Module 5: Capital Investments and Capital Allocation

1/17

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

18 Terms

The incremental after-tax cash flows (in € thousands) and information on two mutually exclusive projects are as follows:

The appropriate hurdle rate to use in evaluating the projects is 15.0%. Which of the following statements is most accurate? The company should accept:

A. Both projects.

B. Project Y only.

C. Project X only.

B. Project Y only.

Given a discount rate of 10%, the net present value (NPV) of the following investment is closest to:

C. 636.

A project has the following annual cash flows:

Which of the following discount rates most likely produces the highest net present value (NPV)?

A. 8%

B. 10%

C. 15%

C. 15%

A firm is considering a project that would require an initial investment of THB270 million (Thai baht). The project will help increase the firm’s after-tax net cash flows by THB30 million per year in perpetuity, and it is found to have a negative NPV of THB20 million. The IRR (%) of the project is closest to:

A. 10.3%.

B. 11.1%.

C. 12.0%.

B. 11.1%.

A measure of how effectively capital is converted into after-tax operating profits is the:

A. hurdle rate.

B. cost of capital.

C. return on invested capital.

C. return on invested capital.

Correct Answer Feedback:

Correct because ROIC reflects how effectively a company’s management is able to convert capital into after-tax operating profits.

Which of the following is considered a capital allocation pitfall? Basing investment decisions on:

A. opportunity costs.

B. after-tax cash flows.

C. short-run accounting numbers.

C. short-run accounting numbers.

Correct Answer Feedback:

Correct because one common pitfall is basing investment decisions on EPS, net income, or ROE: Companies sometimes have incentives to boost earnings per share, net income, or return on equity. Many investments, even those with strong NPVs, do not increase these accounting numbers in the short run and may even reduce them. Paying too much attention to short-run accounting numbers can result in a company choosing investments that are not in the long-run economic interests of its shareholders.

When choosing between mutually exclusive projects, an analyst should:

A. accept the project with the highest IRR.

B. use the opportunity cost of funds as the discount rate.

C. accept the projects for which the IRR is greater than the opportunity cost of funds.

B. use the opportunity cost of funds as the discount rate.

Correct Answer Feedback:

Correct because when the choice is between two mutually exclusive projects and the NPV and IRR rank the two projects differently, the NPV criterion is strongly preferred. We referred to the rate used in discounting the cash flows as the “required rate of return.” The required rate of return is the discount rate that the issuer’s suppliers of capital require given the riskiness of the project. This discount rate is frequently called the “opportunity cost of funds” or the “cost of capital.” For a capital investment with one investment outlay, made initially, the net present value (NPV) is the present value of the future after-tax cash flows minus the investment outlay, where the discount rate equals the required rate of return.

A company is evaluating the following mutually exclusive capital projects:

If the hurdle rate is 8%, the company should invest in:

A. Project 1 only.

B. Project 2 only.

C. both Project 1 and Project 2.

A. Project 1 only.

Correct Answer Feedback:

Correct because Project 1 has a higher NPV. For mutually exclusive investments that are ranked differently by the NPV and IRR, the NPV criterion is more economically sound.

An electric vehicle manufacturer invests in a new technology to meet new safety standards. This project is best classified as a(n):

A. expansion project.

B. compliance project.

C. going concern project.

B. compliance project.

Correct Answer Feedback:

Correct because regulatory and compliance projects are required by third parties, such as government regulatory bodies, to meet safety and regulatory compliance standards. The investment in new technology to meet improved safety standards is therefore a compliance project.

Compared to going concern projects, expansion projects most likely involve:

A. greater uncertainty only.

B. greater amounts of capital only.

C. both greater uncertainty and greater amounts of capital.

C. both greater uncertainty and greater amounts of capital.

Correct Answer Feedback:

Correct because expansion projects typically involve greater uncertainty, time, and amounts of capital than going concern projects.

A company should exercise the abandonment option on an investment if the present value of the cash flows from continuing the investment is:

A. lower than the cash flow from abandoning the investment.

B. the same as the cash flow from abandoning the investment.

C. greater than the cash flow from abandoning the investment.

A. lower than the cash flow from abandoning the investment.

Correct Answer Feedback:

Correct because if the cash flow from abandoning an investment exceeds the present value of the cash flows from continuing the investment, the company should exercise the abandonment option. Conversely, if the PV of the cash flows from continuing the investment is lower than the cash flow from abandoning the investment, the company should exercise the abandonment option.

A company with a required rate of return of 12% is considering a capital project with the following cash flows (in millions):

The expected IRR for this project is most likely:

A. less than 12%.

B. equal to 12%.

C. greater than 12%.

A. less than 12%.

Correct Answer Feedback:

Correct because the IRR is the discount rate that makes the present value of the future after-tax cash flows equal that investment outlay or ∑nt=1 CFt ÷ (1 + IRR)t = Outlay, where IRR is the internal rate of return. Solved using the following calculator inputs: CF0 = −150, CF1 = 8, CF2 = 175, Calculate IRR = 10.7119, rounded to 10.71% which is less than 12%.

Subsequent to making a capital investment, a company reacts to poor financial results from the project by abandoning it. This action alone best exemplifies the exercise of a:

A. sizing option.

B. timing option.

C. flexibility option.

A. sizing option.

Correct Answer Feedback:

Correct because sizing options encompass abandonment or expansion of capacity. If after investing the company can abandon the investment if the financial results are disappointing, it has an abandonment option. At some future date, if the cash flow from abandoning an investment exceeds the present value of the cash flows from continuing the investment, the company should exercise the abandonment option. Conversely, if the company can make additional investments when future financial results are strong, the company has a growth option or an expansion option.

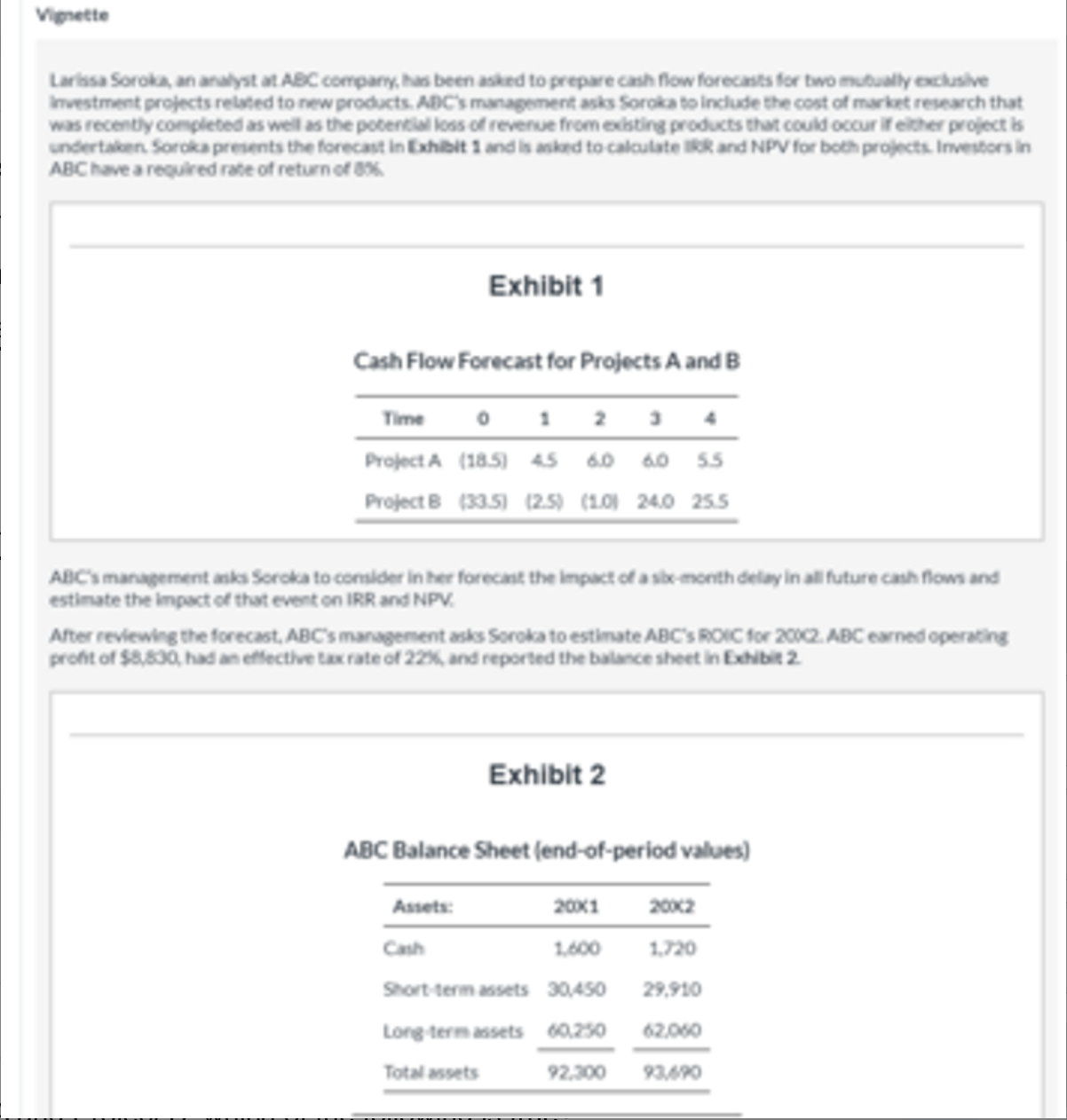

When preparing the cash-flow forecasts for both projects, Soroka should include:

A. only the cost of the market research.

B. only the loss of revenue from existing products.

C. both the market research cost and the loss of revenue from existing products.

B. only the loss of revenue from existing products.

With regard to Project A and Project B, which of the following is true?

A. Both projects should be invested in according to the IRR decision rule.

B. Both projects should be invested in according to the NPV decision rule.

C. Only Project B should be invested in according to the IRR decision rule.

C. Only Project B should be invested in according to the IRR decision rule.

The most likely impact from the cash-flow timing considered by Soroka is that:

A. both IRR and NPV would decrease.

B. both IRR and NPV stay unchanged.

C. only IRR would decrease but NPV would increase.

A. both IRR and NPV would decrease.

Based on ABC’s balance sheet presented in Exhibit 2, Soroka should calculate:

A. average invested capital of $72,510 and ROIC of 9.50%.

B. average invested capital of $80,720 and ROIC of 10.94%.

C. average invested capital of $92,995 and ROIC of 9.50%.

A. average invested capital of $72,510 and ROIC of 9.50%.

Considering ABC management’s ROIC-based investment criterion and the IRR and NPV of both projects, Soroka should recommend to:

A. reject both projects A and B.

B. invest only in Project B because it has a higher NPV.

C. invest only in Project A because has positive cash flow during all four years.

A. reject both projects A and B.