Microeconomics

1/134

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

135 Terms

Mrket mechanism

A tendency in a free market for a price to change until the market clears

Supply and demand curves equations

Qd = a - bP (a - y-intercept, b - slope = dQd/dP) Qs = c+dP

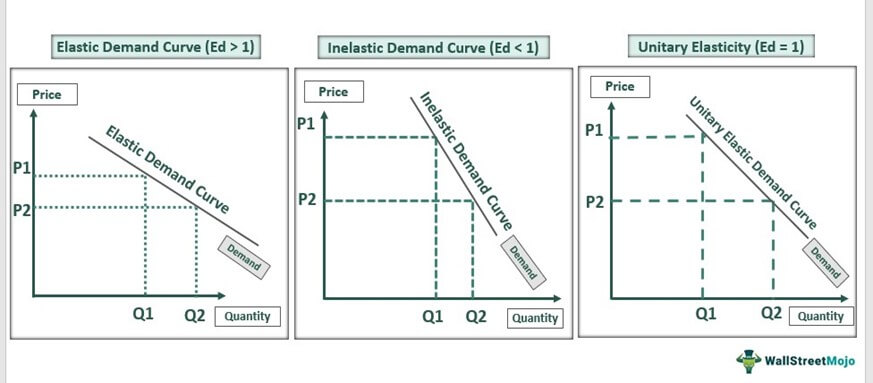

Price elasticity of demand/supply formula + analysis

EQdP = dQd/dP * P/Qd

>1 → elastic

=1 → unit-elastic

<1 → inelastic

(considering absolute values)

Explain

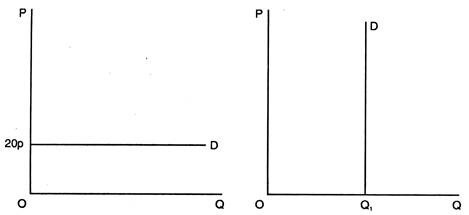

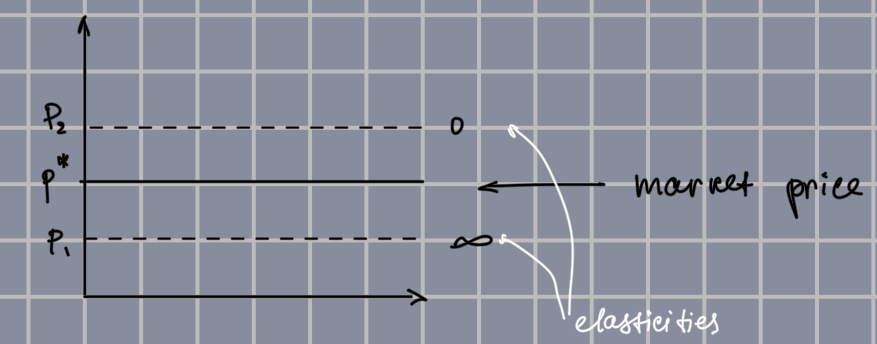

a) Horizontal or Perfectly Elastic demand (E=infinity)

b) Vertical or Perfectly Inelastic demand (E=0)

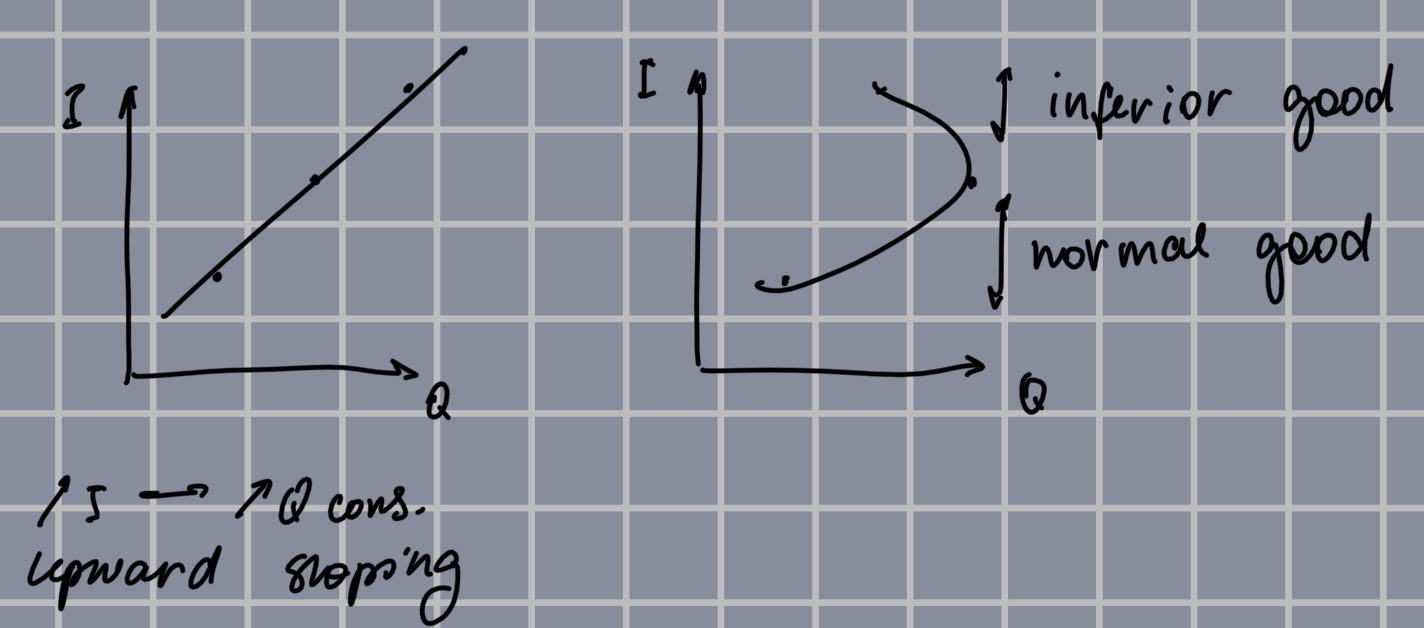

Income elasticity of demand formula + analysis

EQdI = dD/dI * I/D

>0 → normal good

>0<1 → necessary good (1>E>0 )

>1 → luxury good

<0 → inferior good

Cross - price elasticity of demand formula

EQdxPy = dQdx/dPy * Py/Qdx

Point vs Arc elasticity

Point - at a certain price point on the curve

Arc - over a range of prices

Short run vs Long run

Short run: L variable, K fixed (more than 1 production factor cannot be changed)

Long run: L variable, K variable

Durable goods

Goods for which income elasticity is larger in the short run than in the long run (for most goods the opposite, eg gasoline vs cars)

LTV vs Subjective theories

Value of the good is based on:

LTV: socially necessary labour (L+K+Equipment etc)

Subjective: individual consumer’s needs and attitudes towards the good

Marginal utility + formula

Additional utility (satisfaction) from consuming one additional unit of the good

MUx = dTU/dX

What is the slope of the total utility curve?

Marginal utility

Theory of consumer behaviour definiton

How consumers allocate incomes among different goods and services to maximise resources and satisfaction

TCB Assumptions

Completeness - consumers can compare all the alternatives

Costs are ignored

Transitivity - if A>B and B>C the A>C

Goods are desirable - more is always better than less

Goods for which less in preferred

Bads / Undesirable goods (eg pollution)

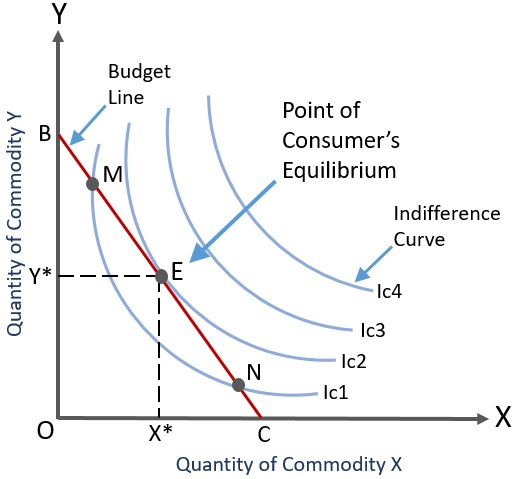

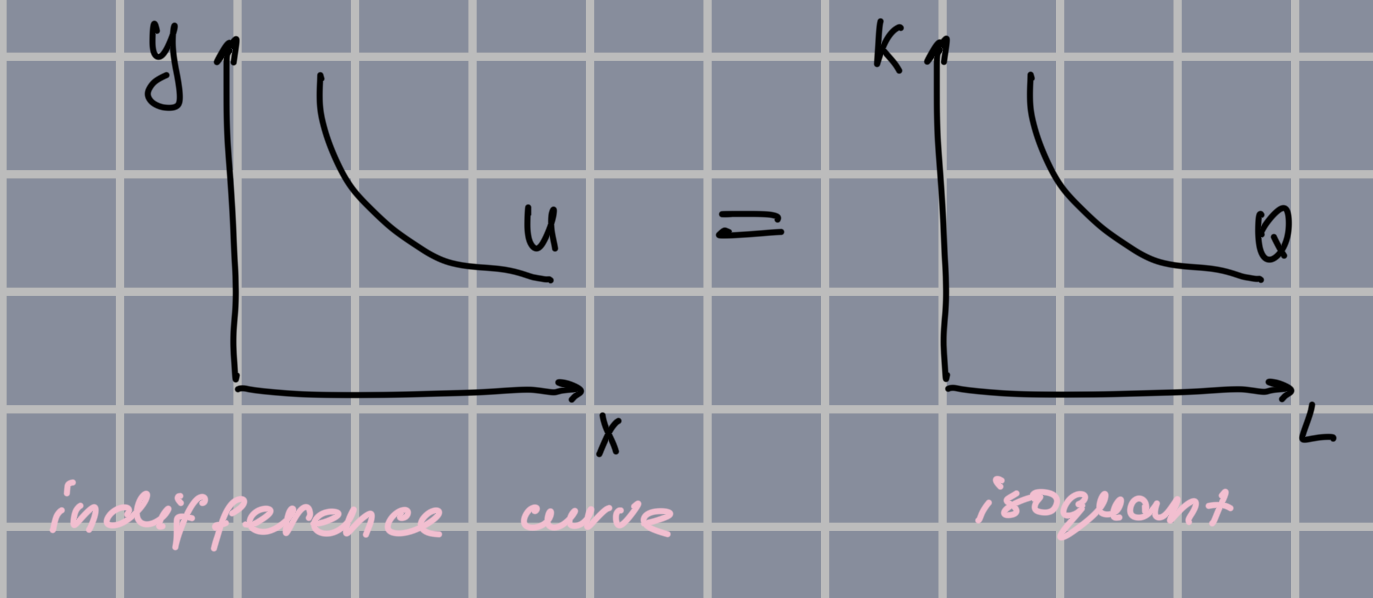

Indifference curve

A curve representing all combinations of market baskets that provide a consumer with the same level of satisfaction

IC Characteristics

Cannot intersect

U3>U2>U1

Negative slope → decrease Y to increase X

Convex curve

MRS

Marginal Rate of Substitution = maximum amount of a good that a consumer is willing to give up in oder to obtain one additional unit of another good (staying at the same level of utility)

MRS = MUx/MUy

What is the slope of the indifference curve?

MRS

Perfect substitutes

2 goods for which MRS of one for the other is a constant → straight line

Perfect compliments

2 goods for which MRS of one for the other is 0 (or infinite) → 90* angle bound lines

Utility

Numerical score that represents the satisfaction that a consumer gets from a certain market basket

Ordinal vs Cardinal utility

Ordinal → general rankings from most to least preferred

Cardinal → concrete numbers (by how much)

Budget constraints

Constraints that consumers face as a result of limited incomes

Budget line + equation formula

All combinations of goods for which the total amount of money spent equals income

I = Px*X + Py*Y

Slope of the budget line

Px/Py

Budget line intersect points with Y- and X-axis formula

Y → I/Py

x → I/Px

Consumer equilibrium equation formula

MUx/Px = MUy/Py

MUx/MUy = Px/Py

MRS = Px/Py

Slope of the indifference curve = Slope of the budget line

Marginal benefit

Benefit of consuming one additional unit of a good

To increase MUx..

We need to decrease X (amount of X) and vice versa

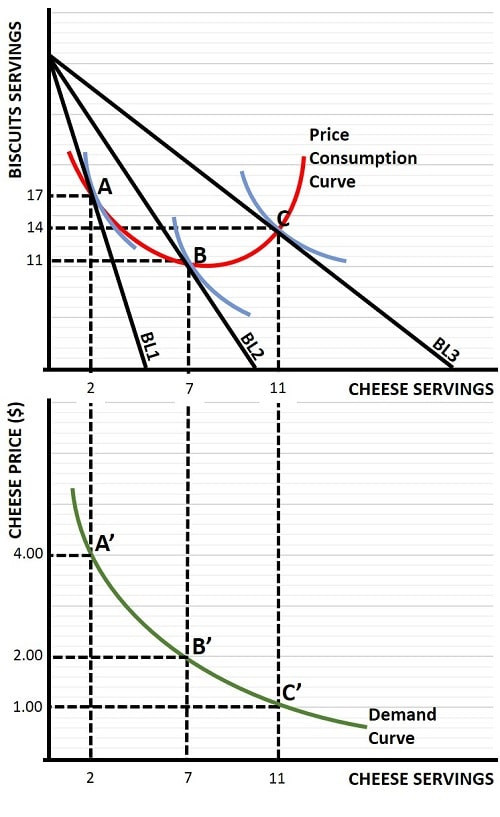

PCC

PCC = Price Consumption Curve = curve tracing the utility-maximising combinations of 2 goods that a consumer can buy at some price point (related to change in price of good X)

Demand curve can be drawn from..

PCC and MUx

Engel curve (ICC)

Curve relating the quantity of a good consumed to income

Isoelastic curve

Has the same elasticity at any point

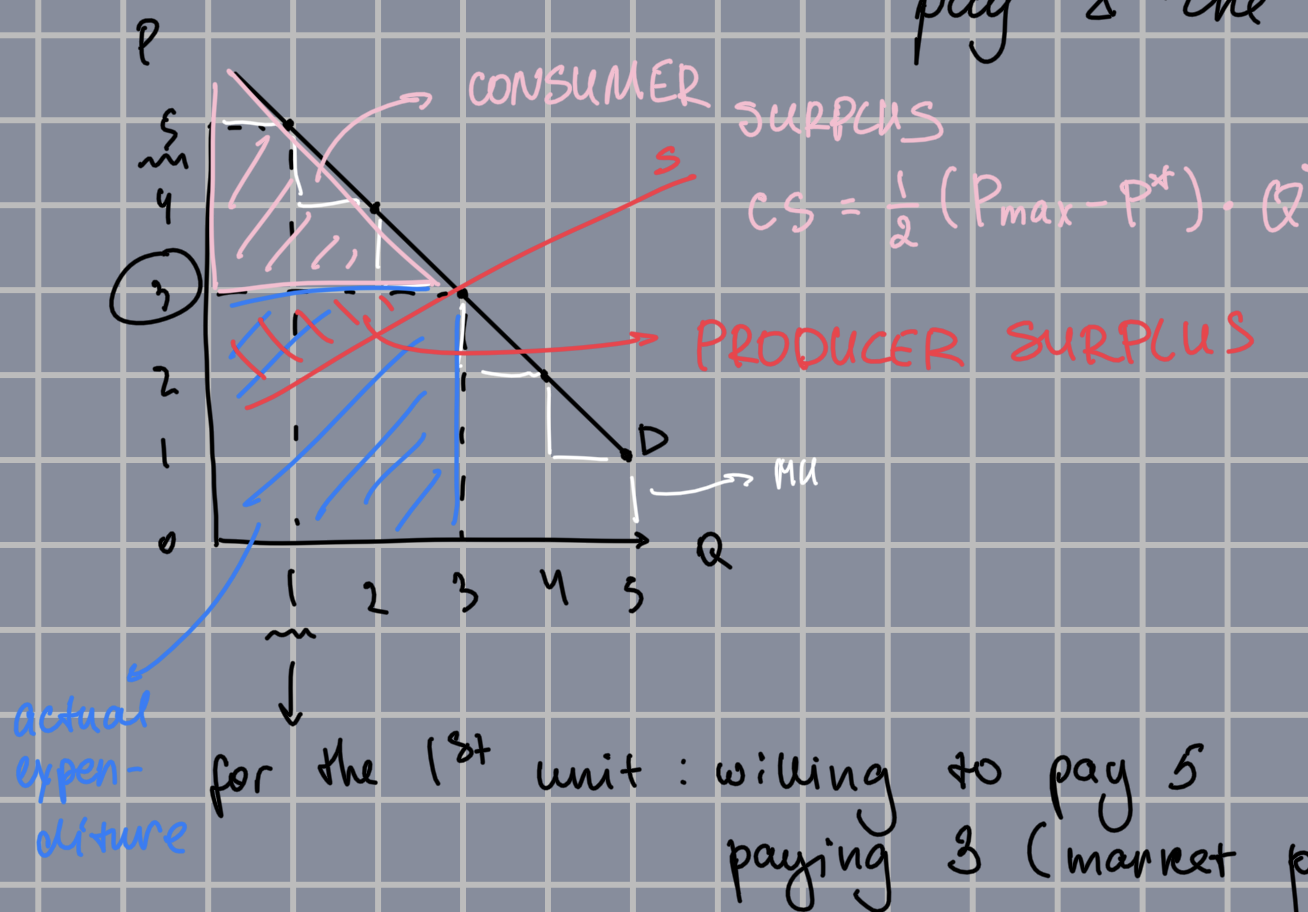

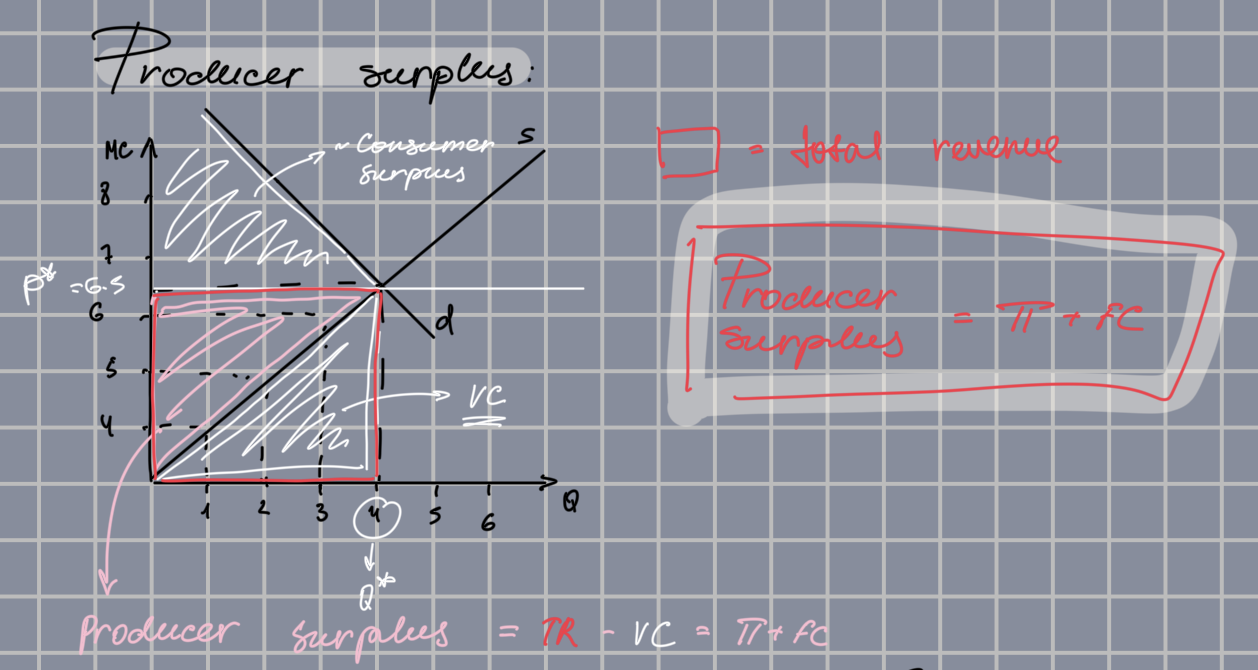

Consumer surplus

The difference between the amount a consumer is willing to pay and the amount actually paid

CS formula

((Pmax - P*) * Q*) / 2

Theory of the firm

How a firm makes cost-minimising production decisions and how the resulting cost varies with output

Factors of production

Inputs into the production process (labour → no of workers/hours, capital → machinery/buildings/materials/equipment - NOT money)

Production function

function showing the highest (fully efficient) output that a firm can produce for every specified combination of inputs

Efficiency

use of all resources in producing any give output (incl. personal time and energy)

Effectiveness

The degree to which the goals are achieved and/or the problems solved

Cobb-Douglas production function formula

Q = A*Lb*Ka

A - degree of technology

b and a - elasticities

Fixed input

Production factor that cannot be changed

Average product + formula

Output per unit of a particular input

APL=Q/L

Marginal product + formula

Additional product per one additional unit of input

MPL=dQ/dL

Output elasticity formula

EQL=MPL/APL (dQ/dL * L/Q)

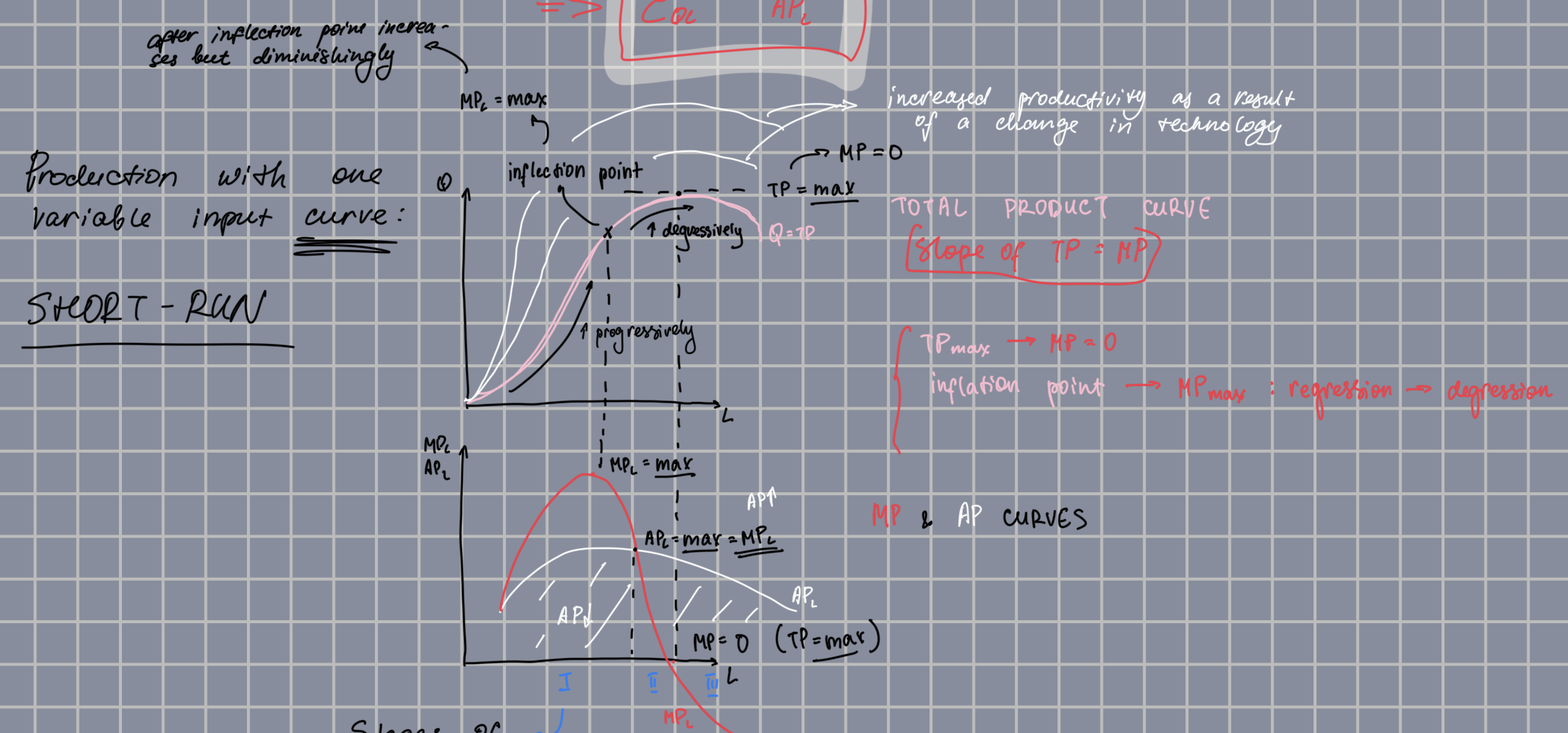

Inflection point, MP is..

max

+ returns increase not progressively but degressively

Short-run production graph

Sloope of the TP (total product) curve

MP

When TP is max, MP is..

0

When AP is max, MP is..

= AP

Stages of production

Stage of increasing returns: TP increases progressively, MPL > APL and MPK > 0

Stage of diminishing returns: starts at the point of APL = max = MPL → TP increases degressively, MPL < APL and MPK > 0 but decreses

Stage of negative returns: starts at TP = max (MPL = 0) → TP decreases, MPL < APL and MPK < 0

Law of diminishing marginal returns

As the use of an input increases (with other inputs fixed) the resulting additions to the output will eventually decrease

APPLIES ONLY TO THE SHORT-RUN PRODUCTION

Isoquant

Curve showing all possible combinations of inputs that yield the same quantity

Slope of the isoquant

MRTS

Isoquant properties

Negative slope

Convex

Cannot intersect

Q3 > Q2 > Q1

MRTS

Marginal rate of technical substitution = the amount by which one input can be decreased to use one extra unit of another input to maintain the same level of production

MRTS formula

MRTS = MPL/MPK (=dK/dL)

Isocost

Curve showing all the different combinations of inputs that can be purchased for a given cost

Slope of the isocost

w/r

Producer equilibrium formula/equation

MPL/w = MPK/r

MPL/MPK = w/r

MRTS = w/r

Slope of the isoquant = Slope of the isocost

Perfect substitutes (inputs)

2 inputs for which MRTS of one for the other is a constant → straight diagonal line

Perfect compliments (inputs)

2 goods for which MRTS of one for the other is a constant = fixed proportions production function → straight angle bent lines

Returns to scale definition

Rate at which output increases as inputs are increased proportionately

Returns to scale types

Increasing: input x2, output x>2 → lines closer to the origin

Constant: input x2, output x2

Decreasing: input x2, output x<2 → lines farther from the origin

PPF

Curve showing the various combinations of 2 different products that can be produced with a given set of inputs

Opportunity cost

Sacrificing the production of one good to produce more of the other

Slope of the PPF

MR(P)T

MRT

Marginal rate of (product) transformation = the rate at which one product must be sacrificed in order to produce a single extra unit of another product

MRT formula

MRT = MCA/MCB

Optimal production point formula/equation

MCA/PA = MCB/PB

MCA/MCB = PA/PB

MRT = PA/PB

Slope of the PPF = Slope of the isorevenue line

Slope of the isorevenue line

PA/PB

Economies of scope

When the joint output of a single firm (2 products) is greater than the output that could be achieved by 2 different firms (1 product each)

Returns to scale formula

RTS = Eq,l + Eq,k

Marginal cost formula

MC = dVC/dQ = w/MPL

Accounting cost

Actual expenses + depreciation of equipment

Economic cost

Cost of utilising economic resources including opportunity cost → Economic c. = Accounting c. + Opportunity cost

Amortisation

Treating a one-time expenditure as an annual cost spread out over some number of years

MC definition

Additional cost of producing one extra unit of output

Economies of scale

A situation in which output can be doubled for less than a doubling of costs

Cost-output elasticity formula

Etc,q = dTC/dQ * Q/TC = MC/ATC

Classifications of market structures (authors)

Stackelberg (9 types, output market and input market)

Samuelson (3 types: PC, limited competition (3 types), monopoly

Waud (4 types)

Weintraub (!)

In which market structure is product differentiated?

Monopolistic competition

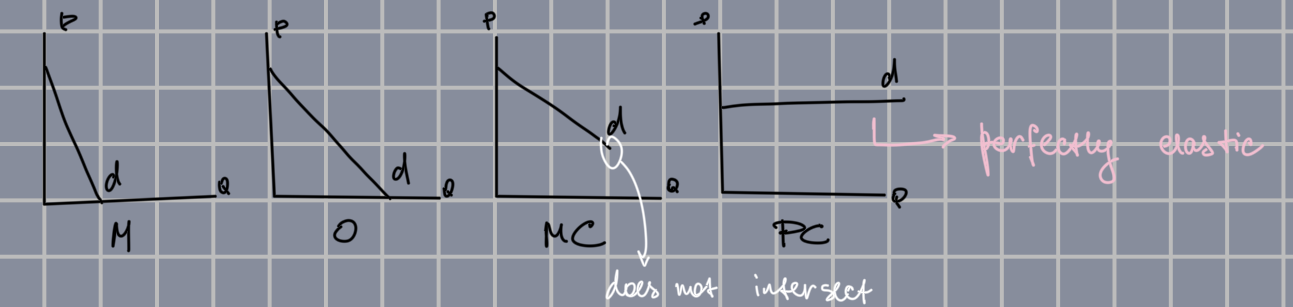

Elasticity in different market structures (how graphs look)

PC: E = infinite, Cross-Elasticity = 0

M: E = small number, CE = 0

O: E = infinite, CE = higher number

MC: E = higher number, CE = small number

PC assumptions

firms are price takers

price = market price

products are homogeneous and perfect substitutes

free entry and exit

P = MR = AR = d = MC

Accounting profit

TR - TC (EXCL opportunity cost)

Economic profit

Accounting profit - opportunity costs

Profit maximisation/Output rule (2 conditions)

MR + MC (in PC → P = MC)

MR’ < MC’ (slope of marginal revenue < slope of marginal cost)

Marginal revenue

Change in revenue resulting from a one unit increase in output

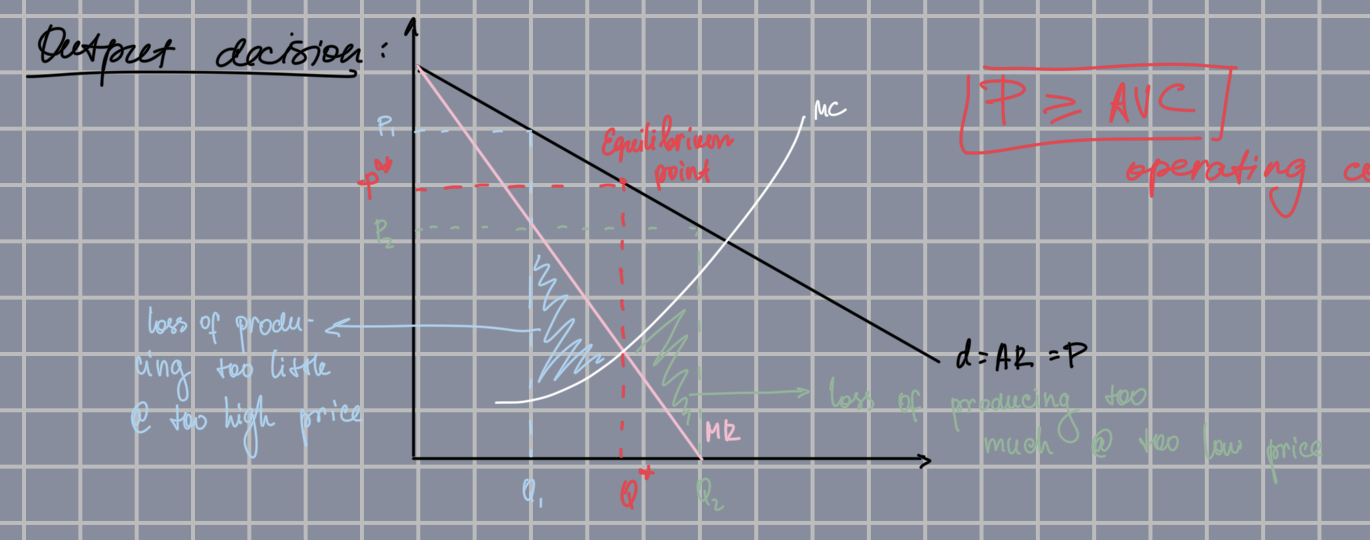

Operating condition

P ≥ AVC

Supply curve

Marginal costs curve that is above AVC (ATC) in the short (long) run

Producer surplus formula

PS = TR - VC = PROFIT + FC

It is above the MC curve and below the P*

In LRPC PS = 0!

Monopoly

Market structure with only one seller selling a product without close substitutes (eg. water supply in a city managed by the givernment)

Monopsony

Market with only one buyer → input market

Market power

Ability of a seller or buyer to affect the price of a good

Average profit formula

Avg profit = AR - AC = P - TC/Q

Output decision graph