3.1.4.3 COMPETITIVE MARKETS

1/36

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

37 Terms

Define perfect competiton?

A market strucure where there are many buyers and sellers, all firms sell identical products, where firms are price takers

What are some characteristics of a perfectly competitive market?

many buyers and sellers

homogenous products (identical)

price takers

free entry and exit

perfect information

no barriers

profit maximizers

How do you define the short run and long run in macroeconomics?

Short - when at least one factor of production is fixed, usually capital

Long - when all factors of production are variable

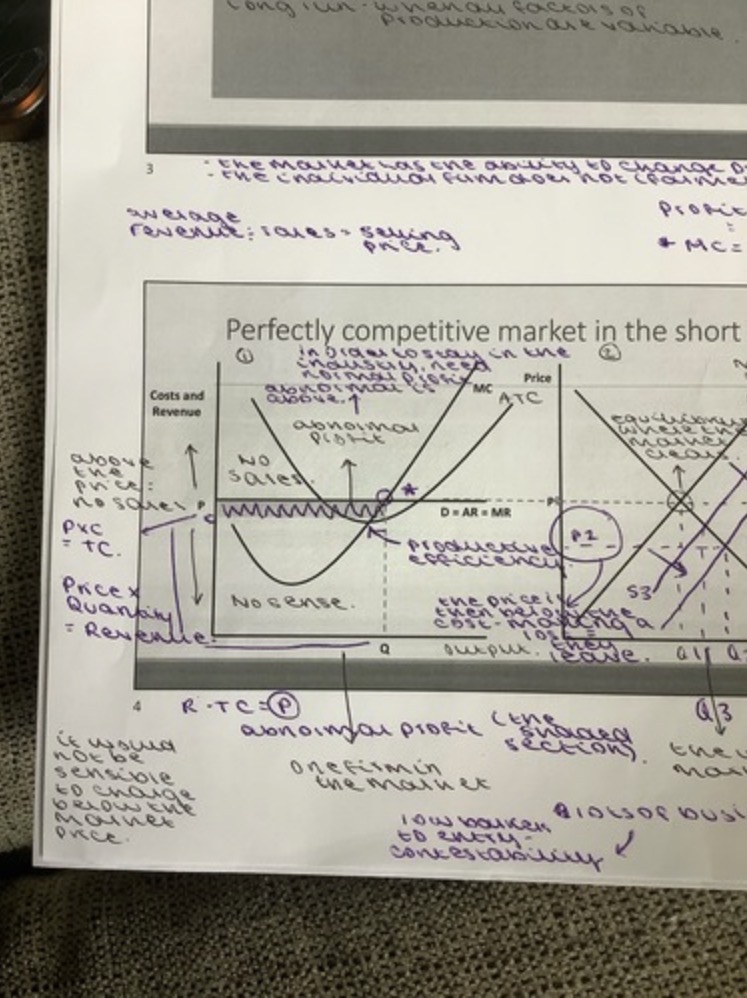

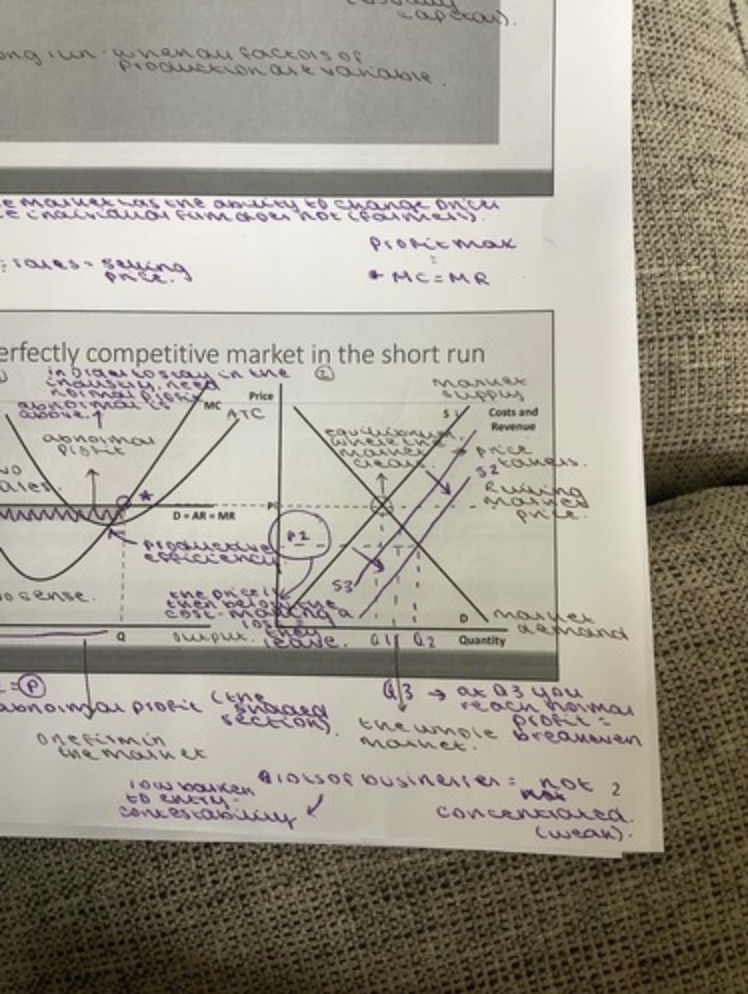

Is there abnormal or normal profit in the short run in a perfectly competitive market?

Abnormal

Is there abnormal or normal profit in the long run in a perfectly competitive market?

Normal

In the short run, in a perfectly competitive market, who determined prices? (Market, firm)

the market has the ability to change prices

the individual firm does not (eg, farmers)

How do you work out selling price?

Average revenue / sales

What equals profit max?

MC = MR

What is the diagram of a perfectly competitive market in the short run? (One firm)

What is the diagram of a perfectly competitive market in the short run? (Whole market)

In order to stay in the market, what type of profit do you need to have?

Normal (abnormal profit is profit)

When is productive efficiency on a graph?

ATC = MC

If there are lots of businesses in a market, is it concentrated or not?

Not concentrated

If there are low barriers, does this mean it is or is not contestability?

Yes contestability

How does the supply curve move on the graph for the entire market?

Supply shifts outwards - decrease price, increases quantity

THEN

Supply shifts inwards slightly - increased price, decreases quantity

How do diagrams move in the long run?

in the long run, firms can enter and exit the market

initially, too many firms enter, shifting supply outwards (S1 to S2)

this causes prices to all (P1 to P2)

when this happens, firms make a loss

some firms leave the market

then supply shifts inwards (S2 to S3)

this causes prices to rise

this then leads to normal profit

Define productive efficiency?

Where a firm produced the maximum possible output from the minimum amount of inputs, resulting in the lowest possible average cost

Define allocative efficiency?

Where resources are distributed to produce the goods and services most desired by consumers

P = MC (the value a consumer places, P, equals the cost of producing it, C)

Where is the most productively efficient point?

The lowest possible point of the ATC curve

Why is the most productively efficient point at the lowest point of the ATC curve?

This is the point where a firm produces maximum output at the lowest possible cost per unit

Give an example of how a waitress cannot be allocatively efficient? And what does this lead to?

If a waiter is not allocatively efficient and is doing too many jobs - customers would not return to the restaurant

If the customer is not satisfied with the good/service, what does this mean for them?

This discourages them from purchasing the good/service again

What point demonstrates allocatively efficient?

The point where society gets exactly what it wants in the right quantities

What does P = MC mean?

Allocatively efficient

What does P < MC mean?

Over-consumption

What does P > MC mean?

Businesses may loose customers

Briefly

What is the difference between productively and allocatively efficient?

Productive - produces at the lowest point on the LRAC curve

Allocative - produces when price equals marginal cost P = MC

In the long run the firm might be both productively efficient and allocatively efficient at the same time

It depends on 3 things, what are they?

No barriers to enter and exit

Profit maximization (MC = MR)

P = MC

Expand on 1. No barriers to enter and exit?

In the long run, there are low barrier to enter and exit

If firms make super norms profits in the short run, new firms will enter

This increases supply

Thus decreases price

Until normal profits are made

Leads to loss and exit

As normal profits exit, firms produce at the lowest possible cost

This equals productive efficiency

Is a monopoly an abstract phenomenon (textbook) or happen in the real world?

Textbook

The conditions required almost never exist simultaneously

Which efficiency does this link to (allocative efficiency or inefficiency)?

P > MC

Allocative efficiency

Which efficiency does this link to (allocative efficiency or inefficiency)?

P < MC

Allocative inefficiency

Why would P > MC discourage consumption?

the price is higher than the cost of production

the firm is essentially “overcharging”

leads to underconsumption

Why would P < MC encourage consumption?

the price is lower than the cost of production

because the price is low, consumers buy the product even if they don’t value it very much

leads to overconsumption

Give me an example of the price being lower then cost of production?

Price - £2

CoP- £10

Customers feel you have got a deal but £8 of resources are wasted to give you a product you do not value highly

When does allocative inefficiency occur? (P > MC / P < MC / P = MC)

P > MC / P < MC

When does allocative efficiency occur? (P > MC / P < MC / P = MC)

P = MC