Unit 2.2 Mortgages

1/32

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

33 Terms

Define mortgage

“A loan secured by the value of a real estate property”

Describe a mortgage is relation to present value (PV)

“A mortgage is an annuity where the present value (PV) is the amount borrowed to purchase a home”

Define amortization

The gradual elimination of a debt or liability

Define amortization period

The time for which the calculation of a mortgage payment is determined

The length of time needed to eliminate a debt

What is a typical amortization period for a mortgage?

20 to 30 years

What is a typical amortization period for a personal loan?

1 to 5 years

Define mortgage term

The length of the mortgage agreement

Often 1 to 7 years

Renegotiated several times over the amortization period

Define amortization table

Table the shows the breakdown of the principal, payments, interest paid, and the unpaid loan balances over the amortization period

Define appreciation rate

The rate at which the value of an item increases over time

Explain the difference between amortization period and mortgage term using an example

A mortgage may be set for an amortization period of 25 years while the mortgage term is 5 years. This means that every 5 years the mortgage is renewed possibly with a new interest rate

Define open mortgage

A mortgage that permits repayment of the principal amount at any time without penalty

Define closed mortgage

A mortgage that has a repayment limit. You are only permitted to pay a certain percentage of the original principal balance of the mortgage per calendar year

Define variable-rate mortgage

A mortgage that will fluctuate with the financial institution’s prime rate throughout the mortgage term. Regular payment will stay the same but your interest rate may change based on market conditions. This impacts the amount of principal you pay off each month

Define fixed rate mortgage

A mortgage that has a fixed interest rate for the entire term of the loan

Define pre-approved mortgage

Used to determine the maximum price for a home that a buyer can afford. The lending financial institution determines the maximum amount that can be borrowed to purchase a home

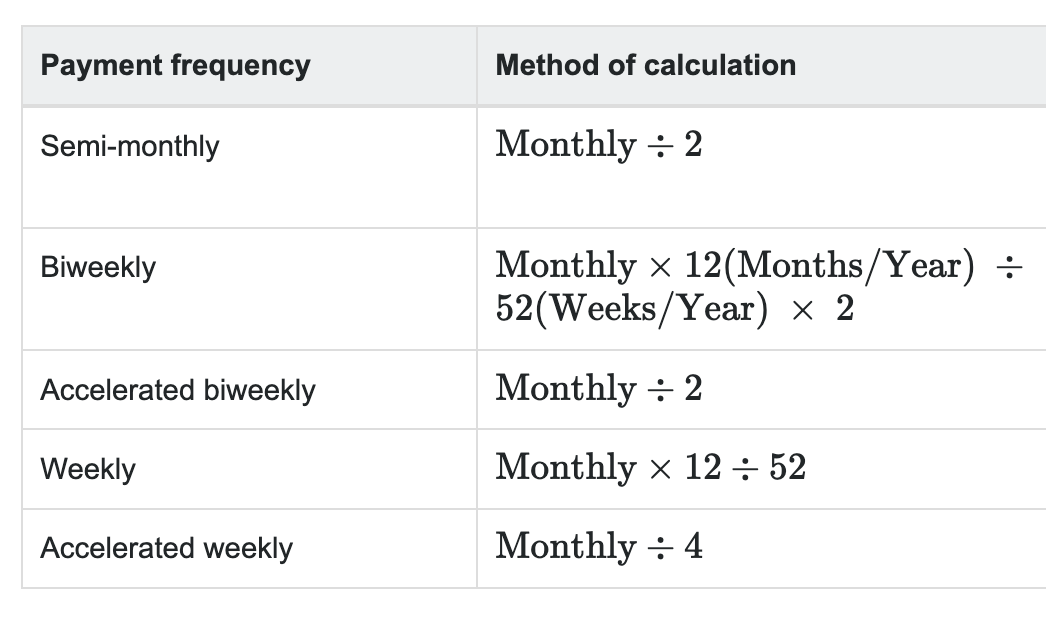

Define semi-monthly payment

Means that half the monthly payment is paid twice a month

Usually on the 15th and 30th of each month

Define biweekly payment

Payment made every 2 weeks

Define accelerated biweekly payment

Half the monthly payment is paid every 2 weeks

Means 1 extra monthly payment is paid each year

Define weekly payment

Payment made every week

Define accelerated weekly payment

One quarter of the monthly payment is paid each week

Means one extra monthly payment is paid each year

Calculating mortgage, which tool should you use- Excel or an online mortgage calculator? Why?

Online mortgage calculator

Canada has special rules that won’t be reflected in Excel

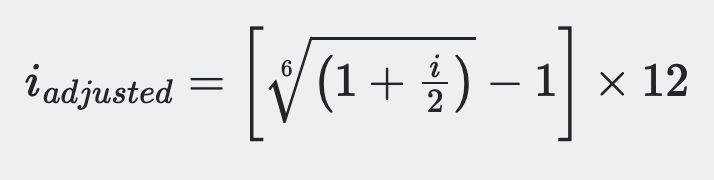

If you want to use Excel to calculate mortgage, what is the equation to adjust for Canada’s special rules?

Every time a mortgage is renewed (mortgage term), what is important to remember?

Important to know the amount still owing on the mortgage

During a question, if given the original loan and a down payment, what do you have to do?

Subtract the down payment from the loan and that number is what you will input into the mortgage calculator

If you figure out your monthly payments for a 5 year mortgage term, would subtracting that number from the original loan show how much is left to pay on the mortgage?

No. Because the monthly payments include interest.

Must find out how much interest was included in all the payments for the 5 years to find out the amount of the principal you have actually paid off

If a question asks you to calculate principal + interest paid at the end of a time period, who would you do it?

Find original loan and the full amount remaining to pay

Subtract remaining from loan

If the monthly payment on a 20-year mortgage was $1000, what would you pay for semi-monthly payment frequency?

Pay twice per month

$500

If the monthly payment on a 20-year mortgage was $1000, what would you pay for biweekly payment frequency?

Every other week (find yearly total and divide by 26 weeks)

$461.54

If the monthly payment on a 20-year mortgage was $1000, what would you pay for accelerated biweekly payment frequency?

Same as semi-monthly

$500

If the monthly payment on a 20-year mortgage was $1000, what would you pay for weekly payment frequency?

Full year amount divided by 52 weeks in a year

$230.77

If the monthly payment on a 20-year mortgage was $1000, what would you pay for accelerated weekly payment frequency?

Instead of dividing by 52 weeks in a year, divide by weeks in a month

$250.00

After calculating the amounts for several payment frequencies, what would you multiply the amounts by if you wished to get a yearly total?

Monthly X 12

Semi-monthly X 24

Biweekly X 26

Accelerated biweekly X 26

Weekly X 52

Accelerated weekly X 52