Business HL year 1 finance

1/28

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

29 Terms

Contribution per Unit Formula

selling price - variable costs

Variable costs

If production increases, variable costs increase.

Total Contribution

Contribution x sales volume

Fixed costs

costs that remain the same regardless of the level of production or sales (They must be paid even if no products are sold) ex: Software subscriptions with fixed monthly fees, property rent, equipment depreciation

Unit contribution

selling price - variable costs per piece

Units of production depreciation per unit

cost - salvage value/ total estimated units

salvage value

It is the amount of money a company expects to sell the asset for (or get for its parts) after they are completely done using it

Net book value

the current value of an asset as recorded in a business's accounting books.

total current assets

the sum of all liquid resources a business owns that are expected to be converted into cash, consumed, or sold within 12 months. (debtors, cash, stock/inventory, prepaid expenses)

Cash

Cash is readily available money for immediate payments (current asset)

debtors

debtors are customers who owe the business money for goods or services bought on credit (current asset)

Income Statement

calculates profit

balance sheet

which lists assets and debts

gross profit margin

percentage of revenue a business keeps after paying the direct costs of producing its goods or services (revenue- COGs/ revenue) x 100

current ratio

current assets/ current liabilities

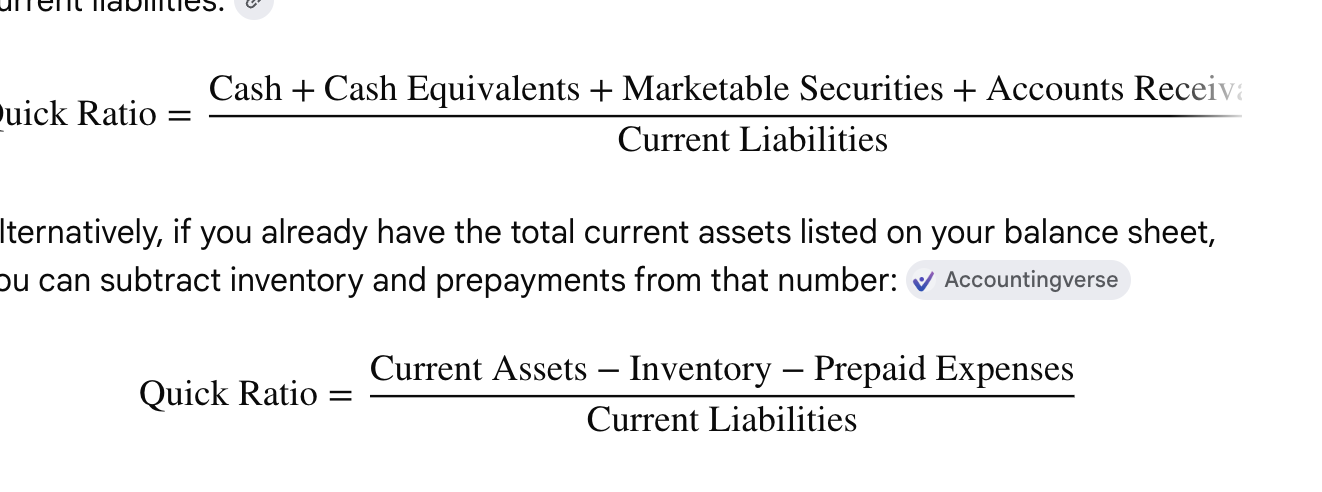

acid test (quick) ratio

current assets - inventory/ current liabilities

Measures a businesses short term liquidity. The ratio strictly limits assets to those that can be turned into cash within 90 days

cost of sales

the total direct cost of producing and delivering the goods or services a business sells during a specific period. It only includes expenses directly tied to production, such as raw materials, direct labor, and shipping, excluding general overhead like rent or marketing

gross profit

company's total revenue minus the direct costs of producing and selling its goods or services (total revenue - cost of goods)

profit margin

percentage of revenue a business keeps as profit after deducting all expenses.

net profit margin

net profit/ revenue x 100

net income

the total amount of money remaining after all expenses, taxes, and deductions are subtracted from total revenue or gross income (total revenue - total expenses)

expenses

the everyday costs required to operate a company, generate revenue, and maintain daily activities.

net fixed assets

the current book value of a company’s long-term, tangible assets

total assets

net fixed assets + current assets

retained earnings/ profit

the portion of a company's net income that is kept and reinvested in the business, rather than being distributed to shareholders as dividends. It accumulates over time and represents a crucial internal source of funding for long-term stability and growth

Return on Capital Employed (ROCE)

profit before interest and tax/ capital employed x 100

capital employed

Capital Employed= Total Assets}- Current Liabilities

(Alternatively: Share Capital + Retained Earnings + Non-Current Liabilities)\

capital invested in a business to generate profits.