Exam Economics

1/263

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

264 Terms

What is microeconomics?

Microeconomics deals with the economic problem from an individual or “micro” point of view.

What does microeconomics focus on?

Individual consumers, firms, and how prices determine resource allocation in markets

What theory is at the heart of microeconomics?

The theory of demand and supply.

What is macroeconomics?

Macroeconomics deals with the economic problem from society’s point of view.

What does macroeconomics focus on?

Total economic activity, including total production, total employment, and the overall price level.

What are the two most important parts of macroeconomics?

The theory of economic growth and business cycles.

What is the economic problem?

Scarcity is the problem that there are not enough resources to satisfy the infinite number of wants.

What is opportunity cost?

Opportunity cost represents the real or economic cost of a decision.

How is opportunity cost best defined and how can it be measured?

Opportunity cost is the value of the next best choice you give up when making a decision.

It is measured by comparing the benefit of the option chosen with the benefit of the next best alternative given up.

What basic wants do individuals have?

Food, clothing, and shelter.

Distinguish between consumption goods and a capital good provide an example for each:

Consumption goods: Goods used directly to satisfy wants.

Example: Food or clothing.Capital goods: Goods used to produce other goods or services.

Example: Machinery or factory equipment.

What does the economic decision making refer to?

The process of making choices about how to use resources in order to achieve the best possible outcome.

What is the best way to allocate society’s scarce recources?

By comparing the benefits of using resources against the cost.

What is the principle of decreasing marginal benefit?

As you consume more of something, the extra benefit gained from each additional unit decreases.

What is marginal analysis in economics?

Comparing the marginal additional benefit and the marginal cost.

How do marginal benefit (MB) and marginal cost (MC) behave for additional hospitals?

Marginal benefit falls as more hospitals are built, while marginal cost stays the same.

Why would building a fourth hospital be inefficient in this example?

Its MB is $40m and MC is $50m, giving a net benefit of –$10m, so resources are wasted.

What is the calculation for a net benefit?

Net benefit = total benefits - total costs

What are marginal benefits and what are marginal costs?

Marginal benefits: The extra benefit gained from consuming or producing one more unit of a good or service.

Marginal costs: The extra cost incurred from producing or consuming one more unit of a good or service.

What is an economic model and the importance?

A simplified representation of economic reality showing relationships between economic variables.

Economic models simplify reality, helping economists analyze, predict, and understand economic behavior.

Why do economists use simplified models?

To identify cause and effect and accurately predict economic outcomes.

What is meant by rational self-interest?

The assumption that people are rational and respond to incentives by comparing costs and benefits.

Positive vs normative economics

Positive economic statements can be tested objectively, for example: "the unemployment rate would increase if the government stopped subsidizing the car industry"

Normative economic statements cannot be tested objectively since they involve a value judgement, for example: "the current unemployment rate too high"

What is an economic system?

It is the way in which a country's resources are allocated to deal with the economic problem.

What are the 3 basic questions that a economic system must answer concerning the economic problem?

what and how much to produce?

how to produce?

for whom to produce?

What is the price mechanism?

The price mechanism is the system where demand and supply determine commodity prices, with buyers and sellers deciding prices through their interactions.

What is the characteristics of a market economy?

A market economy is where resources are privately owned and owners make decisions based on their own self-interest.

What is a planned economy?

A planned economy is where resources are collectively owned and a central planning authority makes economic decisions.

What characterizes capitalist economies like Australia and the United States?

They are predominantly free market economies where most production decisions are determined by market forces.

What is a mixed economy?

A mixed economy combines elements of both market and planned economies.

What role do private markets and governments play in the economy?

Private markets efficiently allocate most goods and services, while governments provide key social goods like health, education, and law and order.

How do market and planned economies answer the three key economic questions?

In market economies, supply and demand decide what, how, and for whom to produce; in planned economies, a central authority makes these decisions, though past failures show coordination difficulties.

What are the key features of a competitive market?

Many buyers and sellers, little price variation, price takers, little or no product differentiation, no barriers to entry or exit, and no market power.

What are the key features of a non-competitive (imperfectly competitive) market?

Few buyers or sellers, large price variation, price setters, product differentiation, barriers to entry or exit, and firms have market power.

What does “price taker” mean in a competitive market?

Buyers and sellers must accept the market price and cannot influence it.

What does “price setter” mean in a non-competitive market?

Sellers or buyers can influence and set prices due to market power.

What is product differentiation?

When products are unique or have special features (USPs) that distinguish them from others.

What is market power?

The ability of a firm to influence the price or supply of a good or service.

What are barriers to entry/exit?

Factors which make it difficult for a new firm to enter the industry

What are examples of barriers to entry?

Brand loyalty - Consumers attached to existing products

Economies of scale - Existing firms benefit from lower average costs due to size

Patents - A legal barrier to copying a product

Vertical integration - If you have no access to suppliers, you cannot sell your product

Geographical barriers - No access to suitable location prevents new entry

Being the first mover - Facebook/Google gain strong position from being the 1st firm to dominate a market.

What is brand loyalty as a barrier to entry?

When consumers are attached to existing products, making it hard for new firms to attract customers.

What are economies of scale as a barrier to entry?

When large firms have lower average costs, making it difficult for smaller new firms to compete.

What is a patent as a barrier to entry?

A legal barrier that prevents others from copying a product.

What is vertical integration as a barrier to entry?

When a firm controls suppliers or distribution, limiting market access for new firms.

What does being a first mover mean?

Gaining an advantage by being the first firm to enter and dominate a market.

What are high exit costs?

Costs such as asset write-offs and closure costs that make exiting expensive.

How can regulation affect exit from a market?

Specialised equipment and high regulation can complicate and delay market exit.

How can tax breaks act as barriers to exit?

Firms may face penalties if they exit a market before receiving full tax benefits.

How can competitors benefit when firms exit a market?

Competitors may buy undervalued assets from exiting firms.

What is market power?

Market power is a firm’s ability to influence prices by affecting supply, demand, or both.

What market power do firms have in competitive markets?

In perfectly or near-perfectly competitive markets, firms have little market power and are price takers.

What is the law of demand?

As price rises, quantity demanded falls; as price falls, quantity demanded rises.

What are the two main reasons for the law of demand?

The substitute effect and the income effect.

What is the substitute effect?

When a price rises, consumers buy less of the good and switch to alternative (substitute) goods.

What is the income effect?

When a price rises, the good takes a larger share of income, reducing purchasing power and quantity demanded.

What is a demand curve?

A graph showing the relationship between price and quantity demanded, derived from a demand schedule.

What are the two types of changes in demand?

A change to the price of a good or service resulting in a change in the quantity demanded.

A change to demand caused by a non-price factor

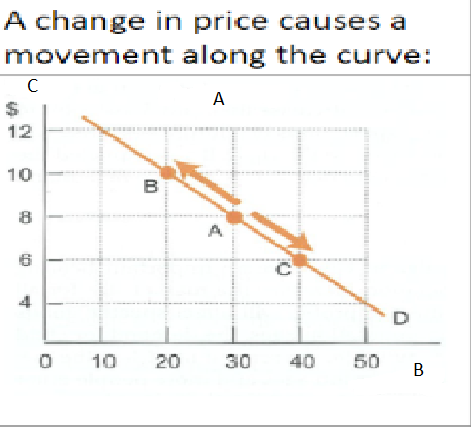

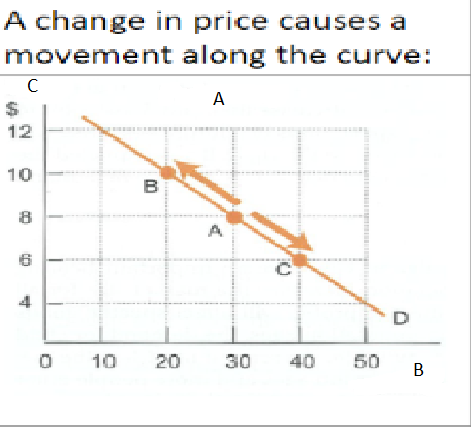

Label the demand diagram showing a change in price

A - Movements

B- Quantity

C - Price

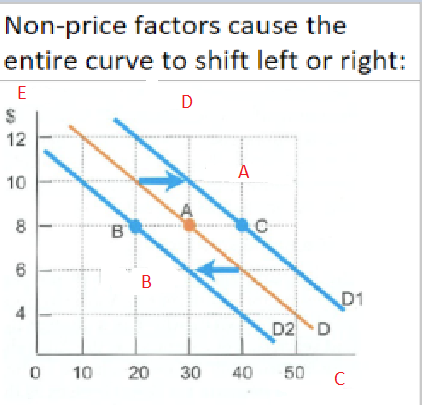

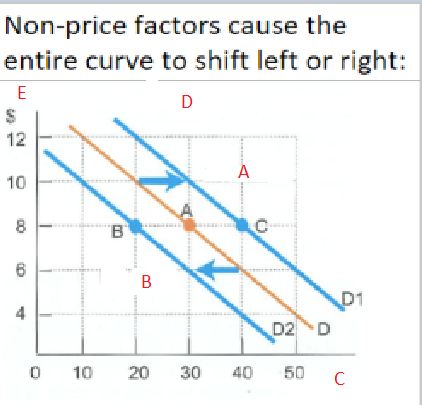

What causes the entire demand curve to shift left or right? And label the demand diagram.

A- Increase

B- Decrease

C- Quantity

D- Shifts

E- Price

What does ceteris paribus mean?

All other things being equal.

Why is ceteris paribus used in economics?

To isolate the effect of one variable while others remain constant.

How does ceteris paribus relate to demand?

It explains how price affects quantity demanded when non-price factors don’t change.

Give an example of ceteris paribus.

If price falls, quantity demanded rises, assuming other factors stay the same.

What happens if ceteris paribus does not hold?

Other variables may affect the outcome, making the relationship unclear.

Describe what is happening to this diagram:

As the price changes the curve stays where it is, but the quantity demanded increases or decreases as more or less people are willing and able to buy the good or service.

What do non-price factors affecting demand cause?

They shift the demand curve left or right, creating a new demand curve as quantity demanded changes at all prices.

How does income affect demand for normal goods?

As income rises, demand increases at all prices (shift right); as income falls, demand decreases (shift left).v

How does income affect demand for inferior goods?

As income increases, demand for inferior goods decreases; as income decreases, demand for inferior goods increases.

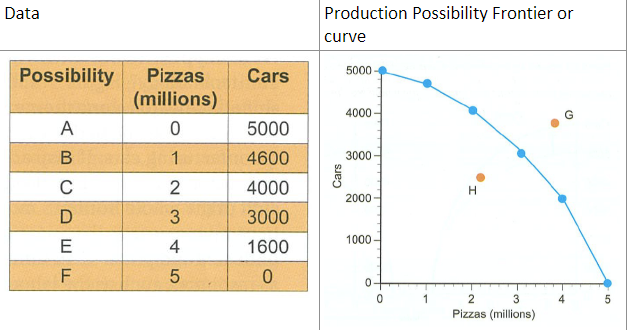

Describe the Production Possibility Frontier (PPF) model (include an example of a PPF model for 2 commodities)

The PPF shows the maximum output combinations of two goods using resources efficiently, illustrating scarcity and opportunity cost.

Explain the law of increasing opportunity cost

The law of increasing opportunity cost states that as more of one good is produced, the opportunity cost of producing it increases because resources are not equally suited to all uses.

What are price takers and price settlers?

Price takers: Firms that must accept the market price because they have no control over it (e.g. firms in perfect competition).

Price setters: Firms that can influence or set prices due to market power (e.g. monopolies, oligopolies).

What are 7 non price factors that affect demand, outline some examples?

Income – Higher income ↑ demand for normal goods (cars); ↑ income ↓ demand for inferior goods (home brands).

Population – More people = higher demand (housing, food).

Tastes & preferences – Trends increase demand (gym wear, electric cars).

Demographics – Age, culture changes demand (aging population → healthcare).

Substitutes prices – Xbox price ↑ → demand for PS5 ↑.

Complements prices – Game prices ↑ → demand for consoles ↓.

Expected future prices – Expected price rise → demand now ↑ (fuel, housing).

Define the term supply

The quantity of a good or service that producers are willing and able to sell at various prices over a given period of time.

State the law of supply

As price rises, quantity supplied increases; as price falls, quantity supplied decreases, ceteris paribus.

Outline how a supply curve is derived

By plotting the quantities producers are willing and able to sell at different prices, showing a positive relationship between price and quantity supplied.

Identify why the supply curve slopes ‘upwards’

Because higher prices provide greater profit incentives and are needed to cover higher marginal and opportunity costs of increased production.

Outline 5 non-price factors that affect supply, give examples of each

Costs of production – Higher wages or raw material costs reduce supply (electricity prices ↑ → factory output ↓).

Technology – Improved technology increases supply (automation in factories).

Number of producers – More firms increase supply (new cafés opening).

Government policies – Taxes reduce supply; subsidies increase supply (fuel excise, farming subsidies).

Natural factors – Weather or disasters affect supply (drought reduces crop supply).

Define equilibrium price

The price at which quantity demanded equals quantity supplied, so there is no surplus or shortage in the market.

How do we determine equilibrium price

At the point where the demand curve intersects the supply curve, meaning quantity demanded equals quantity supplied.

Define market surplus

When producers supply more of a good than consumers are willing to buy at a given price.

Outline how a demand curve is derived:

By plotting the quantities consumers are willing and able to buy at different prices, showing an inverse relationship between price and quantity demanded.

Outline why demand curve slopes 'downward'

Because of the substitution effect and income effect, meaning consumers buy more when prices fall and less when prices rise.

What model is used to explain a situation where the price has gone up and the quantity demanded has gone up?

Supply & Demand diagram

Outline how we determine the equilibrium price:

It is found at the point where quantity demanded equals quantity supplied, where the demand and supply curves meet.

Describe what is meant by ‘efficiency’

Using scarce resources in the best way to produce wants at the lowest cost.

Define “market efficiency”

When resources are used to maximize total surplus (benefits everyone)

What is consumer surplus?

The difference between what consumers are willing to pay and what they actually pay.

State how consumer surplus is measured?

total benefits - expenditure.

(Consumer willing to pay - the amount they actually pay.)

What does a rise in consumer surplus indicate?

Indicates increased consumer welfare, as consumers pay lower prices and gain more benefit.

Why is a demand curve referred to as a ‘willingness to pay’ curve?

It shows the maximum price consumers are willing to pay for each quantity of a good.

If you are willing to pay $12 for a pizza but actually pay $8, what is your consumer surplus?

$4

If you purchase a new puppy for $1500 and your consumer surplus was $2500, how much do you value the puppy?

$4,000

What is producer surplus?

The difference between what a producer is willing to receive (minimum supply price or cost of production) and what they actually receive in the market.

How is producer surplus measured?

total revenue (price x quantity sold) - cost.

If you sell a good for $100 and your cost of production was $60, what is your producer surplus.

$40

At what price and quantity is total surplus maximized/ point of economic efficiency?

At the market equilibrium, where demand equals supply.

That is the equilibrium price and equilibrium quantity.

Define “total surplus”

A measure of society’s net benefit from production and consumption after considering resource costs. (benefit - cost)

State how total surplus is calculated

There is 2 ways

Total surplus = Consumer surplus + Producer surplus

Or

Total surplus = Total benefits - Total costs

Define the term “deadweight loss”

the loss of benefits to society when a market does not produce or sell the right amount of goods. (A tax on cigarettes can create deadweight loss because higher prices reduce consumption below the socially efficient level, causing lost welfare.)

Explain how and why firms with market power (such as Apple) create deadweight loss in their market

Firms with market power restrict output and raise prices above cost, reducing trades and causing deadweight loss in the market.