and EU in real world decision making?

evidence suggests we are not as rational as we are not very proficient at probability, and we do not always choose the optimal outcomer