Investment appraisal - Further aspects

1/33

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

Payback Period

The time a project takes to recover the money spent on it.

Liquidity Measure under payback period

Provides a measure of liquidity and risk based on expected cash flows.

Cash Flow Assumption under payback period

Payback period assumes cash flows occur evenly throughout the year.

Acceptance Criteria under payback period

If payback period is quicker than the company’s maximum return time, the project should be accepted.

Which projects to choose under payback period?

Choose the project with the quickest payback period when faced with mutually exclusive projects.

Payback Calculation (Constant Cash Flows)

Initial investment / Annual cash flow.

Payback Calculation (Uneven Cash Flows)

Add inflows and deduct from investment until the sum equals or exceeds the investment.

Advantages of Payback Period

Simple and intuitive metric that helps evaluate investment projects by calculating the time required to recover the initial investment, making it easy to understand and communicate.

Disadvantages of Payback Period

Ignores cash flows beyond the recovery period, fails to account for the time value of money, and can lead to biased decisions if used as the sole evaluation criterion, potentially prioritizing short-term gains over long-term value.

Accounting Rate of Return (ARR)

Average annual profit / Average value of investment.

Average Annual Profit

Calculated as net cash flow minus depreciation.

ARR Acceptance Criteria

If ARR is greater than targeted returns, accept the project.

Advantages of ARR

Simple and easy-to-calculate metric that helps evaluate investment projects based on their expected profitability, allowing for quick decision-making.

Disadvantages of ARR

Ignores the time value of money, fails to consider cash flows beyond the initial investment, and can lead to incorrect decisions if used as the sole evaluation criterion.

Discounted Payback

Cash flows are discounted to present value to consider time value of money.

Discounted Payback Period = Initial Investment / Annual Cash Flow (Discounted)

Taxable Profits

Net cash flow minus Tax depreciation.

Taxation Assumptions

Half corporation tax is paid in the current year and the other half in the next year.

Tax Depreciation

Reduces taxable profits and is treated as a cash saving.

Balancing Allowance

Ensures full fall in value is allowed. Happens when the amount you receive from the sale (or the market value) is less than the asset’s TWDV at the time of disposal.

Working Capital

Treated as an investment at the beginning of the project and released as inflow at the end.

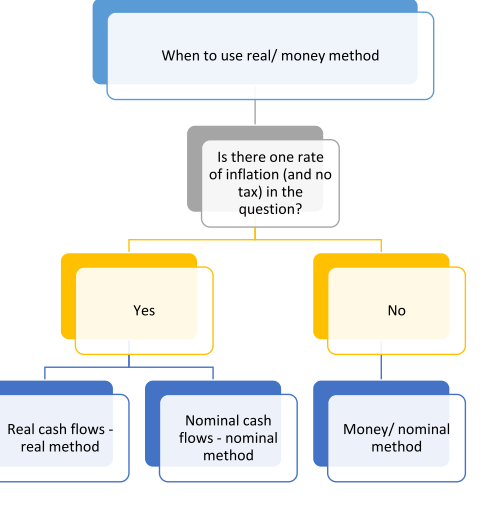

How to deal with inflation in Cash Flows

Cash flows can be adjusted for inflation or left in real terms.

Current Cash Flows

Cash flows not adjusted for inflation. AKA Real cash flows

Money Cash Flows

Cash flows adjusted for inflation

Real Rate of Return Formula

(1+r) = (1+m) / (1+i), where r is real rate, m is money cost, and i is inflation.

Specific Inflation Rate

Impacts each cash flow individually.

General Rate of Inflation

Impacts the overall required rate of return for investors.

Capital Asset Replacement Decisions

Decisions regarding the replacement of capital assets based on various factors.

Equivalent Annual Cost

Formula to compare machines with different lives by annualizing costs.

Optimum Replacement Cycle

The ideal time to replace machines based on maintenance costs and residual value.

Factors for Optimum Replacement Cycle

Capital cost

Operating costs

Resale value

Taxation

Inflation.

Average value of investment

(Initial investment + Residual value) / 2

Balancing charge

Occurs when the amount you receive from selling the asset (or its market value) is higher than its tax written down value (TWDV) at the time of disposal. Occur when excess depreciation is claimed.

Real rate of return

(1+r) = (1+𝑚) / (1+𝑖)

Indications on which type of method can be used in each scenarios