Lecture 7 - Full Costs, Absorption Costing and ABC

1/71

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

72 Terms

What is the main difference between marginal costing and absorption costing?

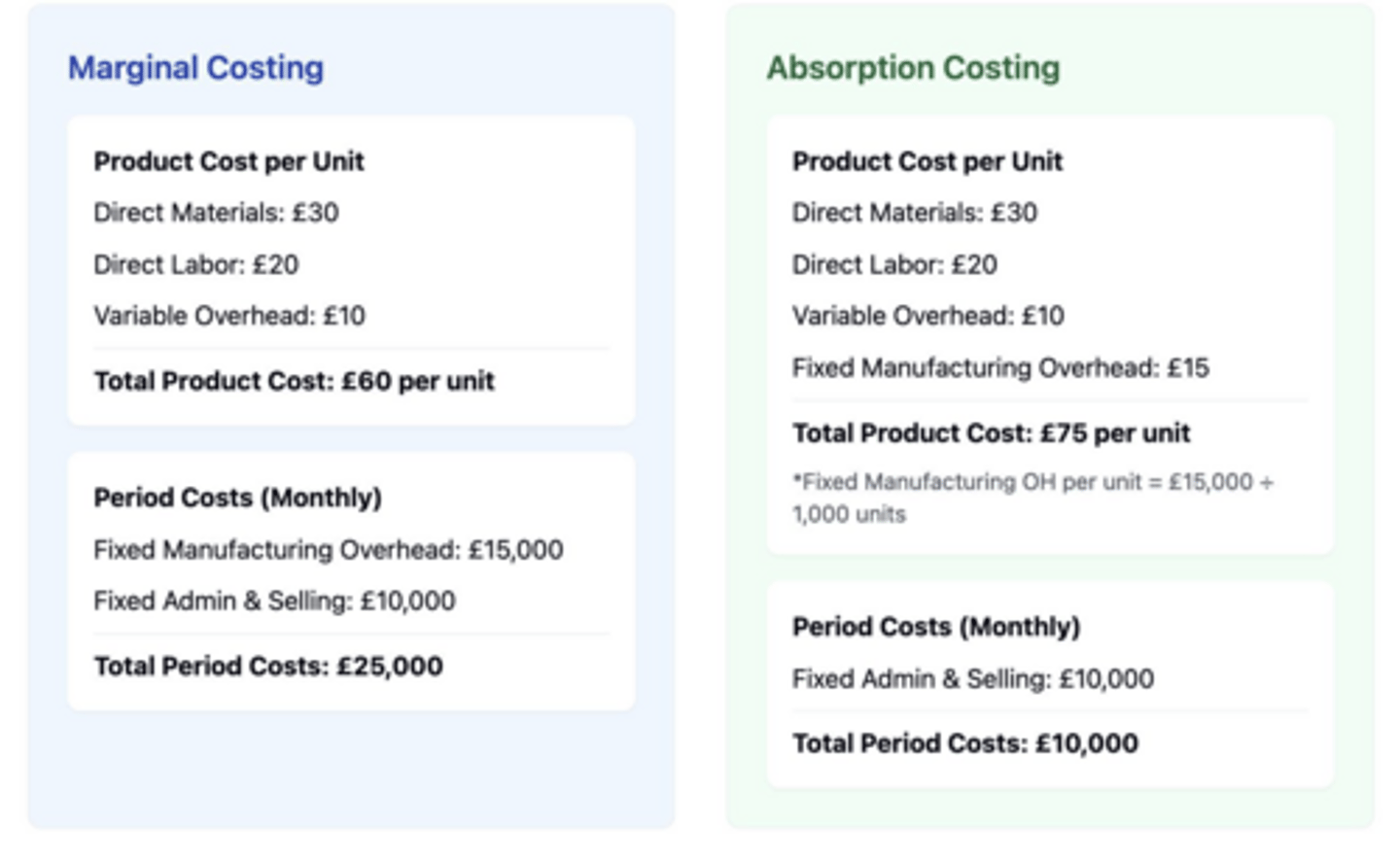

Marginal costing treats fixed production overheads as period costs, while absorption costing includes them in product costs.

What are the components of production cost under absorption costing for Omega Ltd?

Direct Labour (£45), Direct Material (£54), Variable Production Overhead (£36), Fixed Production Overhead (£45) totaling £180.

What is the production cost per unit under marginal costing for Omega Ltd?

£135, which includes Direct Labour (£45), Direct Material (£54), and Variable Production Overhead (£36).

What are the four main purposes of using full cost by managers?

Assessing relative efficiency, exercising control, pricing and output decisions, and assessing performance.

Why are overheads significant in full costing?

Overheads significantly affect the full cost and pricing of products; accurate allocation is crucial for informed decision-making.

What are the two approaches to assign indirect costs in full costing?

Traditional (absorption) costing and activity-based costing (ABC).

What is the definition of allocation in absorption costing?

Allocation is the charging of discrete identifiable items of costs to a cost centre or cost unit.

What does apportionment mean in the context of costing?

Apportionment is the division of costs among two or more cost centres in proportion to the benefits received.

What is the formula for calculating the Overhead Absorption Rate (OAR)?

OAR = Budgeted Production Overhead / Budgeted total of Absorption basis.

What does under-absorption of overheads indicate?

Under-absorption occurs when actual overheads exceed budgeted overheads or when actual activity levels are lower than budgeted.

How is over-absorption of overheads defined?

Over-absorption occurs when actual overheads are less than budgeted overheads or when actual activity levels exceed budgeted.

What is the purpose of the predetermined Overhead Absorption Rate (POHR)?

POHR is used to allocate overhead costs to products based on estimated activity levels.

In the case of Amy, Brian, and Cindy, how should they share the rent and bills?

They should split the rent (£600) and bills (£300) equally among the three.

How should the broadband package cost be shared among Amy, Brian, and Cindy?

The broadband package cost should be shared based on usage; since only Amy and Brian use the phone, they may share differently than Cindy.

What is the total budgeted assembly overheads in the example provided?

£180,000.

What is the budgeted assembly hours in the example?

40,000 hours.

What is the actual assembly hours worked in the example?

38,000 hours.

What is the actual assembly overheads incurred in the example?

£190,000.

How do you calculate the absorbed overheads?

Absorbed overheads = POHR × Actual activity.

What is the result of the under-absorption calculation in the example?

Under-absorbed by £19,000 due to adverse expenditure and volume variances.

What are non-manufacturing overheads treated as for external reporting?

Non-manufacturing overheads are treated as period costs.

What is the significance of the absorption of overheads?

It is necessary to calculate the full product cost for accurate pricing and financial reporting.

What is the first step in the traditional absorption costing approach?

Identify cost centres as service or production.

What is the second step in the absorption costing process?

Determine indirect costs for each cost centre through allocation or apportionment.

What is the third step in the absorption costing process?

Share service cost centre costs to production centres.

What is the fourth step in the absorption costing process?

Absorb overheads to units of output using appropriate absorption rate.

What is the primary difference between Marginal Costing and Absorption Costing?

Marginal Costing considers only variable costs as product costs, while Absorption Costing includes both variable and fixed manufacturing costs.

What are Cost Centers?

Cost Centers are departments or functions that incur costs, which are then allocated to cost objects.

What is a Cost Object?

A Cost Object is any item for which costs are measured and assigned, such as products or services.

How are costs classified by behavior?

Costs are classified as Variable Costs (change with production volume) and Fixed Costs (remain constant regardless of production volume).

What are Direct Costs?

Direct Costs are expenses that can be directly traced to a specific cost object, such as materials used in production.

What are Indirect Costs?

Indirect Costs, or overheads, are expenses that cannot be directly traced to a specific cost object, such as rent and utilities.

What is the difference between Product Costs and Period Costs?

Product Costs are associated with manufacturing and included in inventory until sold, while Period Costs are non-manufacturing costs expensed in the period incurred.

What is included in the determination of Unit Full Cost?

Unit Full Cost includes direct materials, direct labor, direct expenses, and a share of indirect expenses (factory overheads).

What happens to unsold product costs?

Unsold product costs are recorded as inventory on the Statement of Financial Position (SOFP).

What happens to sold product costs?

Sold product costs are recorded as Cost of Sales in the Income Statement.

What are Non-manufacturing Costs?

Non-manufacturing Costs include expenses related to selling and administrative functions, which are not directly tied to production.

In the context of manufacturing, what is a prime cost?

Prime Cost refers to the total of direct materials, direct labor, and direct expenses incurred in the production of goods.

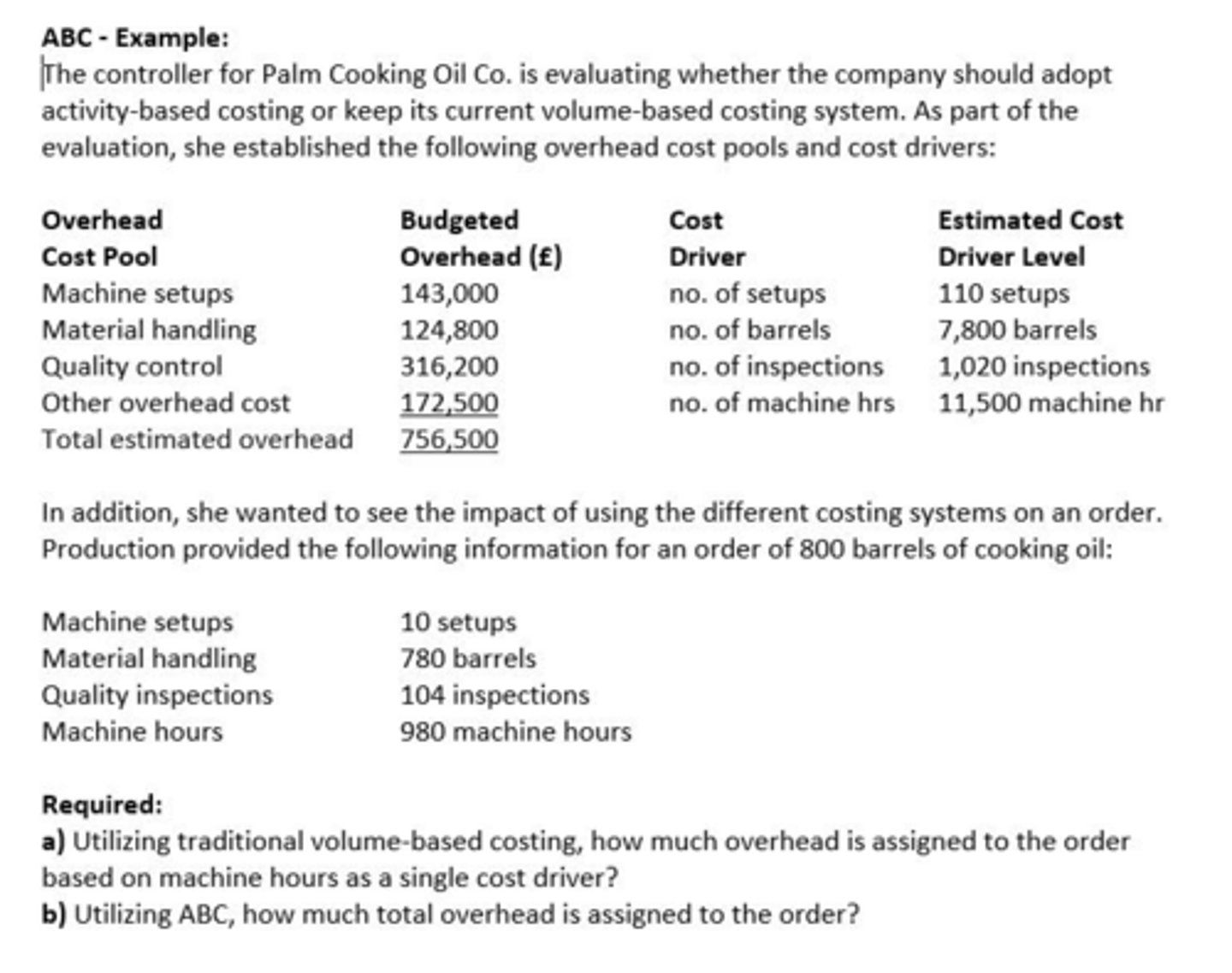

What is the purpose of Activity Based Costing (ABC)?

Activity Based Costing (ABC) aims to allocate overhead costs more accurately by identifying activities that drive costs.

How does management use cost information?

Management uses cost information to formulate strategies, make pricing decisions, manage costs, and meet external reporting requirements.

What is the role of fixed manufacturing overhead in Absorption Costing?

In Absorption Costing, fixed manufacturing overhead is treated as a product cost and allocated to each unit produced.

What is the significance of understanding full product costs?

Understanding full product costs is essential for accurate pricing, profitability analysis, and financial reporting.

What is the cost per unit under Marginal Costing for a chair manufacturing company with given costs?

The cost per unit under Marginal Costing includes only direct materials, direct labor, and variable overhead.

What is the cost per unit under Absorption Costing for a chair manufacturing company with given costs?

The cost per unit under Absorption Costing includes direct materials, direct labor, variable overhead, and a share of fixed manufacturing overhead.

What is the purpose of classifying costs by time?

Classifying costs by time helps in understanding when costs are incurred and how they impact financial statements.

What is the importance of overhead rates in cost allocation?

Overhead rates are used to allocate indirect costs to cost objects based on a predetermined method, ensuring accurate cost measurement.

What is the main difference between marginal costing and absorption costing?

Marginal costing includes only variable manufacturing costs, while absorption costing includes both variable and fixed manufacturing costs.

What does full costing include?

Full costing includes variable and fixed manufacturing costs, as well as non-manufacturing costs.

Why do we need product costs?

Product costs are needed for product mix decisions, stock valuation, pricing decisions, and cost control.

How are non-manufacturing overheads treated in absorption costing?

Non-manufacturing overheads are treated as period costs for external reporting but need to be absorbed to determine full product cost.

What is the purpose of absorption costing?

Absorption costing is used to allocate overhead costs to products to establish selling prices and ensure a desired gross profit margin.

What are the budgeted direct labour hours for Department A?

20,000 hours

What is an overhead absorption rate (OAR)?

OAR is calculated as total overhead costs divided by production hours.

What is the main criticism of traditional costing systems?

Traditional costing systems fail to provide accurate product costs as overhead costs are allocated using simplistic measures that do not reflect actual resource demands.

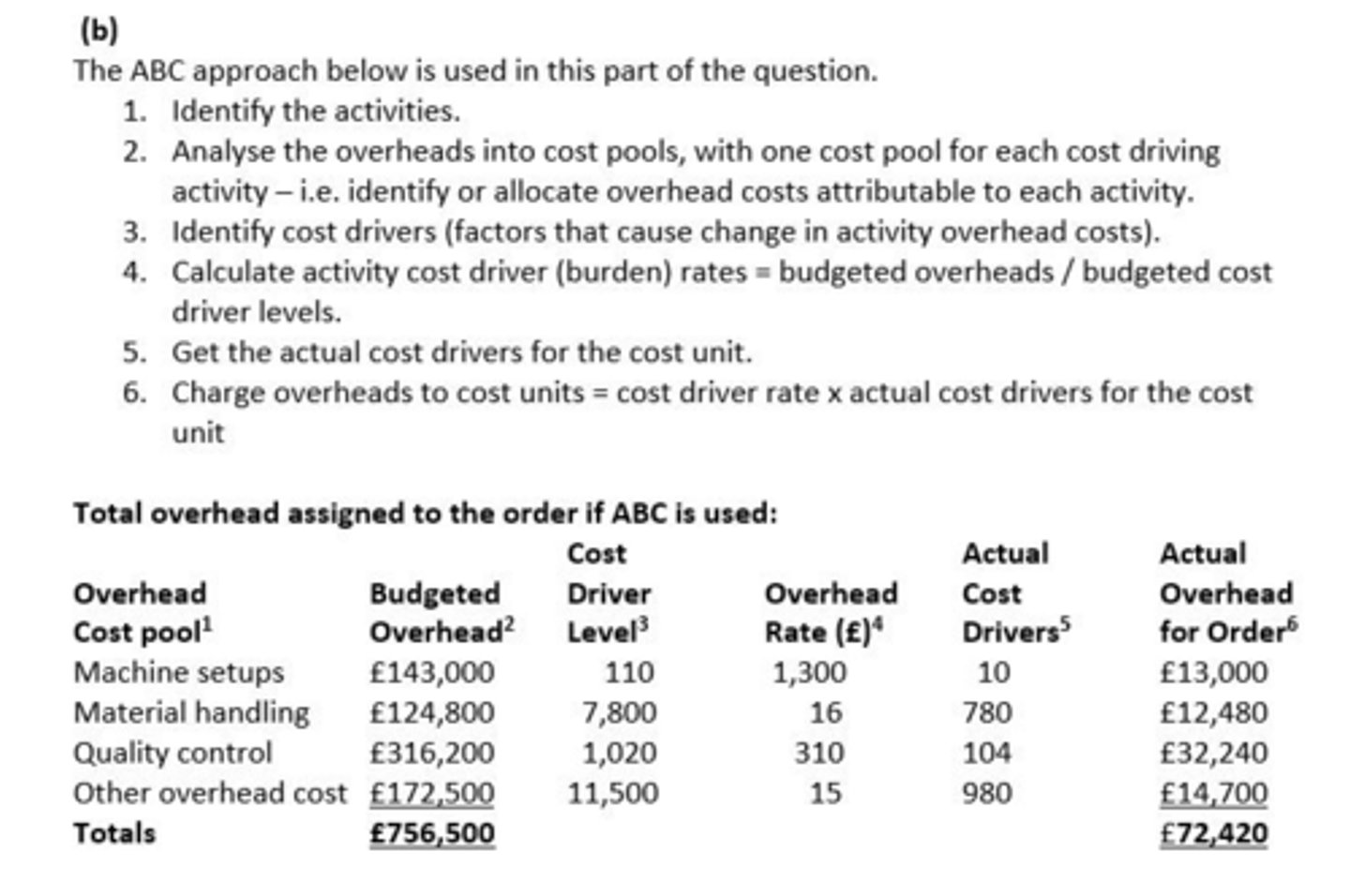

What is the first step in the Activity Based Costing (ABC) approach?

Identify the major activities that take place.

What is a cost driver in ABC?

A cost driver is a factor that causes changes in activity overhead costs.

What are the advantages of using Activity Based Costing (ABC)?

ABC highlights misplaced emphasis on volume-related cost drivers, encourages collaboration between departments, provides useful control data, and focuses on the causes of costs.

What are some limitations of Activity Based Costing (ABC)?

Limitations include the need for identifying cost drivers, advantages for pricing only if cost-plus, reliance on past data, potential conflicts from system changes, and arbitrary cost allocations.

What is the purpose of creating a cost pool in ABC?

To allocate overhead costs attributable to each major activity.

How does the ABC approach differ from traditional costing?

In ABC, overheads are assigned to cost pools first, then allocated to cost units using cost driver rates, while traditional costing assigns overheads to product cost centers first.

What is the significance of calculating activity cost driver rates?

Activity cost driver rates are used to charge overheads to cost units based on actual cost drivers.

What is the role of the production manager's salary in overhead allocation?

It is allocated based on production hours to determine total overhead costs.

Why is there dissatisfaction with traditional costing systems?

Due to changes in cost structures and the need for accurate product costs in a competitive market.

What is the gross profit margin targeted by Green Oak Ltd. for its selling prices?

25% of the sales price.

What are the budgeted variable overhead costs for indirect labor?

£38,000

What is the total budgeted fixed overhead for rent?

£18,000

What is the budgeted cost for maintenance in Department A?

£10,000

What is the budgeted cost for maintenance in Department B?

£8,000

What is the budgeted cost for maintenance in Department C?

£6,000

What is the total budgeted depreciation for Department A?

£3,000

What is the total budgeted depreciation for Department B?

£4,000

What is the total budgeted depreciation for Department C?

£7,000