chapter 8 - losses

1/8

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

9 Terms

trading loss

when accounting profit is adjusted for tax purposes and is negative

treatment for an accounting loss

for an individual, trading profit for tax year will be nil

for limited company, trading profit for that accounting period will be nil

for both, it will be nil and not the actual negative figure

what are the relief options for trading losses (individuals)

losses set against profits of the same trade (loss is carry forward until it is relieved)

losses set against total income

note: maximum possible loss must be set off (PA cant be claimed)

claims to carry forward the loss must be made by 31 January (22 months following end of tax year of loss)

options for relieving losses set against total income

can deduct loss from other income in the current period (period of the loss)

and/or, take the loss back to the previous tax year and reduce its profit

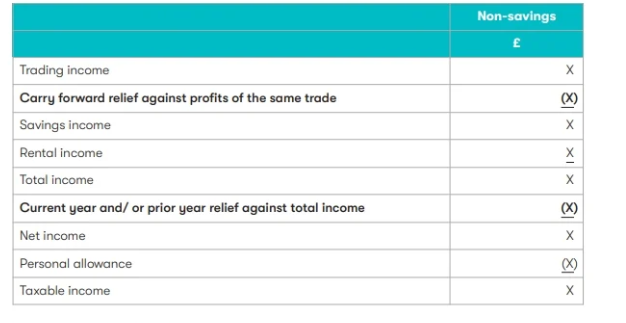

proforma where trade loss appears in income tax computation