Microeconomics

1/196

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

197 Terms

Principles 1-10

Fundamental concepts that guide economic decision-making, including scarcity, opportunity cost, and marginal analysis.

People face trade-offs

the cost of something is what you give up to get it

Rational people think at the margin

People respond to incentives

Trade can make everyone better off

Markets are usually a good way to organize economic activity

Governments can sometimes improve market outcomes

A country’s standard of living depends on its ability to produce goods and services

Prices rise when the government prints too much money

Society faces a short-run trade-off between inflation and unemployment

trade-offs

when making a decision, a person must give up something to get or do something

ex. “guns and butter“- more a society spends on the military, less it can spend on consumer goods

clean environment and level of income- regulation of firms for a cleaner environment and improved health makes it more likely that firms will earn smaller profits, pay lower wages, and charge higher prices

-social trade-off between efficiency and equality

opportunity cost

whatever must be given up to obtain some item

marginal decision-making

making decisions that consider marginal change- incremental adjustments to an existing plan

-rational people make decisions by comparing marginal benefits and marginal costs

-a rational decision maker takes an action if and only if the action’s marginal benefit exceeds its marginal cost

the role of incentives

an incentive is something that induces a person to act

-people respond to incentives by comparing costs and benefits

Adam Smith and the invisible hand

made the most famous observation in all of economics: firms and households in competitive markets acts as if they are guided by an “invisible hand“ that leads them to desirable outcomes

-directs economic activity

scarcity

the limited nature of society’s resources

economics

the study of how society manages its scarce resources

efficiency

the property of society getting the most it can from its scarce resources

equality

the property of distributing economic prosperity uniformly among the members of society

opportunity cost

whatever must be given up to obtain some item

rational people

people who systematically and purposefully do the best they can to achieve their objectives

marginal change

an incremental adjustment to a plan of action

incentive

something that induces a person to act

market economy

an economy that allocates resources through the decentralized decisions of many firms and households as they interact in markets for goods and services

property rights

the ability of an individual to own and exercise control over scarce resources

market failure

a situation in which a market left on its own does not allocate resources efficiently

externality

the impact of one person’s actions on the well-being of a bystander

market power

the ability of a single economic actor (or small group of actors) to have a substantial influence on market prices

productivity

the quantity of goods and services produced from each unit of labor input

inflation

an increase in the overall level of prices in the economy

business cycle

fluctuations in economic activity, such as employment and production

Economics is best defined as the study of _______.

how society manages its scarce resources

Your opportunity cost of going to a movie is _______.

the total cash expenditure needed to go to the movie plus the value of your time

A marginal change is one that _______.

incrementally alters an existing plan

Because people respond to incentives, _______.

-policymakers can alter outcomes by changing punishments or rewards

-policies can have unintended consequences

-society faces a trade-off between efficiency and equality

International trade benefits a nation when _______.

all nations are specializing in producing what they do best

Adam Smith's "invisible hand" refers to _______.

the ability of free markets to reach desirable outcomes, despite the self-interest of market participants

Governments may intervene in a market economy in order to _______.

-protect property right

-correct a market failure due to externalities

-achieve a more equal distribution of income

The main reason that some nations have higher average living standards than others is that _______.

some nations have higher levels of productivity

If a nation has high and persistent inflation, the most likely explanation is _______.

the government creating excessive amounts of money

If a government uses the tools of monetary policy to reduce the demand for goods and services, the likely result is ________ inflation and ________ unemployment in the short run.

lower; higher

the two roles of economists

scientists: try to explain the world

policy advisors: try to improve it

the role of assumptions

simplify the complex world and make it easier to understand

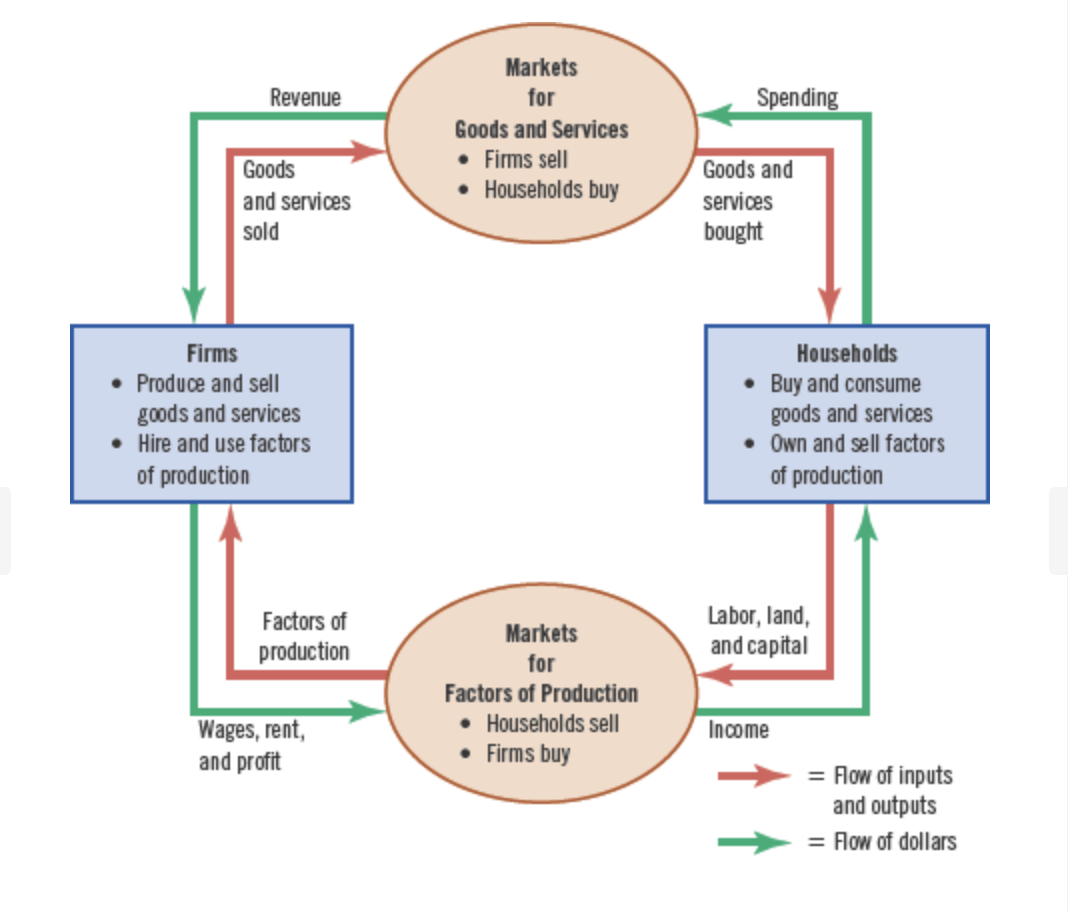

Circular Flow Model

a visual model of the economy that shows how dollars flow through markets among households and firms

Production Possibility Frontier (PPF)

a graph that shows the combinations of output that the economy can possibly produce with the available factors of production and production technology

efficient/inefficient

efficient: economy getting all it can from the scarce resources it has available (points on the PPF)

inefficient: under the PPF

feasible/not feasible

feasible: on or inside PPF

not feasible: points outside PPF

slope represents tradeoff

slope of PPF represents tradeoff of opportunity cost

constant opportunity cost vs. increasing opportunity cost

constant opportunity: a straight downward sloping line

increasing opportunity: bowed- out line- trade-off worsens as you produce more of a good

normative vs. positive statements

normative: claims that attempt to prescribe how the world should be

positive: claims that attempt to describe the world as it is

microeconomics vs. macroeconomics

microeconomics: the study of how households and firms make decisions and how they interact in markets

macroeconomics: the study of economy-wide phenomena, including inflation, unemployment, and economic growth

why economists disagree

Economists may disagree about the validity of alternative positive theories of how the world works.

Economists may have different values and, therefore, different normative views about what government policy should aim to accomplish.

An economic model is _______.

a simplified representation of some aspect of the economy

The circular-flow diagram illustrates that, in markets for the factors of production, _______.

households are sellers, and firms are buyers

A point inside the production possibilities frontier is _______.

feasible but not efficient

All of the following topics fall within the study of microeconomics except _______.

the influence of the government budget deficit on economic growth

Which of the following is a positive, rather than a normative, statement?

Law X will reduce national income.

The following parts of government regularly rely on the advice of economists: _______.

Department of Treasury

Office of Management and Budget

Department of Justice

Economists may disagree because they have different _______.

hunches about the validity of alternative theories

judgments about the size of key parameters

political philosophies about the goals of public policy

Most economists believe that tariffs are _______.

a poor way to raise general economic well-being

determine/define absolute advantage

the ability to produce a good using fewer inputs than another producer

compute opportunity costs

determine/define comparative advantage

the ability to produce a good at a lower opportunity cost than another producer

specialization and trade

based on comparative advantage

when people produce goods in which they have a comparative advantage, total production rises

understand why trade is mutually beneficial

Trade can benefit everyone because it allows people to specialize in the activities in which they have a comparative advantage.

identify terms of trade

For both parties to gain from trade, the price at which they trade must lie between their opportunity costs.

imports

goods produced abroad and sold domestically

exports

goods produced domestically and sold abroad

Before Frank and Ruby engage in trade, each of them _______.

consumes at a point on their production possibilities frontier

After Frank and Ruby engage in trade, each of them _______.

consumes at a point outside their production possibilities frontier

In an hour, Mateo can wash 2 cars or mow 1 lawn, and Sophia can wash 3 cars or mow 1 lawn. Who has the absolute advantage in car washing, and who has the absolute advantage in lawn mowing

Sophia in washing, neither in mowing

Between Mateo and Sophia, who has the comparative advantage in car washing, and who has the comparative advantage in lawn mowing?

Sophia in washing, Mateo in mowing

When Mateo and Sophia produce efficiently and make a mutually beneficial trade based on comparative advantage,

Mateo mows more and Sophia washes more

A nation will typically import those goods in which _______.

other nations have a comparative advantage

Suppose that in the United States, producing an aircraft takes 10,000 hours of labor and producing a shirt takes 2 hours of labor. In China, producing an aircraft takes 40,000 hours of labor and producing a shirt takes 4 hours of labor. What will these nations trade?

China will export shirts, and the United States will export aircraft

Kayla can cook dinner in 30 minutes and wash the laundry in 20 minutes. Her roommate takes twice as long to do each task. How should the roommates allocate the work?

There are no gains from trade in this situation

describe a market

a group of buyers and sellers of a particular good or service

characteristics of competitive markets

a market in which there are many buyers and many sellers so each has a negligible impact on the market price

ceteris paribus

'holding other things constant' or 'all other things being equal.'

law of demand

as the price of a good or service increases, the quantity demanded by consumers decreases

-price and quantity demanded move in opposite directions

law of supply

keeping other factors constant, an increase price results in an increase in quantity supplied

change in quantity demanded vs. change in demand

quantity demanded: the amount of a good that buyers are willing and able to purchase

change in demand:

increase in demand- demand curve shifts to the right

decrease in demand- demand curve shifts to the left

non-price determinants of demand (demand shifters)

number of buyers

income: normal goods vs. inferior goods

price of related goods: substitutes vs. complements

tastes/preferences

expectations: future income and future prices

inferior goods are not economic bads

example of an inferior good might be bus rides

market demand vs. individual demand

market demand: the sum of all individual demands for a particular good or service

individual demand: quantity of a good or service a single consumer is willing and able to buy at various prices

change in quantity supplied vs. change in supply

quantity supplied: the amount of a good that sellers are willing and able to sell

change in supply: when the price of a good rises, the quantity supplied also rises, and when the price falls, the quantity supplied falls as well

non-price determinants of supply (supply shifters)

number of sellers

input prices

technology

expectations: future prices

market supply versus individual supply

sum of the supplies of all sellers

equilibrium: equilibrium price and equilibrium quantity

equilibrium price: the price that balances the quantity supplied and the quantity demanded

equilibrium quantity: the quantity supplied and the quantity demanded at the equilibrium price

shortage

a situation in which the quantity demanded is greater than the quantity supplied

surplus

a situation in which the quantity supplied is greater than the quantity demanded

comparative statics (changes in equilibrium): due to changes in demand/supply or both

single shift

two shifts

the allocation of resources

In market economies, prices are the signals that guide decisions and allocate scarce resources. For every good in the economy, the price ensures that supply and demand are in balance.

normal good

a good for which, other things being equal, an increase in income leads to an increase in demand

inferior good

a good for which, other things being equal, an increase in income leads to a decrease in demand

substitutes

two goods for which an increase in the price of one leads to an increase in the demand for the other

complements

two goods for which an increase in the price of one leads to a decrease in the demand for the other

The best definition of a market is

a group of buyers and sellers of a good or service

In a perfectly competitive market,

every seller takes the price of its product as set by market conditions

The market for which product best fits the definition of a perfectly competitive market?

eggs

A change in which of the following will not shift the demand curve for hamburgers?

The price of hamburgers

Which of the following will shift the demand curve for pizza to the right?

An increase in the price of hamburgers, a substitute for pizza

If pasta is an inferior good, then the demand curve shifts to the ________ when ________ rises.

left; consumers' income

Which of the following moves the pizza market up along a given supply curve?

An increase in the price of pizza

Which of the following shifts the supply curve for pizza to the right?

A decrease in the price of cheese, an input to pizza

Movie tickets and film streaming services are substitutes. If the price of film streaming increases, what happens in the market for movie tickets?

The demand curve shifts to the right

The discovery of a large new reserve of crude oil will shift the ________ curve for gasoline, leading to a ________ equilibrium price.

supply; lower

If the economy goes into a recession and incomes fall, what happens in the markets for inferior goods?

Prices and quantities both rise

Which of the following might lead to an increase in the equilibrium price of jelly and a decrease in the equilibrium quantity of jelly sold?

An increase in the price of grapes, an input into jelly