predicted economics paper 1

1/14

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

15 Terms

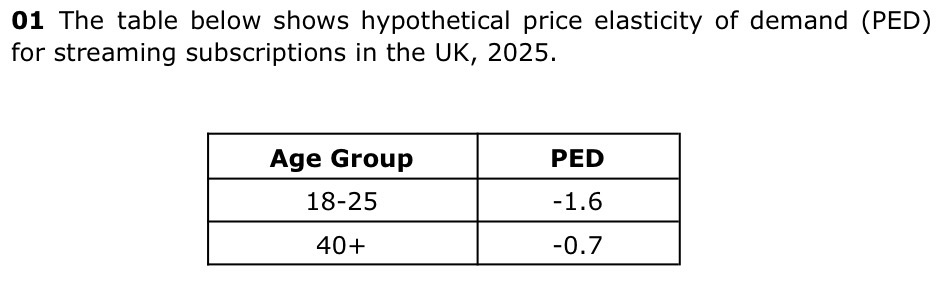

Explain one likely reason for the difference in PED between these age groups (4)

PED: measures the responsiveness of quantity demanded to a change in price

The demand for streaming subscriptions among 18-25 year olds is more price elastic (-1.6) because younger consumers tend to have greater access to substitutes such as free platforms like YT or social media entertainment such as TikTok

This means that if the price of a subscription rises, they can easily switch to alternative forms of entertainment → leading to a larger % fall in Qd

In contrast, older consumers (40+) have more inelastic demand (-0.7) as they may be more brand loyal or less familiar alternative services, making them less responsive to price changes

Factors affecting PED

NASBIT

Necessity or luxury

Addiction and habit

availability of Substitutes

Brand loyalty

proportion of Income

Time

Factors affecting PES

TEASS

Time period

state of the Economy

Availability of substitutes

Spare capacity

Stockpiles and perishability

Explain one likely factor that influences the price elasticity of supply (PES) of streaming services compared to physical cinema tickets (4)

PES measures the responsiveness of quantity supplied to a change in price.

The supply of streaming services is likely to be more price elastic because content is distributed digitally, allowing firms like Netflix, which reaches 59.2% of UK homes, to scale up access almost instantly by increasing server or cloud capacity

This means producers can respond quickly to higher demand without significant additional cost

In contrast, the supply of cinema tickets is more price inelastic since the number of physical seats and showings is fixed in the short run, making it difficult for cinemas to increase output when prices rise

Draw a graph to show a firm switching its objective from profit maximisation to revenue maximisation

Pmax: MC=MR

Rmax: MR=0

(Showing equilibrium)

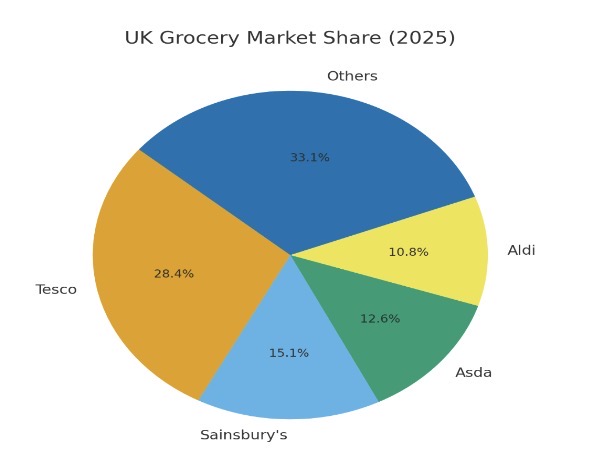

With reference, explain the market structure of the UK supermarket industry (4)

An oligopoly is a market structure in which a few large firms dominate total market sales

The UK supermarket industry fits this definition, as Tesco (28.4%), Sainsbury’s (15.1%), Asda (12.6%) and Aldi (10.8%) together control around 2/3 of the market

This high level of market concentration indicates that a small number of firms have significant power, creating high barriers to entry for new competitors due to economies of scale and brand loyalty

However, competition between these these major firms, particularly from discount retailers such as Aldi, still places pressure on prices and market behaviour

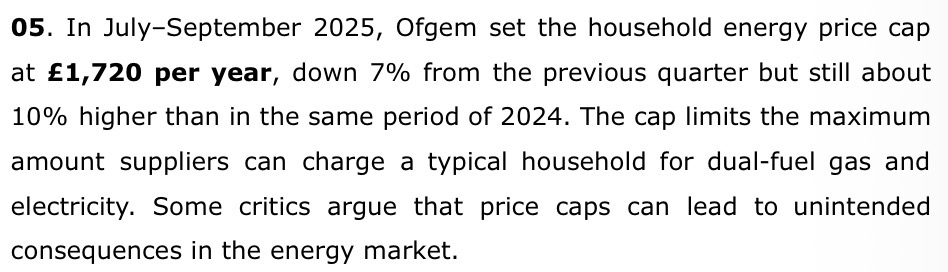

Explain one likely microeconomic reason for imposing this maximum price on energy bills (4)

A maximum price (also known as a price ceiling) is the highest price that firms are legally allowed to charge for a good or service

Ofgem’s 2025 energy price cap of £1,720 per year limits how much suppliers can charge households for gas and electricity

This policy aims to protect consumers from excessively high energy bills

By keeping prices below the free market equilibrium, the cap helps to make energy more affordable for lower-income and vulnerable households, ensuring they can maintain access to essential utilities

Brain drain

When highly skilled workers leave one country to work in another, reducing the domestic labour supply

Factors affecting elasticity of labour supply

(wtr: SUT): skills & qualifications (elastic in markers requiring low skills), unemployment levels (high = elastic), time (increase in wages = inelastic bc little time to train and apply)

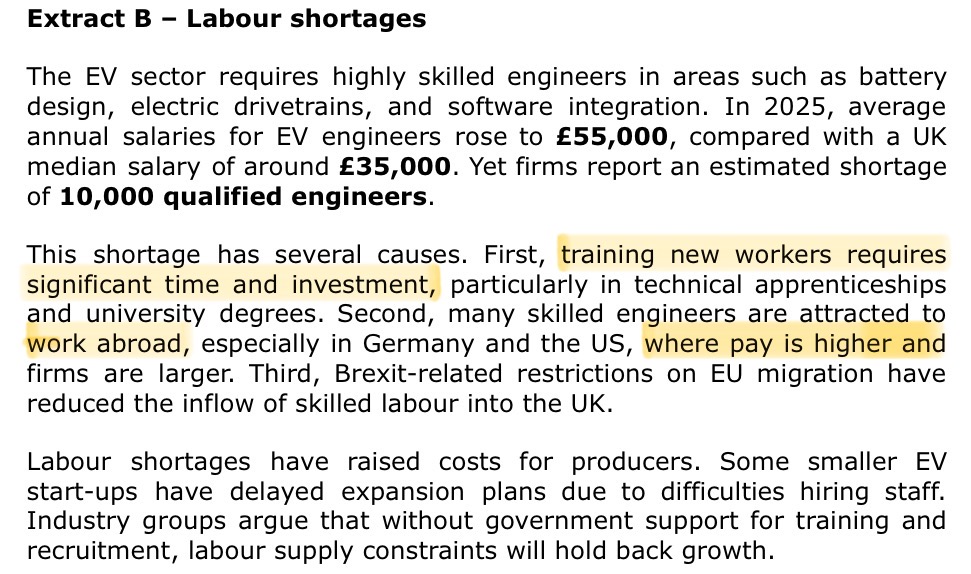

Examine two factors influencing the supply of labour in the EV sector (8)

Paragraph 1: factor

The first major influence is skills and training requirements

Production depends on electrical engineers, chemists and software specialists

Because these skills take years to develop, the SR supply of labour is inelastic, limiting how quickly firms can expand employment

Government STEM programmes and apprenticeships gradually shift the labour supply curve rightward, but capacity constraints remain in 2025

Paragraph 2: alternative factor

A second determinant is relative wages and working conditions

Higher pay in EV plants compared with traditional car factories attracts workers, increasing supply

However, if real wages fail to keep pace with inflation or working hours are antisocial, potential recruits may remain in other sectors

Geographical immobility is further reinforced in the EV sector because gigafactories tend to be concentrated in specific regions, meaning that even if skilled engineers exist elsewhere in the UK, their unwillingness or inability to relocate reduces the responsiveness of labour supply to rising wages.

Paragraph 3: conclusion

Overall, labour supply in the EV industry reflects a tension between high-skill scarcity and wage incentives

In the short run limited training pipelines dominate; in the long run better pay and government training can gradually ease shortages, making supply more elastic

Assess whether firms in the EV industry are likely to benefit from economies of scale (10) (use extract)

Knowledge

EOS are reductions in long-run average cost (LRAC) as output rises

Can arise from technical, managerial, purchasing, financial, marketing, and risk-bearing EOS

Shown by a downward-sloping LRAC curve up to the minimum efficient scale

Application

Battery industry mergers: firms combining operations to share R&D costs

Output rising 28% → spreading fixed costs over more units

Bulk buying inputs like lithium and nickel reduces unit input costs

Automation in gigafactories lowers unit labour costs

Real-world context: Tesla, CATL, BYD all scaling up to exploit EOS

Analysis

As firms expand, average costs fall, shifting LRAC downwards.

Sharing expensive R&D across merged firms lowers per-unit innovation costs → stronger competitiveness.

Purchasing EOS from bulk buying reduces costs, enabling lower consumer prices → higher market share.

Technical EOS: investment in high-capacity production lines raises efficiency

Can lead to increased profitability, or allow firms to cut prices → potential market dominance.

Diagram: LRAC falling with output; MES shown where lowest average cost reached

Evaluation

EOS may be offset by diseconomies of scale: communication problems, loss of managerial control.

Rising raw material prices (e.g. lithium) may erode bulk-buying advantages.

Large firms may suffer X-inefficiency due to lack of competition.

Mergers could attract regulatory scrutiny (competition authorities).

In fast-changing industries, smaller firms may be more flexible and innovative.

Long-term EOS depend on sustained demand growth in EV/battery markets

Discuss the likely concerns of competition authorities about the proposed merger in the battery industry (12)

→ concerns and evaluation of a merger

Knowledge:

Merger reduces the number of firms → increases market concentration

Competition authorities (CMA, EU commission) assess whether it leads to a substantial lessening of competition (SLC0

Higher prices, reduced innovation, consumer detriment

Concerns/ EV 1 (PRICE)

Reduced competition → higher prices for car makers → potentially higher EV prices for consumers

EoS (lower LRAC) could reduce costs → lower prices

Concerns/ EV 2 (INNOVATION)

May stifle innovation if less competitive pressure exists

Mergers may allow greater R&D investment → accelerating EV battery innovation

Concerns/ EV 3 (COMPETITION)

Barriers to entry rise → if merged firm controls R&D patents, raw material contracts or charging infrastructure

Global competition → Chinese and Korean firms (CATL, LG, BYD) already dominate → merger may be necessary to compete internationally

Concerns/ EV 4 (POTENTIAL PROBLEM, SOLUTION)

Collusion risk → merged firm may exploit market power

Authorities may approve with conditions → eg requiring deinvestments, limiting market share, or ensuring technology licensing

With a reference to extract D and figure 2, discuss possible government interventions to improve recycling rates of EV batteries (15)

Knowledge:

Market failure: under-provision of recycling → due to negative externalities (pollution, landfill, resource depletion) + positive externalities (conserves scarce metals, environmental benefits)

Government can intervene with policies to correct the market failure

Application/ analysis + EV

Subsidies (recycling plants)

Batteries contain lithium, cobalt, nickel → scarce and expensive raw materials

Help offset high fixed costs of building recycling plants

Lower costs of recycling → shifts supply curve right → higher recycling rates at lower costs

EV: cost to government: subsidies may require high spending → opportunity cost

Regulation (mandatory recycling quotas)

Ensures minimum recycling standards

EV: effectiveness: regulation may raise business costs and EV prices + difficult to monitor recycling

Taxes (disposal of batteries/ landfill)

Internalise negative externalities, discourage landfill dumping

EV: landfill taxes may discourage improper disposal

Deposit-refund schemes (to encourage consumer returns)

Incentivises consumers: return battery, receive rebate

Public information campaigns (to raise awareness)

EV: consumer response: campaigns may have limited impact without financial incentives

EV: global context: supply chains international; recycling policy needs international cooperation

EV: In the LR: innovation in battery design (eg solid-state, cobalt-free batteries) may reduce the need for recycling intervention

Evaluate the microeconomic effects of rising wages and labour shortages on firms in the hospitality industry or another industry of your choice

(Applies to healthcare, logistics, agriculture)

Ao1 Knowledge

Real wages: the purchasing power of wages (money wages adjusted for inflation

Labour shortages: Q of labour demanded exceeds the Q of labour supplied at the prevailing wage

Labour demand: derived demand, based on the demand of the goods/ services labour helps produce

Labour supply: number of workers willing and able to work at a given wage rate

Raising wages increase variable costs, shifting MC and AC upwards → reduces SNP

In a competitive market firms may be forced to absorb costs/ exit

Ao2 Application and real world examples

Firms face recruitment difficulties despite wage rises

→ hospitality industry examples

Post-Brexit staff shortages (fewer EU workers in UK)

Covid-19 impact → workers moving to different industries

Rising NMW

→ Firms like restaurants, hotels, bars are labour-intensive → more exposed to higher wage costs

Point 1: wages

Rising wages increases firms’ labour costs (major component of total costs in hospitality as industry is highly labour intensive with many low- and semi-skilled roles such as chefs, waiters and cleaners) → higher labour costs shift the SR supply curve to the left → firms supply fewer services at existing prices → (graph showing increase in costs and reduced SNP) → reduces the ability of firms to invest in training, marketing, or expansion + higher wages incentivise firms to change their staffing structure (reducing part-time/ low skilled roles and increase reliance on higher-skilled staff to maintain productivity) → creates chain reaction: fewer staff may reduce capacity, longer waiting times reduce customer satisfaction → lower service quality can lead to reduced demand, particularly in markets where consumers have alternative options

Evaluation 1:

Depends on PED for hospitality services → if demand is elastic → increase in prices leads to a disproportionately large fall in Qd → reducing revenue and forcing firms to cut costs further or reduce services. Where demand is inelastic (high-end restaurants or hotels in tourist-heavy locations) → firms may pass on higher wages to consumers without losing significant revenue → higher wages may improve staff retention, increase morale, attract highly skilled workers → increase productivity and service quality offsetting the cost pressures → therefore, while rising wages increase costs in the short term, they may encourage firms to adopt efficiency-enhancing measures and create longer-term benefit

Point 2: labour shortages

Reduces staff availability which directly limits output in restaurants, pubs, hotels → firms may experience longer waiting times, lower service quality and reduced consumer satisfaction → loss of repeat business and revenue + shortages can force existing staff to work longer hours → increasing stress and the risk of burnout → reduce productivity or increase staff turnover + firms unable to expand or operate at full capacity, persistent shortages can result in temporary closures or reduced opening hours → overall, labour shortages create a chain of negative effects that directly harm the operational efficiency, rev and rep of hospitality firms*

Evaluation 2:

Firms may take steps to mitigate the negative effects of labour shortages (may offer higher wages, signing bonuses, or non-wage incentives such as flexible working hours/ better working conditions) → attract and retain staff + investment in labour saving technologies (self-serving kiosks, online booking systems, automated checkins) → allows firms to maintain output and service quality with fewer employees + training/ upskilling existing staff can increase productivity → fewer workers needed to deliver the same or better level of services + some firms may adjust their business model (reducing menu options, offering fewer services or targeting higher-paying consumers to maintain profitability) → therefore, although labour shortages create significant challenges, proactive strategies can help firms adapt and even maintain efficiency and competitiveness

Conclusion:

In conclusion, rising wages + labour shortages create both immediate challenges and longer-term opportunities for hospitality firms. → in the ST, higher wages increase costs + reduce profit, while labour shortages reduce output/ service quality. However, in the LT → firms may respond by investing in productivity-enhancing technology, improving working conditions, raising staff motivation → offset some initial negative impacts. Overall depends on market structure, price elasticity of demand, firm size, flexibility of labour supply

To what extent can the UK energy supply industry be considered contestable? (25)

Knowledge:

Contestability: a contestable market is one where entry and exit are easy and costless, due to low or zero sunk costs

Key condition: the threat of entry disciplines incumbent firms, even if no entry occurs

Core characteristics of contestable markets: freedom of entry and exit, low sunk costs (advertising, r&d, set-up costs minimal), access to technology and inputs, absence of significant legal/regulatory barriers, potential for hit-and-run entry (enter to earn profits, exit quickly without losses)

Application

Ofgem price cap at £1,720 (july-sept 2025)

Market dominated by ‘big six’, though new entrants like Octopus energy

Barriers to entry: infrastructure, regulation, customer switching inertia

Analysis

Low contestability: high sunk costs (grid infrastructure), regulation, brand loyalty

Price cap limits firms’ ability to earn abnormal profits

New entrant suggest some degree of competition (Octopus, Ovo)

Evaluation

Government regulation creates artificial contestability (reduced regulation/ Ofgem licensing

Long-run: green energy transition may lower entry barriers (smaller renewable providers) → Octopus Energy: they built their model heavily around green energy and technology