Opportunity Fund Final Flashcards

1/238

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

239 Terms

Auditors Report

Where an auditor gives their opinion on if a company’s statements gives a fair and accurate depiction of its financial and operating results

Auditor

an accounting specialist who examines financial statements and records and attests to their accuracy and validity

The Big Three Core Financial Statements

Income Statement, Balance Sheet, Statement of Cash Flows

Gross Profit

Revenue-COGS

Gross Profit Margin

Gross Profit/ Revenue

Operating Income

Total Rev.-Direct Cost-Indirect cost

Gross Profit-Operating Expenses

Net Earnings+Interest Expense+Tax

Operating Margin

Operating Profit/ Revenue

Net Interest Expense

Interest Income-Interest Expense

Pre-tax margin

pre-tax income/ revenue

Net Income

Revenue-Total Expenses

Net Income Before Taxes - Income Taxes

Net Margin

Net Income/ Revenue

Time Value of Money consists of four beliefs

Investment risk is important

Money today is worth more than money tomorrow

Inflation must be considered when making investment decisions

investment opportunities costs must be considered

GDP Equation

Consumption + Investment + Government +Net Exports (Exports-Imports)

Macroeconomics Investors Focus on primarily:

national output

unemployment

inflation

interest rates

consumer spending/ confidence

government and trade balances - Deficits

Foreign Exchange Rates

Elasticity of Demand

Measures how quantity demanded responds to price changes.

Veblen goods

are a type of luxury good for which demand increases as the price increases, contrary to typical demand behavior. They are often associated with higher status and prestige.

Geffen good

is a type of inferior good for which demand increases as income decreases, showing an exception to the normal demand law.

What is a Stock?

a legal document representing ownership in a company

What is a stock market?

a marketplace where shares of publicly traded companies are bought and sold

What are the two sources of capital?

The two sources of capital are debt and equity, representing borrowed funds and funds raised from owners or investors, respectively.

How frequently can the income statement be prepared?

An income statement can be prepared quarterly or annually, depending on the reporting requirements of the business.

Cash Accounting

A method of accounting where revenues and expenses are recorded when cash is actually received or paid, as opposed to when they are incurred.

Accrual Accounting

A method of accounting where revenues and expenses are recorded when they are earned or incurred, regardless of when cash is actually received or paid.

Gross Margin

the percentage of total sales revenue that the company retains after incurring the direct costs associated with producing the goods and service it sells

on the Income Statement

Gross Margin Calculation:

(Gross Profit/ Revenue)x 100

Operating Margin (EBIT Margin)

Indicates how much of each dollar of revenue remains after accounting for both cost of goods sold and operating expenses. It measures a company’s operational efficency and pricing strategy

on the income statement

EBITDA Margin

shows the percentage of earnings before interest, taxes, depreciation, and amortization in relation to total revenue. It provides insight into a company’s operational performance without the impacts of financing and accounting decisions

EBITDA Margin Equation:

EBITDA/ Revenue x 100

Net Margin (Profit Margin)

Reflects the percentage of revenue that remains as net income after deducting all expenses, taxes, and interest. It measures the overall profitability of a company

Net Margin Equation

Net income/ revenue x 100

Free Cash Flow Margin

Measures the percentage of revenue that is converted into free cash flow. It indicates how efficiently a company generates cash from its operating activities.

Free Cash Flow Margin Equation

Free Cash flow/ revenue x 100

Balance Sheet

shows how much it has, what it owes, and what’s left for the owners. It is a snapshot in time that shows what a company owns and owes at that moment.

Total Assets=Total liability+ Shareholders’ equity

Goodwill

the extra amount paid when buying a company based off of value of brand, customers, or reputation. Goodwill can’t be created internally. Only recorded when a business is acquired

Goodwill formula

Goodwill= Purchase price - Net Identifiable assets

Short- term debt consists of:

Bank Loans

Commercial Paper

Credit Line

Revolver

Bank Loans

a type of short-term debt provided by banks, typically requiring repayment within one year, often used for working capital or immediate financial needs.

Commercial Paper

A short-term unsecured debt instrument used by corporations to raise funds, typically maturing in less than a year.

Credit Line

A flexible loan option that allows borrowers to access funds up to a specified limit, typically used for short-term financing needs and requiring repayment over a short period.

Revolver

A type of credit facility that allows borrowers to withdraw, repay, and withdraw again up to a maximum limit within a specified period. It is commonly used for managing cash flow fluctuations.

Working Capital

Working Capital = Current Assets - Current Liabilities

Long-term Debt

Corporate Bonds

Term loan

LT Line of credit

Property mortgages

Corporate Bonds

A type of debt security issued by corporations to raise capital, where investors receive periodic interest payments and repayment of the principal at maturity.

Term Loan

A loan from a financial institution for a specific amount that has a specified repayment schedule and a fixed or variable interest rate, typically used for purchasing assets or funding operations.

LT Line of Credit

A credit facility allowing access to a specified amount of funds by a borrower, usually on a revolving basis, to meet short-term financial needs.

Property Mortgage

A loan secured by real estate, typically used to purchase residential or commercial property, where the property serves as collateral for the loan.

Retained Earnings

cumulative profits not paid out in dividends

Net Identifiable Assets

All the assets you can see and measure, minus the liabilities

IRR (internal rate of return)

The discount rate that makes the net present value of cash flows from an investment equal to zero, indicating its profitability.

EVA (Economic Value Added)

A measure of a company's financial performance that shows the net profit after deducting the cost of capital, reflecting the value created for shareholders.

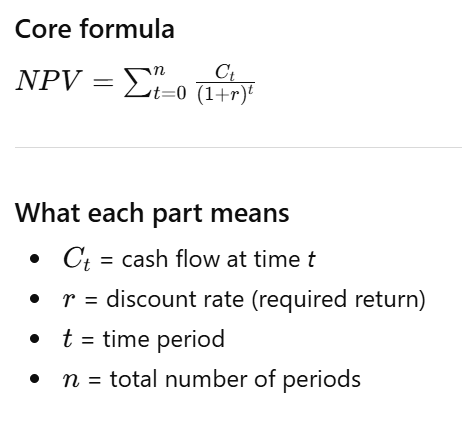

NPV (Net Present Value)

The difference between the present value of cash inflows and outflows over a period of time, used to assess the profitability of an investment.

ROIC (Return on Invested Capital)

A financial metric used to measure the efficiency of a company in allocating capital to profitable investments, calculated as the ratio of net income to invested capital.

ROI (Return on Investment)

(Return on Investment) is a measure used to evaluate the efficiency or profitability of an investment, calculated as the ratio of net profit to the initial cost of the investment.

IRR Equation (%):

(Future Value (FV)^(1/periods)/ Present Value (PV)) - 1

EVA

NOPAT-(WACC*capital invested)

NOPAT: Net Operating Profit After Tax

WACC: Weighted Average Cost of Capital

NPV Formula

ROIC formula

NOPAT/ Average Invested Capital

ROI Formula

Net Return/ Cost of Investment

10K includes five distinct sections:

Business Overview, Risk Factors, Management Discussion and Analysis, Financial Statements, and Notes to Financial Statements.

Equity Research

The process of analyzing a company's financials and performance to determine its value and potential investment merits. This often includes assessing market conditions, financial models, and competitive positioning.

What do Equity Researchers Do?

they look deep into:

Company financials

market trends

industry performance

management quality

then write detailed reports with investment advice

Research Report

A typical equity research report includes

company overview

financial analysis

valuation models (like DCF, P/E)

Price target

Recommendation (Buy/ Sell/ Hold)

Buy side versus sell side

Sell Side (brokerage firms)

publish reports for clients

influence trading volume

Buy-side (mutual funds, AMC’s)

do private research for internal investment decisions

Which accounting principle requires that expenses be recorded in the same accounting period as the related revenues they help generate?

Matching Principle

Cash Flow Statement

A financial statement that summarizes the amount of cash and cash equivalents entering and leaving a company. It provides insights into the company's liquidity, operational efficiency, and financial health by detailing cash flows from operating, investing, and financing activities.

What is the purpose of a cash flow statement?

The purpose of a cash flow statement is to provide a detailed picture of what happened to a business’s cash during a specified period, known as the accounting period. It demonstrates an organization’s ability to operate in the short and long term, based on how much cash is flowing into and out of the business.

Cash flow statement broken into three sections:

Operating, investing, and financing activities.

Operating Activites

operating activities detail cash flow that’s generated once the company delivers its regular goods or services and includes both revenue and expenses

Investment Activites

investment activities include cash flow from purchasing or selling assets— think physical property, such as real estate or vehicles, and non-physical property like patents— using free cash, not debt

Financing Activites

Financing activities detail cash flow from both debt and equity financing

Positive Cash Flow

indicates that a company has more money flowing into the business than out of it over a specified period. This is an ideal situation to be in because having an excess of cash allows the company to reinvest in itself and its shareholders, settle debt payments, and find new ways to grow the business

does not neccesarily trranslate to profit.

Negative Cash Flow

Having negative cash flow means your cash outflow is higher than your cash inflow during a period, but it doesn’t necessarily mean profit is lost. Instead negative cash flow may be caused by expenditure and income mismatch, which may or may not be a bad thing

Negative cash flow can come from the decision to expand the business and invest in future growth, or the decline in the underlying business. Given that, it’s critical to not make a knee-jerk assumption one way or the other.

Quick Ratio

Acct receivable+inventory/ accounts payable

EBIT

Earnings before interest and taxes

Depreciation and Amortization

D+A=DA

EBITDA

Earnings before interest, taxes, depreciation, and amortization

Return on Assets

Profit measure of choice/ asset base of choice

Return on equity

profit of choice/ shareholders equity

Debt to EBITDA

Total debt/ EBITDA

Interest Coverage Ratio (Times interest earned):

EBITDA/ Interest expense

Debt to Equity Ratio

Total debt/ Total shareholders equity

The difference between the balance of a fixed asset account and the related accumulated depreciation account is termed:

the book value

Days Sales Outstanding

(Average Accounts Receivable/ Revenue) x 365 days

Inventory Turnover Ratio

COGS/ Average Inventory

DCF

Discounted Cash Flow

helps to determine the value of an investment based on its future cash flows

the present value of expected future cash flow is arrived at by using projected discount rate

if the DCF is higher than the current cost of the investment, the opportunity could result in positive returns and may be worthwhile

companies typically use the weight average cost of capital for the discounted rate because it accounts for the rate of return expected by shareholders

a disadvantage of DCF is its reliance on estimations of future cash flows,

Okun’s Law

the inverse relationship between unemployment and GDP Growth

Inflation

Definition: A sustained increase in the general price level.

Measurement: CPI (consumer prices) or GDP deflator, which convert nominal values to real terms to separate price changes from real output.

Primary Causes:

Demand-pull: Aggregate demand grows faster than supply.

Cost-push: Rising input costs (wages, commodities).

Built-in: Expectations of future inflation lead to further increases.

Economic Effects:

Erodes real purchasing power.

Distorts relative prices and investment decisions.

Redistributes wealth between debtors and creditors (depending on whether inflation is anticipated).

Policy Response: Central banks use monetary policy (interest rates, open-market operations) to stabilize inflation, balancing the short-run tradeoff between reducing inflation and avoiding excessive output loss.

Nominal GDP

measures output at current market prices; it rises with output and price level changes

Real GDP

measures output at a constant prices (adjusted for inflation); its isolates changes in real production

GDP Deflator

is the price index that converts nominal to real GDP; when the deflator rises, nominal growth can overstate real growth

Policy relevance of Real vs. nominal GDP

Real GDP is used to assess economic growth and productivity; nominal GDP matters for tax receipts, debt ratios, and nominal income measures

What is equity analysis?

Equity analysis is the process of researching and evaluating a

company's financial health, industry position, and future

prospects to determine the PROPER value of its stock. The

primary goal of equity analysis is to determine whether to buy, sell,

or hold a particular stock. This involves a deep dive into various

aspects of a company, including its financial statements,

management quality, competitive landscape, corporate strategy,

and macroeconomic factors that might influence its performance.

By understanding these elements, analysts can form a

comprehensive view of a company's true worth, which may differ

significantly from its current market price.

Net cash balance:

all cash- all interest bearing debt

Total interest-bearing debt:

all short term debt+ all long term debt

Net working capital/ sales

same as working capital/ sales

Cash Flow to Debt Ratio

Total Debt/ Cash Flow From Operations

Operating Cash Flow Margin

Cash Flow From Operations/ Net Revenues

Free Cash Flow Yield

Free Cash Flow/ Market Capitalization

Free Cash Flow to Sales Ratio

Free Cash Flow/ Net Revenue

Free Cash Flow Conversion

Free Cash Flow/ Net Income