Eco 231 - Exam 2 Questions

1/47

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

48 Terms

Prediction Equation (3 independent variables)

y(hat) = b0 + b1X1 + b2X2 + b3X3

F-test for overall fit in multiple regression

checks whether the model explains variation in the dependent variable

F=MSE/MSR

Implication of the F-test for a multiple regression

Reject H₀:

→ Statistically significant

→ At least one predictor variable is useful in explaining YFail to reject H₀:

→Not better prediction than the mean of Y alone

Null and alternate hypothesis for regression with 4 independent variables

Equation:

Y=b0+b1X1+b2X2+b3X3+b4X4+ei

Null hypothesis (H₀):

H0 = β1=β2=β3=B4=0

→ None of the independent variables explain Y

Alternative hypothesis (H₁):

At least one βi≠0

→ At least one independent variable helps explain Y

F-stat formula explaination

MSR (Mean Square Regression)

Measures how much variation in the dependent variable is explained by the model.MSE (Mean Square Error)

Measures the unexplained variation (the residual/error).If F is large → the model explains significantly more variation than noise → predictors are useful

If F is close to 1 → model is not much better than random noise

A large F-statistic (with a small p-value) leads you to reject H₀, meaning the model is statistically significant overall.

Look at P-value

Polynomial Regression

How do we interpret the coefficient on a quadratic variable in a regression?

Curve Direction

b2>0 → upward (U)

b2<0 → downward (n)

Marginal effect is not constant

Turning point

If b2>0 → min

If b2<0 → max

What is the logarithm transformation of the x and y variables?

The % change in y for every 1% change in x

What does the coefficient on the x variable tell us after a log-log transformation of both the x and y variables?

the elasticity

What is an indicator/dummy variable

variable that replaces a qualitative value

difference in the predicted outcome between the group coded as 1 and the group coded as 0

When there are m different groups in the data for an independent variable, how many dummy variables are needed to indicate the m groups?

one less than m

What does the coefficient on a dummy variable tell us in a regression model?

The average difference in Y between the group with D=1 and the group with D=0

If β1>0 → the “1” group has a higher outcome than the baseline

If β1<0 → the “1” group has a lower outcome

If β1=0 → no difference between groups

Can you show the difference using graphs?

Lower line = baseline group d=0

Upper line = dummy variable d=1

Vertical distance between lines =b1

What is an interaction term in a regression?

The effect of one variable on the outcome depends on the level of another variable.

The impact of X, changes when Z changes

What does the coefficient on the interaction of a dummy variable and an independent variable (x) tell us?

Y=β0+β1X+β2Z+β3(X⋅Z)+ϵ

X⋅Z is the interaction term

β3 tells you how the effect of X changes with Z

Can you show the difference using graphs?

When Z=0:

Y=β0+β1X

When Z=1:

Y=(β0+β2)+(β1+β3)X

The intercept is different (shift up/down)

The slope is also different (lines are not parallel)

The difference in slopes is caused by the interaction term β3

How is adjusted R-square different from R-square?

R-squared

Measures the percentage of variation in Y explained by the model

R2 always increases (or stays the same) when you add more variables

Adjusted R-Squared

Used when you have to compare 2 regressions

Adjusts R2 for the # of independent variables

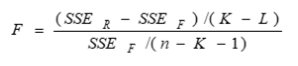

How to use adjusted R-square to compare reduced vs. full model in regression analysis?

SSEr and SSEf are the error sum of squares for the reduced and full model

K and L are the number of independent variables in the full and reduced models

What other criteria could you use for model selection?

stepwise regression

begin with a simple regression then add more independent variables as controls

backward elimination method

begin with full model (F) then eliminate insignificant independent variables in reduced model (R)

How to assess linear assumptions?

Points in a straight trend are linear

How to correct for violations of linearity assumption?

Add a lagged value of the dependent variable as an explanatory variable

What are the ZINE assumptions for multiple regression models?

Zero as the expected value for ei

Independence of errors

Error values are statistically independent

Normality of errors

Error values are normally distributed for any given set of X values

Equal Variance (also called Homoscedasticity)

The probability distribution of the errors has constant variance

How to assess the assumption of constant variance?

points in straight trend are constant

Heteroscedasticity

variance of the error terms is not constant across observations

fan shape” in residual plots

makes standard errors wrong

messes up hypothesis tests and confidence intervals

How to correct heteroscedasticity?

robust standard errors

Transform dependent or independent variables

How to assess the assumption of normality for disturbance distribution?

normal probability plot should be a straight line

68% of the standardized residuals should be between -1 and 1

95% should be between -2 and 2

99% should be between -3 and 3

How to correct for violations of normality?

If the sample size is greater than 30, normality assumption is not a concern

For small sample, use Box-Cox transformation toy: yp where 0<p<1

How to assess the assumption that the disturbances are independent?

Autocorrelation of residuals in time-series data

Et = PEt-1 + Ut where 0 < p < 1

Test for first-order autocorrelation

residual analysis

Durbin-Watson test

Durbin Watson Test

Residual analysis for time series data

The d statistic for Durbin-Watson test

If residuals are uncorrelated, d = 2

If residuals are positively correlated, d <2

If residuals are negatively correlated, d> 2

How to correct violations of independence or autoregressive errors?

Add a lagged value of the dependent variable as an explanatory variable

What is correlation matrix?

are the pairwise correlations greater than 0.5?

How to deal with collinearity problem in regression?

The presence of a high degree of multicolinearityamong explanatory variables can cause:

insignificant coefficients on independent variables

unstable regression coefficients

Detecting multicollinearity

Correlation matrix: are pairwise correlations greater than 0.5?

Large F statistic for regression but small t statistics (low p value) for estimated coefficient

Correction for multicollinearity

Remove those variables that are highly correlated with others

How to detect outliers?

use standardized deviation (ef), focusing on those with a value greater than 2

How to correct outlier problem?

Transformations:

log(X) or log(Y)

Robust regression

What are the four components in a time series dataset?

Trend component (T)

Seasonal component (S)

Cyclical component (C)

Irregular component (R)

How do you identify them?

Trend

overall pattern

Seasonal

part of the variation that fluctuates in a stable way over time

Cyclical

regular cycles in the data with periods longer than one year

Irregular

part of the data not explained by the model

Smoothing Method

smooth away” the rapid fluctuations and capture the underlying behavior

recent behavior is a good indicator of behavior in the near future

Smoothing out fluctuations is generally accomplished by averaging adjacent values in the series

Simple Moving Average (SMA(4))

Yt = (Yt + Yt-1 + Yt-2 +Yt-3) / 4

Yt-1(hat) = Yt(hat)

Exponential Smoothing

EMA(0.7) = Yt(hat) = 0.7Yt + 0.3Yt-1(hat)

Y1(hat) = Y1

Autoregressive model

Yt(hat) = b0 + b1Yt-1 + b2Yt-2 + b3Yt-3

How is autoregressive model different from smoothing method?

Autoregressive

uses past values of the series itself

depends on lagged values of Y

statistical model to analyze structure

Smoothing

uses past observations and forecasts

depends on weighted averages of past values

forecasting technique

Estimation equation for the autoregressive model with 3 lags

y(hat) = b0 + b1Ylag1 + b2Ylag2 + b3Ylag3

What is a multiple regression-based model for time series data with seasonal factors?

Yt=β0 + β1t + β2D1 + β3D2 + ⋯ + βkDk + ϵt

How do you represent the 4 quarters in a regression model?

Step 1: create dummy variables (3)

D1=1 if Q1, else 0

D2=1D_2 = 1D2=1 if Q2, else 0

D3=1D_3 = 1D3=1 if Q3, else 0

Step 2: Write regression model

Yt=β0+β1D1+β2D2+β3D3+ϵt

Step 3: Interpret the coefficents

β0 → mean value in Q4 (baseline)

β1\beta_1β1 → difference between Q1 and Q4

β2\beta_2β2 → difference between Q2 and Q4

β3\beta_3β3 → difference between Q3 and Q4

Step 4: What the model implies

Q4: Y=β0Y = \beta_0Y=β0

Q1: Y=β0+β1Y = \beta_0 + \beta_1Y=β0+β1

Q2: Y=β0+β2Y = \beta_0 + \beta_2Y=β0+β2

Q3: Y=β0+β3Y = \beta_0 + \beta_3Y=β0+β3

MSE

mean squared error

how well a model’s predictions match the actual data

Yt: actual value

Y(hat)t: predicted (forecasted) value

n: number of observations

(Yt−Y(hat)t): error (residual)

MAD

mean absolute difference

measure of the average size of forecast errors, without squaring them

Yt: actual value

Y(hat)t: predicted (forecasted) value

n: number of observations

∣Yt−Y(hat)tl: absolute error (ignores sign)

MAPE

mean average percentage error

measures forecast accuracy as a percentage

makes it easy to interpret across different scales

Yt: actual value

Y(hat)t: forecasted value

n: number of observations

The fraction = percentage error for each observation

How do you choose the best forecasting model?

MAE → average absolute mistake

MSE → penalizes large errors more

MAPE → percentage error

The lower, the better