Cost Accounting Exam 2

1/51

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

52 Terms

Budgeted sales for the first quarter for Hupp Company, a retailer, are as follows:

Budgeted Sales (Units)

January: 175,000

February: 200,000

March: 240,000

The company likes to maintain an inventory equal to 15 percent of next month’s budgeted

sales.

Budgeted purchases in units for February would be:

a. 200,000 units

b. 206,000 units

c. 230,000 units

d. 236,000 units

e. 176,000 units

B.

Projected sales for Taylor, Inc., for next year and beginning and ending inventory data are as

follows:

Taylor’s budgeted sales would be:

a. $490,000

b. $500,000

c. $485,000

d. $495,000

e. None of the above

A.

Projected sales for Taylor, Inc., for next year and beginning and ending inventory data are as

follows:

Sales 10,000 units

Beginning inventory 300 units

Desired ending inventory 400 units

The selling price is $49 per unit.

According to Taylor’s production budget, how many units should be produced?

a. 9,600

b. 9,900

c. 10,100

d. 10,400

e. None of the above

C.

The number of units sold and the number of units produced may differ because of a change in:

a. finished goods inventory levels

b. overhead charges

c. direct material inventory levels

d. sales returns and allowances

e. work-in-process inventory levels

A.

Rizzo Corporation is a distributor of auto parts. Rizzo Corporation had 17,000 units of brake calipers on hand at the end of its calendar Year 5. The company had a policy of maintaining 15 percent of the current year's sales as ending inventory. During Year 6, Rizzo expects to sell 210,000 units of calipers. How many units should Rizzo budget to purchase in Year 6?

A. 196,150 units

B. 210,000 units

C. 224,500 units

D. 194,700 units

E. 241,500 units

C.

Selected data for Anthony Company reveals the following:

Standard price of materials- $4.00 per pound

Actual price of materials- $4.50 per pound

Standard quantity (SQ) of materials allowed- 10,000pounds

Materials Efficiency Variance- $2,300 unfavorable

The actual quantity of materials used is?

a. 10,000 pounds

b. 9,400 pounds

c. 8,378 pounds (rounded)

d. 13,000 pounds

e. 10,575 pounds

E.

The McDermott Furniture Company has established standard costs for the cabinet department, in which one size of a singe four-drawer style of dresser is produced. The standard costs are used in evaluating actual performance. The standard cost of producing one of these dressers are shown below:

STANDARD-COST CARD

________________________________________________

Dresser Style AAA

Materials: Lumber - 50 board feet @ $.20: $10.00

Direct Labor: 3 hours @ $6.00: 18.00

Overhead Costs:

Variable - 3 hours @ $1.00: 3.00

Fixed - 3 hours @ $.50: 1.50

Total per dresser: $32.50

The costs of operation to produce 400 of these dressers during January are stated below (there

were no initial inventories):

Materials purchased: 25,000 board feet @ $.21: $5,250.00

Materials used: 19,000 board feet

Direct Labor: 1,100 hours @ $5.90: $6,490.00

Overhead:

Variable $1,300.00

Fixed $710.00

The flexible budget for this department at the monthly volume level use to set the fix the fixed-overhead rate called for 1,400 direct-labor hours of operation. At this level, the variable overhead cost was budgeted at $1,400, and the fixed overhead cost at $700. Calculate the materials price and efficiency variances:

a. Price variance: $250 F; Efficiency variance: $200 F

b. Price variance: $250 U; Efficiency variance: $200 U

c. Price variance: $250 U; Efficiency variance: $200 F

d. Price variance: $250 F; Efficiency variance: $200 U

e. None of the above

C.

The McDermott Furniture Company has established standard costs for the cabinet department, in which one size of a singe four-drawer style of dresser is produced. The standard costs are used in evaluating actual performance. The standard cost of producing one of these dressers are shown below:

STANDARD-COST CARD

________________________________________________

Dresser Style AAA

Materials: Lumber - 50 board feet @ $.20: $10.00

Direct Labor: 3 hours @ $6.00: 18.00

Overhead Costs:

Variable - 3 hours @ $1.00: 3.00

Fixed - 3 hours @ $.50: 1.50

Total per dresser: $32.50

The costs of operation to produce 400 of these dressers during January are stated below (there

were no initial inventories):

Materials purchased: 25,000 board feet @ $.21: $5,250.00

Materials used: 19,000 board feet

Direct Labor: 1,100 hours @ $5.90: $6,490.00

Overhead:

Variable $1,300.00

Fixed $710.00

The flexible budget for this department at the monthly volume level use to set the fix the fixed-overhead rate called for 1,400 direct-labor hours of operation. At this level, the variable overhead cost was budgeted at $1,400, and the fixed overhead cost at $700. Calculate the labor price and efficiency variances:

a. Price variance: $110 F; Efficiency variance: $600 F

b. Price variance: $110 U; Efficiency variance: $600 U

c. Price variance: $110 U; Efficiency variance: $600 F

d. Price variance: $110 F; Efficiency variance: $600 U

e. None of the above

A.

The McDermott Furniture Company has established standard costs for the cabinet department, in which one size of a singe four-drawer style of dresser is produced. The standard costs are used in evaluating actual performance. The standard cost of producing one of these dressers are shown below:

STANDARD-COST CARD

________________________________________________

Dresser Style AAA

Materials: Lumber - 50 board feet @ $.20: $10.00

Direct Labor: 3 hours @ $6.00: 18.00

Overhead Costs:

Variable - 3 hours @ $1.00: 3.00

Fixed - 3 hours @ $.50: 1.50

Total per dresser: $32.50

The costs of operation to produce 400 of these dressers during January are stated below (there

were no initial inventories):

Materials purchased: 25,000 board feet @ $.21: $5,250.00

Materials used: 19,000 board feet

Direct Labor: 1,100 hours @ $5.90: $6,490.00

Overhead:

Variable $1,300.00

Fixed $710.00

The flexible budget for this department at the monthly volume level use to set the fix the fixed-overhead rate called for 1,400 direct-labor hours of operation. At this level, the variable overhead cost was budgeted at $1,400, and the fixed overhead cost at $700. Calculate the variable overhead spending:

a. $200 F

b. $200 U

c. $100 F

d. $100 U

e. None of the above

B.

The McDermott Furniture Company has established standard costs for the cabinet department, in which one size of a singe four-drawer style of dresser is produced. The standard costs are used in evaluating actual performance. The standard cost of producing one of these dressers are shown below:

STANDARD-COST CARD

________________________________________________

Dresser Style AAA

Materials: Lumber - 50 board feet @ $.20: $10.00

Direct Labor: 3 hours @ $6.00: 18.00

Overhead Costs:

Variable - 3 hours @ $1.00: 3.00

Fixed - 3 hours @ $.50: 1.50

Total per dresser: $32.50

The costs of operation to produce 400 of these dressers during January are stated below (there

were no initial inventories):

Materials purchased: 25,000 board feet @ $.21: $5,250.00

Materials used: 19,000 board feet

Direct Labor: 1,100 hours @ $5.90: $6,490.00

Overhead:

Variable $1,300.00

Fixed $710.00

The flexible budget for this department at the monthly volume level use to set the fix the fixed-overhead rate called for 1,400 direct-labor hours of operation. At this level, the variable overhead cost was budgeted at $1,400, and the fixed overhead cost at $700. Calculate the variable overhead efficiency variance:

a. $100 F

b. $100 U

c. $200 F

d. $200 U

e. None of the above

A.

The McDermott Furniture Company has established standard costs for the cabinet department, in which one size of a singe four-drawer style of dresser is produced. The standard costs are used in evaluating actual performance. The standard cost of producing one of these dressers are shown below:

STANDARD-COST CARD

________________________________________________

Dresser Style AAA

Materials: Lumber - 50 board feet @ $.20: $10.00

Direct Labor: 3 hours @ $6.00: 18.00

Overhead Costs:

Variable - 3 hours @ $1.00: 3.00

Fixed - 3 hours @ $.50: 1.50

Total per dresser: $32.50

The costs of operation to produce 400 of these dressers during January are stated below (there

were no initial inventories):

Materials purchased: 25,000 board feet @ $.21: $5,250.00

Materials used: 19,000 board feet

Direct Labor: 1,100 hours @ $5.90: $6,490.00

Overhead:

Variable $1,300.00

Fixed $710.00

The flexible budget for this department at the monthly volume level use to set the fix the fixed-overhead rate called for 1,400 direct-labor hours of operation. At this level, the variable overhead cost was budgeted at $1,400, and the fixed overhead cost at $700. Calculate the fixed overhead budget:

a. $600

b. $700

c. $710

d. $800

e. None of the above

B.

The McDermott Furniture Company has established standard costs for the cabinet department, in which one size of a singe four-drawer style of dresser is produced. The standard costs are used in evaluating actual performance. The standard cost of producing one of these dressers are shown below:

STANDARD-COST CARD

________________________________________________

Dresser Style AAA

Materials: Lumber - 50 board feet @ $.20: $10.00

Direct Labor: 3 hours @ $6.00: 18.00

Overhead Costs:

Variable - 3 hours @ $1.00: 3.00

Fixed - 3 hours @ $.50: 1.50

Total per dresser: $32.50

The costs of operation to produce 400 of these dressers during January are stated below (there

were no initial inventories):

Materials purchased: 25,000 board feet @ $.21: $5,250.00

Materials used: 19,000 board feet

Direct Labor: 1,100 hours @ $5.90: $6,490.00

Overhead:

Variable $1,300.00

Fixed $710.00

The flexible budget for this department at the monthly volume level use to set the fix the fixed-overhead rate called for 1,400 direct-labor hours of operation. At this level, the variable overhead cost was budgeted at $1,400, and the fixed overhead cost at $700. Calculate the fixed overhead volume variance:

a. $100 F

b. $100 U

c. $110 F

d. $110 U

e. None of the above

B.

Which of the following budgets is geared to assumed conditions?

A. The Master Budget.

B. The Flexible budget.

C. Both the Master and the Flexible Budget.

D. Neither the Master nor the Flexible Budget

E. None of the above.

A.

Wilgers Company has budgeted sales volume of 30,000 units and budgeted production of 27,000 units, while 5,000 units are in beginning finished goods inventory. How many units are targeted for ending finished goods inventory?

a. 2,000 units

b. 3,000 units

c. 8,000 units

d. 32,000 units

A.

An unfavorable price variance for direct materials might indicate:

a. that the purchasing manager purchased in smaller quantities than expected

b. congestion due to scheduling problems

c. that the purchasing manager skillfully negotiated a better purchase price

d. that the market had an unexpected oversupply of those materials

e. that too much materials were used

A.

Direct costing:

a. expenses administrative costs as cost of goods sold

b. treats variable manufacturing costs as a product cost

c. includes fixed manufacturing overhead as an inventoriable

(product) cost

d. is required for external reporting to shareholders

e. both b and c are correct

B.

Gabe’s Auto produces and sells an auto part for $30.00 per unit. In 20X5, 100,000 parts were produced and 75,000 units were sold. Other information for the year includes:

Direct materials $12.00 per unit

Direct manufacturing labor $ 2.25 per unit

Variable manufacturing overhead $ 3.75 per unit

Sales commissions $ 3.00 per part

Fixed manufacturing overhead: $375,000 per year

Administrative expenses, all fixed: $135,000 per year

What is the cost per unit and the value of the ending inventory using variable costing?

a. $21.75 per unit; $543,750 value

b. $18.00 per unit; $1,350,000 value

c. $18.00 per unit; $450,000 value

d. $24.75 per unit; $618,750 value

C.

Gabe’s Auto produces and sells an auto part for $30.00 per unit. In 20X5, 100,000 parts were produced and 75,000 units were sold. Other information for the year includes:

Direct materials $12.00 per unit

Direct manufacturing labor $ 2.25 per unit

Variable manufacturing overhead $ 3.75 per unit

Sales commissions $ 3.00 per part

Fixed manufacturing overhead: $375,000 per year

Administrative expenses, all fixed: $135,000 per year

What is the cost per unit and the value of the ending inventory using absorption costing?

a. $21.75 per unit; $543,750 value

b. $18.00 per unit; $1,350,000 value

c. $24.75 per unit; $618,750 value

d. $18.00 per unit; $450,000 value

D.

Gabe’s Auto produces and sells an auto part for $30.00 per unit. In 20X5, 100,000 parts were produced and 75,000 units were sold. Other information for the year includes:

Direct materials $12.00 per unit

Direct manufacturing labor $ 2.25 per unit

Variable manufacturing overhead $ 3.75 per unit

Sales commissions $ 3.00 per part

Fixed manufacturing overhead: $375,000 per year

Administrative expenses, all fixed: $135,000 per year

How much fixed manufactured overhead will be expensed this year under direct costing?

a. $281,250

b. $93,750

c. $135,000

d. $375,000

D.

Gabe’s Auto produces and sells an auto part for $30.00 per unit. In 20X5, 100,000 parts were produced and 75,000 units were sold. Other information for the year includes:

Direct materials $12.00 per unit

Direct manufacturing labor $ 2.25 per unit

Variable manufacturing overhead $ 3.75 per unit

Sales commissions $ 3.00 per part

Fixed manufacturing overhead: $375,000 per year

Administrative expenses, all fixed: $135,000 per year

How much fixed manufactured overhead will be expensed this year under absorption costing?

a. $375,000

b. $135,000

c. $281,250

d. $93,750

C.

Gabe’s Auto produces and sells an auto part for $30.00 per unit. In 20X5, 100,000 parts were produced and 75,000 units were sold. Other information for the year includes:

Direct materials $12.00 per unit

Direct manufacturing labor $ 2.25 per unit

Variable manufacturing overhead $ 3.75 per unit

Sales commissions $ 3.00 per part

Fixed manufacturing overhead: $375,000 per year

Administrative expenses, all fixed: $135,000 per year

Calculate whether Absorption costing income is higher or lower this period and by how much.

a. Lower by $93,750

b. Higher by $281,250

c. Higher by $93,750

d. Lower by $281,250

C.

The Woody Company manufactures slippers and sells them at $10 a pair. Variable manufacturing cost is $4.50 a pair, and allocated fixed manufacturing cost is $1.50 a pair. It has enough idle capacity available to accept a one-time- only special order of 20,000 pairs of slippers at $8 a pair. Woody will not incur any marketing costs as a result of the special order. What would the effect on operating Income be if the special order could be accepted without affecting normal sales?

a. $80,000 increase in operating income

b. $70,000 increase in operating income

c. $40,000 increase in operating income

d. $30,000 increase in operating income

B.

Mili Co. has five divisions. They plan to drop one division with the following information:

Sales $50,000

Variable Costs 30,000

Contribution Margin 20,000

Fixed Expenses 50,000

Income ($30,000)

All of the Fixed Expenses charged to this division are sunk. The effect of dropping the division on Mili's income would be:

a. Decrease of $20,000

b. Increase of $30,000

c. Decrease of $30,000

d. Increase of $20,000

A.

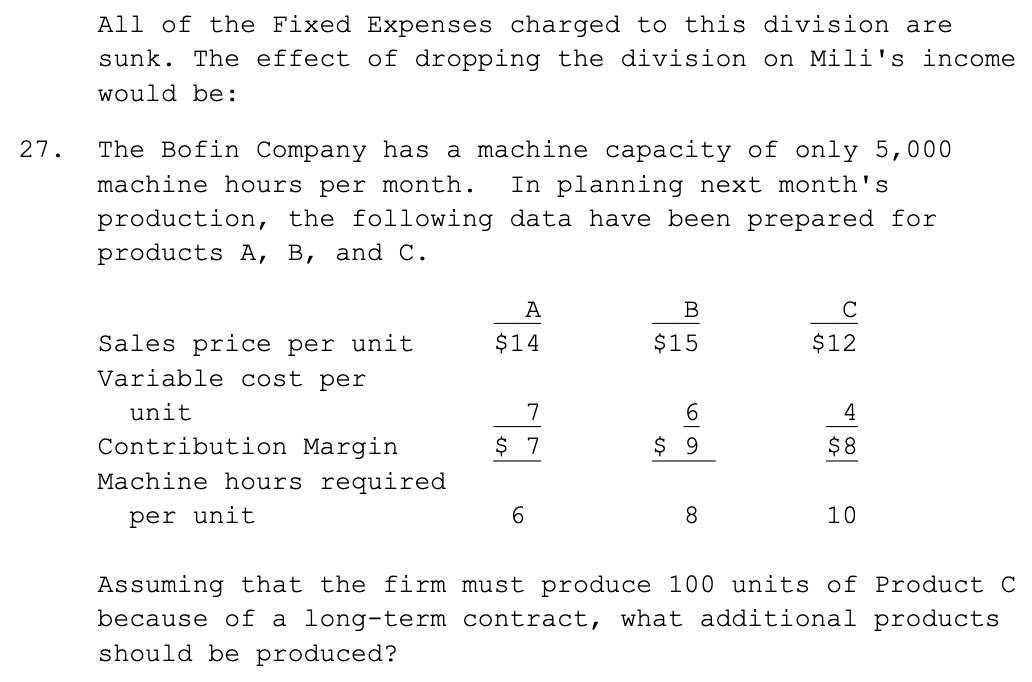

The Bofin Company has a machine capacity of only 5,000

machine hours per month. In planning next month's

production, the following data have been prepared for

products A, B, and C

(view image)

Assuming that the firm must produce 100 units of Product C because of a long-term contract, what additional products should be produced?

a. Produce as much of Product B as possible, as it has the highest total contribution margin per unit.

b. Produce as much of Product A as possible, as it has the highest contribution margin per machine hour.

c. Produce as much of Product C as possible, because it has a higher contribution margin than Product A.

d. Produce an equal amount of Product A and Product B to balance the machine load.

a. $4,000

b. $4,800

c. $5,125

d. $5,462

D.

Earl’s Hurricane Lamp Oil Company produces both A-1 Fancy and B Grade Oil. There are approximately $9,000 in joint costs that Earl may allocate using the sales value at splitoff or the net realizable value approach. At splitoff, A-1 sells for $20,000 while B grade sells for $40,000. After further processing costs of $10,000, $3,000 for B grade and $7,000 for A-1, both the products sell for $50,000. What is the difference in allocated costs for the A-1 product assuming applications of the net realizable value and the sales value at splitoff approach?

a. $300

b. $1,000

c. $1,300

d. $4,300

C.

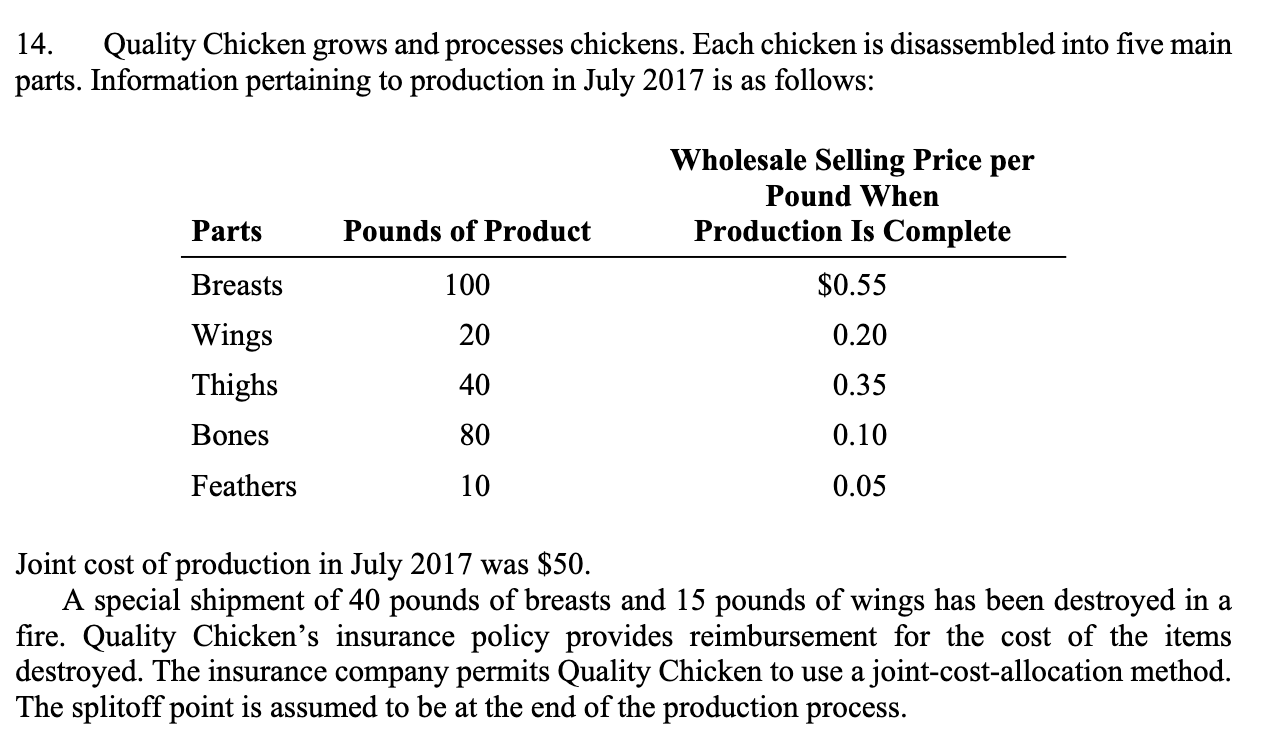

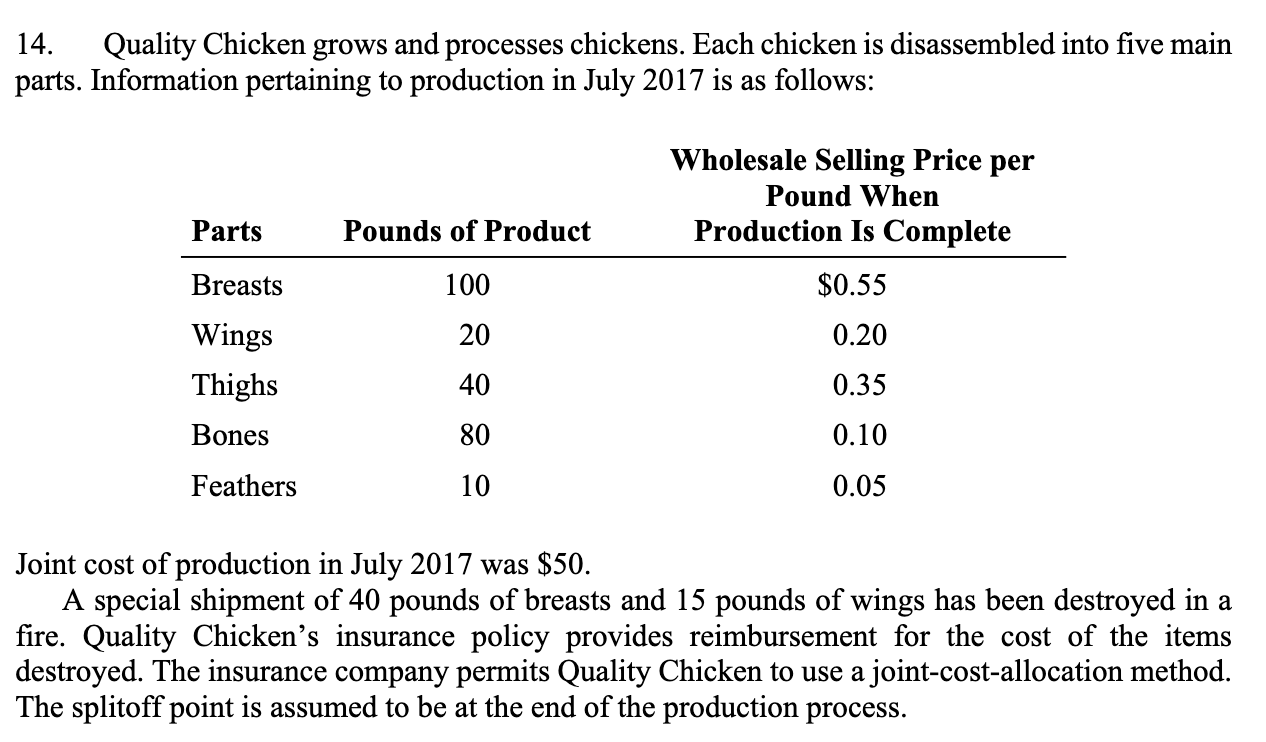

Compute the cost of the special shipment destroyed using the following the sales value at splitoff method:

a. $12.50

b. $15.34

c. $18.60

d. $20.00

B.

Compute the cost of the special shipment destroyed using the following the sales Physical-measure method (pounds of finished product):

a. $11.00

b. $15.34

c. $18.60

d. $20.00

A.

Nervana Soy Products (NSP) buys soybeans and processes them into other soy products. Each ton of soybeans that NSP purchases for $350 can be converted for an additional $210 into 650 pounds of soy meal and 100 gallons of soy oil. A pound of soy meal can be sold at splitoff for $1.32 and soy oil can be sold in bulk for $4.50 per gallon.

NSP can process the 650 pounds of soy meal into 750 pounds of soy cookies at an additional cost of $300. Each pound of soy cookies can be sold for $2.32 per pound. The 100 gallons of soy oil can be packaged at a cost of $230 and made into 400 quarts of Soyola. Each quart of Soyola can be sold for $1.15. Allocate the joint cost to the soy cookies and the Soyola using the sales value at splitoff method:

a. Soy meal: $350.00; Soy oil: $210.00

b. Soy meal: $367.34; Soy oil: $192.66

c. Soy meal: $400.00; Soy oil: $160.00

d. Soy meal: $300.00; Soy oil: $260.00

B.

Nervana Soy Products (NSP) buys soybeans and processes them into other soy products. Each ton of soybeans that NSP purchases for $350 can be converted for an additional $210 into 650 pounds of soy meal and 100 gallons of soy oil. A pound of soy meal can be sold at splitoff for $1.32 and soy oil can be sold in bulk for $4.50 per gallon.

NSP can process the 650 pounds of soy meal into 750 pounds of soy cookies at an additional cost of $300. Each pound of soy cookies can be sold for $2.32 per pound. The 100 gallons of soy oil can be packaged at a cost of $230 and made into 400 quarts of Soyola. Each quart of Soyola can be sold for $1.15. Allocate the joint cost to the soy cookies and the Soyola using the NRV method:

a. Soy cookies: $367.34; Soyola: $192.66

b. Soy cookies: $400.00; Soyola: $160.00

c. Soy cookies: $482.87; Soyola: $77.13

d. Soy cookies: $500.00; Soyola: $60.00

C.

Nervana Soy Products (NSP) buys soybeans and processes them into other soy products. Each ton of soybeans that NSP purchases for $350 can be converted for an additional $210 into 650 pounds of soy meal and 100 gallons of soy oil. A pound of soy meal can be sold at splitoff for $1.32 and soy oil can be sold in bulk for $4.50 per gallon.

NSP can process the 650 pounds of soy meal into 750 pounds of soy cookies at an additional cost of $300. Each pound of soy cookies can be sold for $2.32 per pound. The 100 gallons of soy oil can be packaged at a cost of $230 and made into 400 quarts of Soyola. Each quart of Soyola can be sold for $1.15. Should NSP have processed each of the products further? What effect does the allocation method have on this decision?

a. Process both; yes, the allocation method changes the profit outcome significantly.

b. Process neither; no, the allocation method is irrelevant.

c. Process soy oil only; yes, the allocation method is critical for accurate decision-making.

d. Process soy meal only; no, the allocation method is irrelevant to this decision.

D.

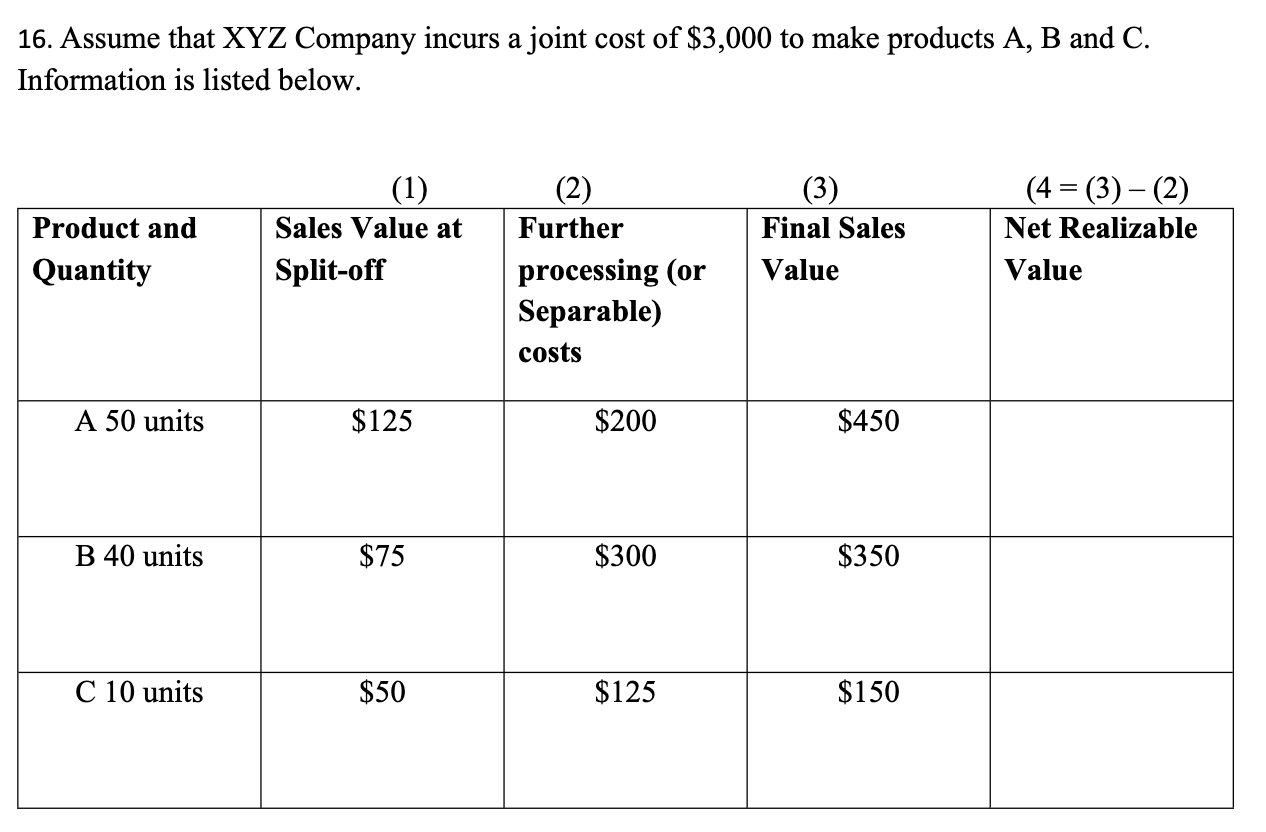

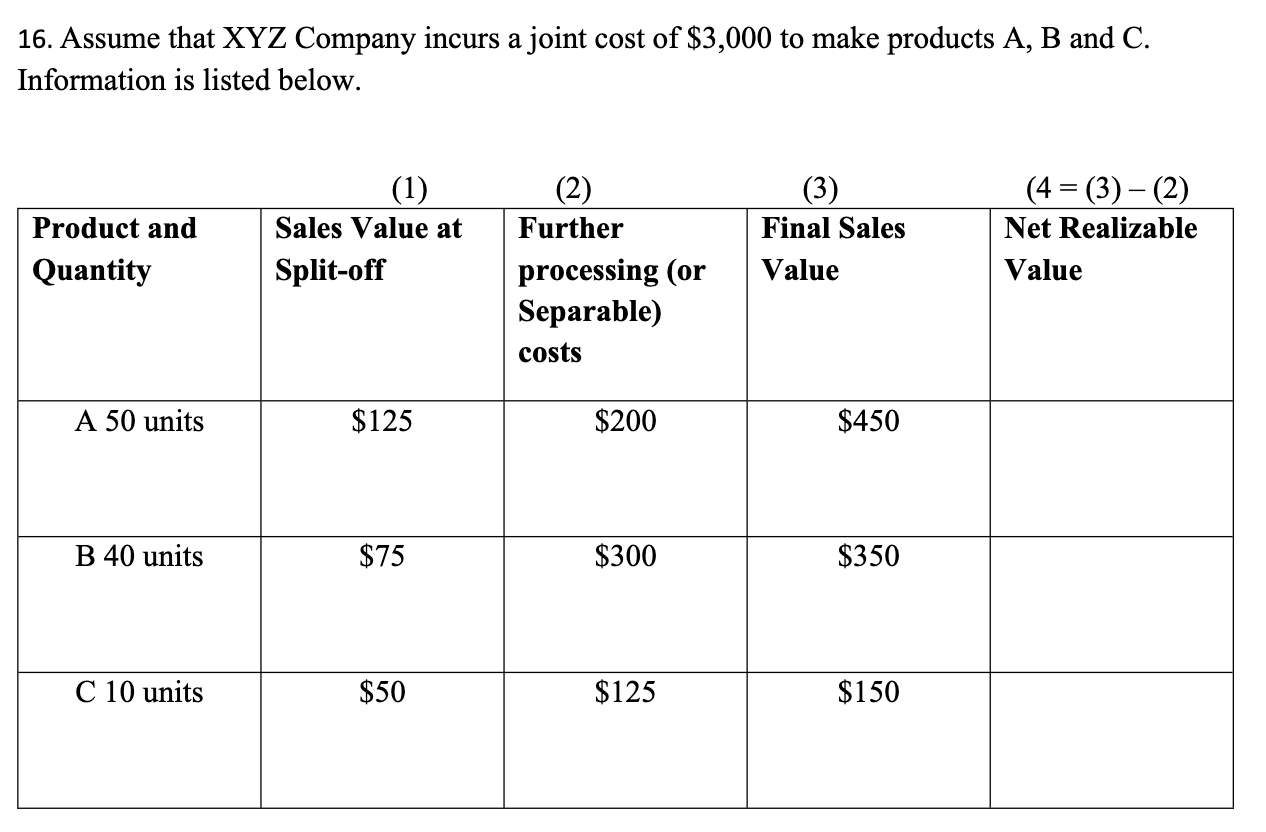

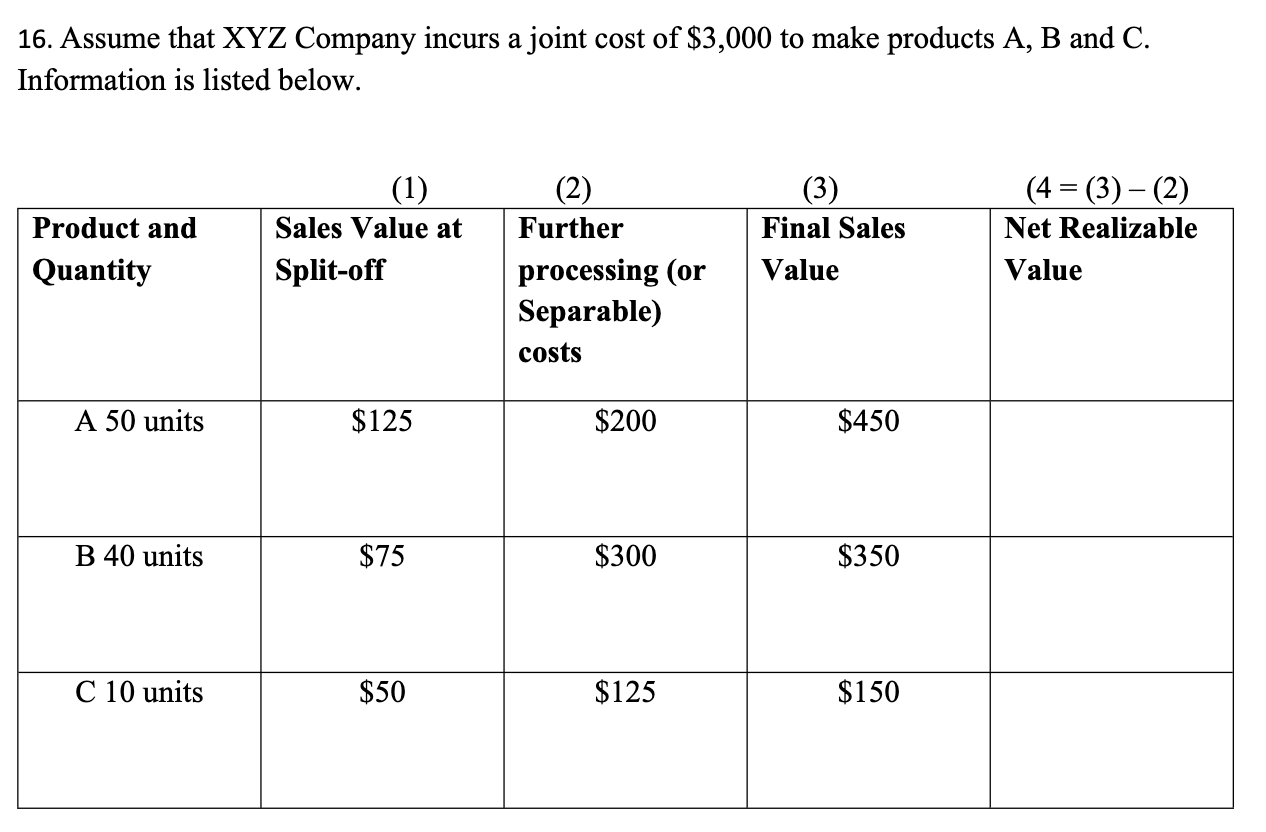

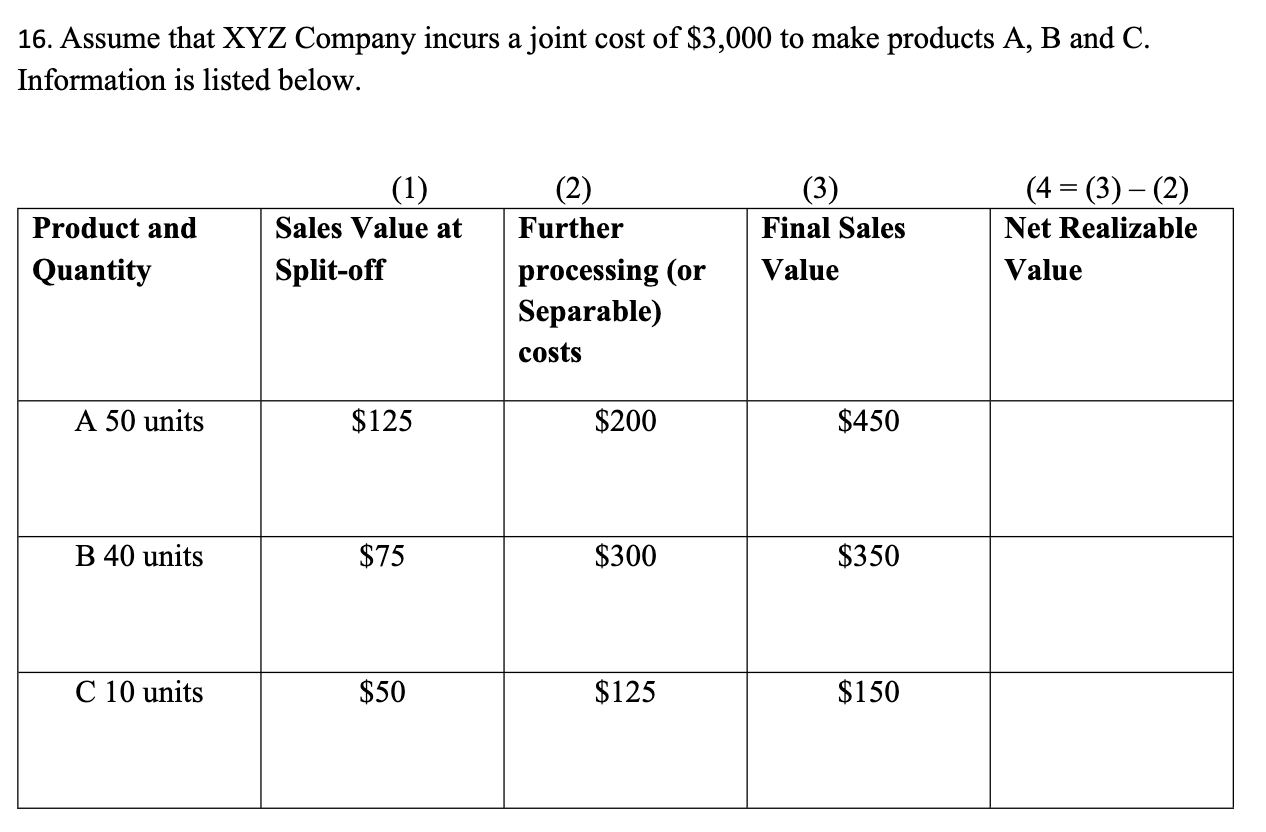

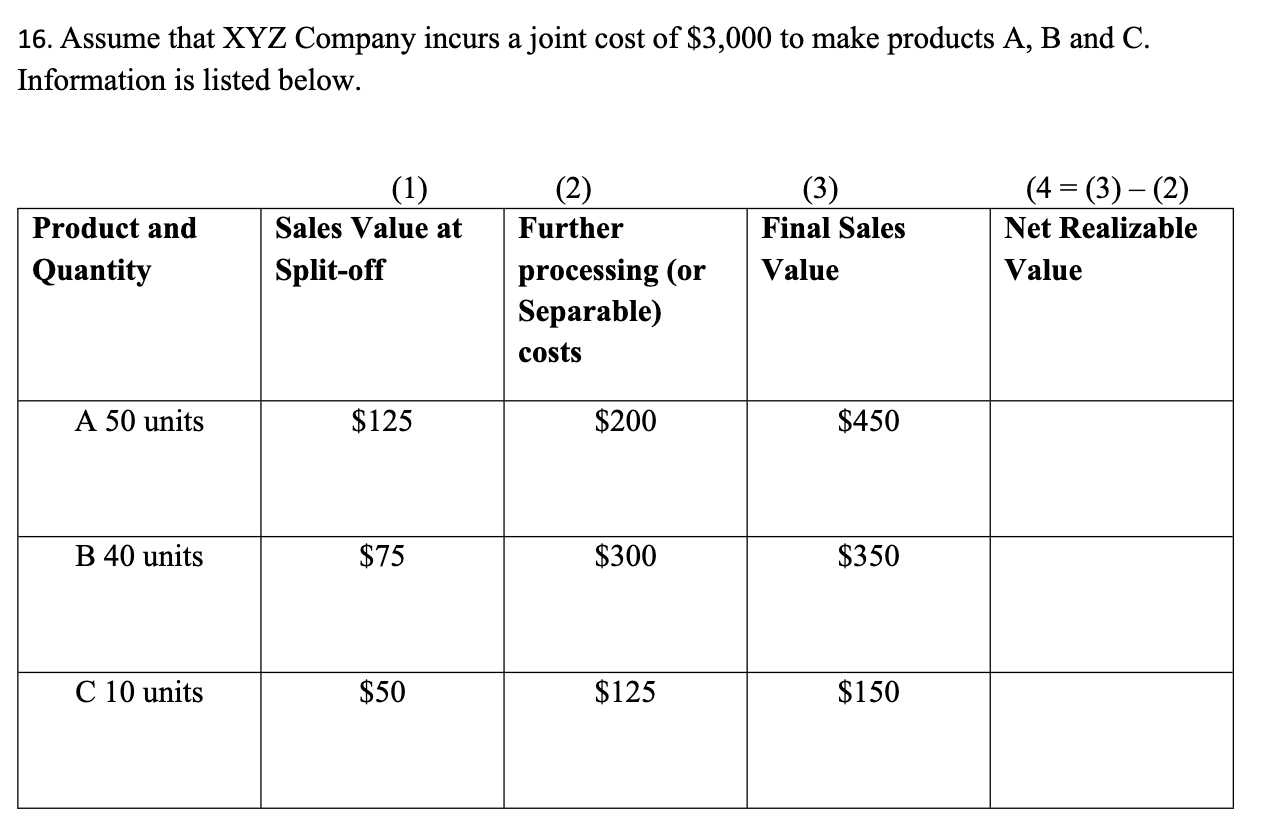

Allocate the joint costs using the Physical Volumes method.

a. Product A: $1,200; Product B: $1,500; Product C: $300

b. Product A: $1,500; Product B: $300; Product C: $1,200

c. Product A: $1,500; Product B: $1,200; Product C: $300

d. Product A: $1,000; Product B: $1,000; Product C: $1,000

C.

Allocate the joint costs using the Sales Value at Split off method.

a. Product A: $1,500; Product B: $600; Product C: $900

b. Product A: $1,500; Product B: $900; Product C: $600

c. Product A: $1,200; Product B: $900; Product C: $900

d. Product A: $900; Product B: $1,500; Product C: $600

B.

Allocate the joint costs using the Net Realizable Value method.

a. Product A: $2,307.69; Product B: $461.54; Product C: $230.77

b. Product A: $1,500.00; Product B: $900.00; Product C: $600.00

c. Product A: $2,000.00; Product B: $700.00; Product C: $300.00

d. Product A: $1,875.00; Product B: $1,125.00; Product C: $0.00

A.

Assume that C is a By-product. Allocate the Joint costs to the main product using method 1 from the book (the only method you are responsible for.)

a. Product A: $1,500; Product B: $1,200; Product C: $300

b. Product A: $1,875; Product B: $1,125; Product C: $0

c. Product A: $2,000; Product B: $1,000; Product C: $0

d. Product A: $1,600; Product B: $1,400; Product C: $0

B.

Assume XYZ sells all products after further processing. Are they maximizing profits?

a. Yes, because the total final sales value for all products is higher than the joint costs.

b. No, because Product A generates a negative contribution margin after further processing.

c. No, because Products B and C incur incremental losses when processed further, and should instead be sold at the split-off point.

d. Yes, because they are adding value to all products by processing them further.

C.

McDonald Industries' sales budget shows quarterly sales for the next year asfollows: Quarter1, 15,000; Quarter2, 13,000; Quarter3, 17,000; Quarter4, 19,000. Company policy is to have a targetfinished-goods inventory at the end of each quarter equal to 25 % of the nextquarter's sales. What would be the budgeted production for the second quarter of nextyear?

A. 17,000 units

B. 14,000 units

C. 17,250 units

D. 10,750 units

B.

Elmhurst Corporation is considering changes to its responsibility accounting system. Which of the following statements is/are correct for a responsibility accounting system?

In a cost center, managers are responsible for controlling costs but not revenue.

The idea behind responsibility accounting is that a manager should be held responsible for those items that the manager can control to a significant extent.

To be effective, a good responsibility accounting system must help managers to plan and to control.

Costs that are allocated to a responsibility center are normally controllable by the responsibility center manager.

A. II and III only are correct

B. I, II and IV are correct

C. I and II only are correct

D. I, II, and III are correct

D.

Mary Jacobs, the controller of the Jenks Company is working on Jenks' cash budget for year 2. She has information on each of the following items:

Wages due to workers accrued as of December 31, year 1.

Limits on a line of credit that may be used to fund Jenks' operations in year 2.

The balance in accounts payable as of December 31, year 1, from credit purchases made in year 1.

Which of the items above should Jacobs take into account when building the cash budget for year 2?

A. I and II

B. II and III

C. I and III

D. I, II, and III

D.

All of the following statements regarding standards are accurate except:

A. Currently attainable standards take into account the level of training available to employees.

B. Standards allow management to budget at a per-unit level.

C. Participative standards usually take longer to implement than authoritative standards.

D. Ideal standards account for a minimal amount of normal spoilage.

D.

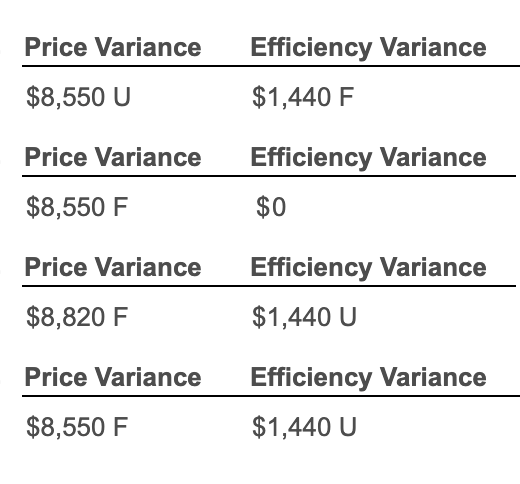

Absolute Manipulation Manufacturing's (AMM) standards anticipate that there will be 6 pounds of raw material used for every unit of finished goods produced. AMM began the month of May with 7,000 pounds of rawmaterial, purchased 28,500 pounds for $ 25,650 and ended the month with 6,100 pounds on hand. The company produced 4,700 units of finished goods. The company estimates standard costs at $ 1.20 per pound. The materials price and efficiency variances for the month of May were asfollows:(Abbreviations used: F= Favorable, U= Unfavorable.)

D.

Basix Inc. calculates direct manufacturing labor variances and has the following information:

Actual hours worked: 200

Standard hours allowed for actual output: 250

Actual rate per hour: $ 12

Standard rate per hour: $ 10

Given the information above, which of the following is correct regarding direct manufacturing labor variances?

A. The price variance is favorable, while the efficiency variance is unfavorable.

B. The price and efficiency variances are favorable.

C. The price and efficiency variances are unfavorable.

D. The price variance is unfavorable, while the efficiency variance is favorable.

D.

Each of the following statements is correct regarding overhead variances except

A. Actual overhead greater than applied overhead is unfavorable.

B. The efficiency overhead variance ignores the standard variable overhead rate.

C. Variable overhead rates are not a factor in the production-volume variance calculation.

D. Favorable spending and efficiency variances imply that the flexible budget variance must be favorable.

B.

Oslund Corporation produces a single product.

Standard Costs for One Unit:

Direct materials (3 pounds at $0.20 per pound) | $0.60 |

|---|---|

Direct manufacturing labor (5 hours at $14 per hour) | 70.00 |

Variable manufacturing overhead (5 hours at $4 per hour) | 20.00 |

Total | $90.60 |

During November Year 2, 3,900 units of Royal were produced.

Costs:

Material purchased (31,200 pounds at $0.90 per pound) | $28,080 |

|---|---|

Material used in production (in pounds) | 15,600 |

Direct manufacturing labor (19,700 hours at $8.25 per hour) | 162,525 |

Variable manufacturing overhead incurred | 80,770 |

What is the variable overhead efficiency variance for Royal for November Year 2?

A. $ 800 favorable.

B. $ 800 unfavorable.

C. $ 2,800 unfavorable.

D. $ 2,800 favorable.

B.

In comparing the absorption and variable cost methods, each of the following statements is true except:

A. Selling, general, and adminstrative (SG&A) fixed expenses are not included in inventory in either method.

B. Only the absorption method may be used for external financial reporting.

C. Variable costing charges fixed overhead costs to the period they are incurred.

D. When inventory increases over the period, variable net income will exceed absorption net income.

D.

Queen Sales, Inc. has just completed its first year of operations. The company has not had any sales to date.

Cost Incurred:

Direct materials | $45,000 |

|---|---|

Production labor | 35,000 |

Bookkeeper salary | 28,000 |

Factory utilities | 18,500 |

Office rent | 12,000 |

Factory supervisor salary | 9,600 |

Machine maintenance contract | 7,500 |

Under absorption costing, what is the inventory amount shown on the balance sheet at December 31, Year 1?

A. $ 155,600

B. $ 115,600

C. $ 98,500

D. $ 80,000

B.

Information

(SG&A = Selling, General, and Administrative)

Direct labor | $430,000 |

|---|---|

Direct materials | 250,000 |

Variable overhead | 208,000 |

Fixed overhead | 361,000 |

Variable (SG&A) expenses | 200,000 |

Fixed SG&A expenses | 193,000 |

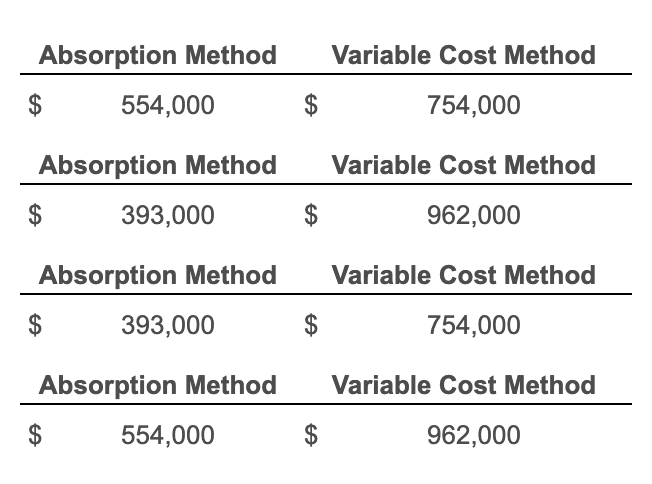

Year 3 period costs for Austin, under both the absorption and variable cost methods, will be

C.

Which of the following statements is not true regarding the use of variable and absorption costing for performance measurement?

A. The net income reported under the absorption method is less reliable for use in performance evaluations because the cost of the product includes fixed costs, which means the level of inventory affects net income.

B. The IRS allows either absorption or variable costing as long as the method is not changed from year to year, while U.S. Generally Accepted Accounting Principles (GAAP) only allows absorption costing.

C. Variable costing isolates contribution margins to aid in decision making.

D.The net income reported under the contribution income statement is more reliable for use in performance evaluations because the product cost does not include fixed costs.

B.

Which of the following is not a qualitative factor that Atlas Manufacturing should consider when deciding whether to buy or make a part used in manufacturing their product?

A. Variable cost per unit of the product.

B. Potential loss of trade secrets.

C. Quality of the outside producer's product.

D. Manufacturing deadlines and special orders.

A.

Lees Corp. is deciding whether to keep or drop a small segment of its business. Key information regarding the segment includes:

Contribution margin: | 35,000 |

|---|---|

Avoidable fixed costs: | 30,000 |

Unavoidable fixed costs: | 25,000 |

Given the information above, Lees should:

A. Keep the segment because the contribution margin exceeds avoidable fixed costs.

B. Drop the segment because the contribution margin is less than total fixed costs.

C. Drop the segment because avoidable fixed costs exceed unavoidable fixed costs.

D. Keep the segment because the contribution margin exceeds unavoidable fixed costs.

A.

Ace Cleaning Service is considering expanding into one or more new market areas. Which costs are relevant to Ace's decision on whether to expand?

A.

Sunk Costs | Variable Costs | Opportunity Costs |

|---|---|---|

Yes | No | Yes |

B.

Sunk Costs | Variable Costs | Opportunity Costs |

|---|---|---|

No | Yes | Yes |

Your answer is correct.

C.

Sunk Costs | Variable Costs | Opportunity Costs |

|---|---|---|

Yes | Yes | Yes |

D.

Sunk Costs | Variable Costs | Opportunity Costs |

|---|---|---|

No | Yes | No |

B.

Austin Corporation has two products, Vitals and Hauls.

Volume Information:

| Volume |

|---|---|

Product Vitals | 15,000 gallons |

Product Hauls | 10,000 gallons |

Total | 25,000 gallons |

The joint cost to produce the two products is $ 140,000. What portion of the joint cost will each product be allocated if the allocation is performed by volume? (Round any weighting values to six decimal places, X.XXXXXX.)

A. $ 125,000 and $0

B. $ 84,000 and $ 56,000

C. $ 56,000 and $ 84,000

D. $ 130,000 and $ 130,000

B.

Easton Company produces jointproducts, TimK and DannyD, each of which incurs separable production costs after the splitoff point. Information concerning a batch produced at a $ 250,000 joint cost before splitoff follows:

Information:

Product | Separable Costs | Sales Value |

|---|---|---|

TimK | $7,000 | $61,000 |

DannyD | 19,000 | 25,000 |

Total | $26,000 | $86,000 |

What is the joint cost assigned to TimK if costs are assigned using relative net realizable value?

A. $ 225,000

B. $ 250,000

C. $ 60,000

D. $ 25,000

A.