Introduction to management accounting

1/13

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

14 Terms

Operational budgets: For sales revenue budget what 2 things do you need?

Budget sales, sales price

Operational budgets: What do you add and take away for production budget

budgeted sales - opening inventory + closing inventory

Operational budget: how do you work out material usage?

Budget usage (mats used in budget) - opening inventory + closing inventory

Average time per unit to produce Y units=

no. units x (time to produce first unit x cumulative no. units^leaning index)

Learning index= Log (learning index decimal)/ Log(2)

What is the high low method

Total cost= total fixed cost + variable cost per unit x no. units

BUT variable cost is cost= cost at highest units - cost at lowest units/ high units - low units

Contribution margin=

selling price per unit - variable cost per unit

Ratio= contribution margin per unit / selling price x100

Break even point

Units: total fixed cost/ contribution per unit

Revenue: Fixed cost/ contribution margin ratio

Margin of safety

Units: Budget units- break even units

%: budget sales- break even sales / budget sales x100

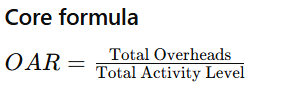

what does the overhead absorption rate show

An overhead absorption rate (OAR) shows how much overhead cost (indirect costs like rent, utilities, supervision) is charged to each unit of activity—for example per labour hour, machine hour, or per unit produced

Discount factor=

1/(1+r)²

Sales volume contribution variance =

(Fixed volume – Flexed volume) x Standard unit contribution

Materials Price Variance=

(Actual Price−Standard Price)×Actual Quantity

Pay back time

start of no. years + difference in cost of initial investment and latest year/ total of year

Like linear interpolation

Internal rate of return

look at 2 different discount values then do linear interpolation