Microeconomics

1/130

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

131 Terms

Reflexivity Assumption

It is assumed that each bundle is at least as good as itself

Preference Symbols

Ad valorem tax and subsidy

Ad valorem means 'to add value'

An ad valorem tax means a tax is paid on a good based on its price; a subsidy implies the inverse

Budget Constraint

The budget line is given by p1x1 + p2x2 = m, which just exhausts a persons income

It has a slope of −p1/p2, a vertical intercept of m/p2, and a horizontal intercept of m/p1.

The Numeraire is when one of the variables is fixed as constant; this doesn't change the constraint (check by rearranging)

Increasing income shifts the budget line outward. Increasing the price of good 1 makes the budget line steeper. Increasing the price of good 2 makes the budget line flatter.

Pareto Efficiency

An allocation is Pareto Efficient if there is no way of making one better off without making another worse off

Equilibrium Principle

Generally, prices are determined when supply for a good meets the demand for a good

Optimisation Principle

People choose the best patterns of consumption available to them

Endogenous and Exogenous Meaning

Most simply, endogenous variables are explained and contained in a particular model whereas exogenous variables are not

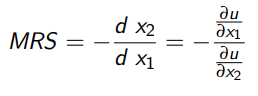

Marginal Rate of Substitution

The rate at which an agent will swap one good for another

The slope of an indifference curve

Monotonic Transformation

Utility functions are ordinal, meaning they only show an order of preference, but don't assign an actual value to preferences

If preferences are represented by numbers - coffee = 4 and tea = 5 - by adding 5 to the values the order of preference is preserved

Perfect Substitutes

An agent is completely indifferent between two goods; they seek to maximise utility regardless of which good they have

u(x,y) = x + y

Perfect Complements

When two goods are only enjoyed when consumed together; there is no point having more of one good without the other

u(x,y) = min(x,y)

Convexity Assumption

Averages are better than extremes

This works when we take a weighted average of two bundles of goods and represent it on an indifference curve; this new curve will be equal to or strictly preferred to the singular curves

Transitivity Assumption

A logical assumption which mitigates against preference cycles

There is no situation in which A > B, B > C, and C > A

Monotonicity Assumption

Assumes that more of a good is better

This simply means that in models we will only study allocations of goods before satiation occurs

Completeness Assumption

Agents are able to exhibit preferences, avoiding situations in which they can't choose between different bundles

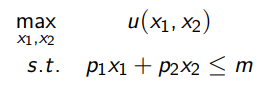

Marshallian Demand

The solution to the constrained optimisation problem in the image

This solution gives the optimum quantity given fixed income and prices x(p,m)

The Equimarginal Principle

Most utility curves are smooth and convex (Cobb-Douglas Equations)

At the optimum, the indifference curve and budget constraint will be tangent at the optimum, giving the equimarginal condition

Find the marginal utility by differentiating a utility function with respect to one of the arguments, then set the ratio of the marginal utilities equal to the ratio of the prices

MUx1/MUx2 = x2/x1, x2/x1 = p1/p2

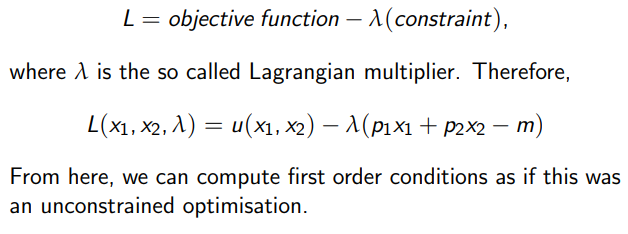

The Lagrange Method

Revealed Preference

In a situation where there are two goods available and one chooses A over B, we can say that A is revealed preferred to B

Weak Axiom of Revealed Preference

If a person chooses x over y at some prices p when both are affordable, we can never reverse the choice at any other price in which both are affordable

Thus, something consists with the weak axiom of revealed preference if someone has a strict preference of one good over another

Strong Axiom of Revealed Preference

Adds a condition to the weak axiom which ensures that transitivity is respected

If A is revealed preferred to B, and B is revealed preferred to C, then C can not be revealed preferred to A (this event would be lots of curves crossing each other)

Optimal choices for concave preferences

Concave preferences imply a person doesn’t want to buy two goods together (like olives and ice cream; if they have ice cream they DON'T want more olives)

Thus the solution for nonconvex preferences is always a boundary point

Shortcut for optimal choices in Cobb-Douglas

To be used instead of conducting the Lagrangian, where the Cobb-Douglas is given by u(x1,x2) = x1cx2d

It is often useful to choose Cobb-Douglas functions where the exponents sum to 1 because this means that the exponents can be interpreted as a fraction of income

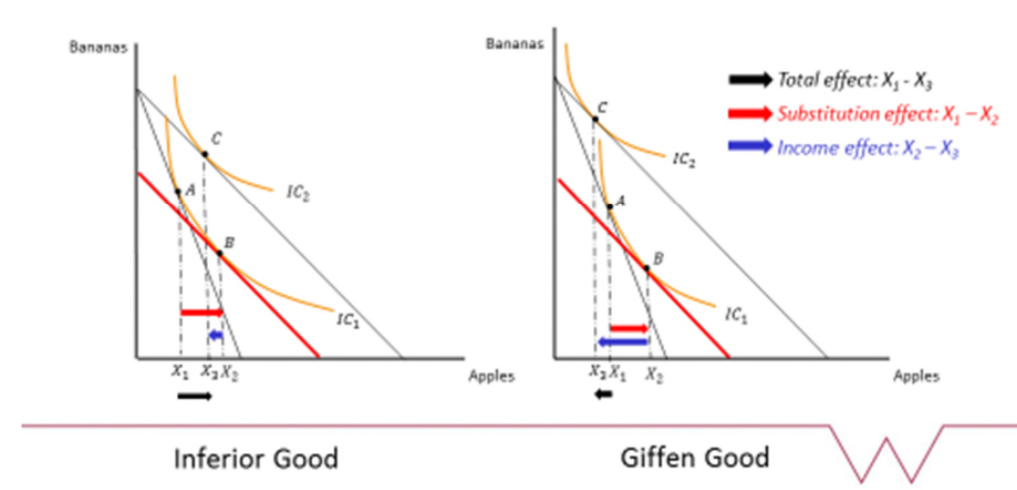

Normal good

A type of good where an increase in income will increase demand (eg cars, steaks)

dx1*/dm > 0

Inferior good

As income increase, demand for the good decreases (eg fast food)

dx1*/dm < 0

Ordinary good

Demand decreases when price increases (eg clothes)

dx1*/dp1 < 0

Giffen good

Demand increases when the price increases (watches, cars)

Often referred to as luxury goods; they are partly valued because of their price

dx1*/dp1 > 0

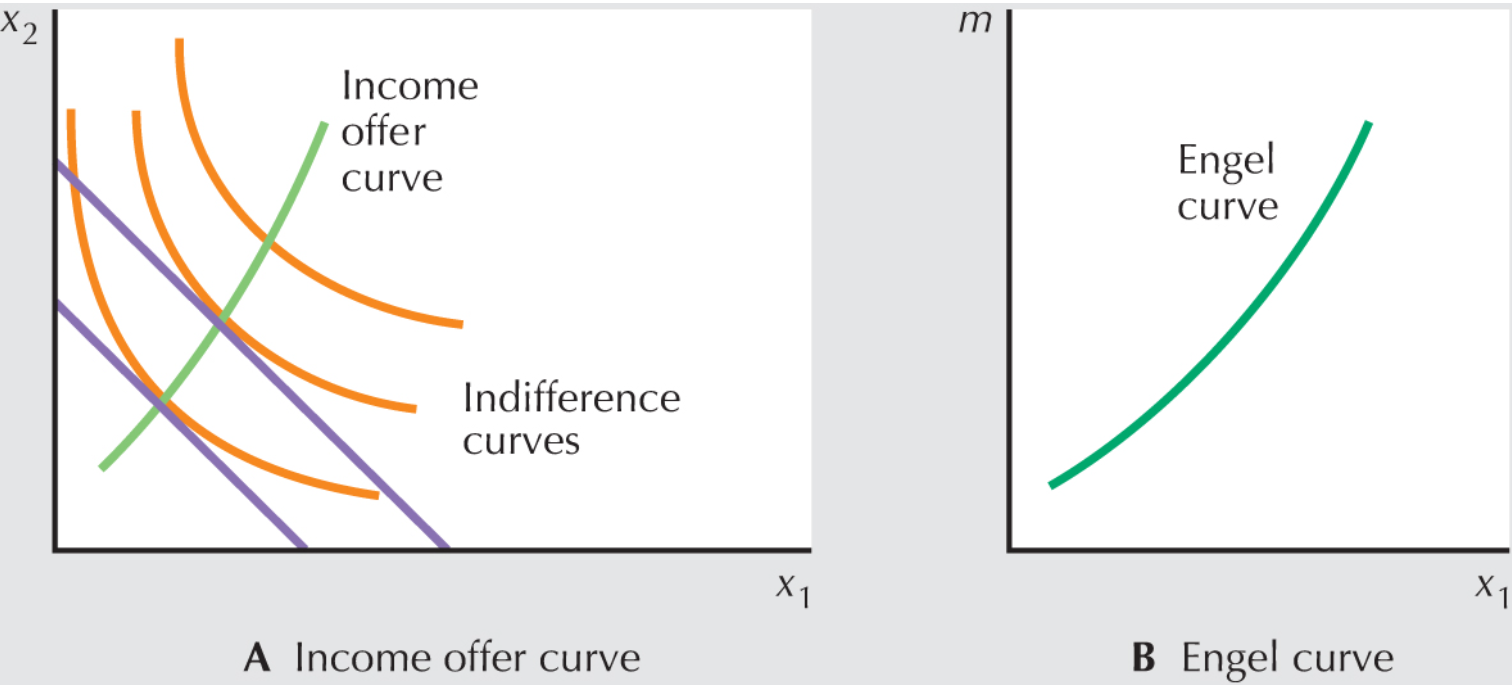

Engel Curve and Income Offer Curves

The shape of the income-offer curve is referred to as the income-expansion path; when income increases and the goods are normal, the slope will be positive

The income offer curve illustrates the bundles of goods demanded at different income levels

The Engel curve is one which shows the path of demand for a good given fixed prices

Demand Curve

Derived by plotting all of the price-demand combinations on a graph (price over demand)

Shows how one person reacts to changes in price and income

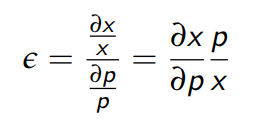

Price Elasticity of Demand

The slope of a demand function, understood as the ratio of relative changes

When the PED > 1, demand is called elastic, meaning that the demand curve is flatter (x changes a lot with price)

Constructing market demand

Summing horizontally is equivalent to fixing the price and summing the demand of different consumers

This allows one to find aggregate market demand at a particular price

Kinks can occur when one is summating market demand and a price goes above one of the consumers WTP

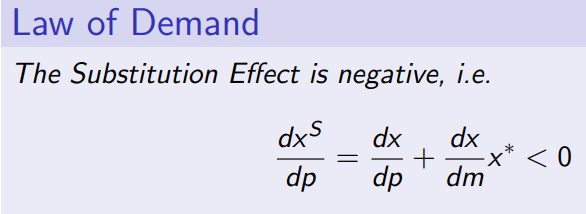

Slutsky Decomposition

Deals with the effects a price change has on demand

The first effect is the substitution effect; a person switches consumption to the other good

The second effect (income effect) involves a change in purchasing power

This separating of these two effects is called the Slutsky decomposition

Compensated Demand

Is constructed to eliminate any purchasing power (income) effect

If original prices are p1 and p2, with income m, then when prices change to p1’ and p2, the new income must be m’ to allow for purchasing the same quantities at different prices

Substitution effect

When a person shifts consumption from one good to another after a price change

The difference between the bundle x* and x’ (where x* is the original quantity demanded, and x’ is the quantity demanded after the price change)

The solution to max(x1,x2) u(x1,x2) s.t. p1’x1 + p2×2 = m’

Income effect

The loss of purchasing power caused by a price change, which is found by locating the optimal bundle at a new price and non-adjusted income

We move from x’ (adjusted demand with adjusted income) to x’’ (adjusted demand with non-adjusted income)

The income effect is the difference between x’’ and x’

The solution to max(x1,x2) u(x1,x2) s.t. p1’x1 + p2×2 = m

Graphically, this is a linear transformation of the budget constraint and indifference curve tangency

Slutsky Decomposition - Maths

Where dx/dp is the change in demand w.r.t the change in price and x*(dx/dm) is the income effect

Homothetic preferences on Engel and Income Offer curves

They will always be represented as straight lines through the origin, because any change in the quantity of bundles doesn’t change the ratio of preferences

Quasilinear indifference curves

All the indifference curves are just linear transformations of one indifference curve

We say that there is zero income effect due to an increase in income, and the Engel’s curve is a straight vertical line

The Price Offer Curve

When we change the price of one good, keeping the other fixed, the budget constraint pivots, intersecting different indifference curves at different points

These new intersections are connected through the price offer curve

Hicksian Compensated Demand

Also known as the Hicksian Subsitution Effect, this computes the optimal point by fixing utility and finding the compensated demand required to reach this utility

This implies a new solution framework; we can’t maximise the problem because we’re keeping utility fixed, so we invert it and solve in terms of expenditure minimisation instead

We minimise expenditure using the Lagrangian or Equimarginal Principle

minx1,x2 p1x1 + p2x2 , s.t. u(x1,x2) = u*, where u* is the fixed level of utility

The minimal point lies on the lowest budget line touching the indifference curve constraint

Unconstrained Optimisation

Rearrange the budget constraint to get x2 = (m-p1x1)/p2

Substitute this into the utility expression and then maximise it, solving for x1 by setting it equal to 0

Hicksian Demand Substitution Effect

We want to fix utility at its optimal level, so plug the Marshallian demands into u(x1, x2) to find the optimal utility, u*

Minimise expenditure subject to the new constraint (ie, x1x2 = u*) and compute

Solve for new optimal quantities given the price changes; take x2 from x2* to see the substitution effect

These new optimal quantities, x1* and x2* are called Hicksian Compensated Demands, subject to H(P1, P2, v), where v is the fixed level of utility

Hicksian Demand Income Effect

Simple compute the Marshallian demands of the goods at the new prices; this accounts for what expenditure will actually be like given the change in income

Hicksian Demand Total Effect

The direction of the total effect depends on what type of good it is; for a normal good, the substitution and income effect will both be positive

Compensating Variation

Fix utility before the price change and find how to adjust income to ensure the same utility after the price change

If e(p’, u(x*(p, m))) is the minimum expenditure needed to achieve the same utility at final prices, then the compensating variation, CV (p,p’,m) = |m - e(p’, u(x*(p, m)))|

Equivalent Variation

Fix utility after the price change, u(x*(p’, m))

Tries to figure out how we can adjust the income to ensure the consumer experiences the same level of utility before the price change as it does after

EV(p, p′, m) = |e(p,u(x*(p′, m))) − m|

Consumer Surplus

The net benefit we receive from consuming q units of good 1, where CS(q1) = v(q1) - p1q1

The area below the demand curve

Comparing Equivalent Variation and Compensated Variation

For a normal good, CV > EV for a price increase and vice versa for a decrease

They will only be equal for quasilinear preferences where indifference curves are parallel and there is no income effect

Computing Compensated Variation

Original budget constraint is P1*x1* + P2x2 = E1. When the price of P1 rises to P1**, the budget constraint changes with new Marshallian Demands to become P1**x1** + P2×2** = E1

We shift the second budget line out so that it becomes tangential to the original utility curve. The budget constraint becomes E2 = P1**x1*** + P2x2*** where E2 is compensated income

E2 - E1 is the compensated variation

Computing Equivalent Variation

How much money to take away from a consumer before a price change to ensure they will be just as well-off after it

Original BC is P1*x1* + P2x2* = M1

When the price P1 rises, BC pivots inwards and new BC is P1**x1** + P2x2** = M1

We must takeaway money from the consumer to ensure constant utility, so shift the original BC inwards to get the new BC P1*x1*** + P2x2*** = M2

EV = M1 - M2

How are demand functions given?

In the form, x1 = x1 (p1, p2, m), as a function of both prices and income

The Slutsky Identity (for the total change in demand)

x1(p’1, m) - x1(p1, m) = (x1(p’1, m’) - x1(p1, m) + (x1(p’1, m) - x1(p’1, m’))

This is an identity, true for all values

This could be simplified into easier symbols like; x’ - x = (x’’ - x) + (x’ - x’’), or x = xs + xi

It is the addition of the substitution and income effect respectively

What is the graphical difference between Hicksian and Slutsky substitution effect?

For the Slutksy substitution effect, the budget line pivots around the optimal point to show the effect

For the Hicksian substitution effect, the budget line doesn’t pivot around the optimal point, but instead moves around the original indifference curve to reach a point which has the same gradient as the final budget line

Thus, where Slutsky keeps purchasing power constant, Hicks keeps utility constant

What is uncertainty?

Uncertainty concerns missing information, where the link between cause and consequence, choices and outcomes, is not clear

Risk

This is where an agent knows the achievable outcomes and probabilities of achieving those outcomes rather than simple uncertainty

Expected outcomes (and utility)

Involves multiplying the outcome of a situation by the probability that it happens

Expected utility involves attaching a utility weight to an outcome; in the case of a lottery, it might look like EU(w) = p1ux1 + p2ux2, where u = utility, p = probability, EU(w) is expected utility of wealth, and x is an outcome

Certain Equivalent

This is the concept of the certain lottery which is equivalent to the risky one

This is the amount of money it would take for a person to be indifferent between the certain amount and the uncertain lottery (the ‘riskier’ choice)

u(CE) = EU(w) = pu(w1) + (1 − p)u(w2)

Risk attitudes

Risk averse | CE < E(w), EU(w) < u(E(w)) — This basically means that the expected utility of the wealth is less than the utility of actually having it; they have more utility by not taking the risky lottery

Risk neutral | CE = E(w), EU(w) = u(E(w))

Risk lover | CE > E(w), EU(w) > u(E(w))

What is Insurance?

Insurance is effectively trading risk; a person would prefer to pay some amount in the eventuality that they are faced with a bad state (lose their car, etc)

Optimal Insurance Contract

k is the amount ensured, w is the value of the insured object, A is the potential damage, á is the price per pound insured, p is the probability of the damage-causing event

Thus, expected utility maximising equation is maxkEU(k) = (1 − p) u(w − αk) + pu(w − A + (1 − α)k)

Insurance FOC

dEU(k)/dk = α(1 − p)u′(wg ) − (1 − α)pu′(wb) = 0

(1 − p) u′(wg) / pu′(wb) = (1 − α) / α

Full insurance, or constant wealth, only occurs when k = A

To make insurance optimal, we must have that p = α, to ensure a ‘fair price’

Willingness to pay and risk premium

An agent is only willing to pay the difference between wealth in the good outcome and the Certain Equivalent

The risk premium is the amount an agent is willing to pay with respect to a risk neutral person, quantified by the difference between E(w) and the Certain Equivalent

Adverse Selection

Involves the situation when two people enter a contract with asymmetric information; a risky driver who should pay a higher insurance premium tries to enjoy lower insurance prices by hiding their behaviour

This is also called a ‘hidden characteristic’ or ‘hidden information’ problem

This could lead to non-efficient outcomes or even stop trading in some markets

Moral Hazard

Occurs when someone has no incentive to mitigate risk because they’re completely insured

In the case of bicycle insurance, a person might not take any care at all if they are reimbursed completely for losing it because they have already made the investment in insurance (as opposed to investing in a really heavy and secure bike-lock)

Occurs when one side of the market can’t observe the actions of the other — a hidden action problem

Signalling

A way to try and solve the ‘lemon market’ problem; sellers can offer warranties to insure a consumer against the risk of their car being a lemon

Owners of the good cars can afford this whereas the owners of the bad cars can’t

The Incentive Compatibility Constraint

Simply states that the utility to the worker of some effort level x* must be greater than any other effort level; this effort level is the one which maximises profit for the incentiviser

Marginal cost of effort must be equal to the marginal product of effort

The incentiviser can aim to do this through many ways:

How might a landowner incentivise a worker in line with the incentive compatibility constraint?

Rent (rent the land to the worker, they keep all the profit over the amount they pay back to the owner)

Wage labour pays a person an hourly rate

Take-it-or-leave-it: the worker is paid if they work at x* and nothing else

Sharecropping is where the owner and worker both take a percentage of the product of labour

What is the independence assumption?

It is the idea that consumption patterns in one state are independent of another state; how much money I am willing to sacrifice in order to get a little more money if my house burns down should be independent of the event that my house doesn’t burn down

Thus, expected utility functions must have an additive form (like p1c1 + p2c2) to ensure that they are independent

What is expected value of wealth?

In a situation with uncertain outcomes, the expected value of wealth, or the utility of expected wealth, is given by finding the average value of the two outcomes

If we have a 50% probability of getting $5 and $15 respectively, then the expected value of wealth is the average of 5 and 15: $10

The utility of expected wealth is u($10)

This is given by ½ (5) + ½ (15) = 10

What is the expected utility of wealth?

In the situation where there are uncertain outcomes, a 50% probability of receiving $5 or $10 respectively, the expected utility of wealth is found by calculating the sum of the two expected utilities

Note that this calculates expected utilities rather than expected wealth

Given by ½ u(5) + ½ u(15)

What are the shapes of risk-averse and risk-lovers utility functions?

The risk-averse consumers utility function is concave whereas the risk-lovers graph is convex (increasing gradient)

Utility on the y-axis, wealth on the x; these different functions show that a persons preferences ‘lean’ towards the axis they value more

A pure exchange economy

Aim to describe an economy through simple concepts

We need three objects, a set of traders, preferences, and resources (each agent is given some endowment)

Generally we’ll use the simple framework of two agents and two goods

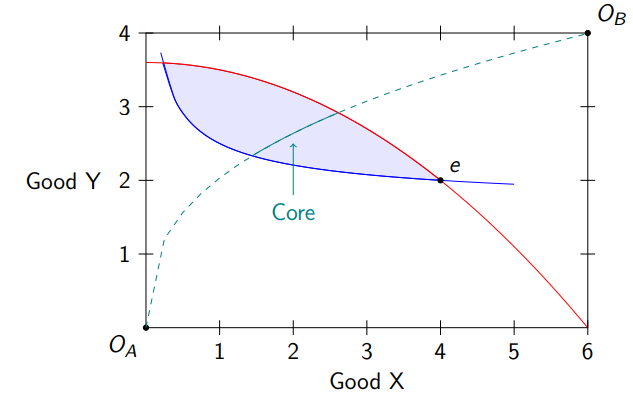

The Edgeworth Box

Consists of fitting the different indifference curves of the different agents into the same graph, from opposite origins, where the sizes of the edges represent the total resources in the economy

There are equilibrium trades where the indifference curves intersect

The contract curve

Is on the same Edgeworth box as the other utility curves, and is the set of all possible Pareto efficient allocations

The set of Pareto efficient allocations which improve upon the original endowment is called the core

Allocation in competitive markets

The main mechanism for allocation is price, meaning individuals simply maximise where their income is the value of their endowment (endowment is valued in monetary terms)

A competitive equilibrium occurs when there is an allocation that maximises each person’s utility at a set of prices (they are price-takers) and the market clears

On the Edgeworth box, the difference between the original equilibrium and the competitive equilibrium can be conceived of in terms of an agents excess supply and excess demand

What is the first fundamental theorem of welfare?

Competitive equilibrium allocations are Pareto Efficient

Requires some monotonicity of preferences as an assumption

This tells us that a competitive economy will end up at some point on the contract curve; a lump sum transfer is a way of transferring money to change the initial endowment and end up on a better place on the contract curve

What is the second fundamental welfare theorem?

For each efficient allocation on the contract curve, there is a price that supports it as a competitive equilibrium

The results requires convexity of preferences and tells us what we can achieve with redistribution

Every point on the contract curve can be reached through decentralised trade

What are political implications of the welfare theorems?

Markets can produce good results

Perfectly competitive markets provide the benchmark

Government redistribution can help ease ethical concern within the market

The second theorem and lump sum transfers

The second theorem assumes we can do lump sum (costless and immediate) transfers (presumably done by the government through taxation)

This taxation can still lead to an equilibrium market outcome so long as the thing being taxed can be measured or can’t be changed (taxing people with blue eyes’ endowment and giving it to people with brown eyes. Or, taking from people with High IQ’s endowment and redistributing it to lower IQ endowments)

This works because we recognise that all trades which occur from initial endowments will result in a Pareto efficient market equilibrium

Situations in which markets are inefficient

Market power: there are agents big enough to be price-makers rather than price-takers

Externalities, where one individuals welfare depends on the consumption of others

If information is incomplete, trading might be obstacled leading to inefficiency

The pricing of public goods by private sectors doesn’t result in efficient allocation

What is gross demand?

Gross demand is the total amount of a good that a person wants to consume at the going price

What is net demand?

This is the difference between gross (total) demand and the initial endowment they already have

It is how much the consumer needs to buy of the good to satisfy their demand of the good

What is Walras’ Law?

It is a condition which specifies that in equilibrium, the value of the aggregate excess demand in an economy is identically equal to 0

p1z1(p1, p2) + p2z2(p1, p2) = 0

This identity means that the value of aggregate excess demand is necessarily 0 for all prices, not just those in equilibrium; it is stronger than necessary

Relative prices

Walras’ law demonstrates that in a market with k goods, we only need to find prices for which k-1 markets are in equilibrium; the kth market will necessarily be in equilibrium

It seems that we are unable to solve for the final price because we have k goods and only k-1 equations, but this is because the k-1 equations are only solving for independent prices

Thus we need to fix a price as constant so that all other prices can be measured relative to it

What is Arrows’ Impossibility Theorem?

If a social mechanism satisfies certain properties (1. the decision mechanism should be complete, transitive, and reflexive, 2. everyone should rank x ahead of y if everybody prefers x to y and 3. that preferences between x and y should depend only on how people rank x versus y and not on other preferences) then this social decision-making mechanism is a dictatorship

This just means that this mechanism for choosing between pareto efficient outcomes resembles the preferences of just one person, not many

If we want to aggregate social preferences whilst maintaining democracy, we will have to give up one of the three properties that are listed in Arrow’s impossibility theorem

When is an allocation equitable?

An allocation is equitable when a person doesn’t prefer any bundle over their own allocation

To desire another persons bundle is to envy it

We say that if an allocation is equitable and pareto efficient, then it is a fair allocation

Why does a market fail?

Due to agents not being price-takers, the market is unable to arrive at efficient outcome due to the pricing mechanism

Simple monopoly model

A single firm with a cost structure c(q) is facing an inverse demand curve p(q)

The firm maximises p and q for π(p,q) = pq - c(q) s.t p = p(q)

By incorporating the constraint, one can just maximise π(q) = p(q)q - c(q)

The solution to this gives the marginal revenue, equal to the marginal cost, which is dc(q)/dp

This leads to a deadweight loss in the market

What is a game?

Requires a set of players, sets of strategies, timing, information, and payoffs

A game has these features

What types of games are there?

Cooperative and non-cooperative games

Simultaneous and sequential games

Complete information and incomplete information

We might also include one-shot and continuous games

What is normal form?

The simplest way of representing a game and its outcomes

What is a dominant strategy?

A strategy which is best for one player regardless of what their opponent chooses

Nash Equilibrium

When players play their mutual best responses

It also requires the absence of regrets; upon knowing what your opponent is doing you do not change your mind

Entry deterrence

Suppose a sequential game where a firm is enjoying a monopoly

Another firm wants to enter the market; the firm in monopoly might decide to react heavily or lightly to this; they might perform an action which doesn’t provide them with the greatest monetary value but it discourages others from entering the market

In sequential games, games are represented by trees

Strategies in sequential games

A strategy is redefined as the set of actions a person undertakes at every node

This means that in the sequential game, where the second player responds to the first, although the first only makes one decision, the second persons best strategy is to act conditionally on the first

This allows for an expanded normal form

A non-credible threat

A threat of adopting a particular strategy which has no weight because the actor would want to deviate from it once it gets to their turn in the game

What is a subgame?

It is a part of sequential games and can standalone as its own game; it has well defined players, strategies, payoffs etc

These games can have their own Nash equilibria — subgame perfect nash equilibria

What is subgame perfect nash equilibrium?

The set of strategies which constitutes a nash equilibrium in all the subgames

To compute this we use backwards induction, which involves deciding what the first player will choose given the decisions of the subsequent players