Basics of investment banking ESADE

1/24

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

25 Terms

Kelly criterion (def & formula)

With p the probability of winning, q = 1-p, and b the return in % in case of win, we can calculate thanks to the Kelly criterion the optimal proportion of your capital to bet/invest to minimize losses —> f* = (bp-q)/b

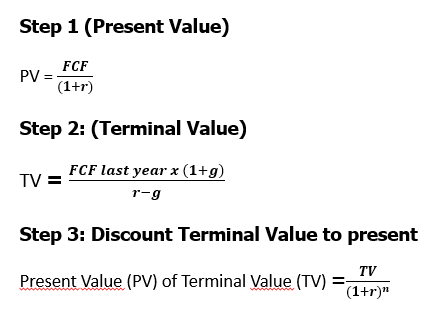

Present Value formula

PV = CFk / (1+r)^k

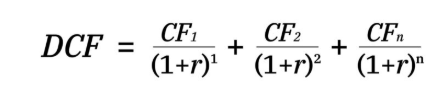

DCF (discounted cash flow) formula

DCF = sum of present value of all future cash flows; le plus souvent, on aura CFk = CF0 x (1+g)^k où g est le taux de croissance de l’entreprise et r est le discount rate

Comment calculer le discount rate r ?

Le WACC (Weighted Average Cost of Capital) est calculé comme suit : WACC=E*re/V+D*rd*(1−T)/V

où : E = valeur des capitaux propres, D = valeur de la dette, V = E + D, re = coût des capitaux propres, rd = coût de la dette, et T = taux d'imposition

Terminal value of an investment ?

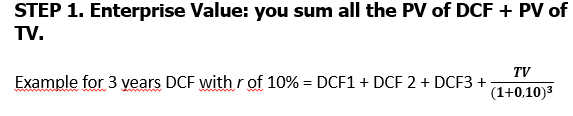

Enterprise value EV formula

Sum of present values of DCF + PV of Terminal Value

Equity value formula

Equity Value = Enterprise Value - Net Debt = EV - (Cash - Debt)

Intrisic share price ISP formula ?

ISP = Equity Value / Oustanding Shares

What are the 3 financial statements ?

Balance sheet (Bilan), Income statement (Compte de résultats), Cash Flow Statement (Tableau de flux de trésorerie) —> You can use them to analyse the financial state of the company

7 steps of the financial analysis of a company ?

MC > EV —> company is positively valued by investors

Total debt / FCF < 5 —> debt is more or less over control

Total revenue is increasing

EV / EBITDA < 20 —> company isn’t too overrated

ROE & ROIC are both over market return (10% in the US) + same for ROA

EPS in increasing

NAV and mNAV —> if mNAV < 1, the company trades at a premium to its underlying assets, else it’s the contrary; ideally it would remain close to 1

Formula NAV, NAV per share, and mNAV ?

NAV = Total Assets - Total Debt

NAV per share = NAV/Outstanding shares

mNAV = MC/NAV

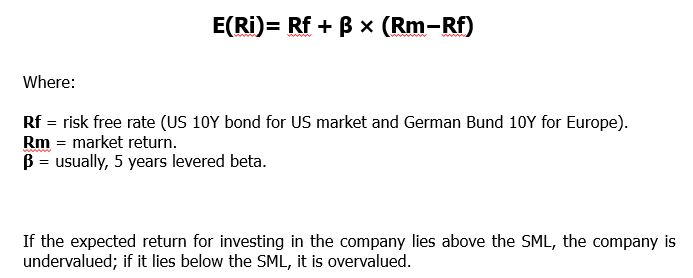

What is Beta ?

It values the risk of a company relatively to the overall market —> for example if beta = 1,5 the stock tends to move 50% more than the market

Levered Beta ? (def + formula)

Levered beta incorporates both operational risk (risk of the business) and the financial risk (risk due to the company’s use of debt) —> see photo for formula

Security market line SML ?

See photo; it represents CAPM, ie the relationship between the 5-years levered beta of an asset and irs potential expected return

If an asset lies above SML, it is undervalued = worth investing in because potential for growth

Gordon Growth Model ? (definition and formula)

Growth Estimated = (EPS forward/P0 current price of share) + g

This gives us the estimated expected return of the company, which we can then compare to CAPM to know if the company is over or undervalued

3 étapes de la création d’une start-up

Idée + Minimum Viable Product

Incubation (valley of death)

Acceleration (from few to many customers)

2 main ways to value a start-up

EV/Revenues —> compare company to its valuation, whether it is an actual capitalization (if public company) or an estimated valuation (if private)

EV/EBITDA —> appropriate for more mature start-ups with positive cash flows and earnings, clear picture of the company’s profitability

6 fundamental aspects to assess a start-up ?

The need = it has to solve a need, and not only a personal interest of yours

The sector has to raise interest

The team (commitment, attitude, skills)

Scalability = is there potential for development & acceleration

Reach VS Magnitude concept ? (inexpensive product for the masses VS expensive product for a niche ?)

Sustainability = fundamental