Lecture 11: Financial Options

1/13

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

14 Terms

How do put & call options change with strike prices?

Call option (right to buy) value increases when strike price decreases → valuable when you pay less

Strike price (k) inc → Call value dec, Strike price (k) dec → call value inc

Put option (right to sell stock) value increases when strike price increases → can sell stock at higher price

Strike price (k) inc → put value inc, strike price (k) dec → put value dec

How do put & call options change with stock prices?

Call option (right to buy) value increases when stock price increases → because can pay less

Stock price inc → call value inc, stock price dec → call value dec

Put option (right to sell) value increases when stock price decreases → because you can just sell the stock in the market

Stock price inc → put value dec, stock price dec → put value inc

What are the 4 limits on option prices?

American option can’t be worth less than European counterpart → American can be equally or more valuable

Time value can’t be negative → can only add no value or positive value

Call option can’t be worth more than stock itself → why buy call when can buy stock

C = (S - K, 0 otherwise)

Put option can’t be worth more than strike price

P = (K - S, 0 otherwise)

What is intrinsic value of an option (arbitrage opportunity)?

The value of option if option expired immediately right now

0 = out of the money

other than 0 = in the money

American option can’t be worth less than intrinsic value → otherwise, there’s an arbitrage opportunity if it is worth less!

What is time value of an option?

Difference between option price & intrinsic value → can’t be negative

American price = intrinsic value + time value

option is more valuable when the exercise date is longer! (this is why American option is usually more valuable or equal to European)

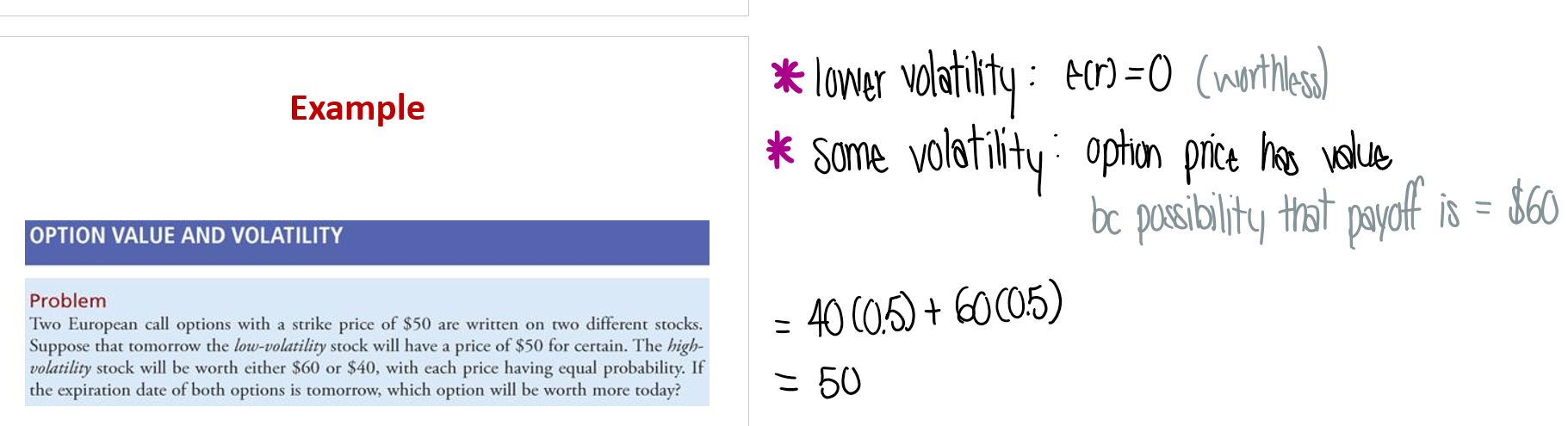

How are option prices related to volatility?

The value of an option increases with the volatility of the stock

lower volatility: expected return = 0 (worthless)

some volatility: option price has value (bc there is a possibility that payoff is $60)

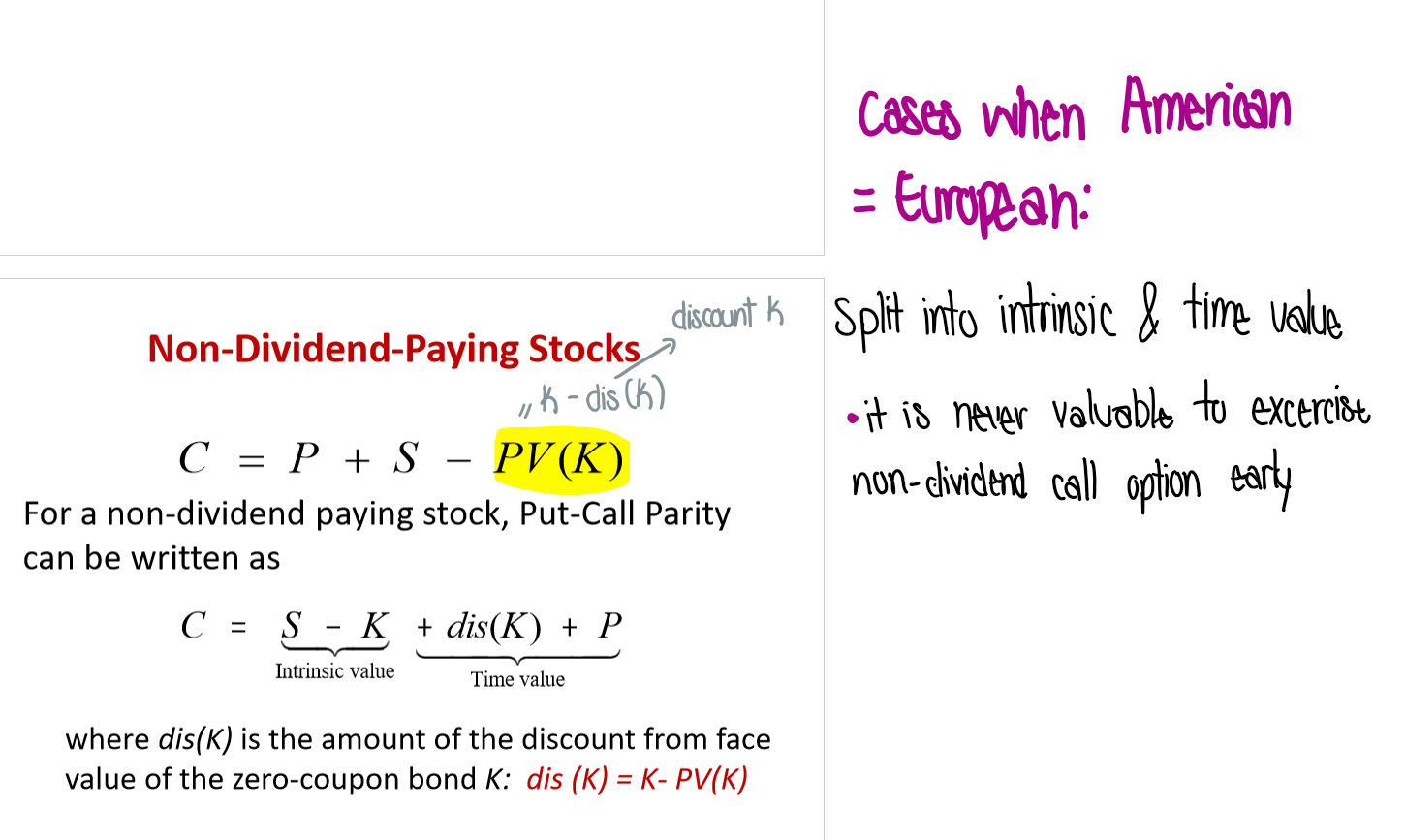

How can call parity without dividends be split into intrinsic & time value?

Never valuable/optimal to exercise non-dividend call option early! → bc price of any call option always exceeds intrinsic value (price is more than the value you get)

European call always has a positive time value bc you can only exercise on expiration date

Negative discount(k) means option can be negative at time value → happens when deep in the money & K is very large (better to buy early than sell in market if deep in the money!)

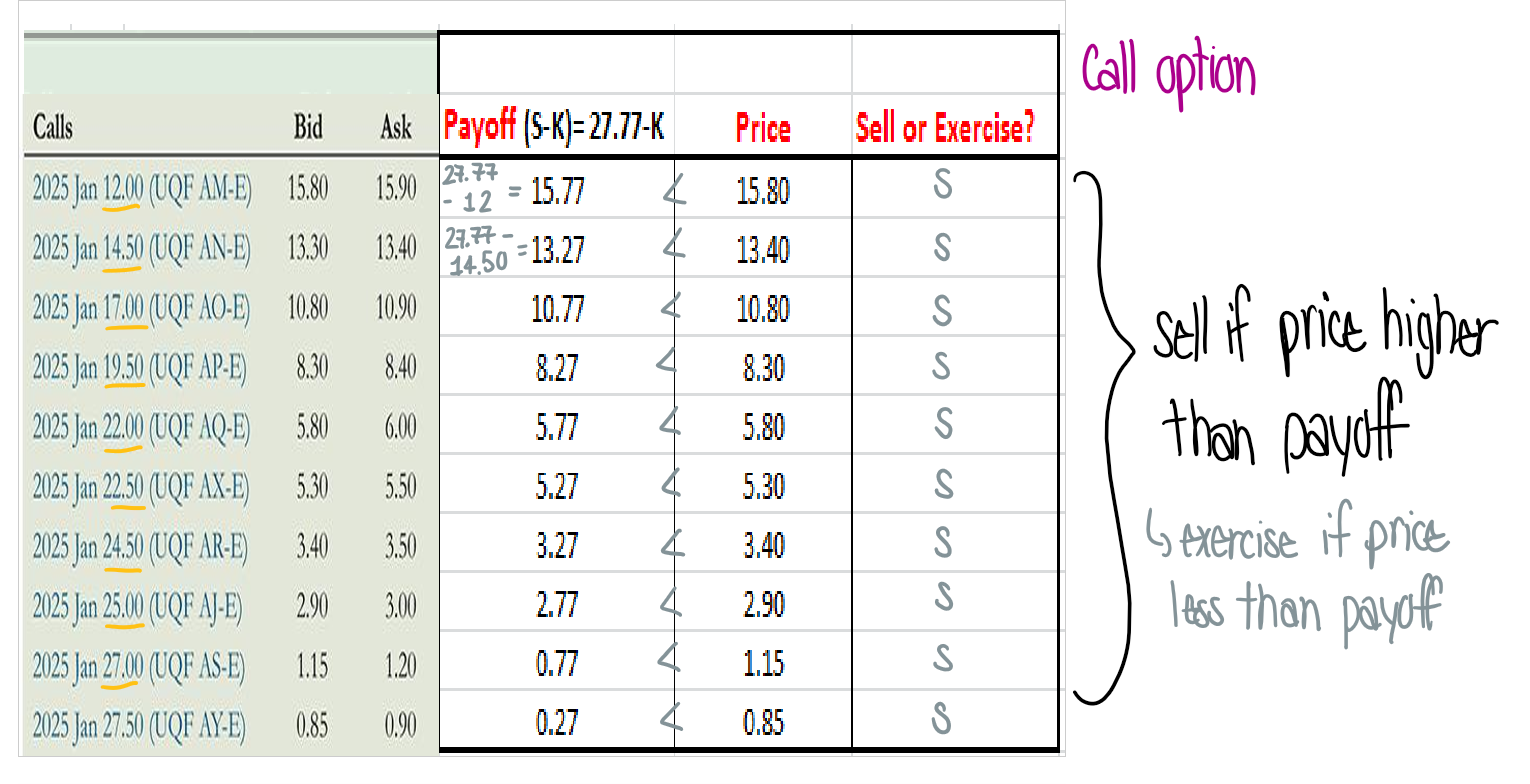

When do you sell or exercise a call option?

Sell → if price is higher than payoff

Exercise → if price is less than payoff

Same for with & without dividends!

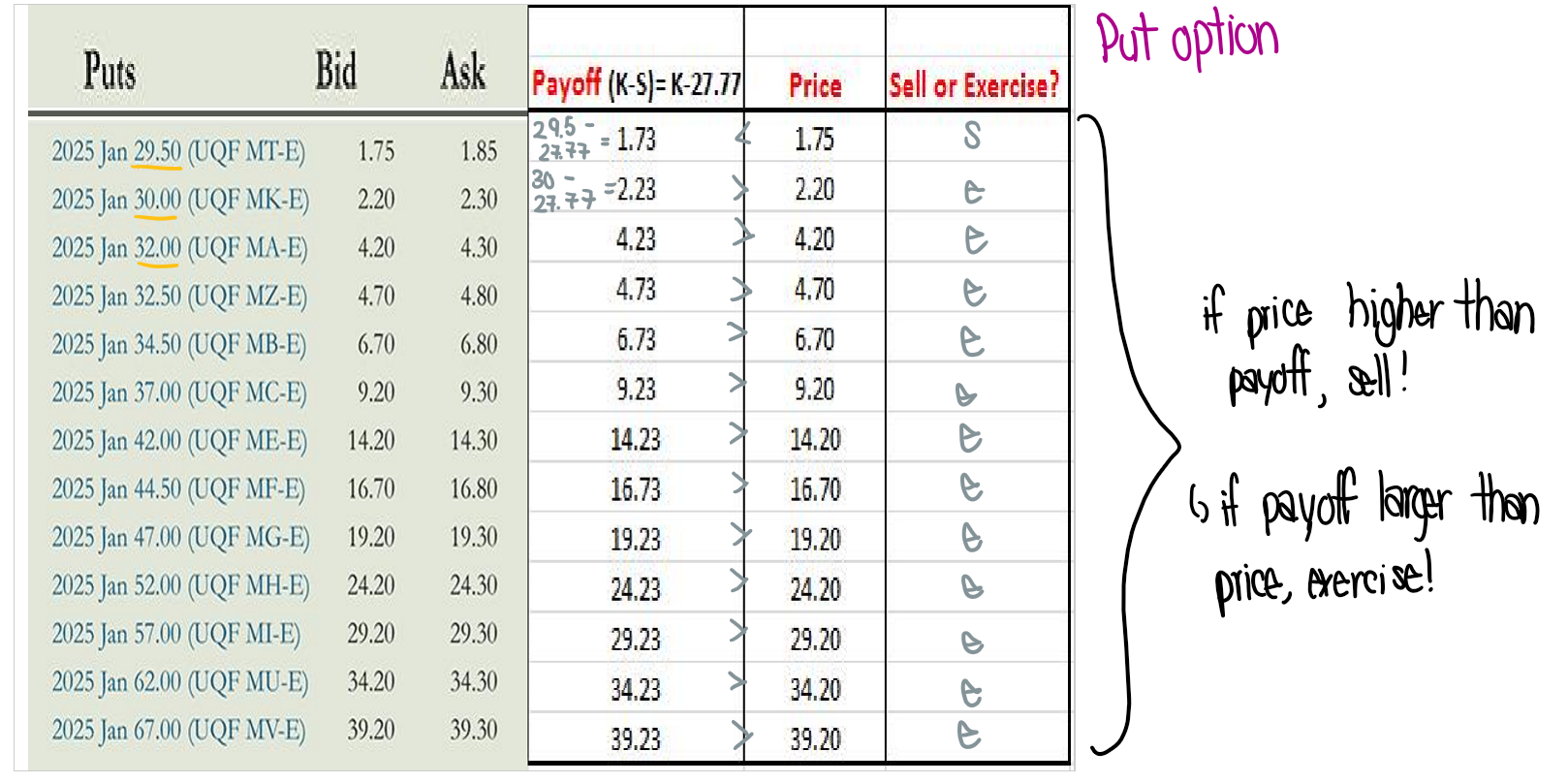

When do you sell or exercise a put option without dividends?

Sell → if price is higher than payoff

Exercise → if price is less than payoff

Same for with & without dividends!

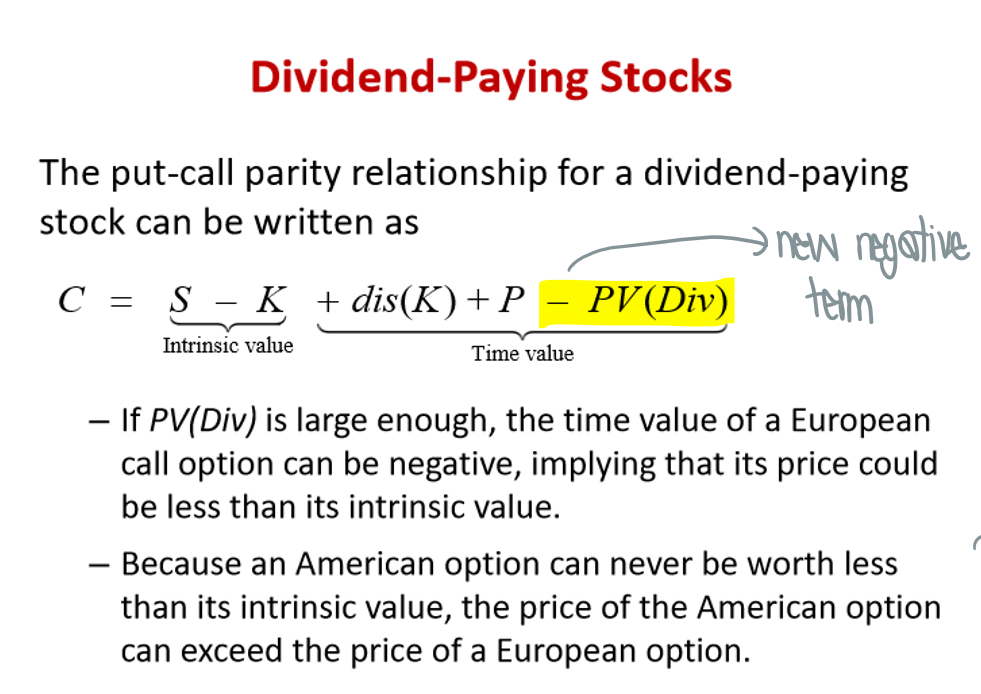

What is the call parity with dividends split into intrinsic & time value?

If time value is negative, better to exercise early! → bc you can capture the dividend itself

If PV(Dividend) is large enough, price can be less than intrinsic value → can’t happen bc arbitrage opportunity

* Sometimes better to exercise early with dividends, never better to exercise early without dividends!

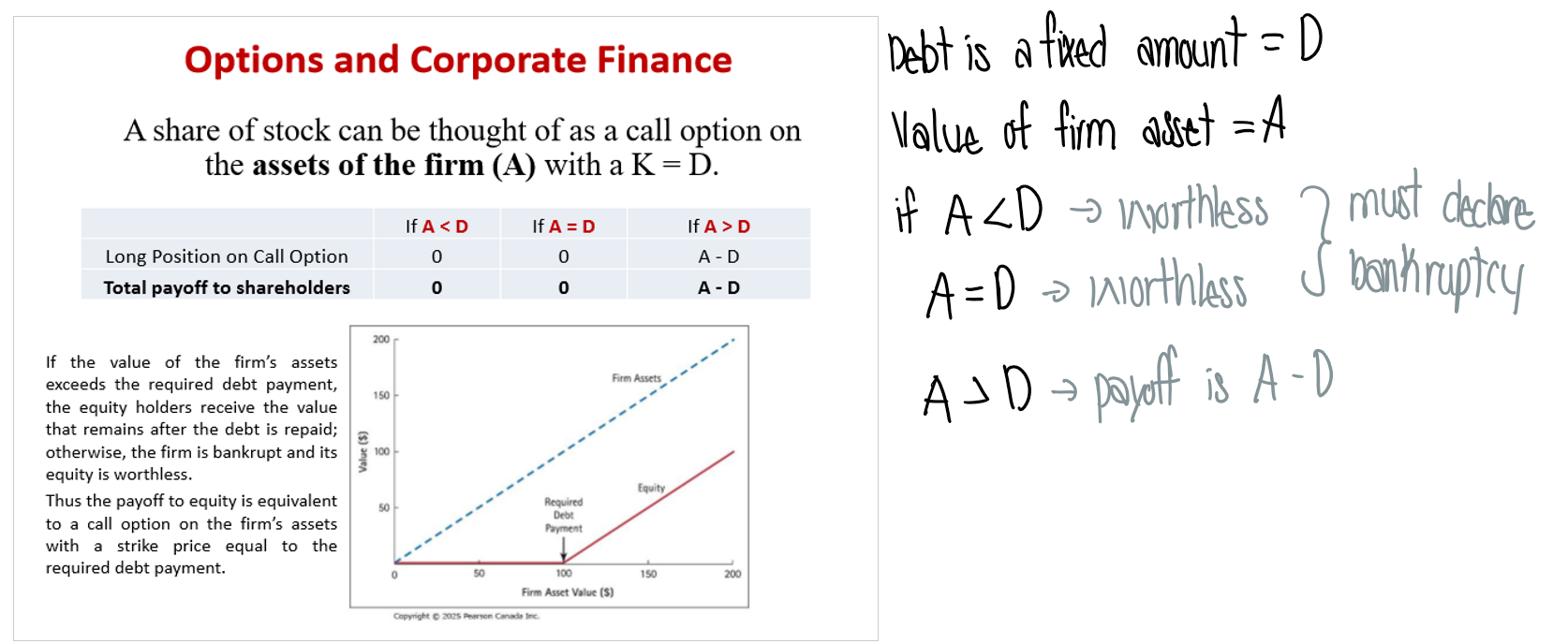

How is call option value related to debt?

When firm value goes down (can’t pay debt) → call option is worthless

After company repays debt, the remaining goes to equity holders/shareholders

D → debt is a fixed amount

A → value of firm asset

If asset less than debt → worthless

If asset = debt → worthless

If asset more than debt → payoff id Asset - Debt

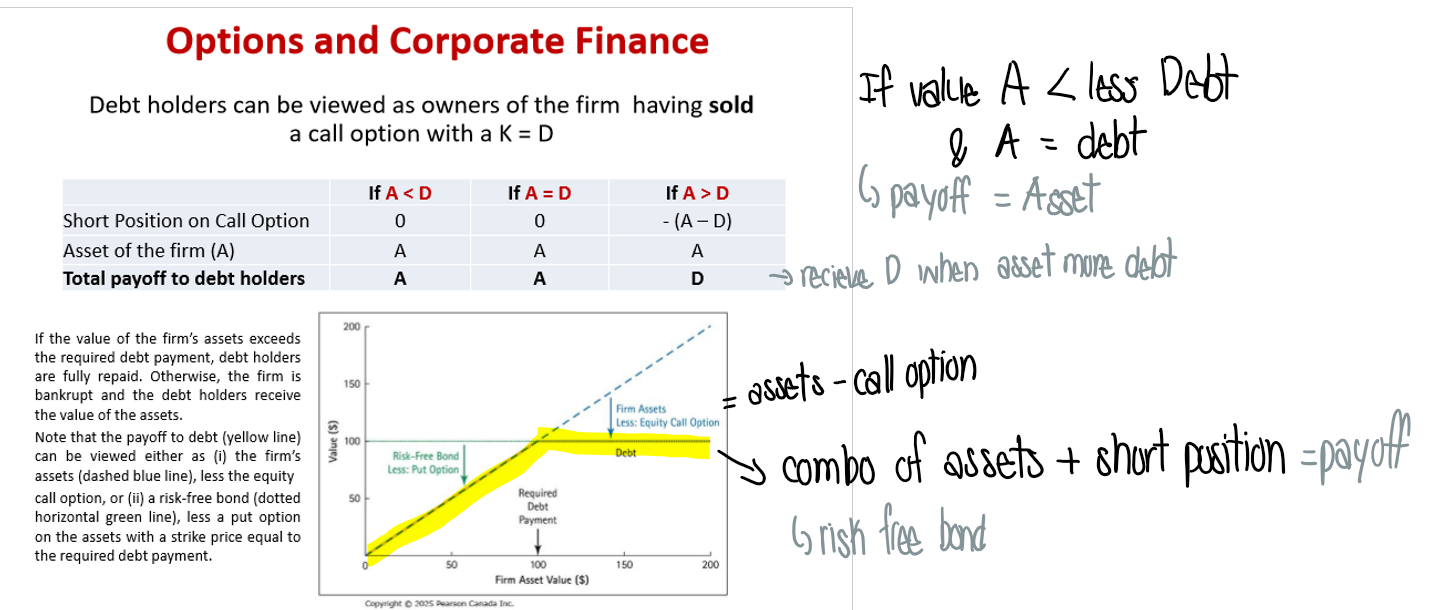

What is debt as an option portfolio?

Debt holders → owner of firm

Owners → sell call option to equity holders

Call option strike price = debt outstanding

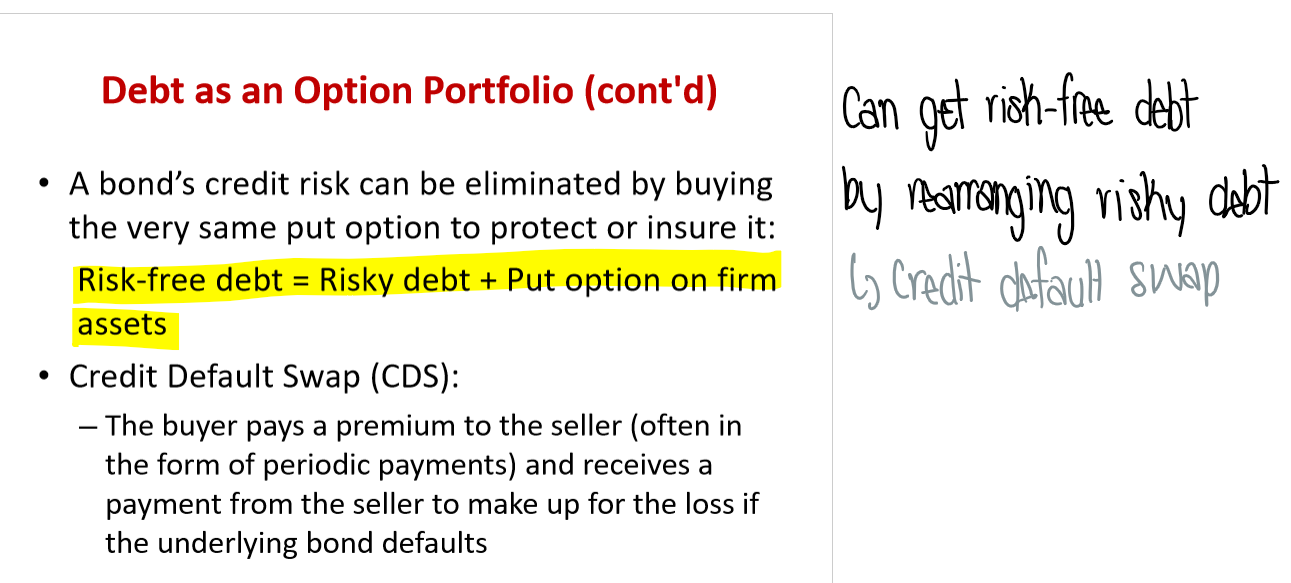

What is risky debt?

Risky debt = Risk-free debt - put option on firm assets

when firm assets are worth less than required debt payment, owner of put option will exercise & receive difference between required debt payment & asset value

If firm value is greater than required debt payment, debt holder only receives required debt payment

How can you get risk-free debt?

By rearranging risky debt

Credit default swap → buyer pays premium to seller & receives payment from seller to make up for loss