ACCT 4334: In-Depth Study of Chapter 3 Concepts and Audit Documentation Practices

1/42

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

43 Terms

What are permanent files?

it contains information of continuing audit significance over many years' audits of the same client

What are some documents of permanent interest?

-Corp bylaws

-Contracts

-History of Co.

-Org chart

-Prior Year f/s and audit reports

-excerpts of minutes of stockholders

-continuing schedules of accounts with balances

What do current files include?

all client acceptance or continuance documentation along with planning documentation for the year under audit such as:

-Client acceptance docs

-Engage letter

-Analytics

-Understanding

-assessments of audit risks

determination of audit materiality

-Audit plan

-staff assignment notes

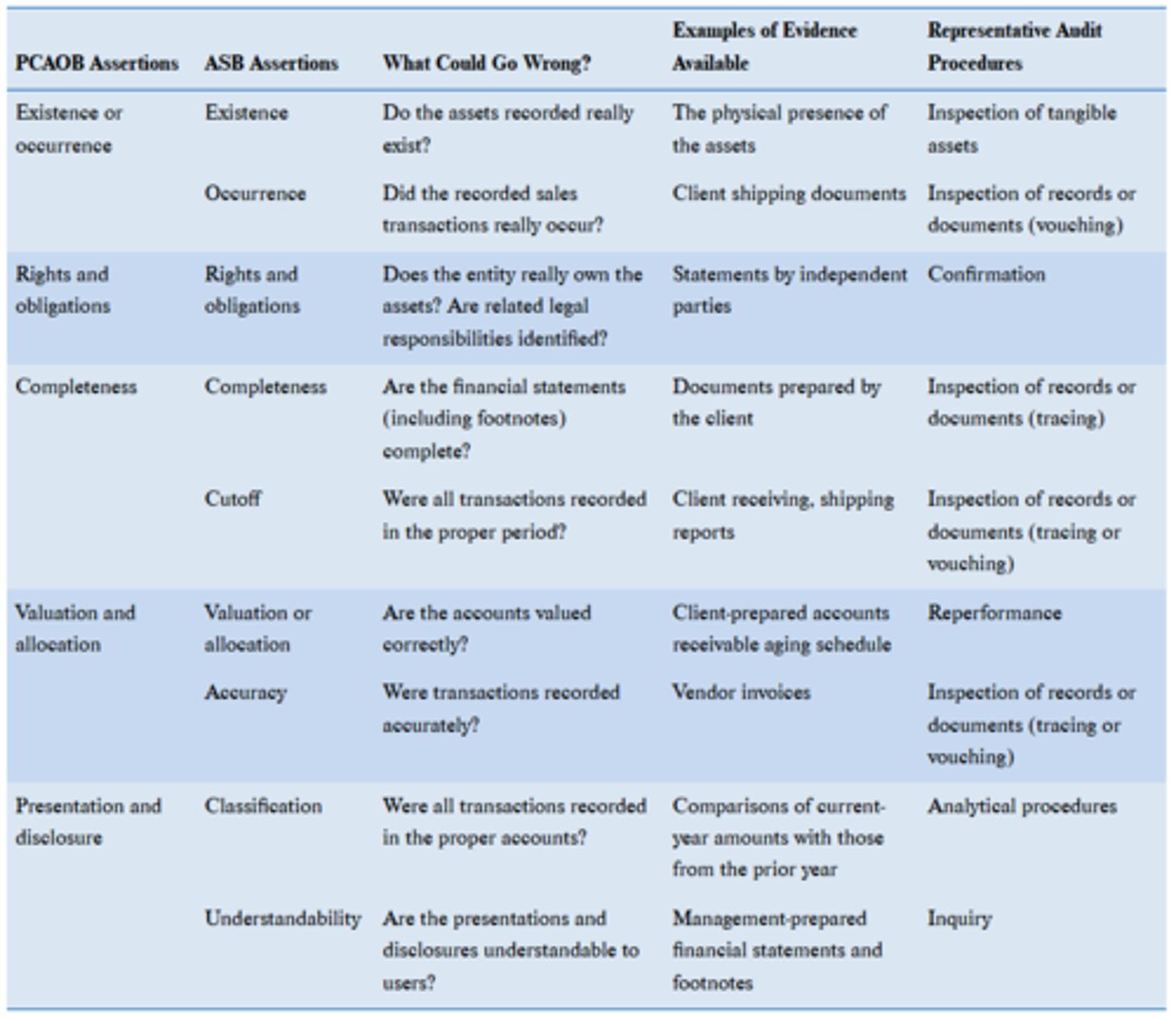

Assertions, Evidence, and Audit Procedures

What are the sources of information to consider when selecting and retaining clients?

•Communication with the predecessor auditor

•Obtaining and reviewing financial info about the client: Annual reports, reports to regulatory agencies, etc.

•Criminal background checks

•Inquiry of bankers, legal counsel, underwriters, people who do business with the client.

•Does the engagement require special attention or involve unusual risks.

•Evaluate our independence.

•Consider the need for special skills.

•Mgmt. integrity is the main consideration

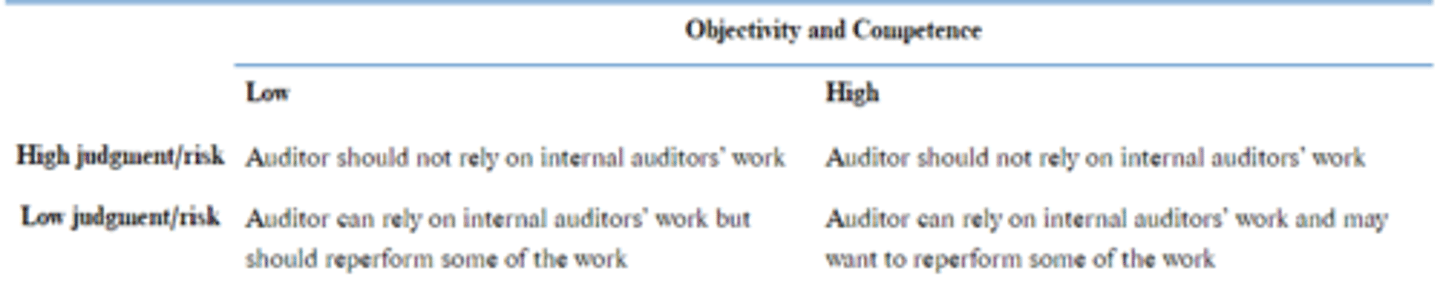

Prior to relying on the work of internal auditors, external auditors should consider their what?

-objectivity

-competence

When is objectivity enhanced?

when the internal auditors report directly to the audit committee of the board of directors

When is objectivity questioned?

-internal auditors report to divisional management, line managers, or other persons with a stake in the outcome of their findings

-managers have some power over the part over the pay of job tenure of the internal auditors

-individual internal auditors have relatives in audit-sensitive areas or are scheduled to be promoted to positions in the activities under internal audit review

How is the competence of internal auditors investigated?

-by obtaining evidence about their educational and experience qualifications

-their certifications and continuing education status

-the department's policies and procedures for work quality and for making personnel assignments, the supervision and review activities, and the quality of reports and audit documentation

What is vouching?

audit procedure in which an auditor selects an item of financial information and follows its path back through the processing steps to its origin

existence or occurrence

What is tracing?

audit procedure in which the auditor selects a source document and follows its processing path forward to find its final recording in a summary journal or ledger

completeness

What are the audit procedures for obtaining audit evidence?

1. inspection of records and documents (includes vouching, tracing, and scanning)

2. inspection of tangible assets

3. observation

4. inquiry

5. confirmation

6. recalculation

7. reperformance

8. analytical procedures

Reasons for planning?

•Identify the risk of material misstatement at the financial statement level and the relevant assertion level

•Design and execute audit procedures designed to mitigate the risk identified

•issuing an appropriate opinion

Factors that contribute to the high risk of a client

•Inadequate capital (no money)

•Lack of long run strategic plans

•Low cost of entry into the market

•Dependence on a limited product range

•Dependence on technology that may become obsolete

•Instability of future cash flows

•History of questionable accounting practices

•Previous inquiries by SEC or other regulatory agencies

Why do clients change auditors?

-Fees,

-Internal Rotation

-Requirements,

-Disagreements

What is an engagement letter?

It sets out terms of the engagement and confirms obligations of both client and practitioner

What does the engagement letter set forth?

-Objectives of the engagement

-Managements responsibilities

-Auditors responsibilities

What does the typical audit staff assignment look like?

•Audit Partner, Audit Manager, Industry Specialist, Senior Auditors, Staff Auditors, IT Specialist and a Concurring Partner as is required by Standards.

Concurring Partner required to give audit a detached, unbiased review

What is an arm's length transaction?

•The ability to exercise significant influence over the other party

What are the three dimensions of materiality?

-Size of the misstatement (dollar amount)

-Circumstances - some things are viewed more critically than others

-User impact - impact on potential users and the type of judgments made

What are the three purposes of audit procedures?

•Risk assessment-used to gain an understanding of the client and the risks associated.

•Tests of Controls-used to test the operating effectiveness of the clients internal control procedures.

•Substantive procedures- Analytical procedures and tests of details for account balances.

General Audit Procedures-8

•Inspection of records and documents (watch for source of docs)-invoices, p.o.s, loan apps, bank statements, title papers

–Vouching

–Tracing

–Scanning-debits in revenue accts, credits in expense accts, etc.

•Inspection of tangible assets-Existence, valuation, not ownership

•Observation-used in tests of controls heavily

•Inquiry-mgmt representations-good starting place-must corroborate

•Confirmation-existence, ownership, valuation, cutoff

•Recalculation-existence, valuation-depreciation, interest expense, pension liabilities, etc.

•Reperformance-reperform a control activity-broader in nature

•Analytical Procedures

AA CORRVIIITS

•Agree Financial Stmts to supporting documents

•Analytical Procedures

•Confirmations

•Observations

•Recalculation

•Reperformance

•Vouch

•Inspection of records and documents

•Inquiry

•Inspect Tangible Assets

•Trace

•Scan

Audit procedures performed by CAATTs

•Recalculation

•Confirmation

•Document Examination (limited)

•Scanning

•Analytical Procedures

•Fraud Investigation

Purposes of Audit Documentation

•Integral part of audit quality

•Nature, timing and extent of work performed

•Professional judgments

•Basis for conclusion

•Facilitates planning, performance and supervision

•Provides basis for review

What activities should following during the pre-engagement phase of the audit?

•Client selection and retention

•Communication between predecessor and successor auditors

•Engagement letters

•Staff assignment

•Time budget

Are public accounting firms obligated to accept undesirable clients?

No.

What are factors in client selection and retention that would be classified as high risk?

•Inadequate capital (no money)

•Lack of long run strategic plans

•Low cost of entry into the market

•Dependence on a limited product range

•Dependence on technology that may become obsolete

•Instability of future cash flows

•History of questionable accounting practices

•Previous inquiries by SEC or other regulatory agencies

What are some sources of information and items to consider in the client selection and retention phase?

•Obtaining and reviewing financial info about the client: Annual reports, reports to regulatory agencies, etc.

•Criminal background checks

•Inquiry of bankers, legal counsel, underwriters, people who do business with the client.

•Does the engagement require special attention or involve unusual risks.

•Evaluate our independence.

•Consider the need for special skills.

Mgmt. integrity is the main consideration

What must be done when changing auditors?

•Client must file a form 8-K-report disagreements

•Attempt to communicate is the only requirement

•Successor initiates the communication

What is the purpose of the engagement letter?

•Standards require auditors to reach a mutual understanding with the client concerning engagement requirements and expectations and to document this understanding.

•The letter acts as a Contract

•Helps to manage engagement risk, because responsibilities and expectations of each party are outlined.

Methods and sources of understanding the client's business

-Inquiry, including prior year working papers

-Observation-tour facilities, watch employees, etc.

-Study numerous sources, ie: audit guides, trade magazines, annual reports, mags. Newspapers, etc.

What are other factors to consider when planning?

-Clients Business Risk

-Materiality and planning

-First-time audits

•Internal auditors-Objectivity and Competence-discuss

•Use of specialists-qualifications, experience and reputation-discuss

•Use of IT auditors - discuss

•Identification of related parties - discuss

•Materiality-see next slides

What are the three main goals of audit planning?

1. staffing

2. materiality

3. risk management

Who is included in the typical audit engagement

•Audit Partner, Audit Manager, Industry Specialist, Senior Auditors, Staff Auditors, IT Specialist and a Concurring Partner as is required by Standards.

•Concurring Partner is required and is supposed to give the audit a detached, unbiased review.

What are the purposes brainstorming sessions?

-informing audit teams of risks in the engagement

-increasing awareness of fraud

Reliance on internal auditors

What is materality?

refers to an amount (or transaction) that would influence the decisions of users (i.e., an amount (or event) that would make a difference). The emphasis is on user, rather than management or the audit team.

Criteria of materiality

Quantitative Criteria:

–Absolute size

–Relative size

–Cumulative effects

Qualitative Criteria

–Nature of the item or issue (illegal payment or liquid assets)

–Circumstances (number that could turn a net loss into a profit)

What type of procedures can be performed by CAATTs?

•Recalculation

•Confirmation

•Document Examination (limited)

•Scanning

•Analytical Procedures

•Fraud Investigation

What are the purpose of audit documentation?

•Integral part of audit quality

•Nature, timing and extent of work performed

•Professional judgments

•Basis for conclusion

•Facilitates planning, performance and supervision

•Provides basis for review

How should documents be retained?

•Seven years from report release date.

–If no report—from last day of fieldwork

•Additions/Amendments

–Documentation may not be deleted or discarded after report release date.

–Additions must indicate

•Date the information was added,

•Name of preparer

•Reason

What are audit programs?

•List of audit procedures to be performed to gather sufficient appropriate evidence.

•The program contains the procedures used for gathering evidence on mgmts assertions (PERCV) about amounts & disclosures in the financial stmts.

•Each audit program is based, in part, on the output of Audit Risk Model.

•Generally one for each major cycle or account.

-Revenue and collection, acquisition and expenditure, production and conversion, finance and investment.

•Signed off as procedures are performed.