accounting exam 2

1/24

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

25 Terms

FOB shipping point

(free on board) ownership of the goods passes to the buyer when the public carrier(truck) accepts the goods from the seller.

FOB destination

(free on board) Freight terms indicating that ownership of the goods remains with the seller until the goods reach the buyer.

Cost of Goods Sold (COGS) formula

Beg Inventory + Purchase - Ending inventory

First-in, first-out (FIFO)

inventory costing method that assumes that the costs of the earliest goods purchased are the first to be recognized as cost of goods sold.

Last-in, First-out (LIFO)

Inventory costing method that assumes the costs of the latest units purchased are the first to be allocated to cost of goods sold.

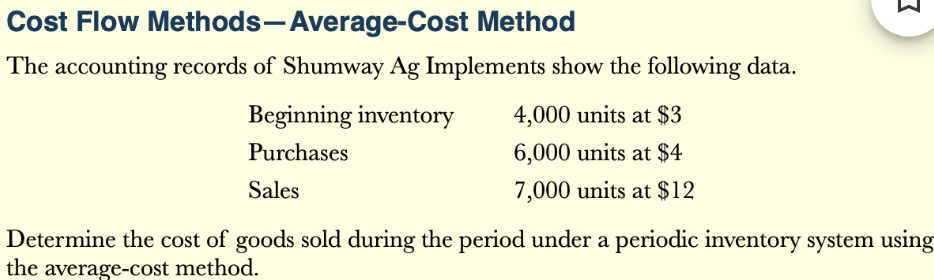

Average cost

Inventory costing method that uses the weighted-average unit cost to allocate to ending inventory and cost of goods sold the cost of goods available for sale.

COG Available for sale / total units available for sale = weighted-average unit cost

Average cost problem

SUM OF COST OF GOODS SOLD +COST OF ENDING INVENTORY =

COST OF GOODS AVAILABLE FOR SALE

if costs are rising fifo’s net income is

higher

if costs are rising lifo’s net income is

lower

if costs are falling fifo’s net income is

lower

if costs are falling lifo’s net income is

higher

In a period of inflation, FIFO produces a higher net income because

lower unit costs of the first units purchased are matched against revenue.

cheaper, older inventory for the COGS

When COGS is higher,

lower net income

Sales Discounts & Allowances journal entry step 1

Dr. Accounts Receivable

Cr. Sales Revenue

Sales Discounts & Allowances journal entry of returns

Dr. Sales Returns and Allowances

Cr. Accounts Receivable

Sales Discounts & Allowances journal entry payment

Dr. Cash

Dr. Sales Discounts

Cr. Accounts Receivable

RECORDING ESTIMATED UNCOLLECTIBLES

Dr. Bad Debt Expense

Cr. Allowance for Doubtful Accounts

WHEN WRITING OFF: when a specific account becomes uncollectible

Dr. Allowance for doubtful accounts

Cr. Accounts receivable

WHEN RECOVERING A WRITE OFF

Dr. Accounts receivable (increase it again, it exists again now)

Cr. Allowance for doubtful accounts (increase)

Dr. Cash

Cr. Accounts Receivable

JOURNAL ENTRY FOR FACTORING

sometimes companies sell A/R to get cash faster

Dr. Cash

Dr. Service charge expense

Cr. Accounts Receivable

JOURNAL ENTRY FOR CREDIT CARD SALES

Dr. Cash

Dr. Service Charge Expense

Cr. Sales Revenue

Balance Sheet presentation of receivables

Accounts Receivable

Less: Allowance for Doubtful accounts

= Net (Cash) Realizable value

Accounts Receivable Turnover formula

assess the liquidity of receivables; Net Credit Sales / Avg accounts receivable

Average collection period (days in receivable) formula

measures the average amount of time that a receivable is outstanding; 365 / A/R Turnover