FIN 391 Test 2 Chapters 6-8

1/59

Earn XP

Description and Tags

FINAL EXAM for FIN 391

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

60 Terms

What is Estate Tax?

AI: The estate tax is a federal tax levied on the transfer of a person's assets after their death. Often called the "death tax," it is paid by the estate itself before any assets are distributed to heirs.

What is gross estate?

It is the starting point, before any deductions.

By definition: “The FMV of all interests owned by the decedent at the time of death.“

may also include certain property interests the decedent transferred during their lifetime, as well as the decedent’s interest in any jointly held property and, in some cases, the proceeds of life insurance on the decedent’s life.

The “adjusted gross estate” (AGE) is the gross estate less certain allowable deductions.

What is taxable estate?

The “taxable estate” is the AGE less the unlimited marital and charitable deductions and the state death tax deduction.

Important Part for the Final Exam

This vocabulary is important. If an exam question states that the taxable estate is $16 million and there was a $2 million bequest to a charity, the charitable bequest has already been subtracted when calculating the $16 million. If you subtract it from the $16 million, you might think there is no estate tax since they are below the $15 million exemption (in 2026), but that is not true. You don’t want to tell a client that they have no estate tax and then have them get a tax bill for $400,000 (40% of the $1,000,000 over the exemption).

Side Note:

Under TCJA, the estate tax exemption (as indexed) was $13.99 million in 2025 and was scheduled to sunset to the pre-2018 base of $5 million, indexed for inflation, in 2026. OBBBA 2025 reset the base exemption at $15 million in 2026 (to be indexed for inflation beginning in 2027).

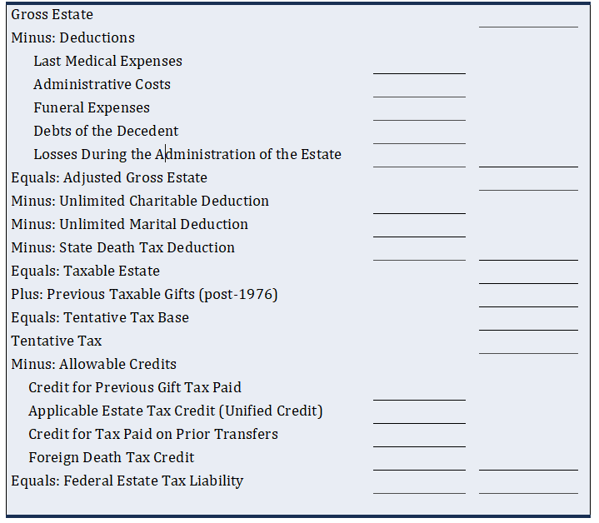

Estate Tax Formula

Gross Estate

Minus: Deductions

Last Medical Expenses

Admin Costs

Funeral Expenses

Debts of the Decedent

Losses During the Administration of the Estate

Equals: Adjusted Gross Estate

Minus: Unlimited Charitable Deduction

Minus: Unlimited Marital Deduction

Minus: State Death Tax Deduction

Equals: Taxable Estate

Plus: Previous Taxable Gifts (post-1976)

Equals: Tentative Tax Base

Tentative Tax

Minus: Allowable Credits

Credit for Previous Gift Tax Paid

Applicable Estate Tax Credit (Unified Credit)

Credit for Tax Paid on Prior Transfers

Foreign Death Tax Credit

Equals: Federal Estate Tax Liability

The Gross Estate (Code Sections)

•2033 – Property owned at death

•2034 – Dower and curtesy interests

•2035 – Gift tax paid within 3 years of death, and

• – Gifts made within 3 years of death under 2036, 2037, 2038, and 2042

•2036 – Transfers with a retained life interest

•2037 – Transfers with a reversionary interest

•2038 – Revocable transfers

•2039 – Annuities

•2040 – Jointly owned property

•2041 – Powers of appointment

•2042 – Proceeds of life insurance

•2044 – QTIP property

Important note: Property interests included in a decedent’s gross estate are defined in Sections 2033-2044 of the IRC.

Code 2033: Property Owned at Death

All property in which the decedent had an interest at their date of death

Rental income accrued before death

Cash surrender value of a life insurance policy owned on the life of another (included in FMV)

Examples:

Life insurance policies with named and alive beneficiaries are not in the probate estate but are included in the federal gross estate.

Business Partners (usually buy and sell to buy out the partner’s wife/husband) = Buy-Sell Agreement

More on Code 2033: Property Owned at Death

State income tax refunds

Medical insurance reimbursements

Awards for paid and suffering (but not wrongful death)

Only the decedent who suffered the pain and suffering is included in the decedent’s gross estate, as it was awarded to the decedent only

Pain and suffering – Decedent who suffered pain and suffering – included in the decedent’s gross estate.

Wrongful death - Awarded to decedent’s surviving family, therefore, not included in decedent’s gross estate.

Considered to be a “catch-all” provision

Examples of this are: Cash, Stocks, Bonds, Retirement Accounts, Autos, Clothes, Etc.

Important to Remember:

The GROSS ESTATE is ALWAYS GREATER THAN or EQUAL to the PROBATE ESTATE.

GROSS ESTATE > OR = PROBATE ESTATE

Code 2034: Dower and Curtesy Interests

Dower:

Originally, the right of the wife to receive a life estate between 1/3 and ½ of the land owned by the husband at the husband’s death if one or more children were born

Now more in line with curtesty (life estate in land)

Curtesy:

Husband’s right to receive a life estate in land owned by the wife at the wife’s death if one or more children were born.

More on Code 2034: Dower and Curtesy Interests

Many states have a spousal right to elect against the probate estate instead of dower or curtesy

Prevents the spouse from being completely disinherited.

Code 2035: Any gifts tax paid on gifts made within 3 yrs of the decedent’s date of death.

Any gifts tax paid on gifts made within 3 yrs of the decedent’s date of death.

Not the actual amount of the gifts

Gifts given within the last 3 yrs if the gift was a:

2036 - Transfer with a life estate

2037 - Transfer taking effect at death

2038 - Revocable transfer

2042 - Transfer of life insurance on the life of the decedent

Premiums paid on a life insurance policy not owned by the grantor are not included under section 2042

Must live 3 yrs otherwise included in gross estate

More on Code 2035: Any gifts tax paid on gifts made within 3 yrs of the decedent’s date of death.

Disclaimer:

GRAT where the grantor receives income for a 10-year term. The grantor does not have to live for an additional 3 years at year 10. Rather, the three-year rule applies when you have a retained life estate (included in your gross estate under Sec, 2036) and you give away that right within 3 years of death.

Examples:

If assets of $1,000,000 were given away as taxable gifts last year and gift taxes were paid, ($400,000 in gift taxes paid, will reduce the gross estate (GE) by the amount of gift taxes paid), so the IRC requires that it be added back in.

Kristen owns family farm and lives in the farmhouse on the property. She gifts ownership of the farm to her son, Kit, but retains the right to live on the property for the rest of her life. She decides to move to a retirement community and gifts the right to live on the farm for the rest of her life to her brother, Dax. If Kristen dies within 3 years of the gift of the retained life interest to Dax, the value of the property will be included in her gross estate.

Code 2035: Transfers with a Retained Interest

Property transferred where the decedent retained an interest: Express or implied understanding

Retained interest for life

Retained interest for period not ascertinable without reference to death

Ex: I will retain the interest until the day before I die

Reserved for period that does not end before death

Ex: Reserves for a period of 10 years but dies in year 5

More on Code 2035: Transfers with a Retained Interest

Retained life interest versus life estate: retaining a life interest in property you previously owned (e.g., you establish a trust and retain the right to income from the trust for life) results in inclusion in your gross estate. Being given a life estate from someone else (e.g., you get income for life from a trust set up by your uncle) is not included in your gross estate.

2037: Transfers Taking Effect on Death

Property transferred where:

Possession of enjoyment requires the beneficiary to survive the decedent

Decedent has retained a reversionary interest

Value of reversionary interest is >5%

The FMV of a decedent’s reversionary interest is calculated immediately before death, and election of the alternative valuation date is not available.

If less than or equal to 5%, then it is considered de minimis.

2038: Revocable Transfers

Interest subject to the power of the decedent to alter, amend, revoke, or terminate

Also applies to affecting the time or manner of enjoyment of property or income, even if the identity of the beneficiary is not affected

Side Note: Revocable living trust - Can revoke, so while it is effective for avoiding probate, it is still included in gross estate (i.e., strings attached).

More on 2038: Revocable Transfers

Does not apply if:

Transfer was for full and adequate consideration, or

Power can only be exercised with the consent of all parties in the transferred property, or

Power held solely by another person, or

Power to remove a trustee and replace them with a trustee that is not related or subordinate to the grantor/decedent.

The ability to change a beneficiary or the income streams to beneficiaries would render the transfer includable in the gross estate (exception: if approval from all beneficiaries is required).

2039: Annuities

Straight Single-Life Annuity - Not Included in annuitant’s/decedent’s gross estate

An annuity is paid to the annuitant until their death.

(since the annuitant’s interest in the contract terminated at death and no other annuitant receives payments after the death of the decedent/annuitant).

Survivorship Annuity - Included in the first annuitant’s/decedent’s gross estate at the FMV of the remainder interest (i.e., the value of a comparable policy on the surviving annuitant)

An annuity that provides payments to one person, and then provides payments to a second person upon the death of the first.

When the first annuitant dies, the value of a comparable policy on the second annuitant is included in the first annuitant’s gross estate.

If the second to die has contributed to the purchase of the policy, then only the proportionate value of the annuity is included in the gross estate of the first to die.

2040: Jointly Owned Property

JTWROS

Tenancy by the entirety

Remember - Contribution Rule!

Included at percentage of actual contribution (except for spouses, due to their presumed 50%/50% contribution).

See Examples: 6.18-6.21

Fee simple retitled JTWROS with Jeff, where Bridget owns 50% and Jeff owns 50%; 100% included in Bridget’s gross estate, because she contributed 100%. However, this rule does not apply to Tenants In Common (TIC) ownership by spouses. TIC inclusion is based on the percentage ownership of the decedent.

2041: Powers of Appointment

General Power of Appointment:

Power holder can appoint assets to themself, their creditors, their estate, or their estate’s creditors - Included in gross estate (GE)

General POA is generally given to the spouse because of the unlimited marital deduction

Example:

Gia appoints Daniel as the power holder (can appoint assets to himself, his creditors, his estate, or his estate’s creditors, then considered general POA), which is included in Daniel’s GE, if Daniel dies with the general POA (even though Gia technically owns the assets).

If Gia dies first, then this is not at issue.

More on 2041: Powers of Appointment

Except if the power is subject to an ascertainable standard (HEMS):

Health

Education

Maintenance

Support

HEMS (ascertainable standard) presumes that the appointed property will be consumed rather than transferred by power holder.

Thus, no transfer tax to appointee.

2042: Proceeds of Life Insurance

Proceeds receivable by the decedent or decedent’s executor = Includable in Gross Estate

Decedent/insured possessed an incidence of ownership in the policy = Included in Gross Estate

Owned it, or

Right to:

change beneficiary,

surrender or cancel policy,

assign policy,

revoke an assignment, or

pledge the policy for a loan

More on 2042: Proceeds of Life Insurance

If the beneficiary receives the life insurance proceeds but is required to remit money to the decedent’s estate to pay taxes, debts, etc., then also part of the decedent’s GE.

An irrevocable life insurance trust (ILIT) may have the right (not obligation) to loan money to the decedent’s estate without adverse estate tax consequences;

However, an ILIT should not be “required” to loan money or buy assets from the estate because this will cause inclusion in GE.

Example:

Kristi is the owner and insured of a life insurance policy. Greg is the listed beneficiary of the life insurance policy on Kristi’s life. Kristi dies. Is there probate estate inclusion here? No. But the death benefit (DB) is included in Kristi’s gross estate because she owned the policy on her own life.

Note: If Kristi owned a life insurance policy on someone else (Paul), and then Kristi dies, the value of the policy may be included in her GE under Sec. 2033 (valued at interpolated terminal reserve, not DB), which will be reviewed in Chapter 11

2044: QTIP Property

Property for which a QTIP election was made in the gross estate of the first-to-die spouse is included in the gross estate of the second-to-die spouse

More on 2044: QTIP Property

Example:

Two spouses, Olivia and Benson, are married. At Olivia’s death she leaves assets in trust with a QTIP (Qualified Terminable Interest Property) election, where Benson gets an income interest, and Olivia’s children from a prior marriage get the remainder interest. This transfer qualifies for the unlimited marital deduction at Olivia’s death and is included in the gross estate for estate tax purposes at Benson’s death (i.e., inclusion is deferred until the surviving spouse’s death).

Valuation of Assets

FMV at date of death (or alternate valuation date)

Real Estate

Appraisals

Closely Held Business

Minority interest

Lack of marketability

Key person

Publicly-Traded Securities

Average of high and low on the date of death (or alternate valuation date)

Blockage discount

What is Alternative Valuation Date?

6 months after the decedent’s date of death

Executor must make the election by the filing date of the estate tax return

Election must lower the gross estate and estate tax due

Election applies to all assets in the gross estate

Exceptions:

Wasting assets

Def: Assets that lost value based on the nature of the asset (not necessarily economics), such as an installment note, copyrights, patents, annuitized annuities, etc.

Assets disposed of between death and the alternate valuation date are included at the FMV as of the date of disposition (sold, distributed to heirs, or otherwise disposed of)

Why does Real Estate need appraisals?

In practice, an appraisal for real estate may depend on the size of the estate.

If the estate is subject to estate tax, consider filing and disclosing the valuation and appraisal to get the statute of limitations running.

Statute of Limitations is generally 3 years, 6 years for 25% understatement, and none for fraud

Why is there an valuation of assets for a closely held business?

Closely held business interests will require an appraisal.

What happens in a Minority Interest Discount?

A minority share in a business is worth less than a majority share’s interest (due to a lack of control over the business).

Example: If a business is worth $1,000,000, would you pay $100,000 for a 10% interest?

Probably not, since a 10% interest is likely worth less than $100,000

Note, this discount is used in gift planning situations.

What happens in a Lack of Marketability Discount?

Not as marketable as say a listed security, such as Microsoft, which would be easy to sell.

What happens when in a Key Person Discount?

If the business rainmaker dies, then the value of business may also decline.

What happens in a Blockage Discount?

Large volumes of publicly listed stock that if sold all at once would make the stock price decline.

More Valuation of Assets

Financial Securities

Average of the high and low FMV on the date of death (or alternative valuation date)

Accrued Interest - Included in gross estate as IRD

Accrued Dividends - Included in gross estate as IRD

Stock that is not actively traded

Formula for Valuation of Assets

If the there were no trades on the date of death, the value is a weighted average of the value (average of high and low) on the last trade date before and the next trade date after the date of death.

Example of Valuation of Assets

Date of Death is Wednesday, February 4th.

The stock did not trade on date of death.

The stock traded on Monday, February 2nd and on Tuesday, February 10th. On February 2nd, the high was $29 and the low was $19, and the closing price was $28.50.

On February 10th, the high was $32, the low was $28, and the closing was $32.

What is the value of date of death?

((Trading price after death *Number of days between date of death and 1st preceding trade) + (Trading price before death *Number of days between date of death and next subsequent trade))/the sum of days before and after death

Feb 2: ($29+$19)/2 = $24

Feb 10: ($32+$28)/2 = $30

Feb 2 to Feb 4 is 2 days

Feb 4 to Feb 10 is 4 days (weekends don’t count)

(($30 × 2 days)+($24 × 4 days))/(2 days + 4 days)

($60 + $96)/ 6 days = $26.00

Last on Valuation of Assets

Life Insurance

Policy on others

If in a premium pay status/ordinary life policy, the replacement cost is interpolated terminal reserve + unearned premiums

If paid up policy, the replacement value is what it would cost today to fully buy that same policy in one payment for the same coverage and age.

Policy on decedent’s life

Generally, the death benefit if policy on the decedent’s life and owned by the decedent (or assigned within three years of the decedent’s death)

Example on Alternate Valuation Date

Andre dies with an adjusted gross estate (AGE) of $16M, leaving $7.60M to his B trust, $3M to his church, and $5.40M to his wife. Can his executor elect the AVD?

No, because there is no transfer tax due to the exemption equivalent of the applicable credit, the marital estate tax deduction, and the charitable estate tax deduction.

That $7.60M Amount covers the applicable credit

The marital estate tax deduction and the charitable estate tax deduction are fully deductible

There is nothing to save by changing dates, so no reductions

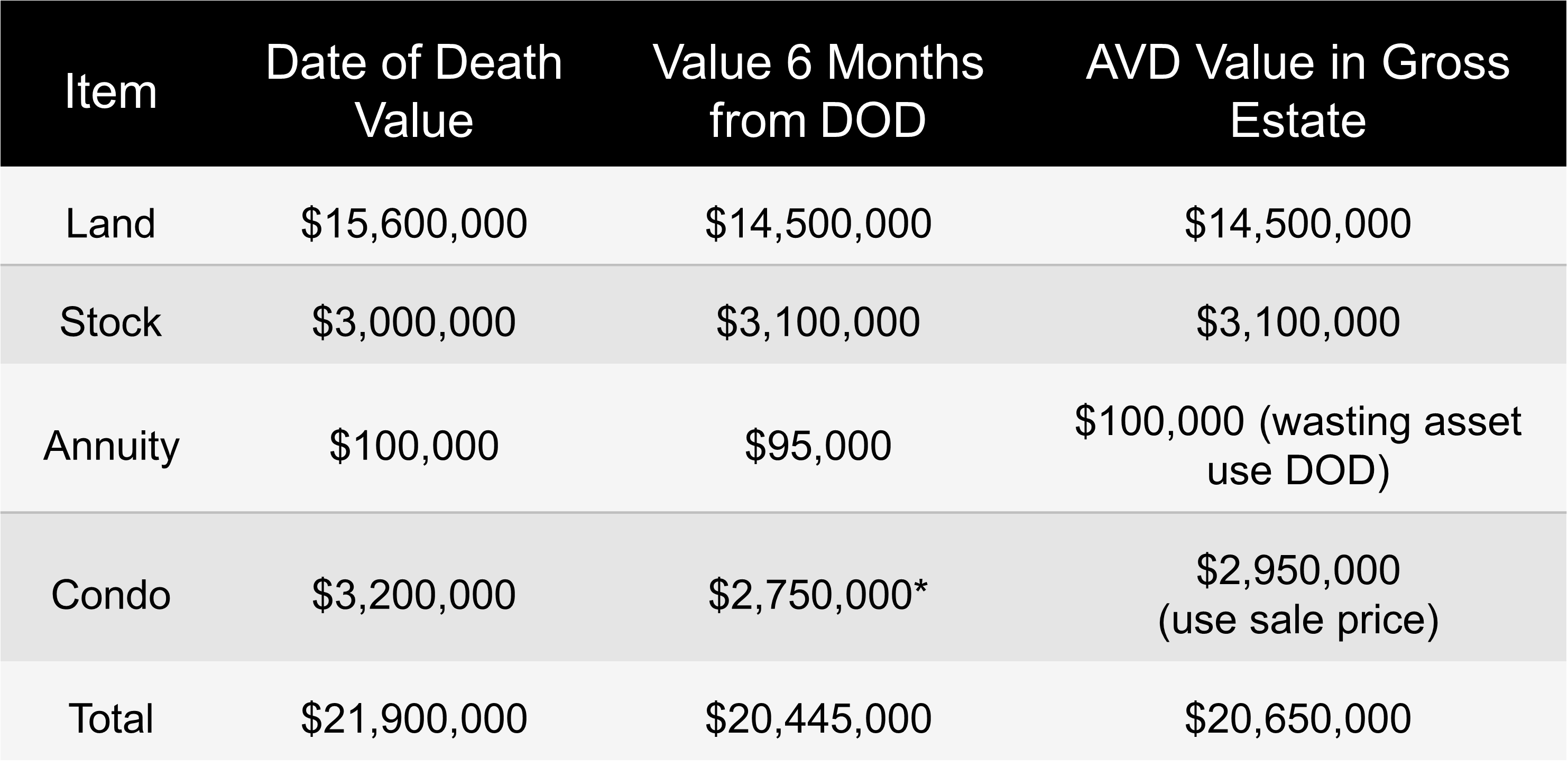

Another Example on Alternate Valuation Date

Only use the AVD if trying to reduce things:

Land Value after DOD = included in the value at Gross Estate

The land was still owned by the estate 6 months after death, so under the AVD rules, you use the FMV 6 months after death.

Stock Value after DOD = included in the value at Gross Estate

Despite the stock increasing in value after death. Under AVD rules, if the asset is still held at 6 months, you must use the value at that date — even if it went up.

You do not selectively choose the lower value asset-by-asset. The election applies to the estate as a whole.

Annuity → $100,000

The annuity is labeled a wasting asset.

Wasting assets are items whose value naturally declines simply because time passes (like annuities, patents, leases, life estates, etc.).

For wasting assets, the IRS requires using the DOD value, not the later lower value caused merely by the passage of time.

Condo → $2,950,000

DOD value: $3,200,000, Value at 6 months: $2,750,000, & Sold after 2 months for $2,950,000

When an asset is sold before the 6-month alternate valuation date, the estate uses the actual sale price, not the later 6-month value.

Because the condo was sold 2 months after death, that becomes the AVD value included in the gross estate.

Total Gross Estate Using AVD

Add the included AVD amounts:

14,500,000+3,100,000+100,000+2,950,000 =20,650,000

That is why the alternate valuation gross estate equals:$20,650,000

instead of the original DOD gross estate of:$21,900,000

Since the overall estate value declined, the executor may elect the alternate valuation date if it also lowers estate tax liability.

Side note: Note that if no estate tax is due (e.g., estate is below exemption, or all assets go to spouse and qualify for marital deduction) the cannot use the AVD - the gross estate (GE) (not asset-by-asset but the entire GE) and the taxes due must also decline in value.

Deductions from the Gross Estate:

Funeral Expenses

Last Medical Expenses

Administration Expenses

Debts

Losses during Administration

Mnemonic for Deductions from the Gross Estate

A = Administrative Expenses

B = Burial Expenses

C = Casualty Losses

D = Debts (including medical expenses)

Funeral Costs

Reasonable Expenditures:

Funeral

Burial plot

Grave markers

Transportation of body

Future care of burial site

THIS DOES NOT INCLUDE TRAVEL EXPENSES FOR FAMILY TO ATTEND FUNERAL.

Last Medical

Costs related to the last illness (not covered by insurance)

Postmortem planning - Can include options in terms of where to claim the deductions (i.e., Forms 1040 for surviving spouse, 1041,706)

Medical expenses not tax reduction productive on final Form 1040 unless > 7.5% of return’s AGI

Medical expenses not tax reduction productive on Form 706 unless taxable estate

In many cases, medical expenses do not generate any tax reduction at all

CANNOT have been deducted on decedent’s final income tax return

Administrative expenses:

Expenses actually and necessarily incurred in administering the estate.

Examples are expenses related to:

Collection of assets

Payment of debts

Distribution of property

Attorney and accounting fees

Appraisal and valuation

Debts

Debts the decedent was obligated to pay

Examples include:

Outstanding mortgages

Income tax due

Gift tax due

Credit card debts

Monthly service providers (gas, electric, phone bills)

Discuss obligated to pay versus “loans” to family

Losses during Adminstration

Casualty and theft losses if not compensated for the loss by insurance

Must be incurred during the administration of the estate

If after death, can be included on Form 1041 or Form 706 as a loss during administration of estate.

Unfortunately, if before death, these losses would be included on the decedent’s final income tax return (Form 1040).

Post 76’ Adjusted Taxable Gifts in the Estate Formula

Review again the cumulative (unified) nature of gift and estate taxation.

During lifetime you were filling a bucket with “taxable gifts.”

You don’t get a new bucket when you die, the taxable estate goes into the same bucket you were filling during your lifetime.

Gifts included in the gross estate (for example, due to a retained life interest) are not included as taxable gifts; therefore, no double-counting occurs.

Post-1976 gifts are added back at the fair market value as of the date of the gift.

These values can be directly determined from an individual’s previously filed gift tax returns.

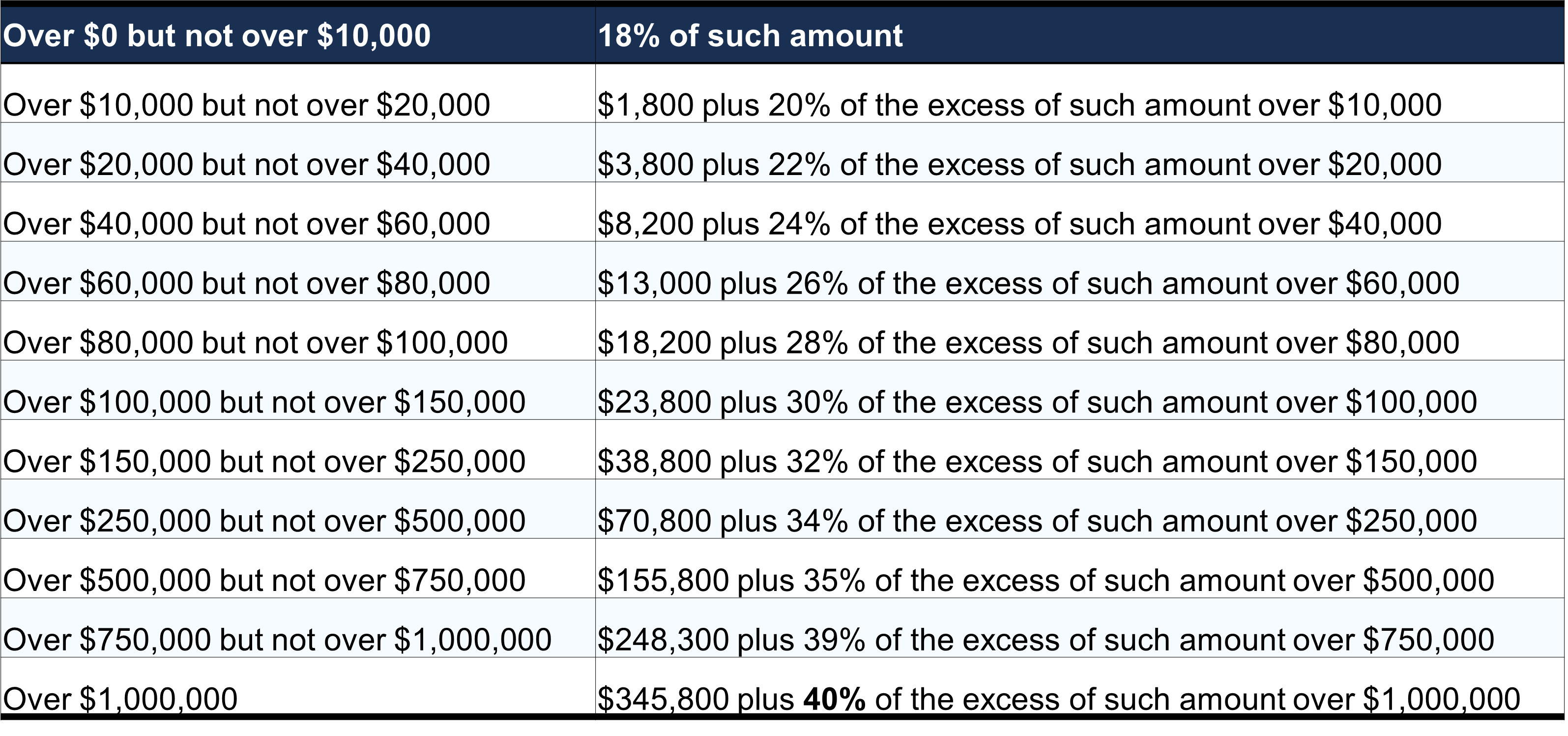

Tentative Tax: Estate Tax Rate Schedule (2013-2026)

The tentative tax is the total transfer taxes, estate and gift, on all property transferred by the decedent during their life and at their death.

The tentative tax is reduced by the total gift tax paid during the individual’s life, or payable on gifts included in the tax base (calculated at date of death tax rates, less the unified credit applied in the year of the gift) to give the decedent credit for the tax paid on the post-1976 taxable gifts added when determining the tentative tax base.

Note that the gift taxes are recalculated using the rate schedule for gifts that is in effect at the time of the decedent’s death. Thus, the amount subtracted is not the actual gift taxes paid, but the amount of gift taxes that would be payable if the decedent had made the gifts on the date of death

The tentative tax is then reduced by certain tax credits.

REMEMEBER: ANYTHING OVER $1,000,000, IT IS $345,800 + 40% OF THE EXCESS OF SUCH AMOUNT OVER $1,000,000

Credits

Applicable Estate Tax Credit:

$5,541,800 for 2025

$5,945,800 for 2026

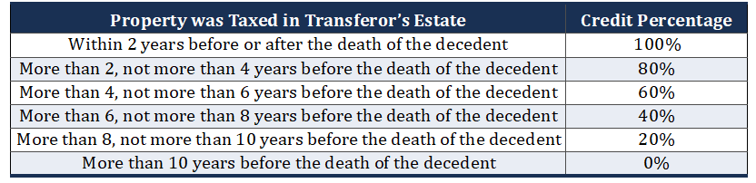

Prior Transfer Credit:

Credit for estate taxes paid within the last 10 years = Included in the Gross Estate

An asset that was included in another decedent’s gross estate (and estate taxes paid) more than 2 years but less than 10 years prior, can qualify for a credit.

Foreign Death Taxes Credit: Tax paid on property outside the U.S.

More on Credits

Within 2 years is 100%

Every 2 years is 20% reduction

Over 10 years is 0%

Estate Tax Liability

Estate tax is paid by the executor or the administrator

If there is no executor or the administrator, then the person in receipt of the property must pay

If the executor distributes to heirs before paying tax, then the executor may be personally liable

Executor must timely file Form 706 and elect to transfer any unused estate tax credit to surviving spouse

Side note: If no probate assets but estate tax is due, then executor will have to get the cash to pay the estate taxes from beneficiaries