ECON UNIT 3

1/70

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

71 Terms

Explicit Costs

The direct, out‑of‑pocket payments a firm makes for resources it does not own.

Implicit Costs

The opportunity costs of using resources the firm already owns—costs that don’t require a direct monetary payment, but still represent a real sacrifice.

Profits

Represents how much a firm earns after covering its costs — but the meaning shifts depending on whether we’re talking about accounting profit or economic profit. Here’s the clean breakdown.

Diminishing Marginal product

Stating that as more units of a variable input, (like labor are) added to fix inputs (like machinery,) the additional output per new unit eventually declines

Fixed Costs

Cost of fixed inputs; expenditure that a firm must make before production starts

Variable Costs

Some of effects in variable costs of production

Total Costs

Some of fixed and variable costs of production (FC+VC)

Average Fixed Costs

average total cost curve in the short term; shows the total of the average fixed cost costs and the average variable costs (FC/Q)

Average Variable Cost

Variable costs divided by quantity of output (VC/Q)

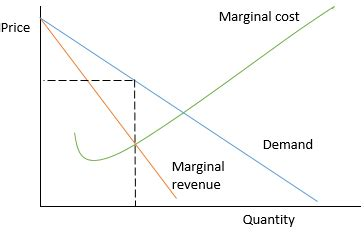

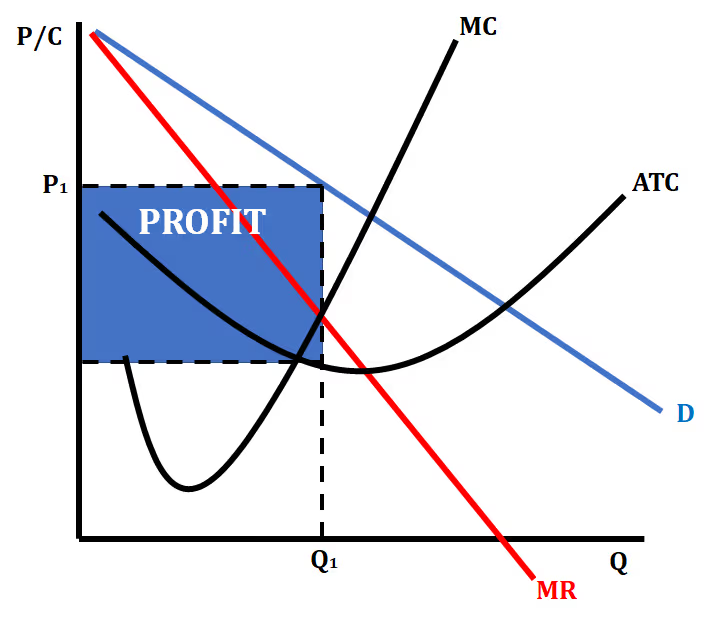

Marginal Cost

The additional price of producing one more unit (MC=🔺TC/🔺Q)

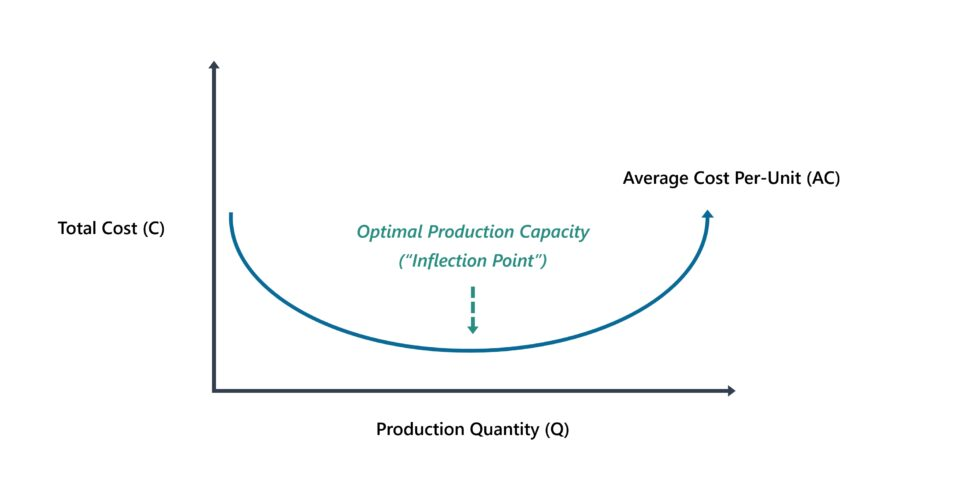

Economies of Scale

Occur when a firm’s average cost per unit decreases as output increases. This happens because producing more allows the firm to spread fixed costs over more units and operate more efficiently.

Constant Returns to Scale

Occur when a firm doubles all inputs and output also doubles, meaning the average cost stays the same as production expands.

Diseconomies

Occur when a firm’s average cost per unit increases as output increases. This happens because the organization becomes too large to manage efficiently

Average Total Cost

Total cost/the quantity of output (TC/Q)

Marginal Revenue

The extra revenue a firm earns from selling one more unit of output =ΔTR/ΔQ.

Efficiency

Maximum possible output with the minimum necessary resources. In economics, it describes how well an economy or firm uses inputs like labor, capital, and time to create value.

Sunk Costs

This is a type of cost that is spent and can't be recuperated.

Variable Costs

Some of effects in variable costs of production

Perfect Competition

The market structure where no individual firm has any power to influence price. It represents the most competitive possible environment in microeconomics

Monopolistic Competition

The market structure where many firms compete, but each sells a slightly differentiated product, giving every firm a small amount of market power. It sits between perfect competition and monopoly.

Oligopoly

A market structure where a small number of large firms dominate the industry, creating strategic interdependence—each firm’s decisions affect the others.

Monopoly

A market in which one firm is the sole producer of a good or service with no close substitutes, giving it substantial power to set price and control output.

Profit Maximization

A firm maximizes profit where marginal revenue (MR) equals marginal cost (MC).

Total Revenue

The money a firm earns from selling its product, calculated by multiplying price and quantity sold. =P×Q

First Degree Price Discrimination

When a firm charges each individual consumer their exact maximum willingness to pay for every unit, allowing the firm to capture the entire consumer surplus as profit.

Second Degree Price Discrimination

Occurs when a firm charges different prices based on the quantity purchased or the version of the product chosen, but not based on who the buyer is. Consumers self‑select into different price tiers.

Third Degree Price Discrimination

Occurs when a firm charges different prices to different identifiable groups of consumers based on differences in their price elasticity of demand, not on quantity purchased. Each group pays a uniform price, but prices differ across groups.

Price Discrimination

A pricing strategy where a firm charges different prices for the same product to increase profit, based on differences in consumers’ willingness to pay or their demand characteristics.

Variable Price

Refers to any strategy where the price of a product changes depending on conditions, rather than staying fixed. The key idea is that the firm adjusts price in response to demand, time, customer type, or market conditions to increase revenue or profit.

Fixed Price

A pricing strategy where the seller charges one constant price for all buyers and all units, regardless of demand, time, quantity purchased, or customer characteristics. The price does not change unless the firm deliberately resets it.

Market Efficiency

Describes how well a market allocates resources to maximize total surplus—the combined welfare of consumers and producers. A market is efficient when all mutually beneficial trades occur and no resources are wasted.

Price Discrimination

A strategy where a firm charges different prices for the same product in order to capture more consumer surplus and increase profit. The product itself does not change only the price does. What varies is who pays what, how much they buy, or which group they belong to.

Inefficiency

When a market fails to produce the right amount of a good, society misses out on potential benefits because some valuable trades never happen.

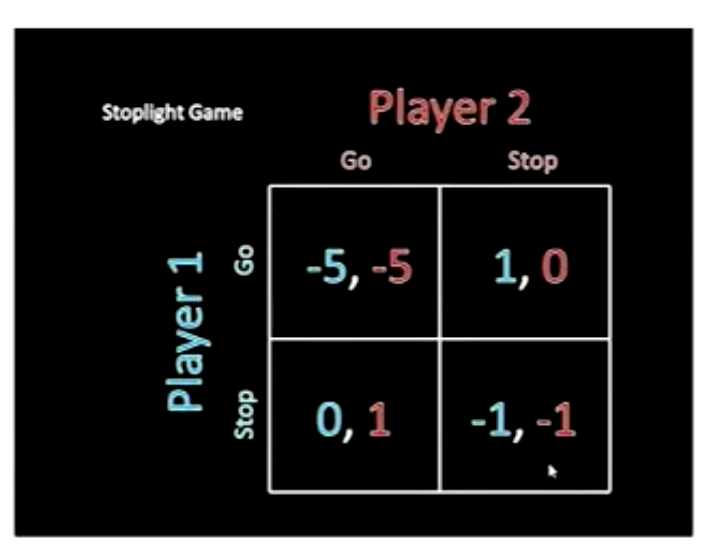

Prisoners Dilemma

Two people end up choosing actions that make them both worse off because each one is trying to protect themselves from being taken advantage of.

Pareto-Efficient

A situation is described this way when no one can be made better off without making someone else worse off.

Nash Efficiency

A situation has this property when each participant is doing the best they can given what everyone else is doing, yet the outcome still leaves room for everyone to be better off through a different set of choices.

Game Theory

It describes situations where people or firms make choices while considering how others will react, because each person’s best move depends on what the others do.

Sequential Decision Making

It describes situations where people make choices one after another, and each person’s best move depends on what earlier players have already done.

Tit-forTat

It describes a strategy where you begin by cooperating, and afterward you simply repeat whatever the other person did on the previous round, rewarding cooperation with cooperation and responding to betrayal with the same behavior.

Sequential Games

It refers to situations where people make choices in a specific order, and each person must take into account what earlier decision‑makers have already done before choosing their own action.

Government Regulation

It refers to rules set by public authorities that limit or guide how firms and individuals behave in markets so that outcomes align better with society’s goals.

Antitrust Laws

They are rules designed to stop businesses from working together to limit competition or from becoming so dominant that they can control prices or shut out rivals, with the goal of keeping markets open, fair, and competitive.

Predatory Pricing

It describes a situation where a business deliberately charges a very low price for a period of time in order to drive competitors out or keep them from entering, even though the price is too low to be sustainable in the long run.

Regulatory Capture

It describes a situation where the officials meant to oversee an industry end up acting in ways that favor the very companies they are supposed to monitor, rather than protecting the public’s interests.

What is diminishing marginal product?

It describes a situation where adding more of one input—like workers—causes output to rise by smaller and smaller amounts because the fixed resources (like space or machines) become crowded or overused.

What are the factors of production in an economy?

They are the basic ingredients an economy uses to produce goods and services: the inputs every business needs to create anything.

Give an example of a sunk cost.

Money you spent on a concert ticket that you can’t get refunded, even if you later decide you don’t want to go.

1st Degree Price Discrimination

It describes a situation where a seller charges each individual buyer the maximum amount that specific person is willing to pay, capturing all the extra value the buyer would normally keep.

2nd Degree Price Discrimination

It describes a pricing approach where the amount a buyer pays depends on how much they purchase or which version of a product they choose, even though every buyer faces the same menu of options.

3rd Degree Price Discrimination

It describes a pricing practice where a seller charges different groups of customers different prices because those groups respond differently to price changes, even though everyone within the same group pays the same amount.

Negative Sum Game

It describes a situation where everyone involved ends up worse off overall, because the total losses from their actions are greater than the total gains, even though each participant may feel pressured to act the way they do.

Positive Sum Game

It describes a situation where everyone involved can end up better off because their choices create more total value than they take away, so the “pie” grows rather than shrinks.

In any business, what is the profit maximizing point, and therefore the stopping point?

The point where a business should stop increasing output is the quantity at which the extra revenue from the next unit is exactly equal to the extra cost of producing that unit. At that moment, profit is as high as it can get, and any additional unit would reduce it.

What are features of an oligopoly?

Is marked by a small number of large firms that dominate a market, creating a situation where each firm’s decisions meaningfully affect the others. Because of this interdependence, firms behave strategically rather than taking prices as given.

Phil goes to the store. He sees that if he buys 12 rolls of paper towels, he pays $1 per roll. However, if he buys 24 rolls, he will pay $.75 per roll. This is an example of:

2nd Degree Price Discrimination

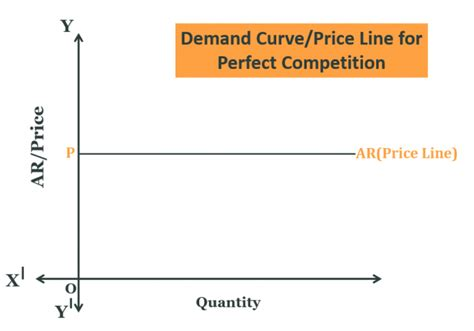

A perfectly horizontal demand curve would be related to which of the following markets?

Perfectly Competitive

Price taker, does not advertise, and cannot earn economic profits in the long run are all traits of which market structure?

Perfect Competition

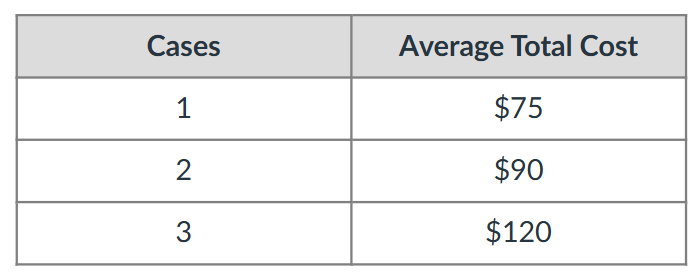

Find the total and marginal cost for the production of the 2nd case given the chart below:

TC of producing 2 cases: $180

MC of the 2nd case: $105

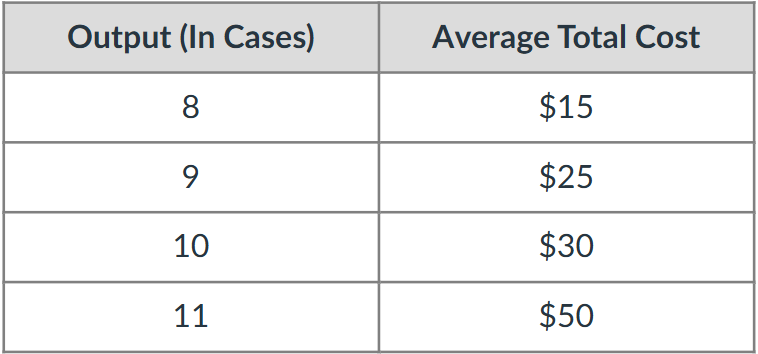

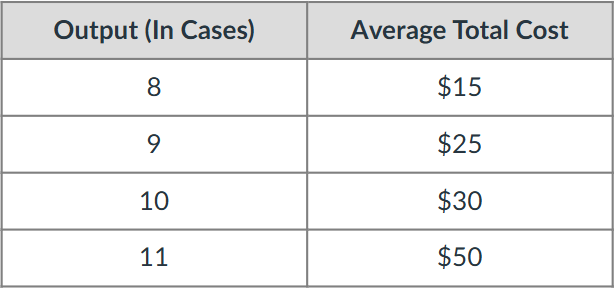

Given the above chart, what is the total cost for producing the 9th case?

$225

Given the above chart, what is the marginal cost for producing the 10th case?

$75

What are the traits of a Perfectly Competitive Market, and what do their demand curves look like?

Market has many buyers and sellers, identical products, free entry and exit, and perfect information, which together ensure that no individual firm can influence the market price. Because each firm is a price taker, its demand curve is perfectly horizontal, meaning it can sell any quantity at the market price but nothing above it.

What are the traits of a Monopoly, and what do their demand curves look like?

A market where one seller controls the entire supply of a product, allowing it to set price rather than take it. Because buyers have no close substitutes, the seller faces the whole market demand curve, which slopes downward.

What are the traits of a Monopolistic Competition, and what do their demand curves look like?

A market of this type has many firms selling products that are similar but not identical, giving each seller a small amount of pricing power. Because buyers see differences in branding, style, quality, or location, each seller faces a downward‑sloping demand curve rather than a perfectly flat one.

Economies of Scale

Occurs when producing more lowers the cost per unit, because fixed resources are spread over more output and production becomes more efficient.

Diseconomies of Scale

Occurs when producing more raises the cost per unit, because the organization becomes too large to manage efficiently. As output expands, coordination breaks down, communication slows, bureaucracy grows, and workers become harder to monitor — all of which push average cost upward.

Constant Returns of Scale

A situation where producing more leaves the cost per unit unchanged. When a firm doubles all inputs and output also doubles, the average cost stays flat because the production process is already operating at an efficient size

Predatory pricing occurs when the price is:

Less than AVC

In a long run cooperative game, the best strategy is to

Copycat (or tit-for-tat)

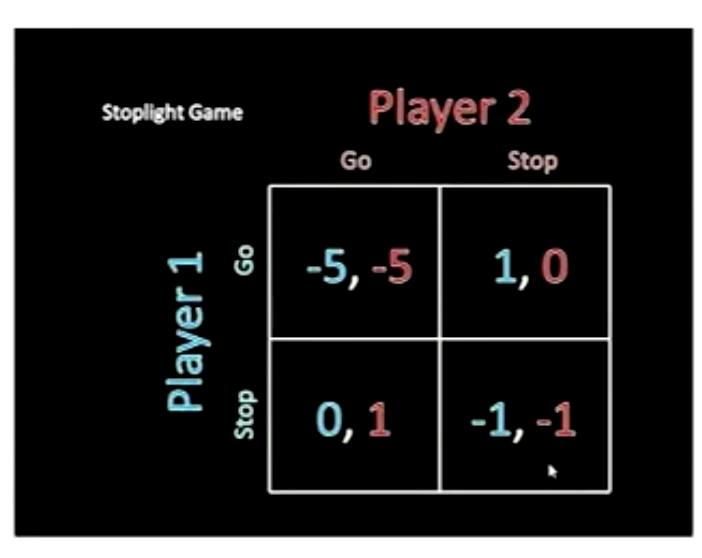

The dominant strategy given the scenario below is

Does not exist

How many Nash Equilibria are in this game?

2

Nash Equilibrium

It is the outcome where each player is already doing the best they can given what the other player is doing, so no one can improve their payoff by changing their choice alone.