FINANCE LEC 8: Takeovers PT 2

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

20 Terms

What is a cash bid

When the acquirer pays for the targets shares with cash

How do calculate the synergy gain, Net cost and NPV of a cash bid

Gain: Vat-(Va+Vt)

Net cost: CASH PAIDt-Market VALUEt

NPV: Gain - Net cost

What is a share/script bid

When you pay for the targets firm with shares as the currency of exchange eg. I’ll give you 3 newly issued acquirer shares in the company for every 10 of your shares.

What does Beta represent

the proportion of the new firm’s shares that are owned by the target

How do calculate the synergy gain, Net cost and NPV of a cash bid

Synergy gain: Vat-(Va+Vt)

Net cost: bxVat - Market valueT

NPV: gain - net cost

What is the stock exchange ratio and how do you find the maximum exchange ratio

The number of acquirer shares that the target shareholders receive for each target share. eg. 3:10.

Find b, when you let NPV=0, this tells you the proportion owned by the target

then do b=proportion x acquirers shares/acquirers shares + proportion x acquirers.

What happens if the exchange ratio is too high and too low

Too high: wealth gets transferred from acquirer to target shareholders

Too low: wealth gets transferred from target to acquirers shareholders

Methods to pay for shares and their features

cash bid

what’s fixed: $ amount paid is fixed

ownership: target shareholder’s don’t own any of new company

risk: acquirer bears all the market/financial risk risk pre-closing and operational risk after closing

Fixed share bid

what’s fixed: share count of acquirer’s shares is fixed, even though $value may change. eg. we will give you 3 shares for every 10 of your shares

Ownership: proportional ownership fixed at announcement

risk: both parties share pre-closing market risk and post closing operational risk in proportion to ownership

Fixed value bid

where the value of acquirer shares is fixed not the share count. the share count is set using prevailing share price.

Ownership: proportional ownership unresolved until closing cuz that decides number of shares

risk: pre closing risk beared by acquirer (ie. if sp drops they have to issue more shares), post clsoing operational risk shares

Collars, floors and ceilings: assuming fixed count

Collar: between $53 and $71.73

Floors: protection for target is SP drops too low, ie. if share price drops to 50, instead they only have to give (53/50)=1.06 shares to target

ceilings: protection for acquirer, is SP is too high, ie. share price rises to $74, they instead have to give (71.73/74)=0.969 shares to target instead of 1

Order of finding ratios

they tell you EPS

Earnings

market cap/number of shares

Share price (MV/no.shares)

P/E ratio

Calculation of new P/E ratio

(P/Ebidder * earningsB/earnings BT)+(P/Etarget * earningsT/earningsBT)

What is EPS bootstrapping

when a higher p/e ratio firm acquriers a lower pe ratio firm to boost eps even though with no real gains, no value can be created.

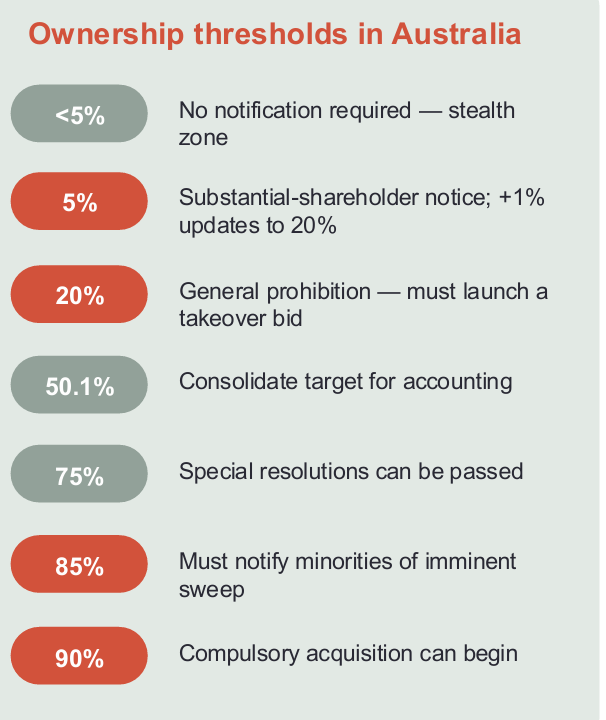

ownership thresholds

How to launch takeover bid after 20% wall

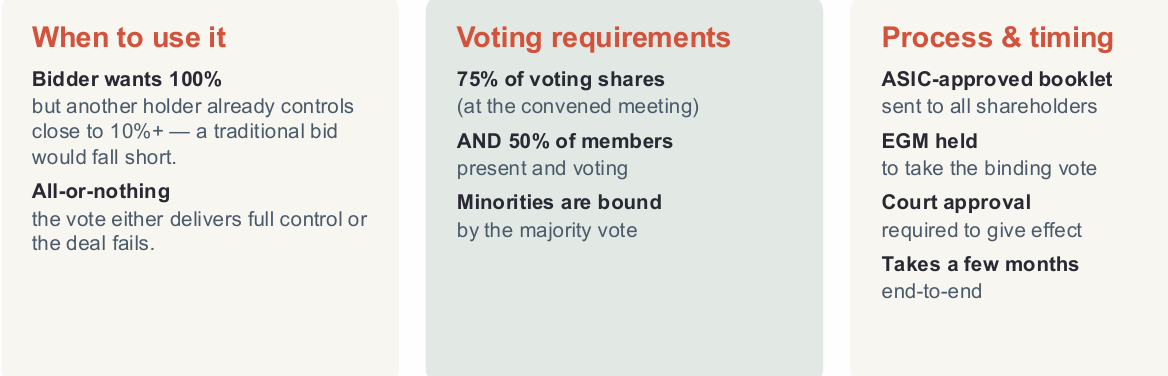

scheme of arrangement

What is the takeover panel

Bc target management can try issue lots of lawsuits to slow down takeover process that would normally take long to process in court there is a creation of a special takeover panel to assist in lawsuits filed by signficant shareholders, targets, acquirers, ASIC. the takeover panel can force or restrict the sale of shares.

Types of responses to takeovers

Friendly:

target and acquirer approve

So acquirer makes public offer, target accepts, shareholders vote yes

Hostile

target and acquirer in disapproval

Acquirer can still try acquire firm

buy buying 20% of shares then pusuing thru three methods

or do a proxy fight where the get on board or convince investors to get ppl on the board who would vote yes for takeover

Defenses to takeovers

poison pill

illegal in Australia

but when acquirer ownership passes certain threshold, target may be allowed to issue rights in order to dilute their ownership and voting rights making takeover more expensive

Staggered board

only 1/3 of leadership able to be replaced in a give year to slow down takeover and allow target to benefit from other defenses

Golden parachutes

lucrative payouts attached if senior execs are replaced after takeover can deter takeover

White knight

getting acquired by friendlier target

White squire

getting acquired by large shareholder

Directors fidiciary duties

must express their position/rec. ie. accept/reject takeover

can’t frustrate bid

takeover panel can strike down frustrating tactics

Do takeovers create value

target yes, bidder generally no, in general uncertain cuz they are expensive, impose discipline on target management but can have synergy gains