1.2 How Markets Work

1/119

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

120 Terms

Rationality

The assumption that economic agents will maximise the benefit gained from an economic transaction

(e.g. consumers maximise utility and producers maximise profits)

Utility

The satisfaction gained through the consumption of a good/service

Irrationality

The assumption that economic agents make decisions that do not maximise the benefits gained from an economic transaction due to social influence, habitual behaviour or poor computation skills

Reasons for irrationality (Genevieve Problem) - social influence

Social influence; when consumers purchase goods that do not maximise net gain, as the behaviour of others influences them to fit into society

(e.g. buying branded clothing to fit in)

Reasons for irrationality (Genevieve Problem) - habitual behaviour

Habitual behaviour; when consumers purchase goods that do not maximise net gain due to a routine or habit, often done to save time in decision making

(e.g. buying the same brand of bread)

Reasons for irrationality (Genevieve Problem) - weakness at computation

Weakness at computation (calculation); consumers purchase goods that do not maximise net gain because they simply lack the mathematical ability to calculate utility

(e.g. Herbert Smith's theory)

Deep rationality

Behaviour that appears irrational but may in fact be rational when exploring the sources of satisfaction

(e.g. buying expensive clothing, but it helps you fit in, giving satisfaction)

Evaluation for rationality

Friedrich Hayek's Snooker Players Experiment

The fact that snooker players are able to calculate angles and forces must suggest that humans have the innate ability to understand complex mathematics and hence have innate rationality

Evaluation for irrationality

Demand

The quantity of a good or service that consumers are willing and able to purchase at a given time at a given price

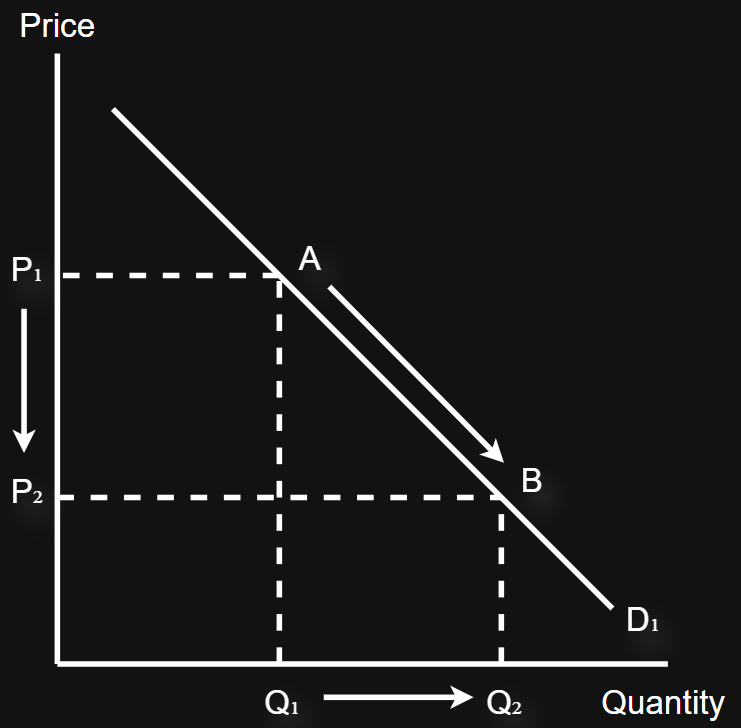

Law of demand

Assuming ceteris paribus, as the price of a good decreases, the quantity demanded increases; and as the price increases, the quantity demanded decreases

Movement in the demand curve

A movement in the demand curve occurs when there is a change in price

A decrease in price = an extension in demand

An increase in price = a contraction in demand

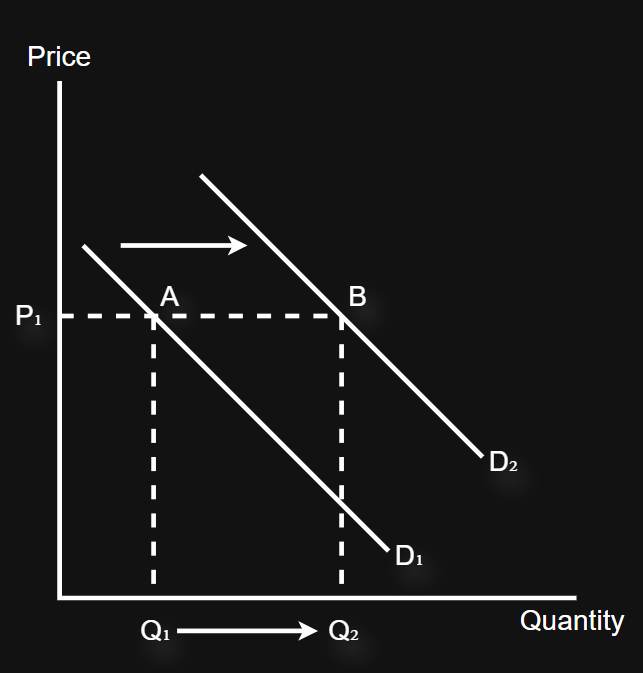

Shift in the demand curve

A shift in the demand curve is caused by non-price factors

Population

Income

Related goods (substitutes and complements)

Advertising

Tastes and fashions

Expectations

Seasons

Explaining the shape of the demand curve

The demand curve shows the maximum price each consumer is willing to pay for a good/service

The maximum they are willing to pay would be the maximum utility they would receive

Maximum price = maximum utility

Factors causing a shift in demand - population

Assuming ceteris paribus, a higher population = a greater number of willing consumers

Factors causing a shift in demand - income

More income = greater consumer purchasing power = greater ability to gain utility = higher demand

Factors causing a shift in demand - related goods (complements)

Complements - products where the utility of one good is raised by the joint consumption of the other

(e.g. tea and sugar are weak complements, tennis ball and racket are strong complements)

Demand curve of complements

As the price of tea decreases (extension in demand), the demand for sugar shifts to the right (price remains the same, but quantity demanded increases)

Negative relationship

Factors causing a shift in demand - related goods (substitutes)

Substitutes - products where the utility gained by one good can be replaced/substituted with another good

(e.g. coke and pepsi)

Demand curve of substitutes

As the price of pepsi falls (extension in demand), the demand for coke shifts to the left (price remains the same, but demand decreases)

Positive relationship

Factors causing a shift in demand - advertising

Greater advertising of a product = more consumers are aware of the product = an increase in demand

Firms can also use adverts to increase the perceived utility of a product, therefore increasing the demand for it

Factors causing a shift in demand - tastes and fashions

When a good becomes trendy or fashionable, it becomes desirable to a greater number of consumers (social influence) = higher demand

Deep rationality can also explain trends and fashions

Factors causing a shift in demand - expectations

Expectations refer to investors' predictions of future price movements when trading speculative assets (cryptocurrency, stocks and shares, housing, vintage cars)

If investors expect a future price rise, more will buy the asset in order to profit, resulting in an increase in demand

If investors expect a future price fall, less will buy the asset as it is less profitable, resulting in a decrease in demand

Factors causing a shift in demand - seasons

The utility gained from certain products may vary with the weather or seasons

(e.g. consumers gain a higher utility when buying ice cream in the summer)

Speculative demand

Speculative demand can create a 'self-fulfilling prophecy' whereby investors believe an asset will rise in price, hence they purchase more, increasing demand, in line with the investors belief

Expectation of a price increase = an actual price increase = an increase in future prices - hence stuck in a loop

Law of diminishing marginal utility

The satisfaction consumers gain from the last unit of a good/service consumed falls with the number of units consumed

Supply

The quantity of a good or service that a producer is willing and able to produce at a given price at a given time

Law of supply

Assuming ceteris paribus, as the price of a good increases, the quantity supplied increases; and as the price decreases, the quantity supplied decreases (explanation of profit)

Joint supply

When the production of one good automatically results in the production of another good

(e.g. beef and leather)

Competitive supply

When the production of one good reduces the ability to produce another good

(e.g. wheat and barley, if a farmer increases the production of wheat, there would be less land to produce barley)

Movement in the supply curve

A movement in the supply curve occurs when there is a change in price

A decrease in price = contraction in supply

An increase in price = extension in supply

Shift in the supply curve

A shift in the supply curve is caused by non-price factors

Productivity

Indirect tax

Number of firms

Technology

Subsidies

Weather

Cost of production

Factors causing a shift in supply - productivity

An increase in productivity allows a firm to produce more output with the same levels of input, increasing the supply

(e.g. better machinery or incentives for employees)

Factors causing a shift in supply - indirect tax

An increase in indirect taxes (VAT) can cause a leftwards shift in supply as the cost of production increases

Factors causing a shift in supply - number of firms

When new firms enter the market, there are more producers supplying the good, causing a rightwards shift, increasing the total market output at every price level

More firms also incentivise producers to increase productivity, which also increases supply

Factors causing a shift in supply - technology

Technological improvements can increase productivity as they allow firms to produce more output with the same level of inputs, increasing the supply

Factors causing a shift in supply - subsidies

A subsidy from the government can lower costs, allowing firms to produce more output at every price level, causing a rightwards shift in supply

Factors causing a shift in supply - weather

Favourable weather can increase the supply in markets regarding agriculture or tourism

Factors causing a shift in supply - cost of production

High costs of production make it more expensive for firms to produce the good/service, hence they are less willing to supply, as it may hinder profitability

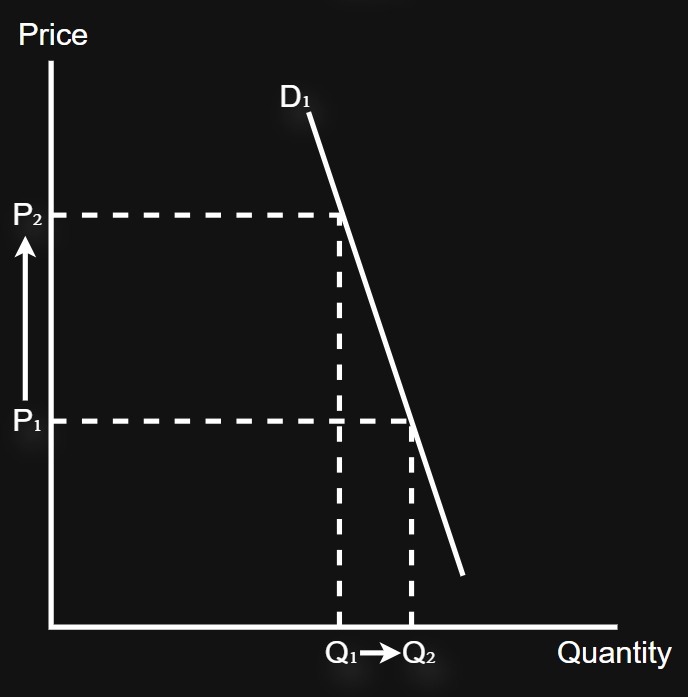

Price elasticity of demand

Measures the responsiveness of quantity demanded to a change in the price of a given product over a given period of time

PeD formula

(% ∆ in quantity demanded)/(% ∆ in price)

PeD is always negative, quantity demanded and price have a negative relationship

Law of PeD

Assuming ceteris paribus, when the price increases, quantity demanded decreases; when the price decreases, quantity demanded increases, hence the value of PeD will always be negative (negative relationship)

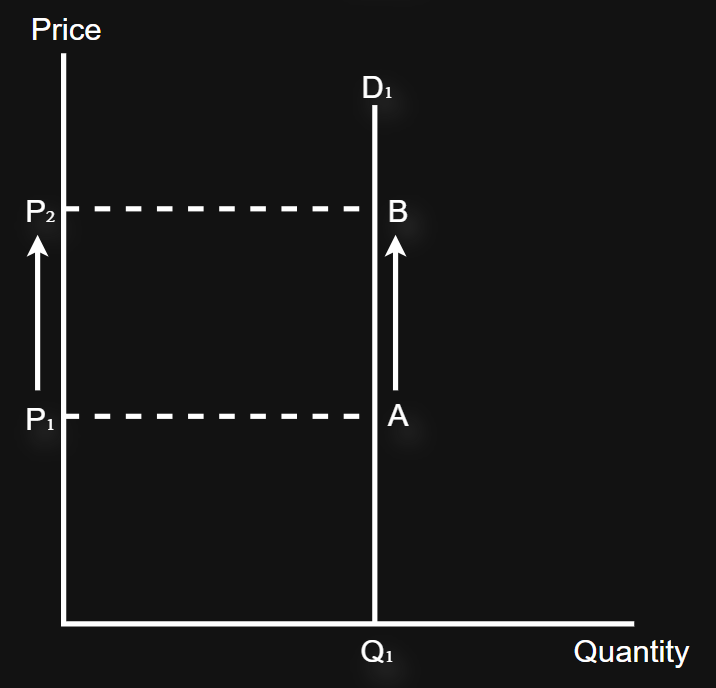

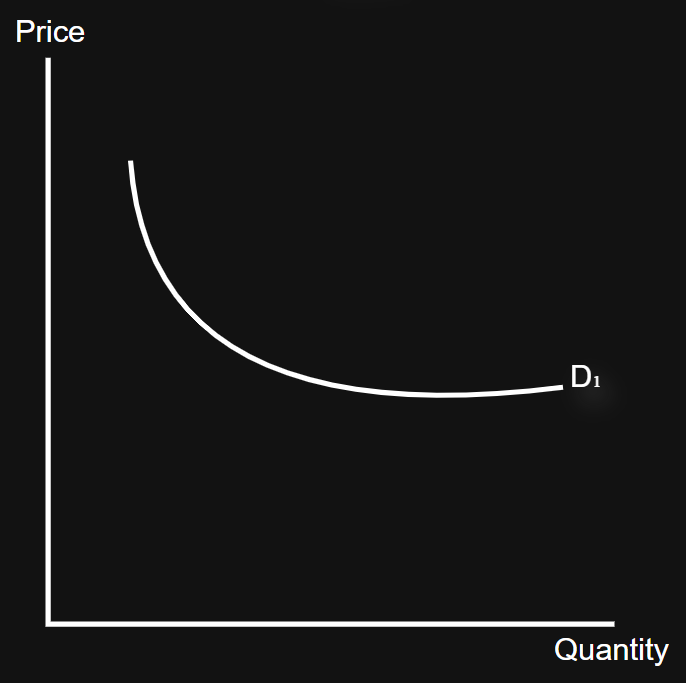

Perfectly inelastic demand

(% ∆ in quantity demand) = 0

(% ∆ in quantity demand)/(% ∆ in price) = 0

Relatively inelastic demand

(% ∆ in quantity demanded) < (% ∆ in price)

(% ∆ in quantity demanded)/(% ∆ in price) < 1

Unitary elastic demand

(% ∆ in quantity demanded) = (% ∆ in price)

(% ∆ in quantity demanded)/(% ∆ in price) = 1

Relatively elastic demand

(% ∆ in quantity demanded) > (% ∆ in price)

(% ∆ in quantity demanded)/(% ∆ in price) > 1

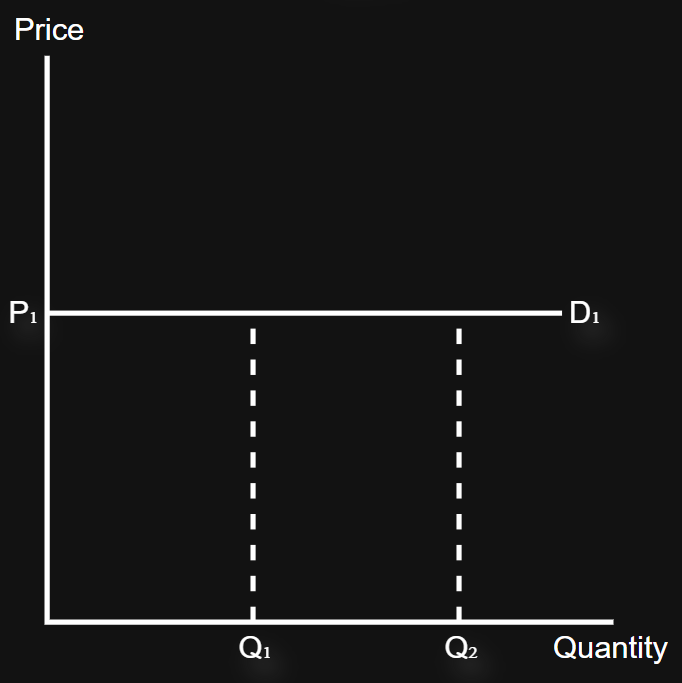

Perfectly elastic demand

(% ∆ in price) = 0

(% ∆ in quantity demanded)/(% ∆ in price) = ∞

Factors affecting PeD - price as a proportion of income

Elastic - price is a large % of income

(e.g. if UK house prices rise, there would be a big change in demand)

Inelastic - price is a small % of income

(e.g. if the price of chocolate increases, there would be a small change in demand as it is still affordable)

Factors affecting PeD - addictiveness

Elastic - no addictive properties = no compulsion to buy

Inelastic - addictive properties = consumers feel a psychological compulsion to buy, regardless of price

Factors affecting PeD - necessities

Elastic - luxury goods do not aid survival, hence consumers will stop buying with a rise in price (low loyalty)

Inelastic - necessity goods aid survival, hence consumers will continue to buy with a rise in price

Factors affecting PeD - time to react

Elastic - long time for consumers to react to a change in price

Inelastic - short time for consumers to react to a change in price, hence there is no time to gather information and plan changes in spending

Factors affecting PeD - substitutes

Elastic - lots of substitutes, hence consumers switch to alternatives

Inelastic goods - lack of substitutes, hence consumers do not switch to alternatives

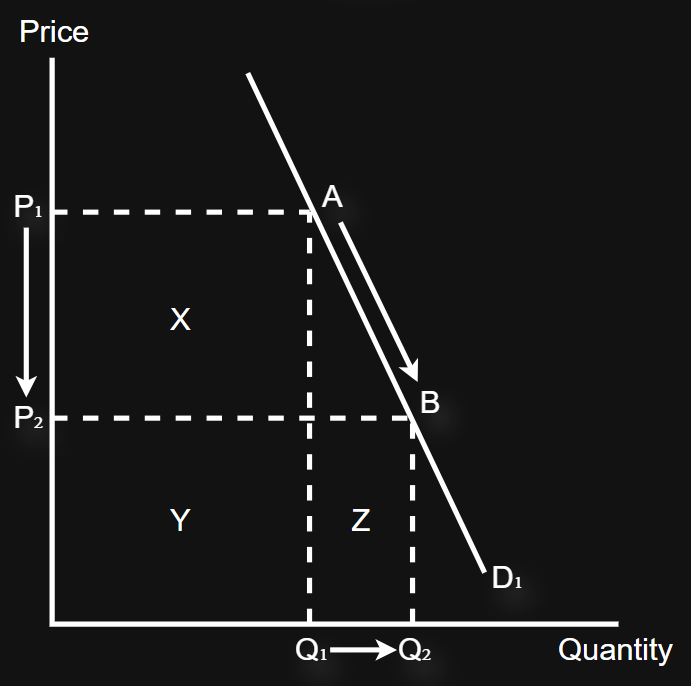

Relationship between PeD and total revenue

Whether a firm’s total revenue increases or decreases when it changes price is dependent on the elasticity of demand for the good/service

Elastic demand and total revenue

(% ∆ in quantity demanded) > (% ∆ in price)

When price decreases, there is a large increase in quantity demanded, hence you gain more total revenue

When price increases, there is a large decrease in quantity demanded, hence you lose more total revenue

Inelastic demand and total revenue

(% ∆ in quantity demanded) < (% ∆ in price)

When price increases, there is a small decrease in quantity demanded, hence you gain more total revenue

When price decreases, there is a small increase in quantity demanded, hence you lose more total revenue

Income elasticity of demand

Measures the responsiveness of quantity demanded to a change in consumers income of a given good over a given period of time

It is determined by a non-price factor (income), hence it causes a shift in demand, not a movement

YeD formula

(% ∆ in quantity demanded)/(% ∆ in income)

YeD can either be positive or negative, depending on the type of good

Normal goods

Quantity demanded and income have a small POSITIVE relationship (YeD is between 0 and 1)

Luxury goods

Quantity demanded and income have a large POSITIVE relationship (YeD is greater than 1)

Inferior goods

Quantity demanded and income have a NEGATIVE relationship (YeD is less than 0)

Importance of YeD to producers

In a boom (high average incomes), rational producers would switch from inferior goods to normal/luxury goods

In a recession (low average incomes), rational producers would switch from normal/luxury goods to inferior goods

Cross elasticity of demand

Measures the responsiveness of the quantity demanded for one good following a change in the price of another good

Only references complements and substitutes, therefore it relates to shifts in demand, following a change in the price of a related good

XeD formula

(% ∆ in quantity demanded of good A)/(% ∆ in price of good B)

XeD - complements

An increase in the price of tennis rackets = a decrease in quantity demanded of rackets

A decrease in quantity demanded of rackets = a decrease in quantity demanded of tennis balls

Therefore XeD is negative, as there is a negative relationship between quantity demanded and price

Strong vs weak complements

Strong complements - XeD is greater than 1 (elastic)

(e.g. left and right shoes)

Weak complements - XeD is less than 1 (inelastic)

(e.g. fish and chips)

XeD - substitutes

An increase in the price of coke = a decrease in quantity demanded of coke

A decrease in the quantity demanded of coke = an increase in quantity demanded of pepsi

Therefore XeD is positive, as there is a positive relationship between quantity demanded and price

Strong vs weak substitutes

Strong substitutes - XeD is greater than 1 (elastic)

(e.g. coke and pepsi)

Weak substitutes - XeD is less than 1 (inelastic)

(e.g. coke and coffee)

Unrelated goods

Unrelated goods have an XeD of 0

When a change in the price of one good has no effect on the demand for the other

Price elasticity of supply

Measures the responsiveness of quantity supplied following a change in the price of a given product over a given period of time

PeS formula

(% ∆ in quantity supplied)/(% ∆ in price)

PeS is always positive, quantity supplied and price have a positive relationship

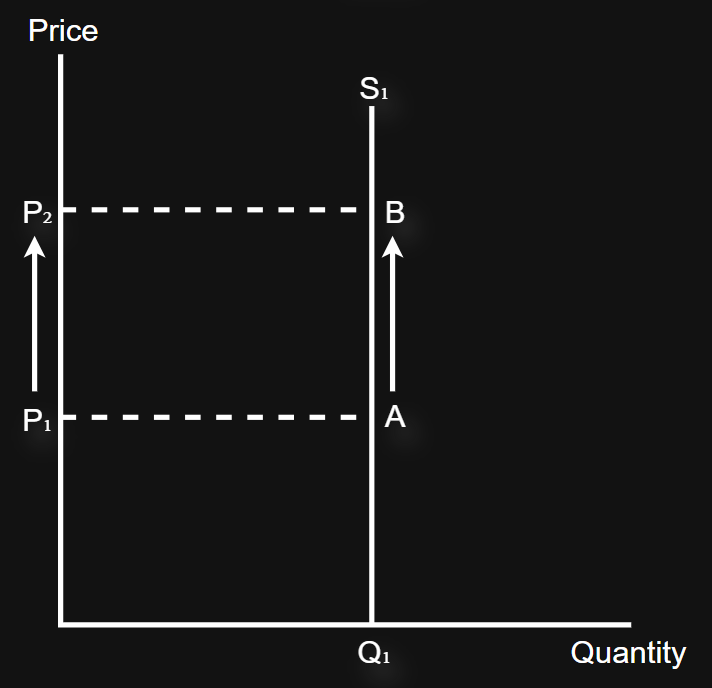

Perfectly inelastic supply

(% ∆ in quantity supplied) = 0

(% ∆ in quantity supplied)/(% ∆ in price) = 0

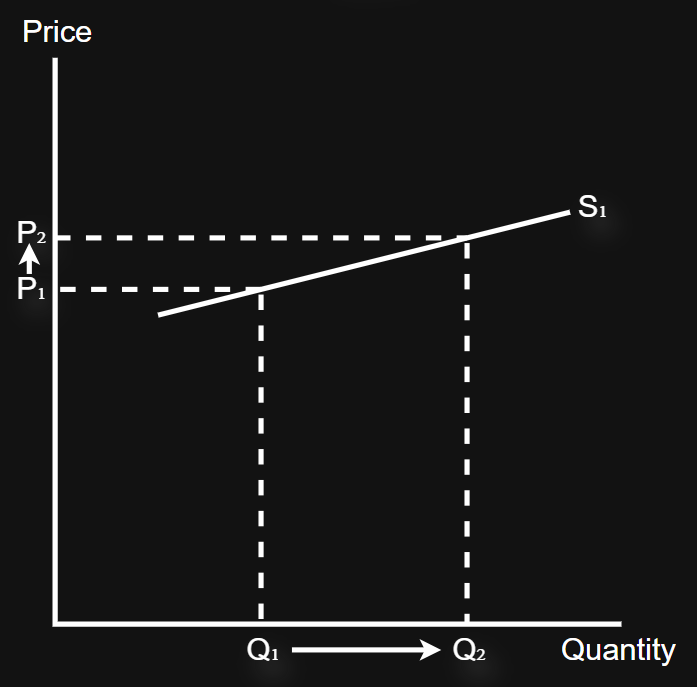

Relatively inelastic supply

(% ∆ in quantity supplied) < (% ∆ in price)

(% ∆ in quantity supplied)/(% ∆ in price) < 1

Unitary elastic supply

(% ∆ in quantity supplied) = (% ∆ in price)

(% ∆ in quantity supplied)/(% ∆ in price) = 1

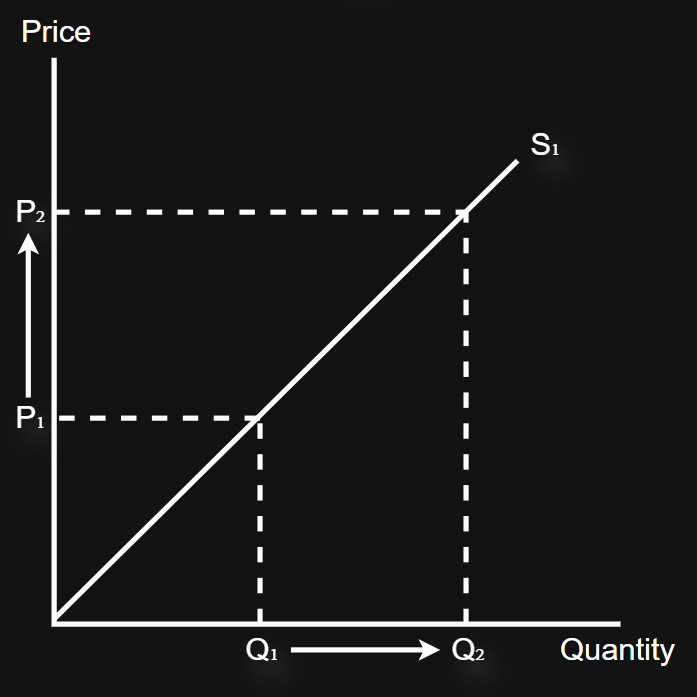

Relatively elastic supply

(% ∆ in quantity supplied) > (% ∆ in price)

(% ∆ in quantity supplied)/(% ∆ in price) > 1

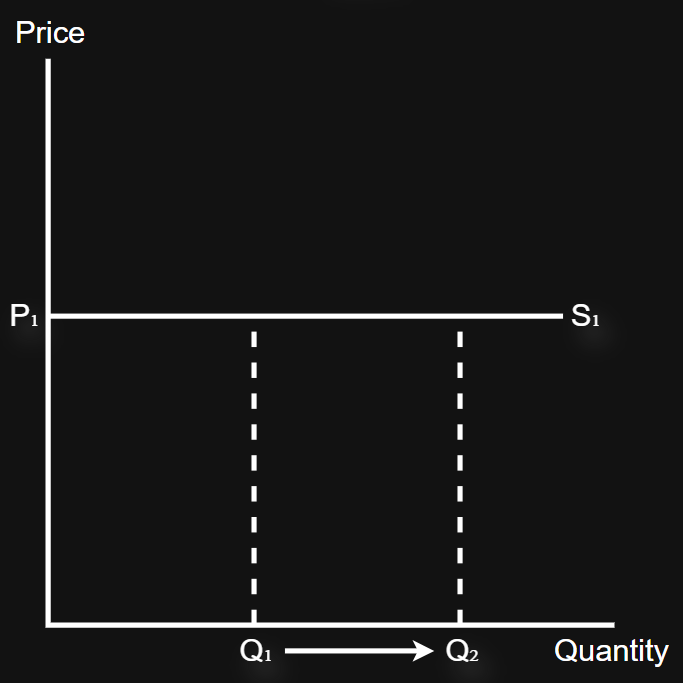

Perfectly elastic supply

(% ∆ in price) = 0

(% ∆ in quantity supplied)/(% ∆ in price) = ∞

Factors affecting PeS - stockpiles/perishability

Elastic - goods that can be stockpiled can be easily released into the market if prices rise

Inelastic - perishable goods cannot be stored, hence the good must be made from scratch if prices rise

Factors affecting PeS - time to produce

Elastic - short time to produce = quantity supplied can easily increase as sellers can produce quickly

Inelastic = long time to produce = quantity supplied cannot easily increase as sellers cannot produce quickly

Factors affecting PeS - access to factors of production

Elastic - if factors of production are readily available, firms can use this input to increase output

Inelastic - if there are shortages of factors of production, firms will not have the input available to increase output

Factors affecting PeS - barriers to entry

Elastic - low barriers to entry = easy for new firms to join the market when prices rise, hence they can all increase market supply

Inelastic - high barriers to entry = hard for new firms to join the market when prices rise, hence it is hard for a few firms to increase the market supply

Short-run PeS

Long-run PeS

Equilibrium

The price and quantity which markets are stable because demand is equal to supply

The price in a market will always gravitate towards the equilibrium, never away from it

Short side

The inability of economic agents to fulfil market plans

Consumers - to purchase goods

Producers - to sell goods

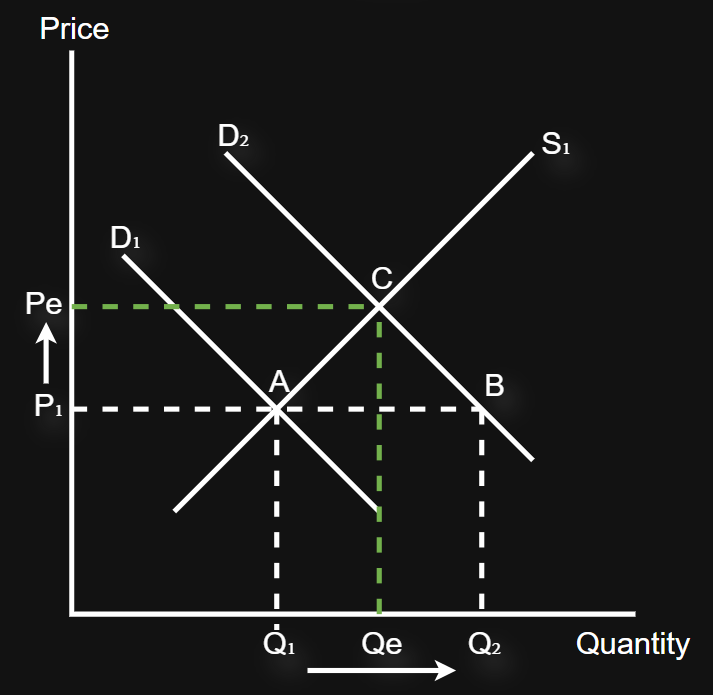

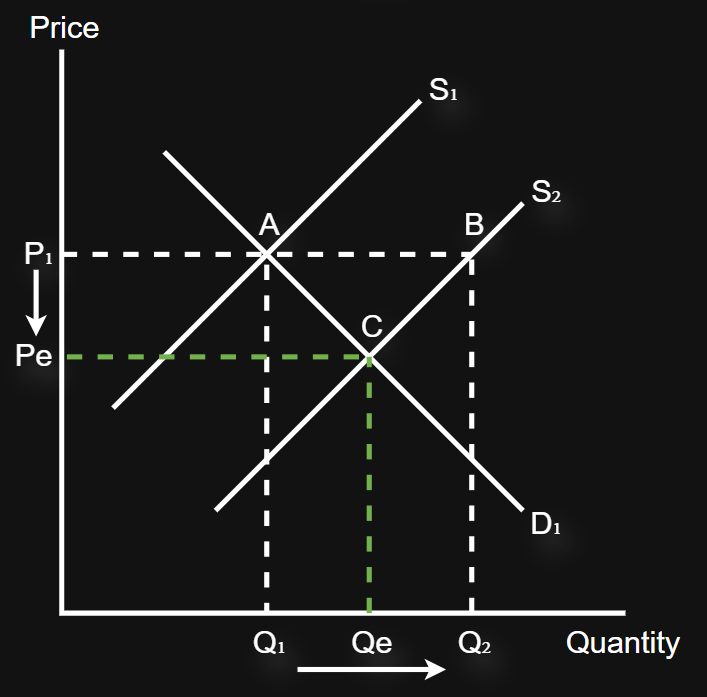

Excess demand

When prices start too low (below the equilibrium), consumers will be left on the short side, therefore they will have the incentive to increase the price (they are more willing to pay at a higher price) to help attract a producer

However, some consumers will leave the market as the price rises (demand contracts - B to C)

An increase in price encourages more producers to enter the market (supply extends - A to C)

When prices reach equilibrium, the market is static because all buyers have a seller, therefore none are on the short side, so none have the incentive to change prices

Excess supply

When prices start too high (above the equilibrium), producers will be left on the short side, therefore they will have the incentive to decrease the price to help attract a consumer

However, some producers will leave the market as the price falls (supply contracts - B to C)

A decrease in price encourages more consumers to enter the market (demand extends - A to C)

When prices reach equilibrium, the market is static because all sellers have a buyer, therefore none are on the short side, so none have the incentive to change prices

Shifts in equilibrium

Non-price factors in demand or supply create a new equilibrium

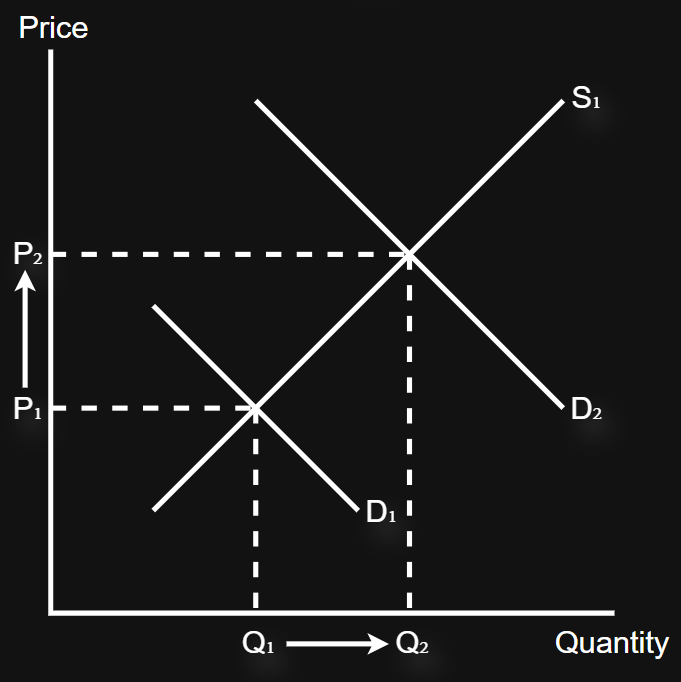

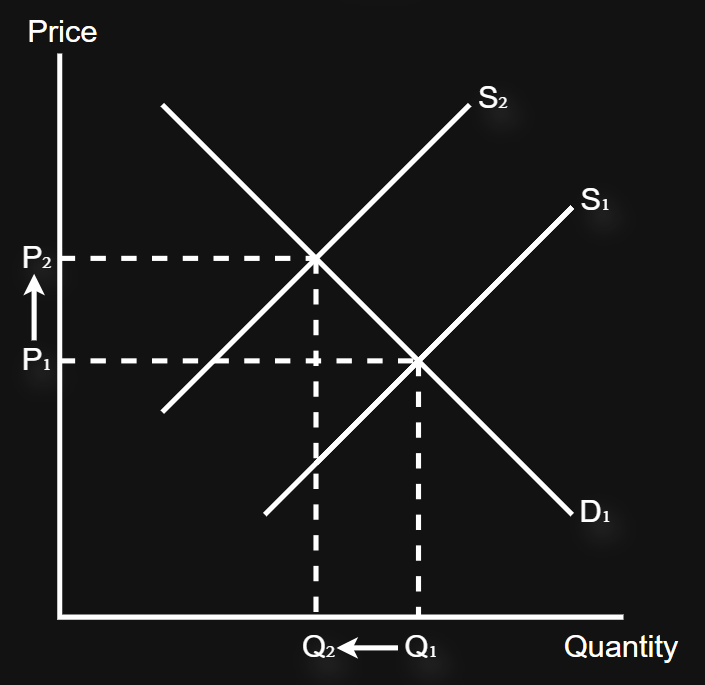

Equilibrium diagram (increase in demand)

An increase in demand causes an increase in price and quantity

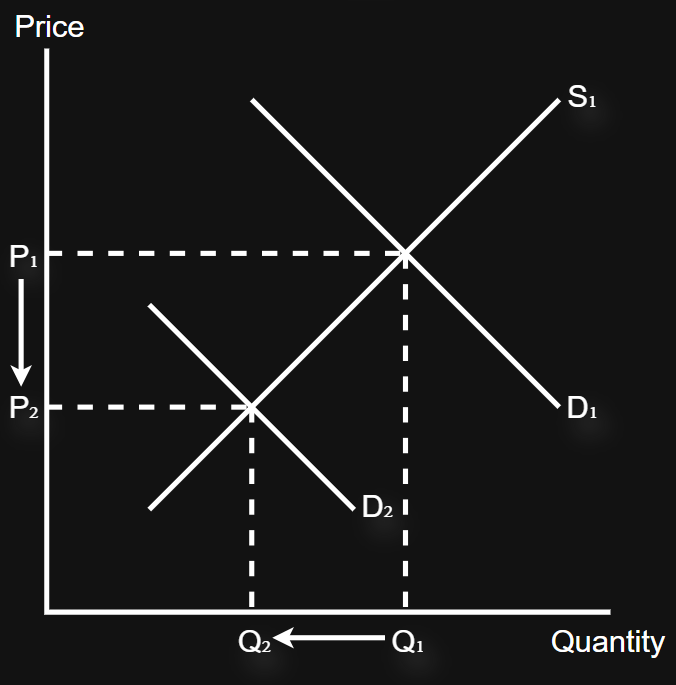

Equilibrium diagram (decrease in demand)

A decrease in demand causes a decrease in price and quantity

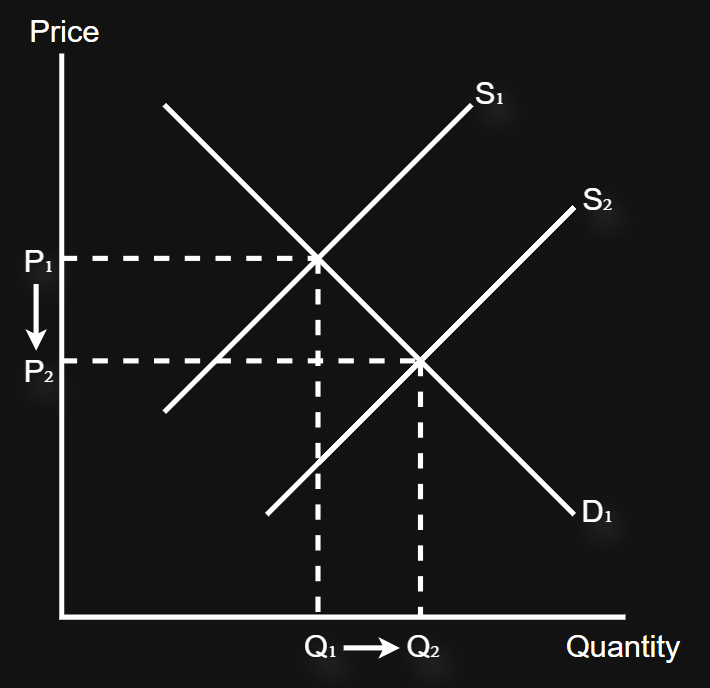

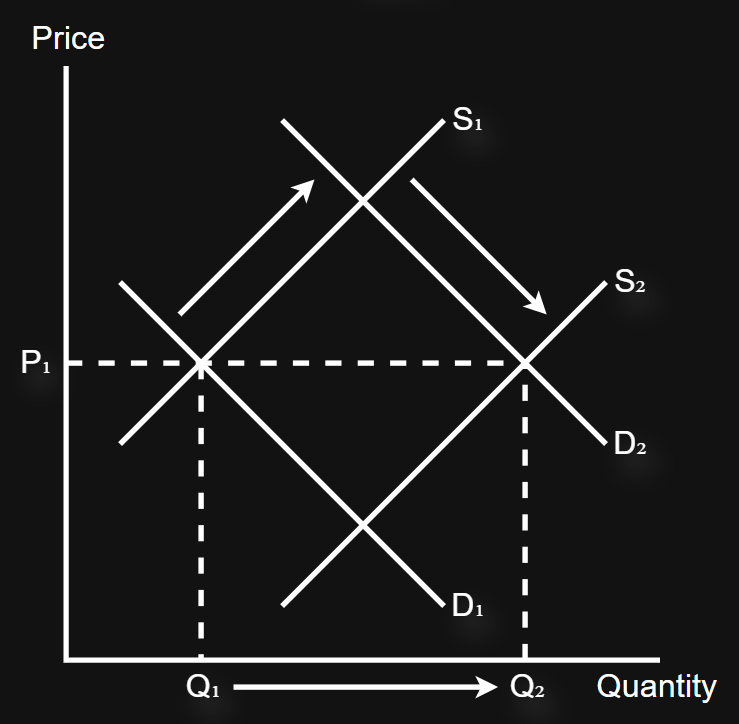

Equilibrium diagram (increase in supply)

An increase in supply causes a decrease in price and an increase in quantity

Equilibrium diagram (decrease in supply)

A decrease in supply causes an increase in price and a decrease in quantity

Complex explanation of a change in the equilibrium price

The old equilibrium shifts due to a non-price factor in either supply or demand

This creates a new equilibrium and hence creates either excess demand or supply

Economic agents on the short side (buyers or sellers) will resolve the excess demand or supply by increasing or decreasing the price

This creates a new equilibrium

Equilibrium price evaluation

The magnitude price and quantity changes by is dependent on the elasticity of demand and supply, respectively

A shift in demand can be evaluated with PeS

A shift in supply can be evaluated with PeD

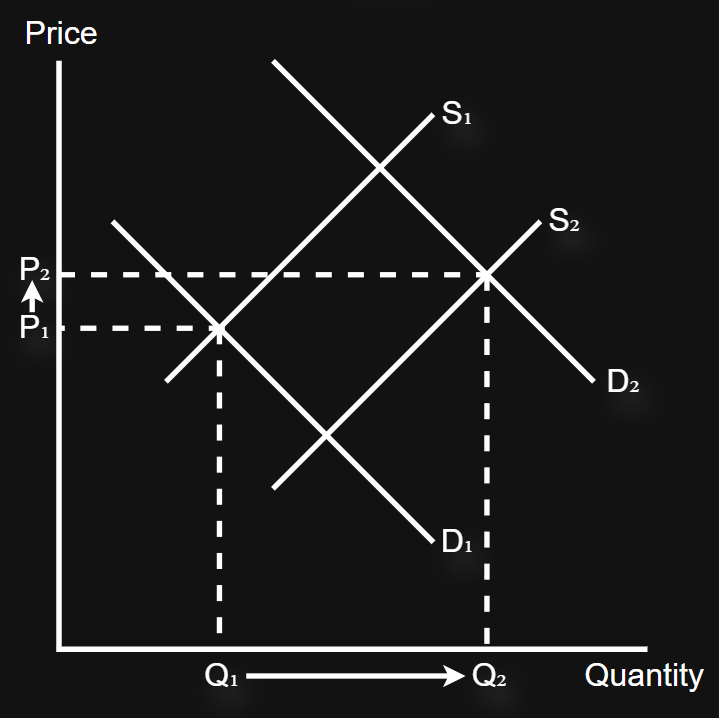

Double shifts (price remains the same)

Demand and supply shift by an equal amount, hence the price remains the same

Double shifts (increase in price)

When demand increases, and the magnitude of the increase is greater than the change in supply, price will always INCREASE, and the quantity will always INCREASE

When supply decreases, and the magnitude of the decrease is greater than the change in demand, the price will always INCREASE, and the quantity will always DECREASE

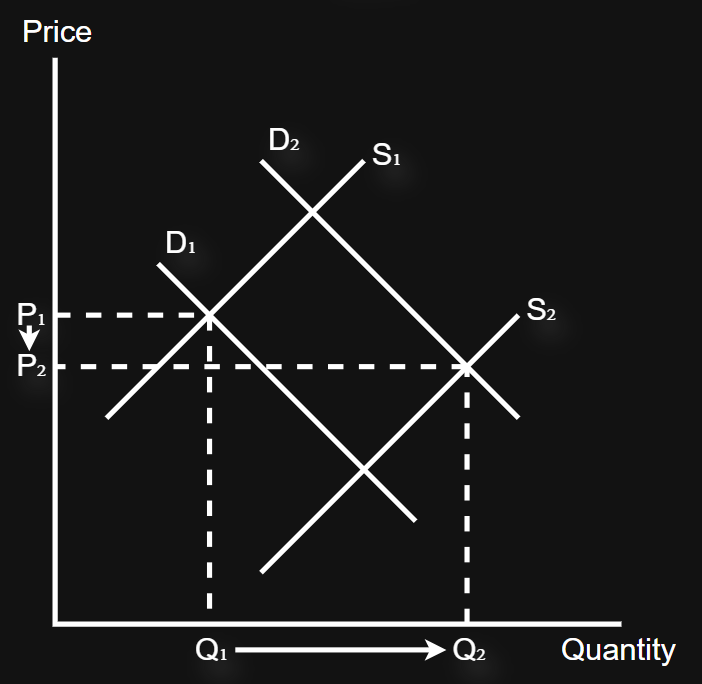

Double shift (decrease in price)

When demand decreases, and the magnitude of the decrease is greater than the change in supply, price will always DECREASE, and the quantity will always DECREASE

When supply increases, and the magnitude of the increase is greater than the change in demand, the price will always DECREASE, and the quantity will always INCREASE

Complex explanation of equilibrium with elasticity

When a curve shifts, it causes an extension/contraction along the other curve, the size of the extension/contraction is dependent on the elasticity

(e.g. when supply shifts right, excess supply is created (leaving producers on the short side), encouraging producers to decrease prices, this reduction in price leads to an increase in quantity (extension of demand), the size of the extension of demand is dependent on the elasticity of PeD)

Price mechanism

The role price plays in the allocation of scarce resources

Price mechanism - signalling

Prices send information to buyers or sellers about the relative costs and benefits of allocating resources in a particular way

Depicted by a shift in demand/supply, where the buyers/sellers are on the short side, hence they increase/decrease price (excess demand and supply)

Price mechanism - incentive

Prices encourage buyers/sellers to change their market behaviour

(e.g. an increase in price incentivises buyers to purchase less, and sellers to produce more, and vice versa)

Depicted by extensions/contractions in supply

(e.g. increase in price = greater incentive to supply, a decrease in price = less incentive to supply)

Price mechanism - rationing

Price determines who is allocated scarce resources by preventing consumers less willing and able to pay from consuming the good (assuming prices rise)

Depicted by extensions/contractions in demand

(e.g. increase in price = consumers are rationed out, a decrease in price = consumers are rationed in)

Complex explanation of the price mechanism (excess demand)

As buyers increase the price from P₁ to Pₑ, a signal is sent to suppliers that the benefit of selling has increased

As the benefit has affected sellers, they have an incentive to increase supply (A to C) (extension in supply)

As prices rise, buyers unwilling/unable to pay are rationed out of the market (B to C) (contraction of demand)