CFA - Quant 1

1/91

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

92 Terms

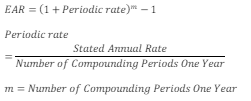

Effective Annual Rate (EAR)

*Rate and Returns

Rate of interest that an investor can earn (or pay) in a year after taking into consideration compounding

Nominal Risk-Free Rate

*Rate and Returns

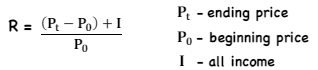

Holding Period Return (HPR)

*Rate and Returns

Return on an asset/portfolio over the period during which it was held

Multi-Period HPR

*Rate and Returns

Arithmetic Mean

*Rate and Returns

When it's used: Used to estimate E(R) over one period

Geometric Mean

*Rate and Returns

When it's used: Used to estimate average E(R) per period over multiple periods, use for returns

RG <= RA

FV = PV(1 + RG) - measures an investment’s terminal value over multiple periods

Harmonic Mean

*Rate and Returns

Reduces the effect of outliers & underweight their impact

When it’s used: Multiples/ratios, dollar-cost averaging, average price per unit

Relationship w other means: RA (overweight) x X-barH (underweight) ~ RG²

Trimmed Mean & Winsorized Mean

*Rate and Returns

Trimmed: Remove a percentage from both largest and smallest, e.g. 8% trimmed - 16% total (common with CPI)

Winsorized: Replacing values at both ends with cutoff value

Money-Weighted Return (IRR, YTM)

*Rate and Returns

Discounting CFs

What your money earned, not the typical $1

More sensitive to the timing and amount of withdrawals/additions to the portfolio (e.g. if you committed more money to a poor performance year, your mwrr < RA)

Time-Weighted Return

*Rate and Returns

= RG (same as geometric mean)

Represents growth of $1 over a given period

Method

Break investment period into holding periods

Calculate each HPR, compound HPRs, express annually

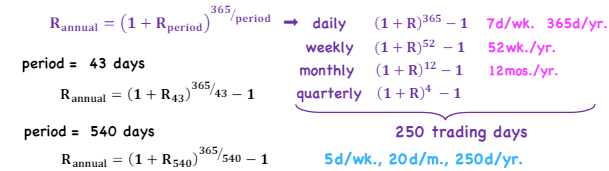

Annualized Return

*Rate and Returns

All rates/returns are quoted annually

Can be misleading - assumes that returns can be repeated

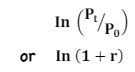

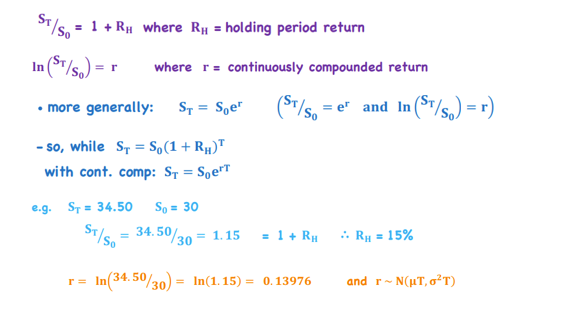

Continuously-Compounded Return

*Rate and Returns

Continuously compounded return is equivalent to its annual counterpart

To get back to annual rate: erc - 1

Gross v. Net Return

*Rate and Returns

Gross: What the fund earns - return before deductions for management. exp, custodial fees, taxes… BUT after trading expenses

Net: What the investor earns

Real Return

*Rate and Returns

After-tax real return - Investor measure of growth in purchasing power of portfolio

Leveraged Return

*Rate and Returns

Use leverage when return on portfolio Rp > cost of debt rd (if you’d earn more an more in an investment than you would from borrowing money)

RL = RP/PE = [RP x (Total Value) - (Debt Value x rb)]/Equity Value

RL = RP + VB/VE*(Rp - rd)

![<p>Use leverage when return on portfolio R<sub>p</sub> > cost of debt r<sub>d</sub> (if you’d earn more an more in an investment than you would from borrowing money)</p><p>R<sub>L</sub> = R<sub>P</sub>/P<sub>E</sub> = [R<sub>P</sub> x (Total Value) - (Debt Value x r<sub>b</sub>)]/Equity Value</p><p>R<sub>L </sub>= R<sub>P</sub> + V<sub>B</sub>/V<sub>E</sub>*(R<sub>p</sub> - r<sub>d</sub>)</p>](https://knowt-user-attachments.s3.amazonaws.com/273b968d-43bc-4c33-a221-d90a3867e16d.png)

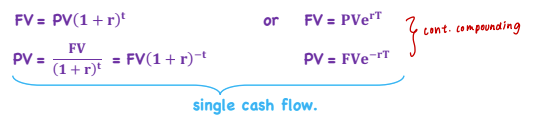

Zero-Coupon Bond/ZCB (Single CF)

*TVM - Fixed Income

Sold at a discount, matures at par

Ex. T-bills

Coupon Bond

*TVM - Fixed Income

Investor receives a number of interest payments over time and par at maturity

Ex. Notes, bonds

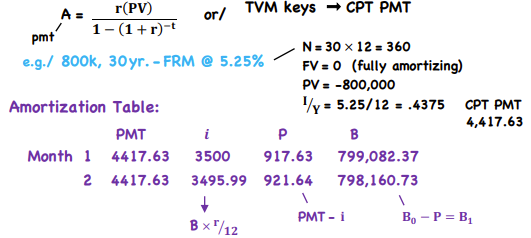

Fully Amortizing Bonds

*TVM - Fixed Income

Investor receives level payments of both interest and principal

Ex. Mortgage, auto loan

Perpetuity

*TVM - Fixed Income

Ex. bonds, preferred shares

Annuity

*TVM - Fixed Income

Ex. mortgage, car loans

Perpetuity (Constant Dividend)

*TVM - Equity

Ex. Many REITs

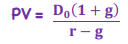

Growing Perpetuity (Constant Growth Dividend)

*TVM - Equity

Ex. Commercial real estate - to calculate property value

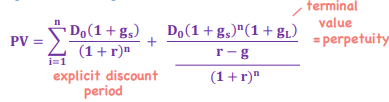

2-Stage Model (Growth Moving to Value)

*TVM - Equity

Rate of growth will slow down in the long-term

Explicit discount period - Similar to coupon bonds

Terminal value - Perpetuity (discount terminal value to this PV)

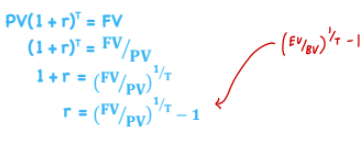

Implied Return on Fixed Income

*TVM - Fixed Income

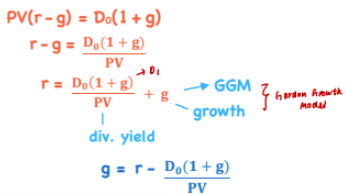

Required Return and Implied Growth of Equity

*TVM - Equity

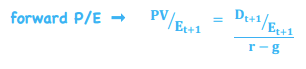

Forward PE

*TVM

PE formula: Constant growth dividend formula / Equity

Numerator becomes dividend payout ratio (DPR), D0 / E

Forward dividend payout ratio = DPR * (1 + g)

If forward dividend OR growth rate (g) is expected to increase, the stock/index will trade a higher forward multiple

Higher required return (r) leads to lower multiple (greater denominator)

Principle of No Arbitrage

*TVM

Cash flow additivity - 2 economically equivalent strategies should have the same price

Calculate PV of two CFs, select the higher one OR take the difference in CFs (A-B), if PV>0, choose A, else B

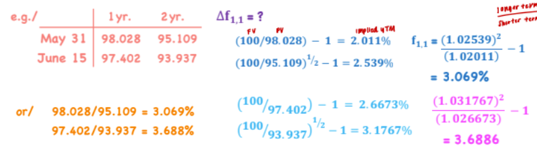

Implied Forward Rate

*TVM

fwhen, what — f3,4 = forward rate that begins in 3 years and lasts 4 years

Can also just divide the two PV’s to get implied forward rate

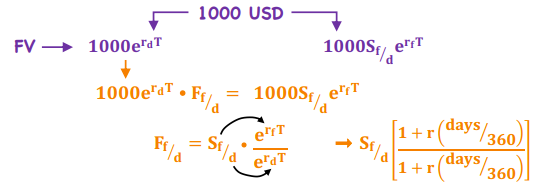

Forex - Foreign Exchange Rate

*TVM

Ff/d = Forwards/futures price

Sf/d = Spot rate (foreign/domestic)

rd = Domestic rate

rf = Foreign rate

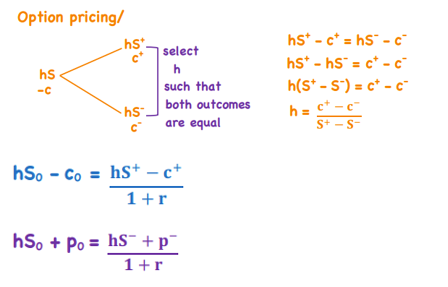

Option pricing

*TVM

h = Hedge ratio

Short a call (-)

Long a put (+)

Notations for X and Y Terms

X-bar/Y-bar = Sample mean

X-hat/Y-hat = Estimate

Xi/Yi = Specific values of X/Y

Dispersion

*Statistical Measures of Asset Returns

Variability around the central tendency

A measure of risk or uncertainty

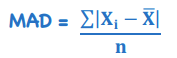

Mean (of the) Absolute Deviation

*Statistical Measures of Asset Returns - Dispersion

Average distance between each data point and the mean

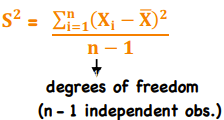

Sample Variance

*Statistical Measures of Asset Returns - Dispersion

Average/expected deviation from the mean

Square root of sample variance = sample SD

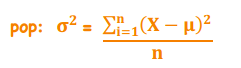

Population Variance

*Statistical Measures of Asset Returns - Dispersion

Square root of population variance population SD

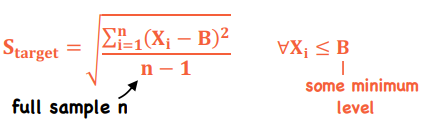

Downside Deviation (ex. Target Semideviation)

*Statistical Measures of Asset Returns - Dispersion

A measure of the risk of being below a certain target B

As B increases, Starget also increases

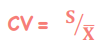

Coefficient of Variation (CV)

*Statistical Measures of Asset Returns - Dispersion

Measure of relative dispersion

For returns, CV measures the risk per unit of return

Lower = better, since it indicates less uncertainty, tighter distribution

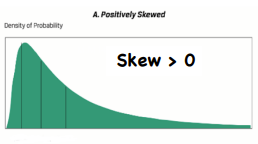

Positive Skew

*Statistical Measures of Asset Returns - Distribution

Mean > median > mode (highest point of distribution)

Ex. Long options portfolio - a lot of small losses & a few large gains

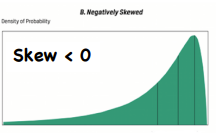

Negative Skew

*Statistical Measures of Asset Returns - Distribution

Mean < median < mode (highest point of distribution)

Ex. Short options portfolio - a lot of small gains & a few big losses

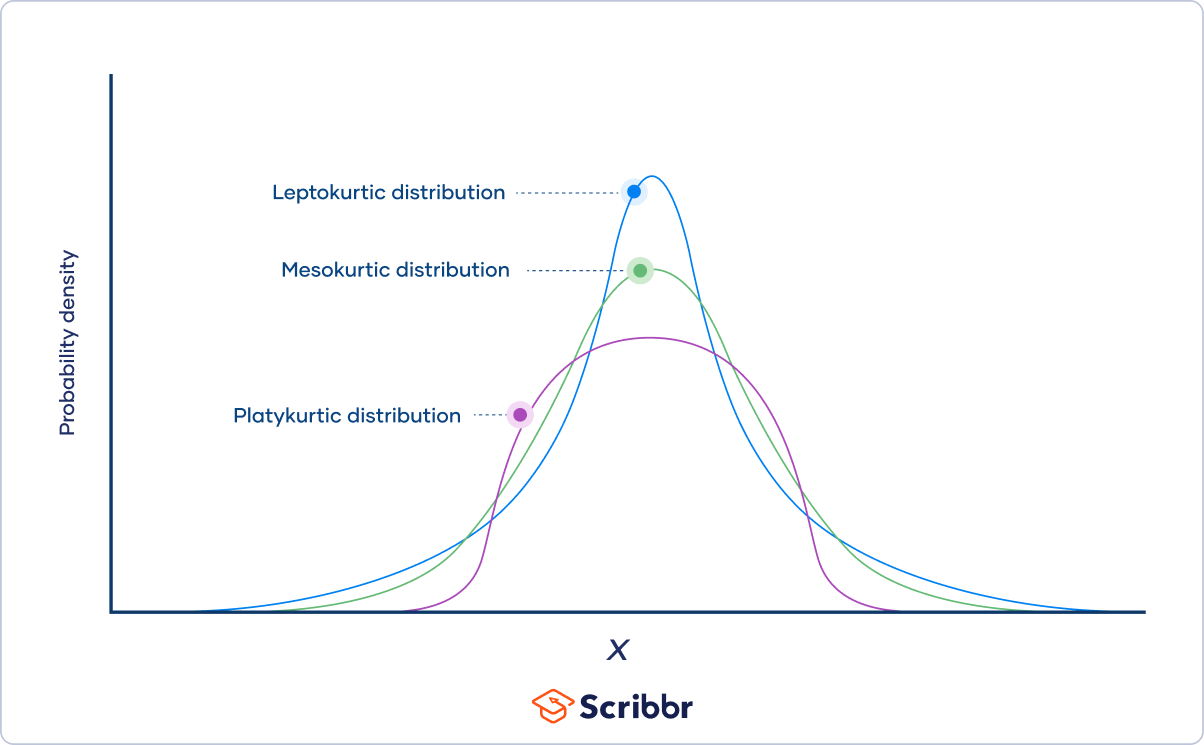

Kurtosis

*Statistical Measures of Asset Returns - Distribution

Measures how much of a probability distribution falls in the tails instead of its center (Normal distribution has K = 3)

Types:

Leptokurtic (K > 3, Ke > 0) - More observations around the mean with more weight in the tails

Mesokurtic (K = 3, Ke = 0)

Platykurtic (K < 3, Ke < 0) - Few observations around the mean with less weight in the tails

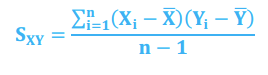

Covariance

*Statistical Measures of Asset Returns - Correlation

Joint variability of two random variables

SXY > 0 when the variables covary together (observation of X above its mean & observation of Y above its mean, vice versa with observations below means)

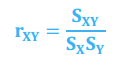

Correlation

*Statistical Measures of Asset Returns - Correlation

Measures linear association between two variables

Maximum diversification - No linear relationship (r = 0)

Perfect replication - Perfect positive correlation (r = 1)

Perfect hedge - Perfect negative correlation (r = -1)

Limitation: Spurious correlation - chance relationship with a third variable a (X/a, Y/a, still correlation rXY)

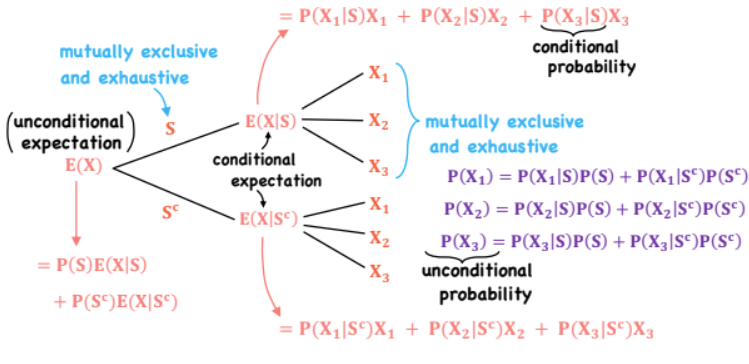

E(X) - Expected Value of a Random Variable

*Probability Trees and Conditional Expectations

Probability-weighted average of the possible outcomes - estimation of the ‘true’ population mean based on a sample

Variance/SD of a Random Variable (σ2/σ)

*Probability Trees and Conditional Expectations

Probability Tree

*Probability Trees and Conditional Expectations

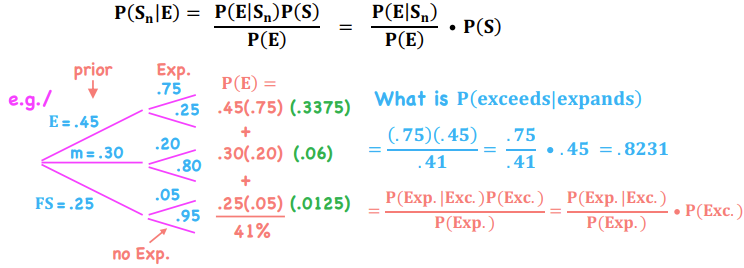

Bayes’ Formula

*Probability Trees and Conditional Expectations

Definition - A method for updating prior probabilities based on new information (switching conditionals)

Method:

1) Find total probability of the condition

2) Find each sub component that makes up the condition

3) Divide sub-component by total to update all prior probabilities

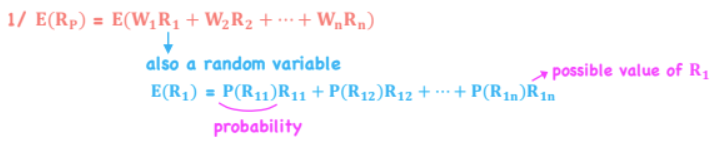

E(Rp) - Expected Value of Return

*Portfolio Mathematics

Portfolio Return - measure of expected reward

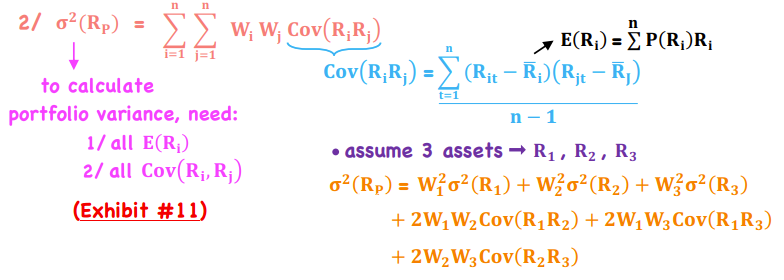

Portfolio Variance

*Portfolio Mathematics

Covariance of portfolio with 2 asset classes i and j = wi2(Ri) x wj2(Rj)× 2wiwjCov(RiRj)

For n securities/asset classes, there are:

n variances (ex. n = 5)

n2 - n covariances (ex. 25 - 5 = 20 cov)

(n2- n)/2 distinct covariances (ex. 20/2 = 10 unique cov)

Portfolio risk is lowered by selecting assets with 0 or negative covariance

Correlation

*Portfolio Mathematics

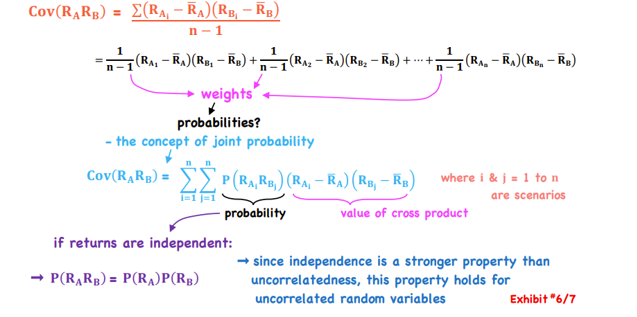

Covariance as a Joint Probability Function for Returns

*Portfolio Mathematics

Moving away from having expected return of an asset class to having expected returns based on possible scenarios (need joint probability)

Product of Deviations x Probability of Condition

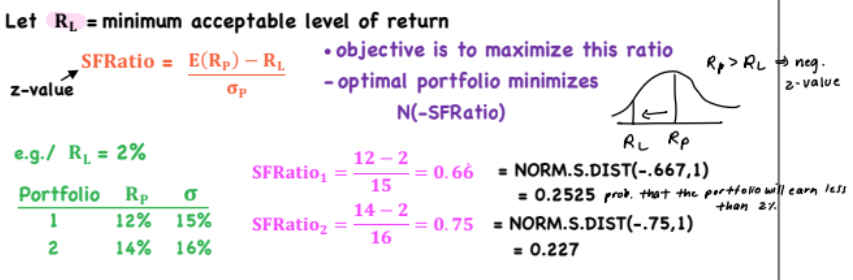

Shortfall Risk

*Portfolio Mathematics

Definition: The risk a portfolio value (or return) will fall below some minimum acceptable level over some time horizon

Objective is to maximize this ratio - Optimal portfolio minimizes N(-SFRatio)

NORM.S.DIST(-SFRatio, df) - Result is the probability that the portfolio will earn less than RL

If RL = Rf then SFRatio = Sharpe Ratio

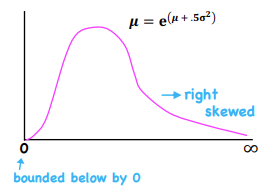

Lognormal Distribution

*Probability Distributions

Used to model the probability distribution of asset prices - described by the mean and variance of its associated normal distribution

Relationship between lognormal and normal distribution - A variable Y follows a lognormal distribution if LN(Y) is normally distributed

Lognormal Distributions - Return

*Probability Distributions

Used to model asset prices when using continuously compounded asset returns - cannot be negative (bounded below by 0)

Lognormal Distribution - Volatility

*Probability Distributions

Annualized SD of the continuously compounded daily returns of the underlying asset

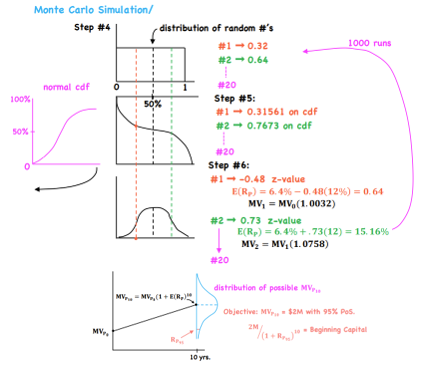

Monte Carlo Simulation

*Probability Distributions

Situation: We have a number of variables & we know how they behave since some common probability distributions describe the behavior of these variables - What are some other possible pathways of meeting my goals in the future with my portfolio return and SD?

Method:

1) Specify quantity of interest (ex. MVp in 10 years)

2) Specify a time grid - K sub-periods with time increment over the full time horizon (time increment = 6 months, 20 sub-periods)

3) Specify distributional assumptions for the key risk factors - E(Rp) & σ

4) Draw standard normal random numbers for each key risk factor over each K sub-periods (random number generator produces a distribution of random numbers from 0 to 1, all equally likely)

5) Map area under cdf (flip it?)

6) Obtain z-values to map out (approx. 1,000 runs)

7) Simulation will produce a distribution of outcomes around the point estimate of expected return at a certain time

Simple Random Sampling

*Estimation - Probability Sampling

Definition: A subset of a larger population such that each element has an equal probability of being selected

Sample size = n, 1/n probability of being selected

Useful when data are homogenous

Systematic Sampling

*Estimation - Probability Sampling

Definition: Select every Kth element until the desire sample size is reached

No logical ordering/selection process, used when the population is too large to code

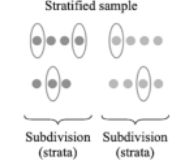

Stratified Random Sampling

*Estimation - Probability Sampling

Definition: Population is sub-divided into sub-populations based on one or more classifications. Simple random samples are drawn from each sub-population, which is pooled to form main sample

Each sub-sample is proportionate to the size of it’s sub-population, guaranteeing representation & more precision

Cluster Sampling

*Estimation - Probability Sampling

One-stage cluster sampling: Population is divided into clusters, and some of these clusters are randomly selected into your sample

Two-stage cluster sampling: Sub-samples are selected from each cluster

Cost & time efficient, but usually results in lowest precision

Sampling Error

*Estimation and Sampling

Definition: Difference between observed values of a statistic and population parameters as a result of using just a subset of the population. Deviations of sample drawn from true population

Tapers at around n=200

Non-Probability Sampling

*Estimation and Sampling

Types:

Convenience sampling - Observations are selected that are easy to obtain or accessible (ex. prof uses students)

Judgemental sampling - Select observations based on experience and knowledge (ex. auditor selectively reviewing accounts)

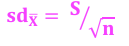

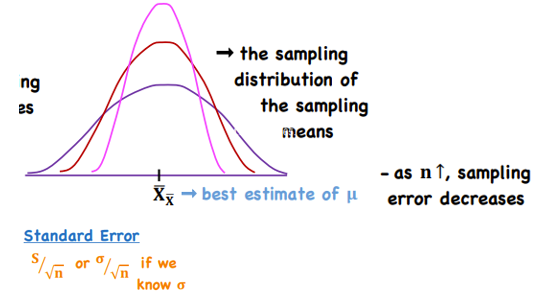

Standard Error

*Estimation and Sampling

Definition - Standard deviation of sample means around population means

Central Limit Theorem - Sampling distribution of the mean will always be normally distributed, as long as the sample size is large enough (tapers at around n=200)

z-values

60% = 1

90% = 1.64

95% = 1.96

99% = 2.58

Bootstrap Method

*Estimation - Resampling

Method - Draw 1 observation, record & replace n times to create a distribution (rather than estimating)

Uses computer simulation

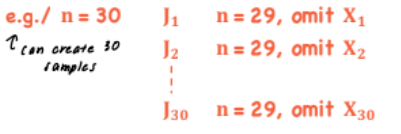

Jackknife Method

*Estimation - Resampling

Method - Omit one observation from a sample, one at a time

Will produce similar results from sample to sample

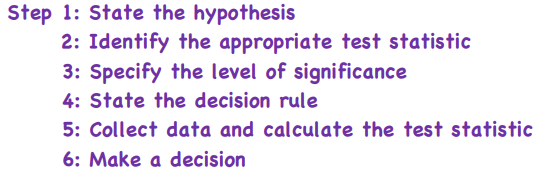

Hypothesis Testing

Test to see whether a sample statistic is likely to come from a population with the hypothesized value of the population parameter - Does X-bar = μ0?

*Typically want to reject null, and accept alternative

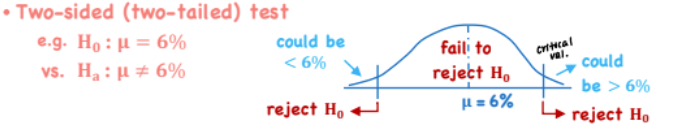

Two-sided (Two-Tailed) Test

*Hypothesis Testing

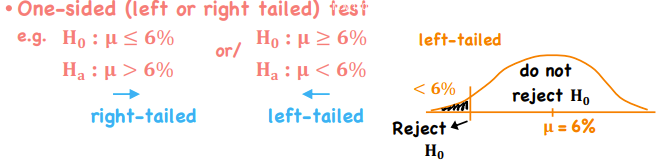

One-sided (Left-Tailed or Right-Tailed test) Test

*Hypothesis Testing

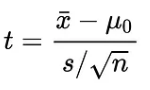

Test of a Single Mean

*Hypothesis Testing - t-Distributed Test Statistic

df = n - 1

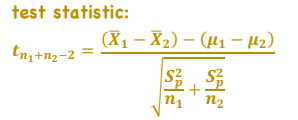

Test of the Difference in Means

*Hypothesis Testing - t-Distributed Test Statistic

Are X-bar1 and X-bar2 from the same population or different populations?

df = n1 + n2 - 2

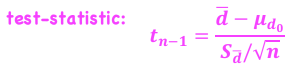

Test of the Mean of Differences (Paired-Sample t-Test)

*Hypothesis Testing - t-Distributed Test Statistic

Is the mean difference between two sets of observations 0?

df = n - 1

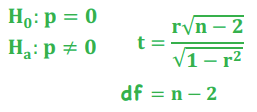

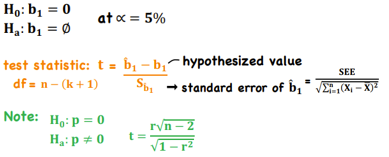

Test of a Correlation

*Hypothesis Testing - t-Distributed Test Statistic

*Parametric Test of Correlation

Is there a statistically significant correlation between two variables?

df = n - 2

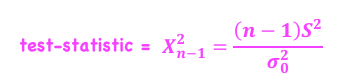

Test of a Single Variance

*Hypothesis Testing - Chi-square-Distributed Test Statistic

Is the variance of the population equal to a specific value?

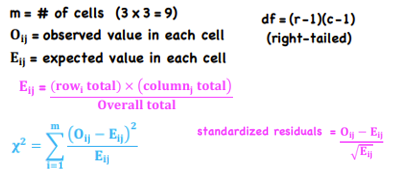

Test of Independence

*Hypothesis Testing - Chi-square-Distributed Test Statistic

*Non-Parametric Test of Independence

Categorical Data - Values that describe a quality or characteristic (nominal, ordinal)

Are these classification types independent? ex. Are growth stocks likely to be any size or are they more likely to be large-cap stocks?

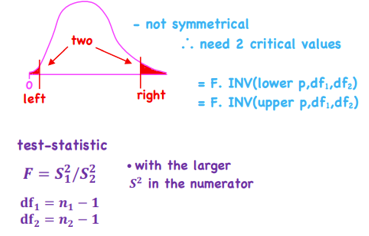

Test of the Difference in Variances

*Hypothesis Testing - F-Distributed Test Statistic

Are the variances of two populations equal? ex. Comparing the volatility of two funds

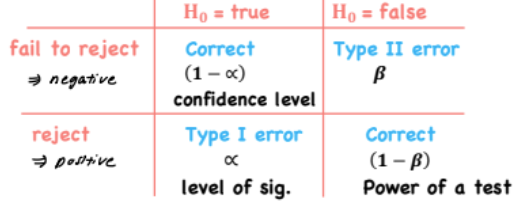

Level of Significance

*Hypothesis Testing

Alpha & beta have an inverse relationship - Only way to decrease both is by increasing n

Type I error: False positive

Type II error: False negative

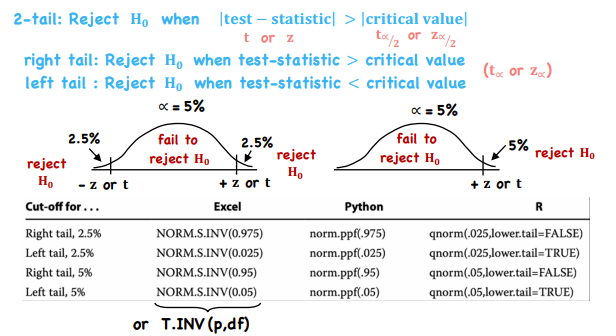

Decision Rules + Excel Formulas

*Hypothesis Testing

NORM.S.INV( ) - probability in, critical value out

NORM.S.DIST( ) - critical value in, probability out

OR

T.INV (p, df) - probability in, critical value out

T.DIST (val, df) - critical value in, probability out

Non-Parametric Testing

When data do not meet distributional assumptions (n <30), population is non-normal)

When there are outliers (test of median vs mean)

When data are given in ranks or use ordinal scale (NO IR)

Hypothesis doesn’t concern a parameter (ex. Is a sample random?)

Spearman Rank Correlation Coefficient (rs)

*Non-Parametric Test of Correlation

Definition - Essentially a correlation calculated on rank values, not on the actual values of the observation

Method:

1) Rank all X from largest to smallest (1 - n). If there’s a tie, put in an average rank

2) On original data set, calculate di2 = (rank Xi - rank Yi)2

3) Calculate rs

4) If n > 30, test rs

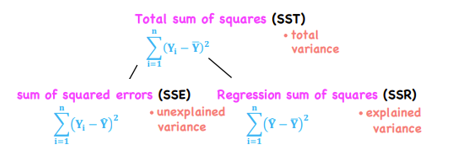

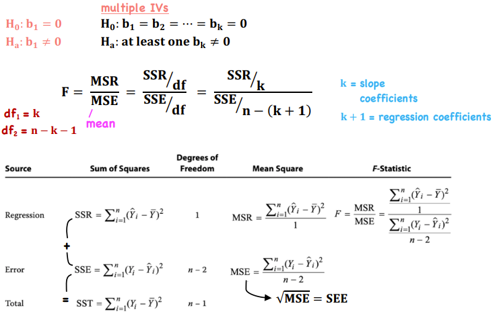

Total Sum of Squares (SST)

*Linear Regression

The sum of all squared differences between the mean of a sample and the individual values in that sample

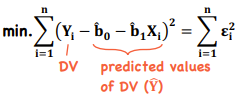

Sum of the Squares Error (SSE) or Residual Sum of Squares (RSS)

*Linear Regression

The sum of difference between observed and predicted values

Goal of regression is to compute a line of best fit that minimizes the sum of the square deviations between observed and predicted values of Y

Linear Regression (components)

Linear Regression Assumptions

*Linear Regression

1) Linearity - The relationship between X&Y is linear in the parameters b0 and b1 (IV is not random)

2) Homoscedasticity - Variance of the dependent variable is the same for all observations

3) Independence - The pairs (X,Y) are independent of each other; error term is uncorrelated across observations (no serial correlation - ability to predict likelihood of next error being +/-)

4) Normality - Error term is normally distributed

Total Sum of Squares (SST)

*Linear Regression - Analysis of Variance

SST (total SS) = SSE (unexplained SS)+ SSR (explained SS)

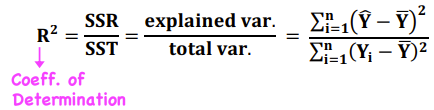

Coefficient of Determination

*Linear Regression - Analysis of Variance

Measures the fraction of the total variation in the DV that is explained by the IV (goodness of fit measure)

NOT a statistical test

Statistical Test - ANOVA test

*Linear Regression - Analysis of Variance

F-Stat Excel Function - F.INV(prob, SSR df, SSE df)

Standard Error of the Estimate/Regression (SEE) = (MSE)1/2 - The smaller the SEE, the more accurate the regression

Hypothesis Tests of b-hat1

*Linear Regression - Hypothesis Test

Test - Is it significantly different from 0?

t-stat Excel Function - T.INV (prob, n-k-1)

Hypothesis Tests of b-hat0

*Linear Regression - Hypothesis Test

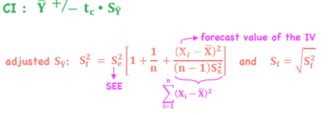

Prediction Interval for Y-hat

*Linear Regression

2 sources of error that we need to account for in the :

Y residuals

b-hat0 and b-hat1 are estimated with error

Properties

1) The better the fit of the regression model. the lower Se2, the lower Sf2 (SE of forecast)

2) Larger n = smaller Sf2

3) The closer Xf is to X-bar = smaller Sf2

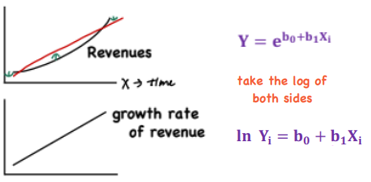

Log-Lin Model

*Linear Regression - Functional forms of the regression model

Relative change in Y for absolute change in X

Lin-Log Model

*Linear Regression - Functional forms of the regression model

Absolute change in Y for the relative change in X

Ex. Y = Percent, X = $B in Revenue

Log-Log Model

*Linear Regression - Functional forms of the regression model

Relative change in Yi for a relative change in Xi