AP Macro FULL REVIEW TERMS

1/13

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

14 Terms

Scarcity

unlimited wants/needs but limited resources (labor, land, capital, natural resources)

Planned V. Market Economy

A comparison of two economic systems where a planned economy is controlled by the government while a market economy relies on supply and demand with minimal government intervention.

Invisible Hand

Individuals/businesses meet societies’ needs when they seek their own self-interest

Physical capital

Refers to tangible assets such as machinery, buildings, and tools used in the production of goods and services.

Human capital

Refers to the skills, knowledge, and experience possessed by individuals that contribute to economic productivity.

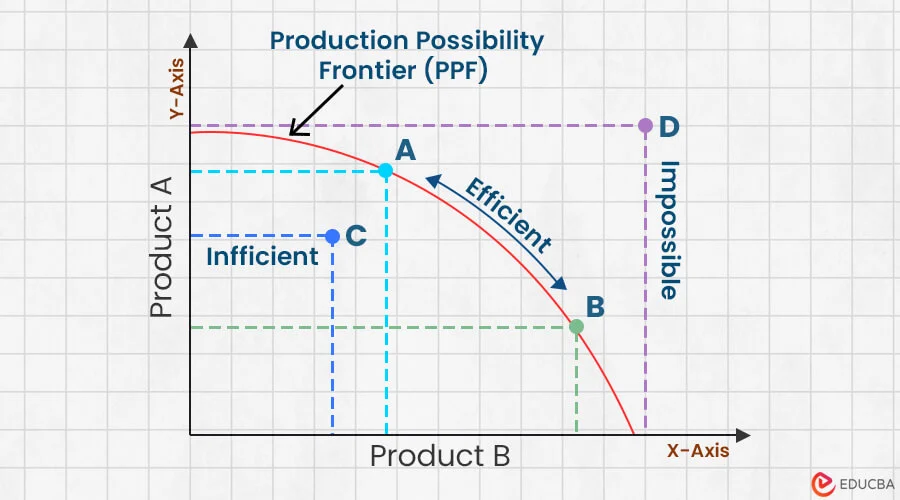

Production Possibilities Curve

A graph that shows the maximum possible output combinations of two goods or services that can be produced with available resources and technology. (inside curve= not efficent; outside curve= not enough resources)

Opportunity Cost

The loss of potential gain from other alternatives when one alternative is chosen, reflecting the true cost of a decision.

Absolute Advantage

Refers to the ability of an individual or group to carry out a particular economic activity more efficiently than another individual or group. It indicates that a party can produce more of a good or service with the same resources than another.

Comparative Advantage

Refers to the ability of an individual or group to produce a good or service at a lower opportunity cost than another party, emphasizing the benefits of specialization and trade.

Terms of Trade

The rate at which one good is exchanged for another in trade between countries or parties, determining the benefits derived from specialization and comparative advantage.

Explicit V. Implicit Benefits

Refers to the clear and measurable advantages (explicit) that come from an economic decision, in contrast to the indirect or less obvious advantages (implicit) that may also exist but are harder to quantify. (cost of going to school vs. benefits that come from it like seeing your friends)

Total Utility

explicit + implicit benefits

Marginal utility

The change in ulitity over the number of times something is done (difference in values of y)

-Total ulitity = adding up marginal ulitity

MU/P

-Rule to maximize utility = the consumer’s money should be spent so that the marginal ulitty per dollar of each goods equal to each other