PortM P3.3: Allocating the Risk Budget

0.0(0)

Studied by 0 peopleCard Sorting

1/3

There's no tags or description

Looks like no tags are added yet.

Last updated 2:46 AM on 4/15/26

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

4 Terms

1

New cards

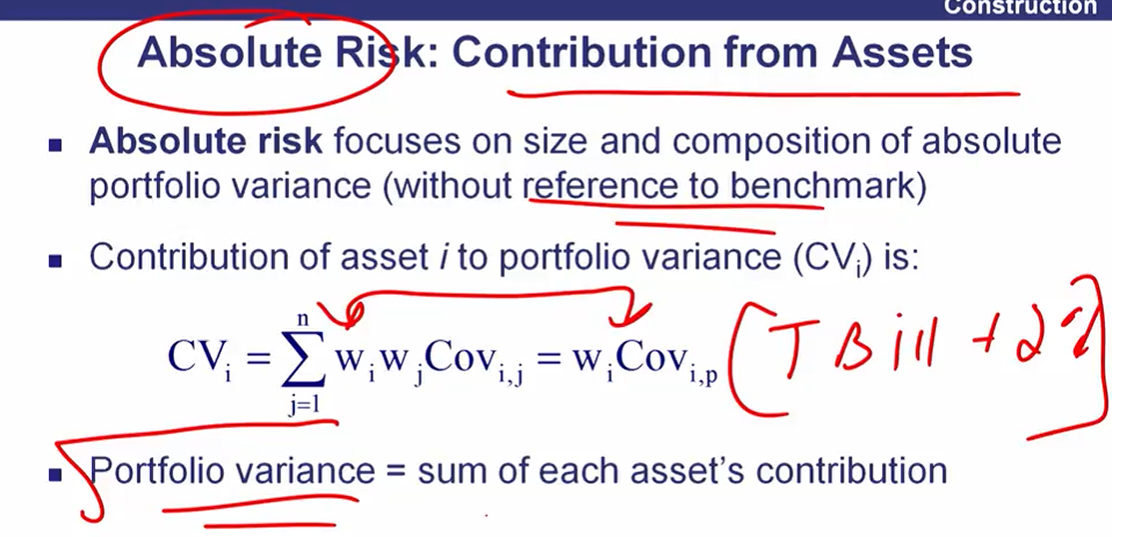

Absolute risk focuses on…

Contribution of asset i to portfolio variance (CVi) is:

Portfolio variance =

2

New cards

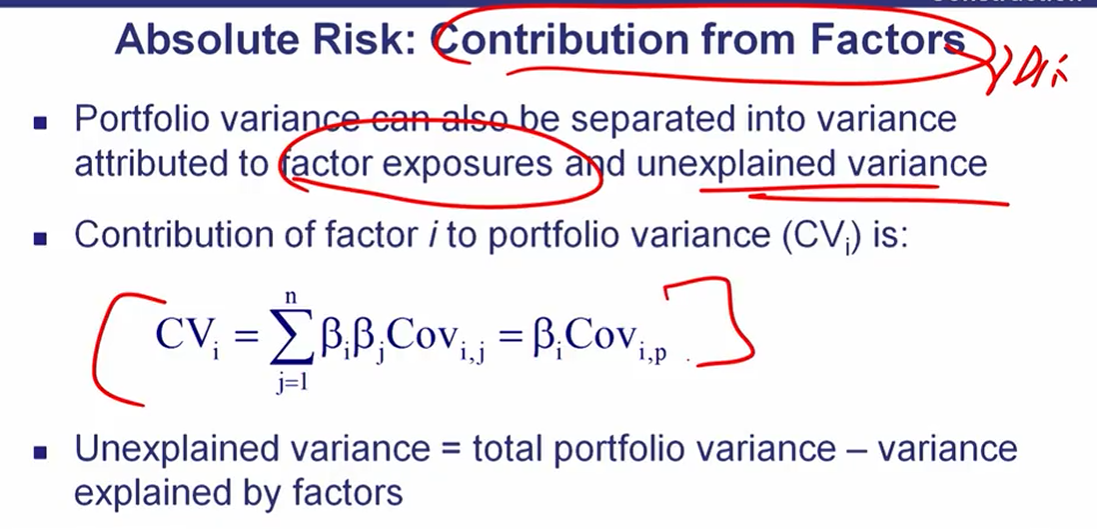

Portfolio variance can also be separated into variance attributed to…

Contribution of factor i to portfolio variance (CVi) is:

Unexplained variance =

3

New cards

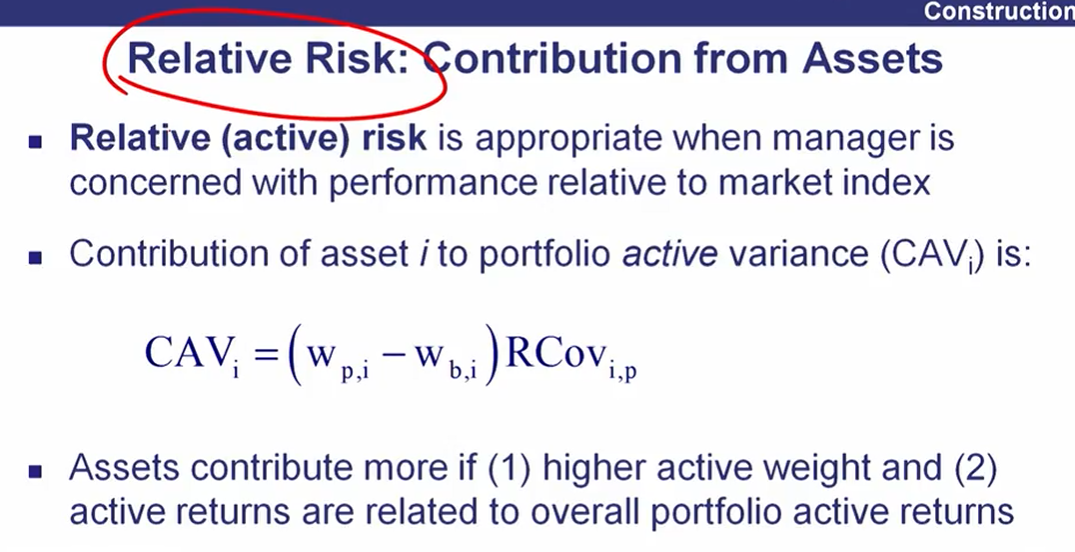

Contribution of asset i to portfolio active variance (CAVi) is:

Assets contribute more if

4

New cards

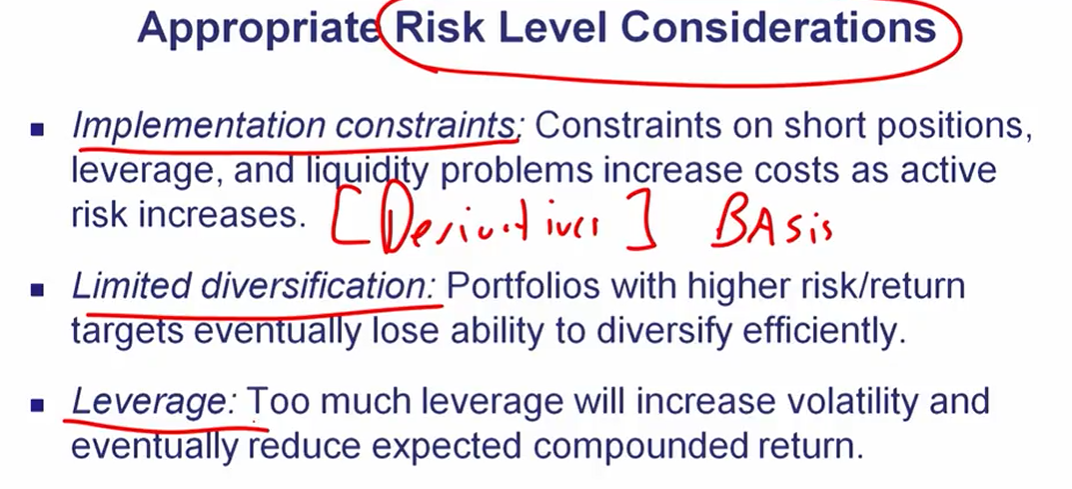

appropriate risk level considerations: