7.3 Efficiency & Market Failure

1/42

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

43 Terms

What is Economic Efficiency and what does it represent and consist of

The optimal use of scarce resources so that maximum output and satisfaction is achieved.

Represents the best possible solution to the fundamental economic problem (unlimited wants, scarce resources)

It consists of productive efficiency and allocative efficiency.

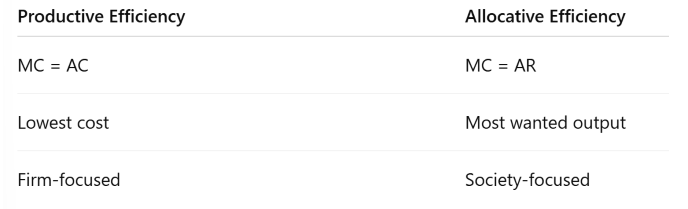

What is Productive Efficiency

Occurs when goods are produced at the lowest possible cost, using the least amount of resources.

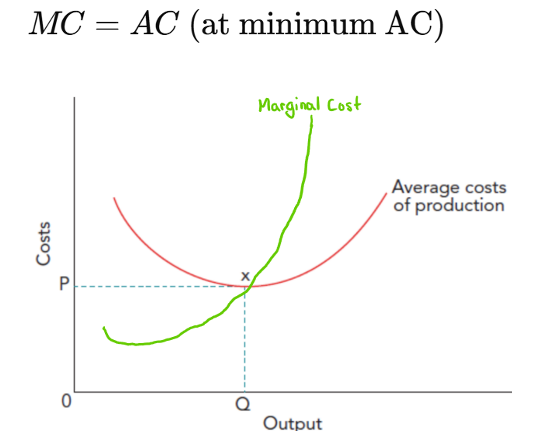

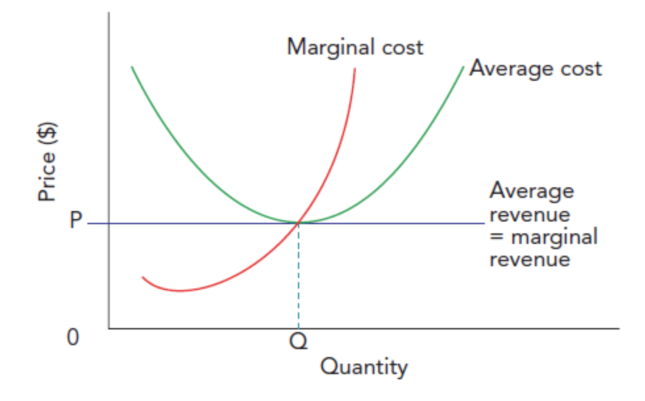

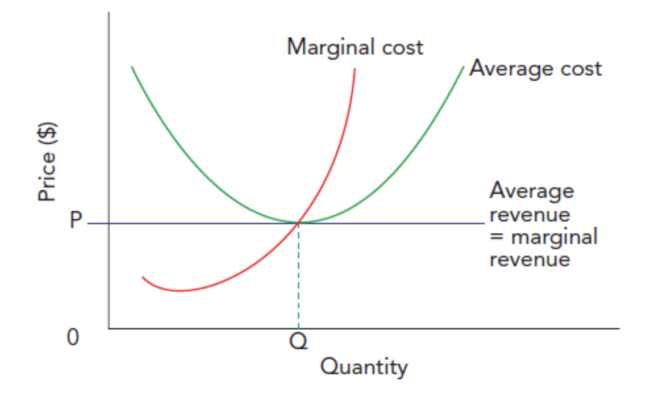

What is the condition and point on diagram for Productive Efficiency + diagram

Productive efficiency occurs when marginal cost equals average cost at the minimum point of the average cost curve.(x).

Any output above or below → inefficient

When does productive efficiency occur and not occur

✔ Perfect competition in the long run

❌ Monopoly (often X-inefficient)

What is marginal cost

The addition to total cost when making one extra unit of output

What is Allocative Efficiency

Occurs when resources are allocated to produce the combination of goods most wanted by consumers.

Where price is equal to marginal cost: firms are producing the goods and services most wanted by consumers.

Gives consumers maximum satisfaction at their current level of income.

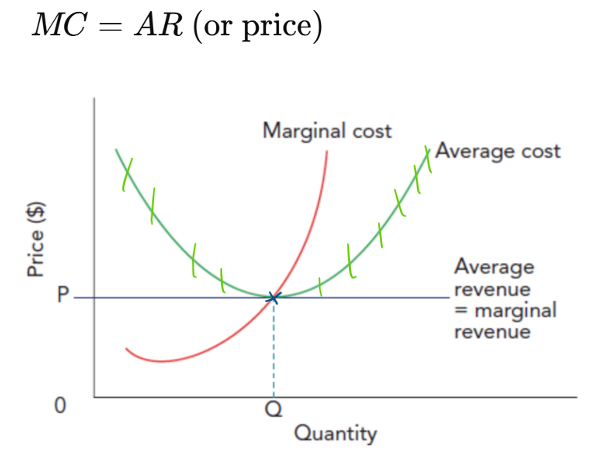

What is the condition and point on diagram for Allocative Efficiency

Allocative efficiency occurs when marginal cost equals average revenue (price).

MC = AR/price

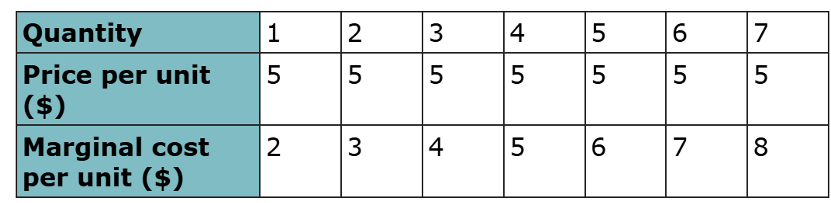

What quantity should this firm produce for maximum allocative efficiency

Answer- 4 as MC = Price (5=5)

Why can you not show allocative efficiency on PPC

Any point on the PPC could potentially be a point provided price is equal to marginal cost at this point. The exact location will depend on consumer preferences which are not part of PPC model.

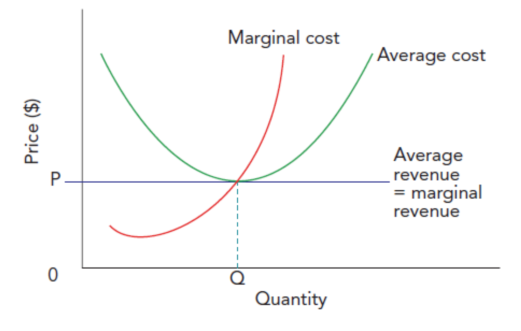

How does a competitive market lead to allocative efficiency (2 ways)

Firms in competitive markets will be forced to produce those products most demanded by consumers. If firms do not produce these goods, other firms will step in and do so. A failure to produce such products will therefore force some firms to close.

Point of equilibrium (price P and output Q) is a position at which price is equal to marginal cost which is the requirement for allocative efficiency

What is the meaning of MC = AR

The cost to society of producing the last unit equals the value consumers place on that unit.

When does allocative efficiency occur and not occur

✔ Perfect competition

❌ Monopoly (P > MC → underproduction)

Productive vs Allocative Efficiency

Productive efficiency focuses on lowest cost production, while allocative efficiency focuses on meeting consumer preferences.

Diagram of productive efficiency in a competitive market (also shows allocative efficiency)

Alternative diagram to show productive efficiency in an economy:

A point on the PPC, Y, shows the maximum production for combinations of any two goods (for example, capital goods and consumer goods) that are produced in an economy.

Productive efficiency can only exist when an economy is producing on the boundary of its PPF.

Point X shows productive inefficiency.

What can lead to productive efficiency and why

Competition - as firms are constrained to produce at the lowest possible cost in a competitive market as they have an incentive to make maximum profit.

Competitive market also leads to the necessary conditions for productive efficiency as given by the point of long run equilibrium given by P and Q.

Why is efficiency both a microeconomic and macroeconomic problem using examples(2 - oil & timber)

Efficiency is both a microeconomic and macroeconomic problem because scarce resources must be allocated well at the level of individual markets and the whole economy.

• Oil (macro + micro): Inefficient fuel use (e.g. traffic congestion, high-consumption vehicles) wastes a scarce resource. At the micro level this reflects inefficient consumption and production choices; at the macro level it threatens long-term growth, energy security and climate targets (Net Zero 2050).

• Timber (macro + micro): Firms may overproduce timber products to maximise profits (micro inefficiency due to external costs), but collectively this leads to deforestation, loss of ecosystems and long-run global inefficiency (macro problem).

Overall: Because resources are scarce, efficiency is essential to maximise welfare for consumers and producers within markets (microeconomics) and to sustain growth, stability and living standards across entire economies (macroeconomics).

What is Pareto Optimality and what does it represent and require(link to efficiency)

A situation where no one can be made better off without making someone else worse off.

Represents the best possible situation in the circumstances, with resources allocated in the most efficient way (On the PPC)

Pareto optimality requires allocative efficiency and a complete allocation of resources. (Rare in reality.)

Where would pareto inefficiency be on PPC and why

Anywhere inside the curve as it would be possible to increase the output of either type of good without reducing the output of another.

Example of pareto optimality (+chain of reasoning)

Turkeys new Istanbul airport

• Airport expansion increases efficiency → airlines and passengers gain from fewer delays and better facilities.

• Some groups are worse off → local residents may lose homes, face noise pollution and poorer air quality.

• Compensation is possible in theory → but not always paid in practice.

• Conclusion → the project raises overall efficiency but is not Pareto optimal, since some people lose out even if total benefits exceed costs.

What is Dynamic Efficiency

Form of productive efficiency, where resources are allocated efficiently that benefits a firm overtime (a long-run concept)

- meaning when firms improve products and production methods over time through innovation and investment.

Often associated with monopolies and oligopolies.

When is dynamic efficiency achieved and how

Achieved when a firm meets the changing needs of its market by introducing new production processes in response to competitive pressures.

- By using investments sourced from within(excess profits) or outside the firm, firms are able to engage in research, development and product innovation in order to protect their market share.

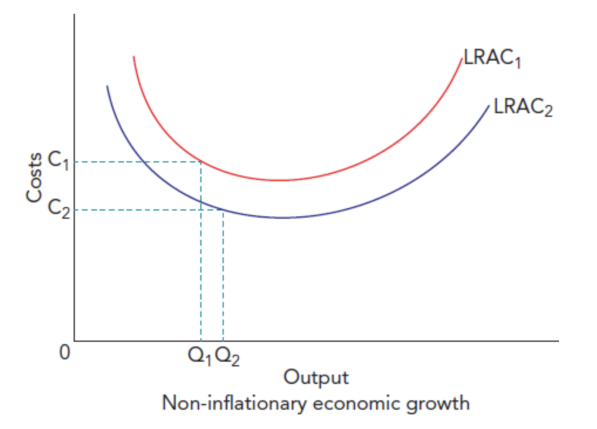

What happens to the LRAC when a firm is dynamically efficient

The LRAC shifts downwards

Who benefits from dynamic efficiency and how

Benefits consumers in form of new technologies and lower prices

Benefits firms in a more efficient means of production

Examples of Dynamic Efficiency (+chain of reasoning)

The motor vehicle manufacturing industry

• Highly competitive industry → firms must become more efficient to survive.

• Ongoing innovation and investment → automation, robots and computer-aided production.

• Long-term improvements → lower unit costs and higher productivity over time.

• Conclusion → the motor vehicle industry demonstrates dynamic efficiency, where efficiency improves through sustained innovation rather than at a single point in time.

What is Market Failure

Occurs when the price mechanism leads to a misallocation of resources (inefficient allocation of resources), resulting in a loss of economic welfare.

Market outcome ≠ socially optimal outcome

Examples of market failure (5)(looked at in more detail in other chapters)

- Where there are externalities in the market

- The provision of merit and demerit goods

- The provision of public and quasi-public goods

- Information failure

- Abuse of monopoly power in the market

Why does market failure arise (2 ways) - (key concept link)

Price mechanism failure -> Misallocation of resources

Poor government regulation

What are Externalities

Costs or benefits of an economic activity that affect third parties and are not reflected in market prices.

What are Public Goods

Goods that are non-excludable and non-rival, leading to free-rider problems.

Underprovided by markets.

What are Merit Goods

Goods that are underconsumed because consumers underestimate their benefits. e.g. education

What are Demerit Goods

Goods that are overconsumed because consumers underestimate their costs. e.g. cigarettes

How does Monopoly Power Cause Market Failure

Monopolies charge prices above marginal cost, leading to allocative inefficiency and deadweight welfare loss

What is Asymmetric Information

Occurs when one party in a transaction has more information than the other.

Leads to moral hazard & adverse selection

Examples of Asymmetric Information

Healthcare and insurance markets.

What is Factor Immobility

When labour or capital cannot move freely between occupations or locations, causing inefficiency and unemployment.

Efficiency in Perfect Competition

✔ Productive efficiency

✔ Allocative efficiency

❌ Dynamic efficiency (low profits)

Efficiency in Monopoly

Monopolies are often allocatively and productively inefficient but may be dynamically efficient.

❌ Productive efficiency → X-inefficiency

❌ Allocative efficiency → P > MC

✔ Dynamic efficiency → high R&D spending

What is Welfare Loss

A reduction in economic welfare due to inefficient allocation of resources.

What is the Price Mechanism

The system by which prices allocate resources through demand and supply.

What happens when the Price Mechanism Fails

Prices do not reflect true social costs and benefits, leading to inefficiency.

Overall Evaluation of Market Efficiency

Markets can achieve efficiency, but market failures mean government intervention may be required.