1.2 - Monetary model

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

28 Terms

Floating ER - assumptions

AS curve vertical

price is flexible

Supply Side factors which make up AS not modelled (tech or K accumulation)

Small local economy

Foreign variables taken as given

Simple Demand for money

Not dependent on interest rates

Only depends on real income

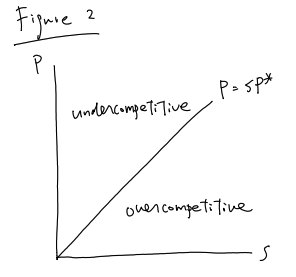

PPP holds

SP* = P

demand for real money balance - equation

Md / p = kY

kY - Share of total output

Money market equilibrium

MS = Md

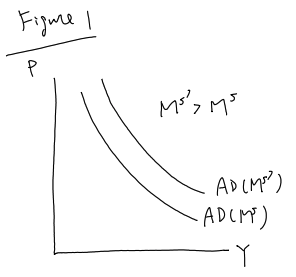

Simple AD relation - equation

MS = kPY

Md / P = kY → Md = kPY

MS = Md

Simple AD relation - graphically

PPP holds - graph

Monetary model equilibrium

Using AD-AS relation

MS = MD = kPY → P = MS / kY

PPP holds by assumption

P = SP*

MS / kY = SP* → S = MS / kP*Y

What changes Model equilibrium

If MS rises, S rises (depreciation)

If output (Y) rises, S falls (appreciation)

If foreign price (P*) rises, S falls (appreciation)

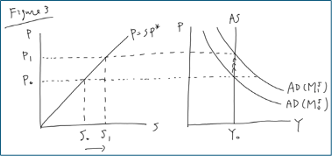

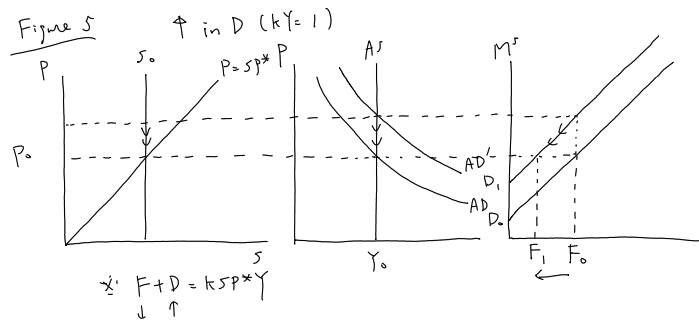

Money Supply increase effects on equilibrium - graph + explanation

If MS increases (treat MS as exogenous):

At initial p (p0 = S0P*) there is excess D for goods

Since Y fixed (Y0), p rises → dom goods now relatively more expensive

D for H goods & H currency falls

Dom currency depreciates to keep competitiveness for PPP to be preserved

decrease proportional to increase in MS

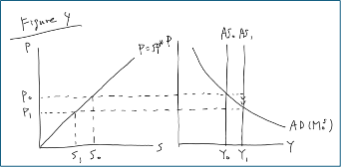

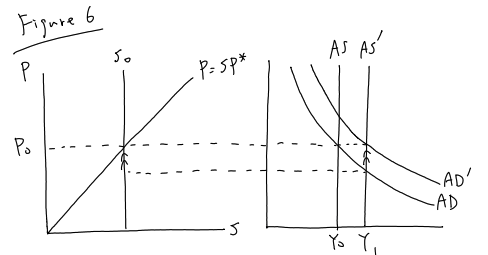

Income increase effects on equilibrium - graph + explanation

Income (Y) increases (Y exogenous in model):

At original p (p0) there is excess supply

p falls to keep money market in equilibrium

Exchange rate appreciates (S falls) – to restore competitiveness of F goods

Balance sheet of a Central Bank (CB)

Assets

Domestic-currency bonds (D)

Foreign exchange reserves (F)

Liabilities

High powered money (H)

Ms in a fixed ER

Ms = hH = h(F+D)

h - money multiplier

assume h = 1 (Money consists of currency only)

If CB holding of D increases -> monetary base increases -> MS increases through the money multiplier (expansionary MP)

Ms = F+D

Fixed ER assmptions

Dom Output (Y) + Foreign price (P*) - Exogenous

MS no longer exogenous

CB adjusts Foreign reserves (F) to preserve ER

When other exogenous variables change (shock)

Money supply increase (↑ in D) - graph + explanation

An increase in govt bonds (D) leads to increase in MS (expansionary MP)

Shifts AD upwards from the excess demand -> increases P (domestic price index)

Dom goods become under-competitive → Which leads to demand falling + D for dom currency falls

Without CB intervention, dom currency would depreciate to correct competitiveness (floating ER)

To preserve fixed exchange rate, CB buys dom currency using Foreign reserves (F)

F falls till competitiveness restored

An increase in D is exactly offset by a decrease in F (MS falls so movement along AS curve)

F = kS0P*Y – D

Asset composition changes (F falls but D increases)

PPP doesn’t shift at all so p & output (Y) doesn’t change

Income increase with fixed ER - G + E

Shock to income (Y)

dont need MS diagram as assumed kY = 1 implicitly (so always consistent)

Y increases due to supply side shock → AS curve shifts right

At initial price (p0) there is excess supply → Dom price falls and dom goods become over-competitive as they are cheaper

Demand for home currency increases -> Without CB intervention Dom currency would appreciate to correct competitiveness

CB increases F reserves (F) -> Issue dom currency & buy F currency to keep exchange rate constant

F increases for given D → MS increases → AD shifts upwards until PPP restored

Output (Y) increase BUT price fixed + CB now hold more F

Asset price approach

Dynamic version of the model with nominal exchange rate viewed as an asset price

PPP still holds

Money demand function with nominal interest rate - dynamic

PPP in logs - dynamic

Rational expectations

Rational expectations use all information available

Peoples subjective expectations conditional on all information available today

UIP with expectation

Combine UIP with logs equation

Difference in H & F interest rate should be equal to expectation of depreciation rate

What does γt equal

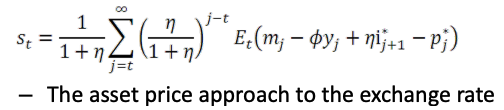

Combined equation - st

law of iterated expectations

Expanded st with 1 level of expectations

Expanded using Law of iterated expectations

Expanded st with all levels of expectations & iteration

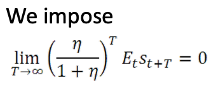

Asset bubble restriction (on iteration)

The assumption rules out a bubble situation where p keeps increasing at a fast rate

limit of present discounted value of terminal ERs

Non-bubble condition hold if s increasing at slower rate than (n/1+n)^t inverse

Final st equation

Exchange rate today is a function of:

Expectation of future money S + output in the future + future foreign interest rate + future foreign p