econ final definitions

1/31

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

32 Terms

Characteristics of pure competition

-large # of sellers

-Standardized product: the product is the same across sellers, consumers are indifferent about who to buy from

-freedom of entry & exit: new firms can enter freely & existing firms leave when they want to

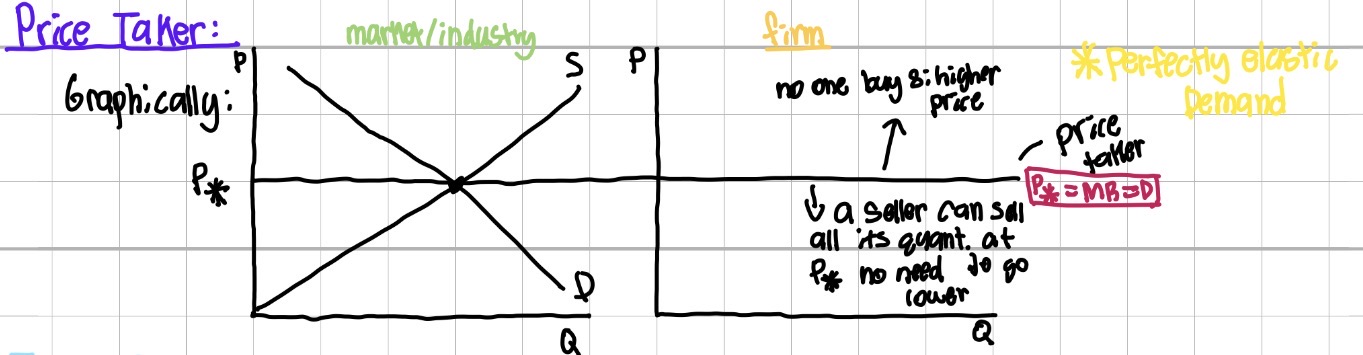

-price takers: individual sellers have no significant control over the price. Each seller has a small market share & must accept the price from the market

Firm vs market/industry demand curve for pure competition

industry=downward sloping, firm=perfectly elastic

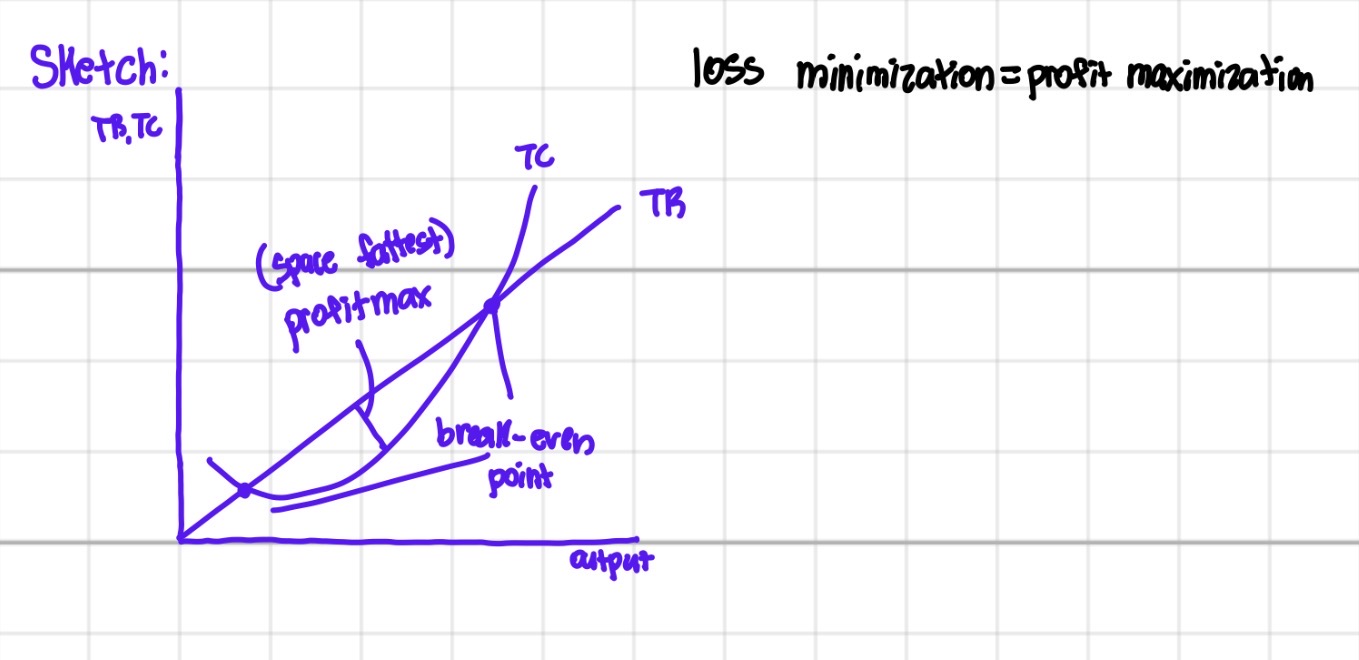

profit maximization rule for pure competition

MR=MC

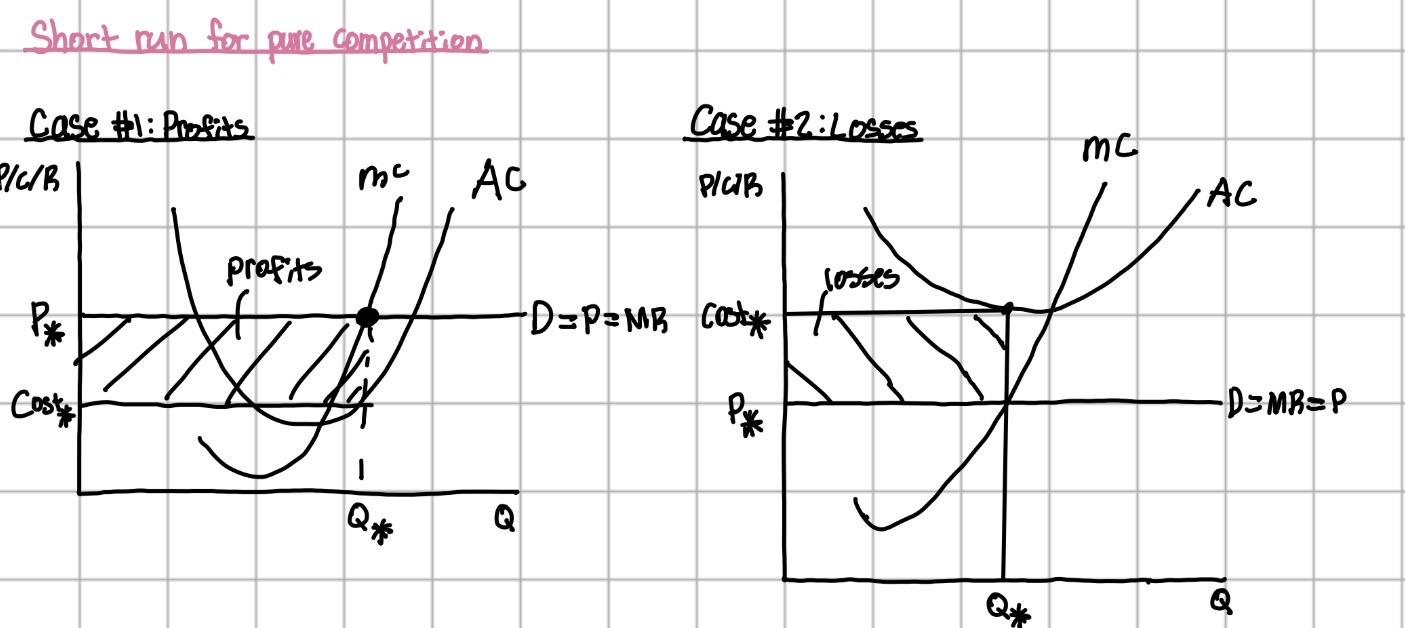

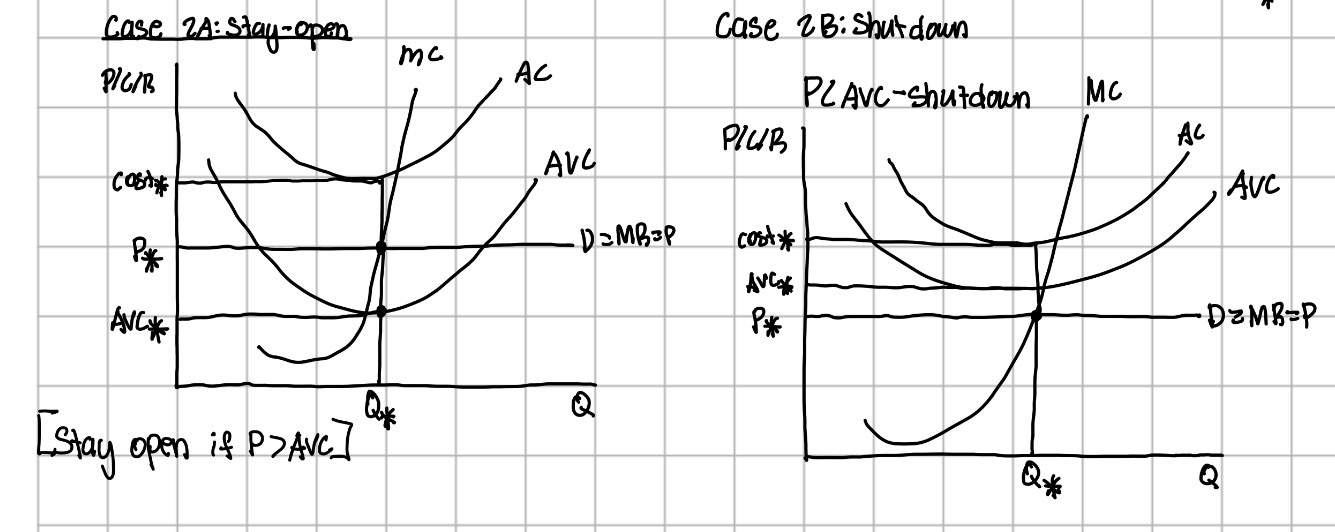

Short Run Cost Curves for pure competition

Shutdown rule for pure competition

operate if P>_AVC

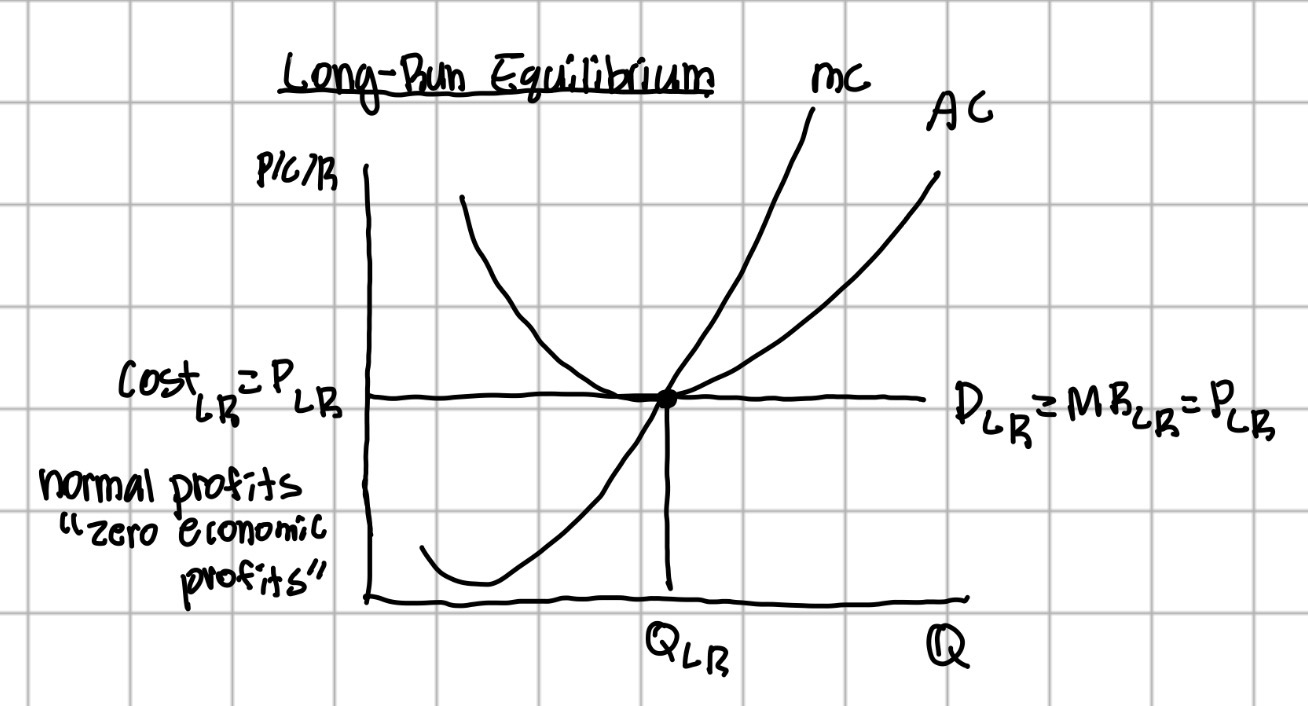

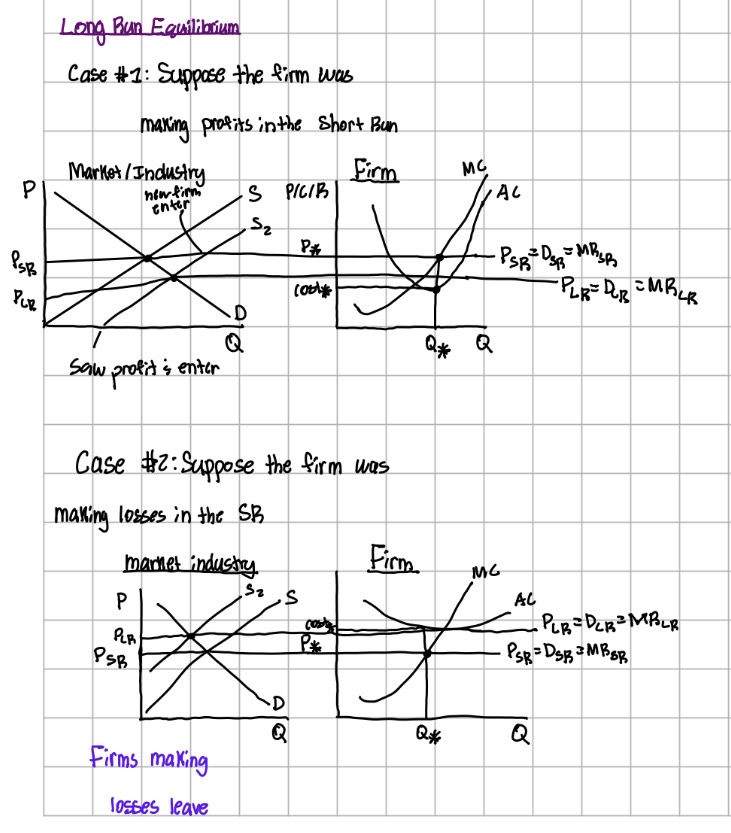

long-run equilibrium for pure competition

normal profits only

What are the differences between pure competition, monopolistic competition, oligopoly, pure monopoly. number of sellers, control over price, barrier to entry, entry/exit, same/diff product

number of sellers, control over price, barrier to entry, entry/exit, same/diff product

Long run equilibrium case #1 and case #2

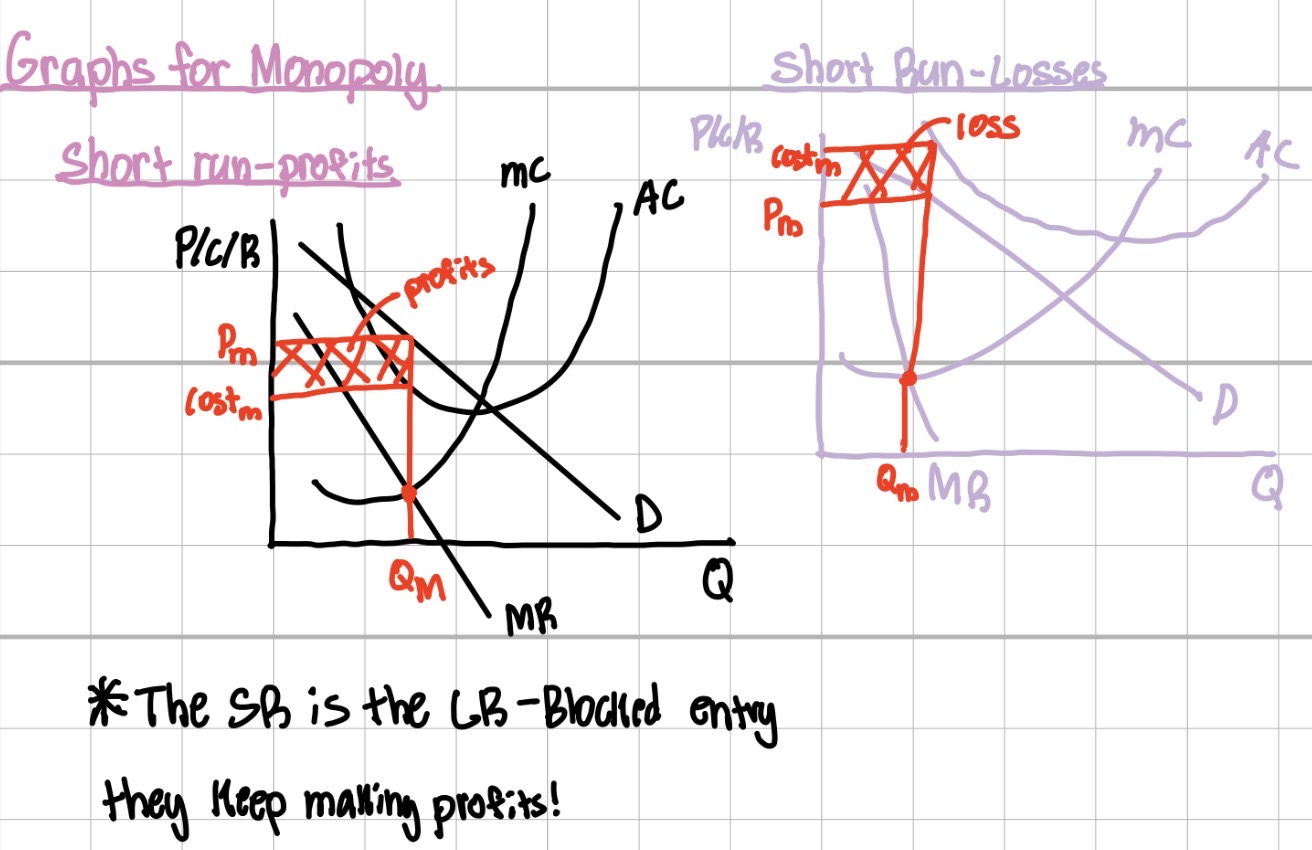

making profits in short run, making losses in the short run

Perfectly elastic demand for pure competition

normal profits p=cost, find what efficiency is and what it means

Tips for pure competition

-always locate MR=MC on graph

-price<AVC→shutdown in the short run

-in the long run→firms earn zero economic profit

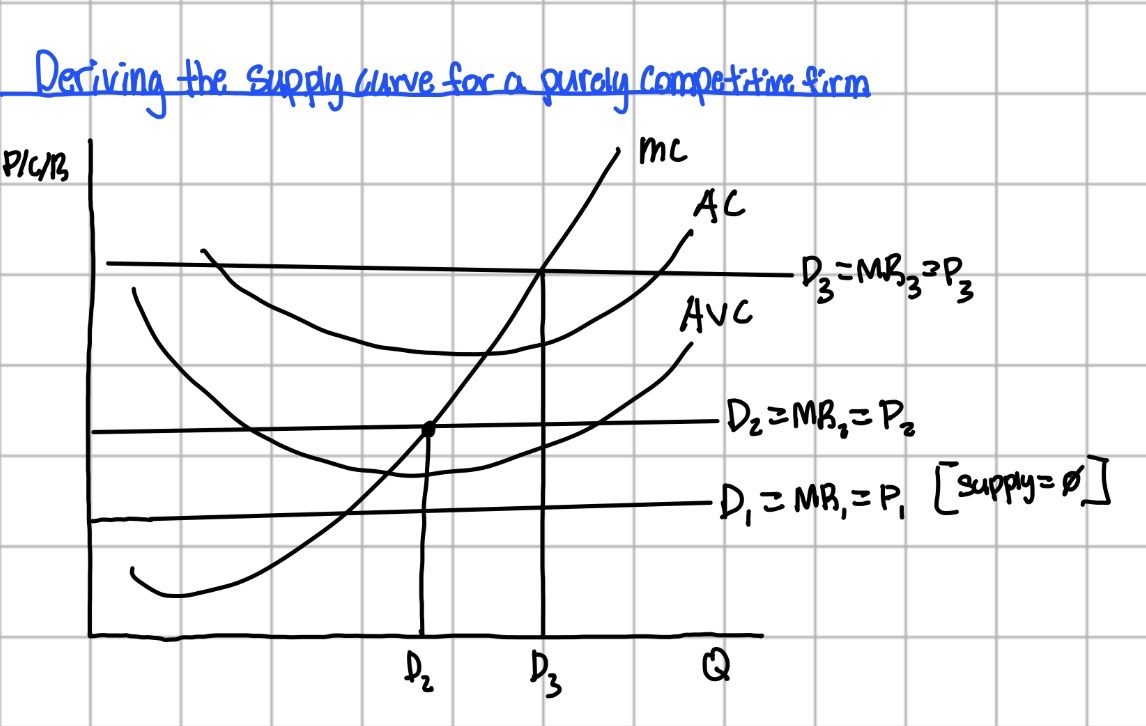

supply curve for purely competitive firm

supply is MC curve that is above the AVC

characteristics of monopoly

-Single seller: one firm dominates; has a high market share and there are no close substitutes

-Price makers: The monopolist controls the quantity sold and has control over the price

-Blocks entry: Barriers to entry, no competitor can easily enter the market

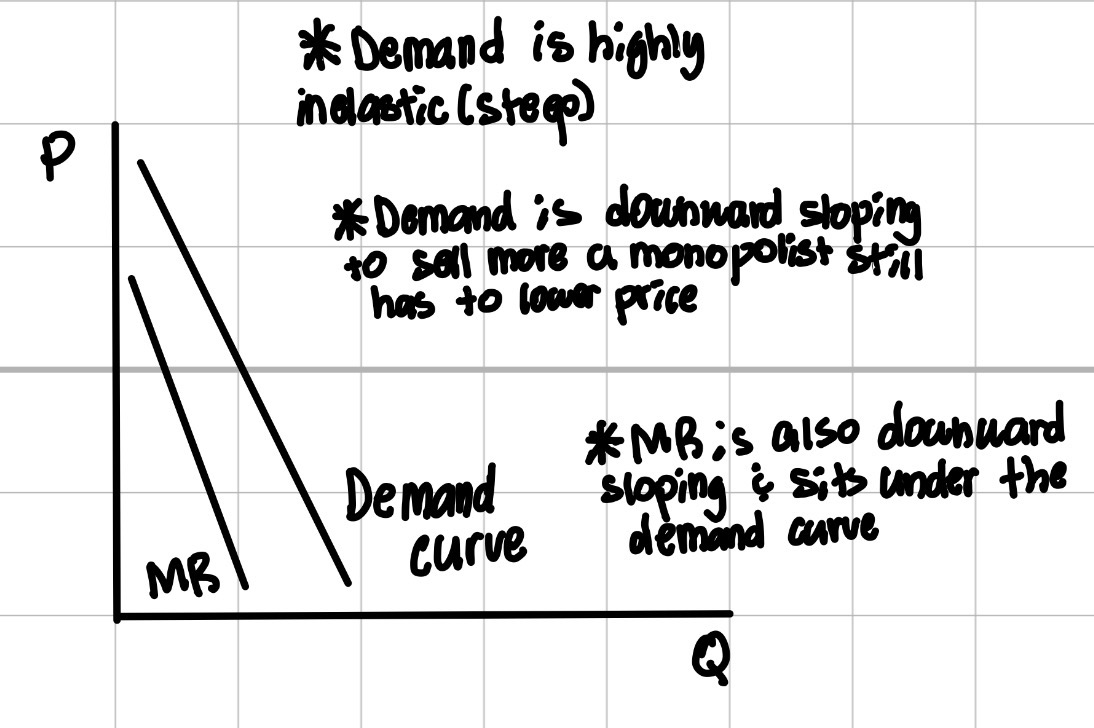

demand and MR for monopoly

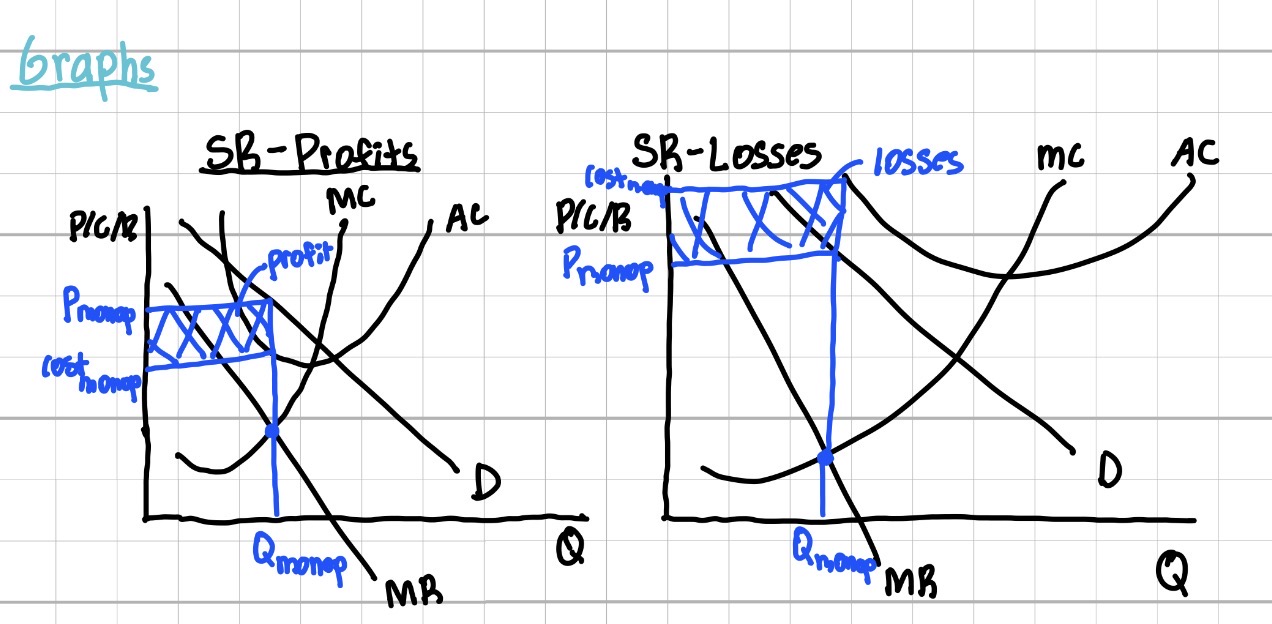

profit maximization for pure monopoly

profit maximization at MR=MC but price is set on the demand curve

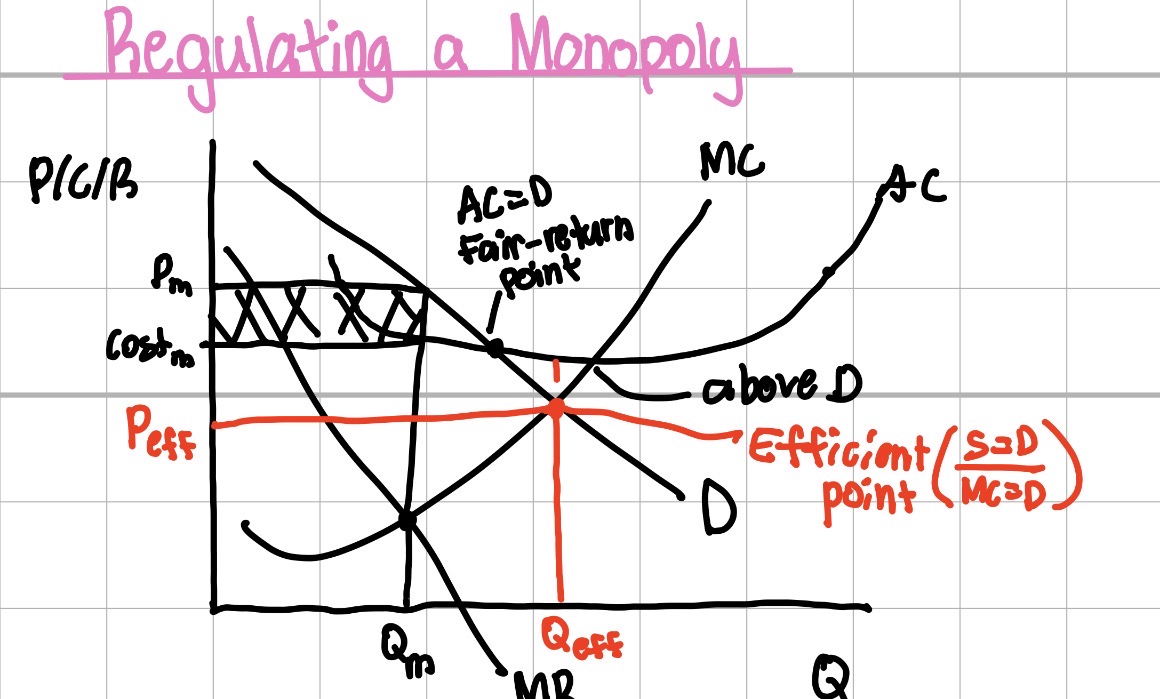

socially optimal and fair-return regulation

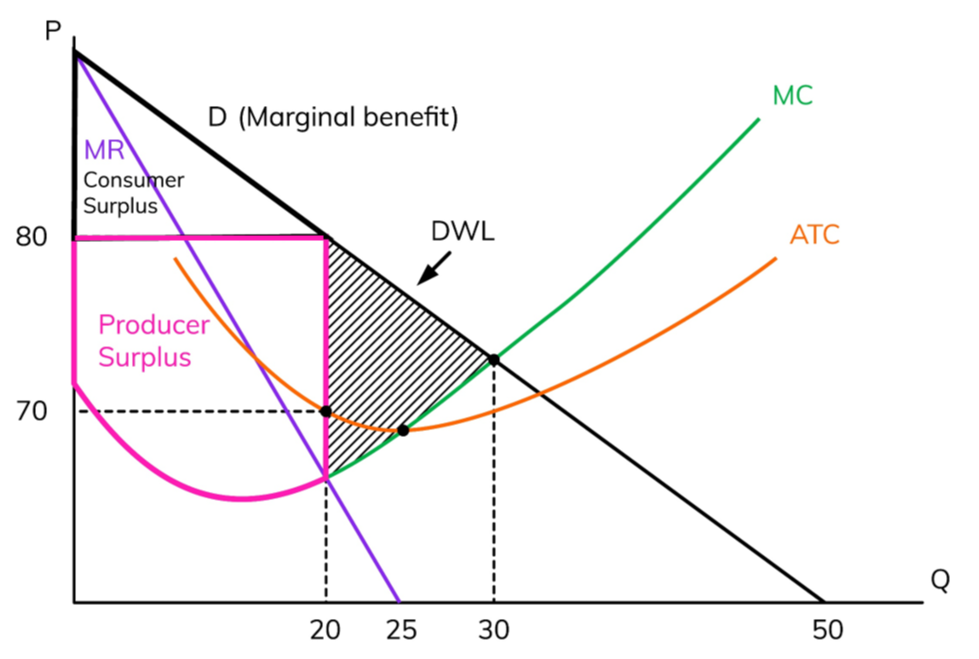

deadweight loss of monopoly power

Natural monopoly cost structure

Qm<Qeff

Pm>Peff

underproduce and overcharge

Barriers to entry for monopoly

-economies of scale: when the average cost is declining as output expands

-legal barriers to entry: Patents: exclusive of an inventor to use or allow others to use their invention, Licenses: limitation on the # of products of a particular service

-ownership or control of essential resources, e.g., diamonds

-pricing and other strategic behavior

graphs for monopoly short run profits/losses

tips for pure monopoly

-socially optimal regulation is price=MC

-fair-return regulation price=ATC

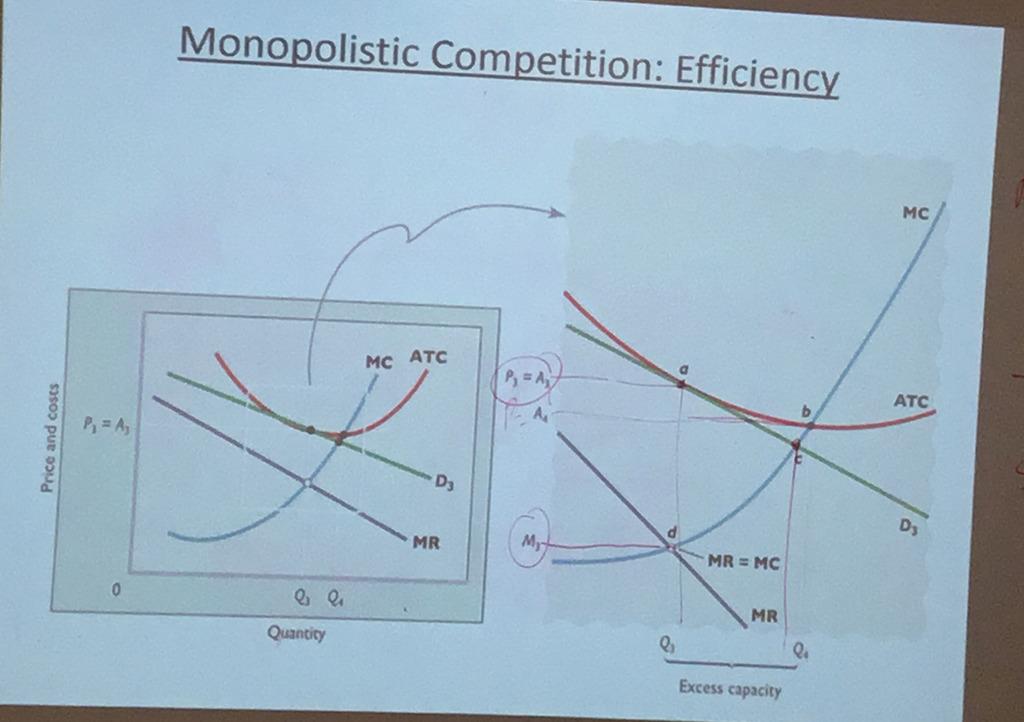

monopolistic competition

-large number of sellers, acting independently, small market share

-differentiated products, gives some monopoly power

-freedom of entry + exit

-advertising is common

-some pricing power

-NON-PRICE COMPETITION(advertising, branding)

short-run profit or loss monopolistic competition

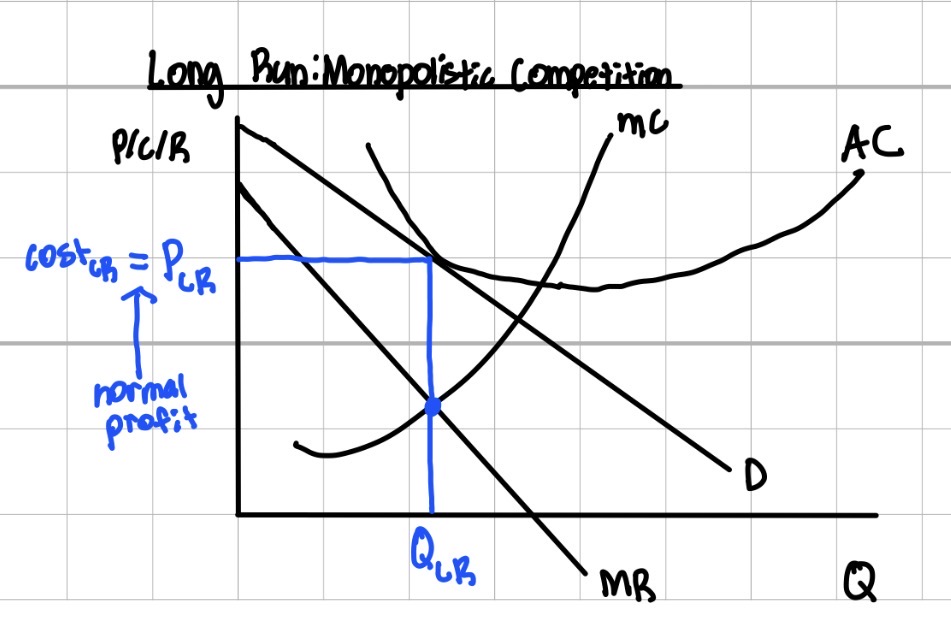

long run monopolistic competition

in long run if firm make profit, new firm enter and compete away profit until only normal profits made

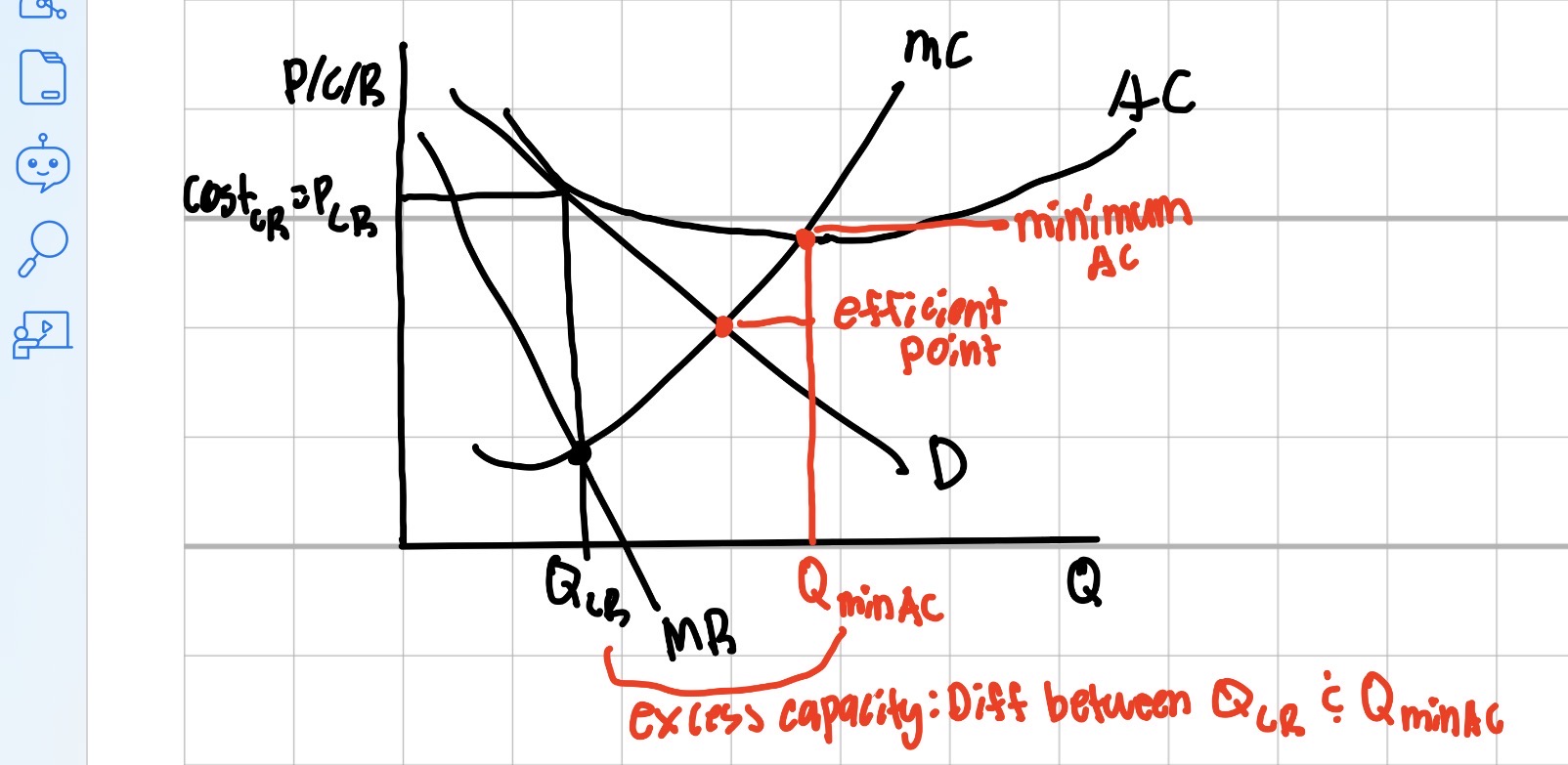

inefficient structure for monopolistic competition

tips for monopolistic competition

-P>MC in the long run

-ATC tangent to the demand curve

monopolistic competition efficient graph

Price (P) = Marginal Cost (MC) → allocative efficiency

Average Total Cost (ATC) is minimized → productive efficiency

Oligopoly characteristics

-a few large sellers

-differentiated/similar products

-control over the price but mutual interdependence, price matters, consider how rivals will react to price, output, and the product

-barrier to entry-economies of scale, legal (license, patents), control of essential resources, strategic pricing and marketing

-mergers: combining two or more competing firms to increase market share “urge to merge”.

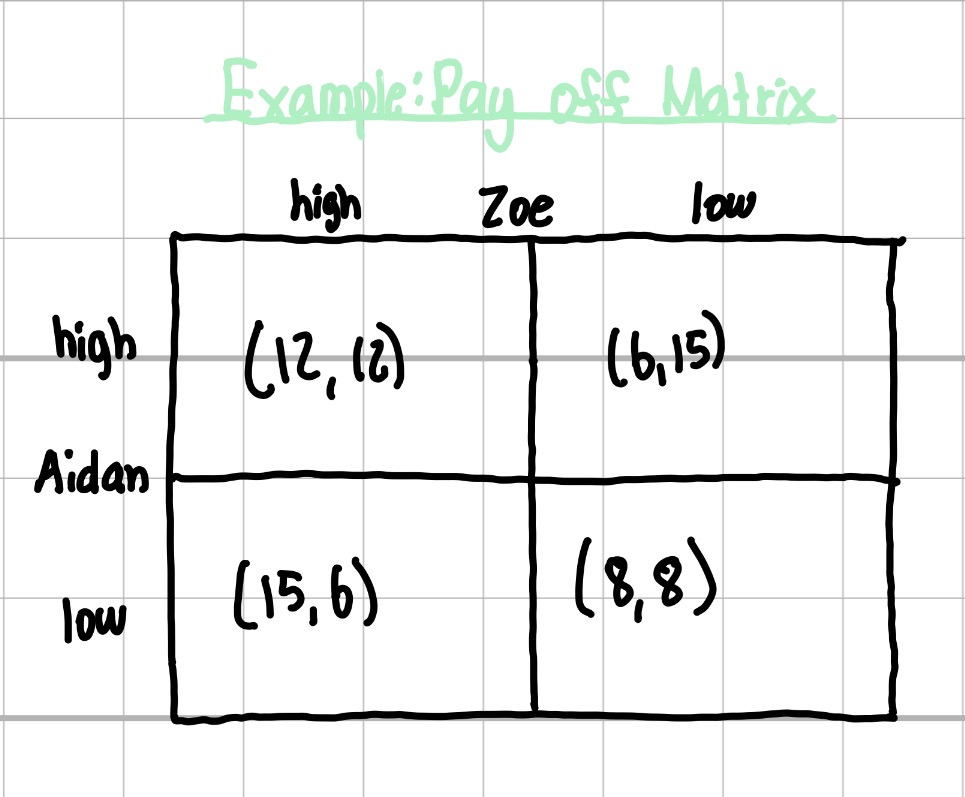

Game Theory and payoff matrix for oligopoly

game theory: firms have to watch their rivals & make decisions based on each others actions (strategic behavior)

Nash equilibrium: no player can improve their payoff by unilaterally changing their strategy, assuming everyone else keeps theirs constant

*mutual interdependence: to make $12m; no firm can separately be guaranteed this profit by charging a high price. they “must know” what the competitor is doing

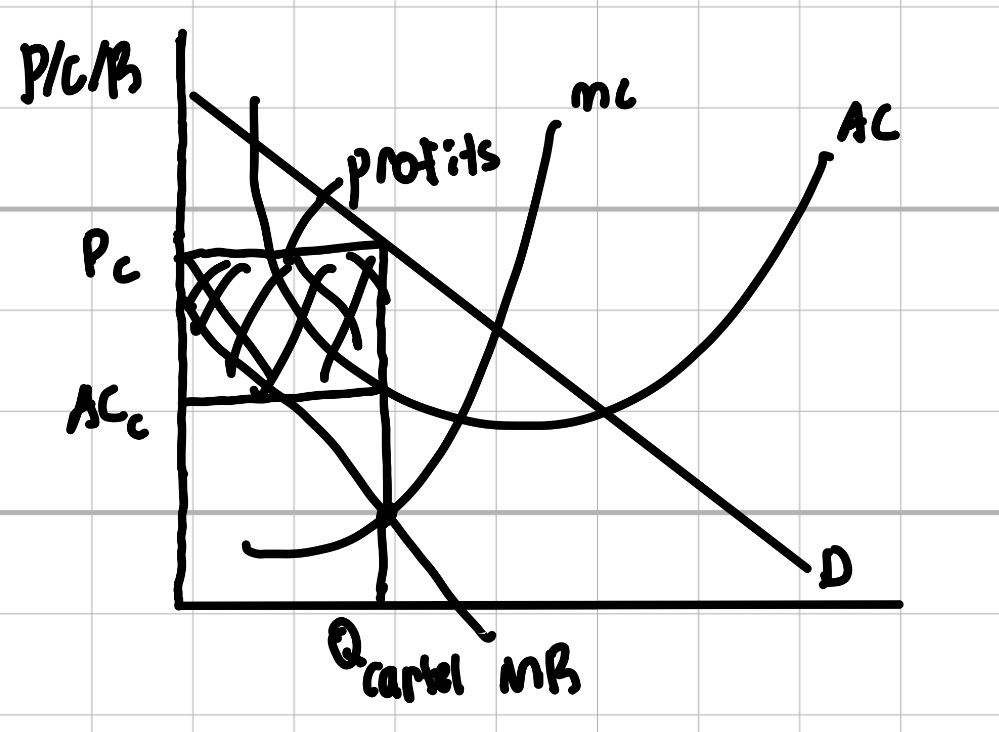

Collusion for oligopoly

If firms act independently they end up at (low, low). The incentive exist to collude & charge customers a high price rather than compete *ALWAYS an incentive to cheat*

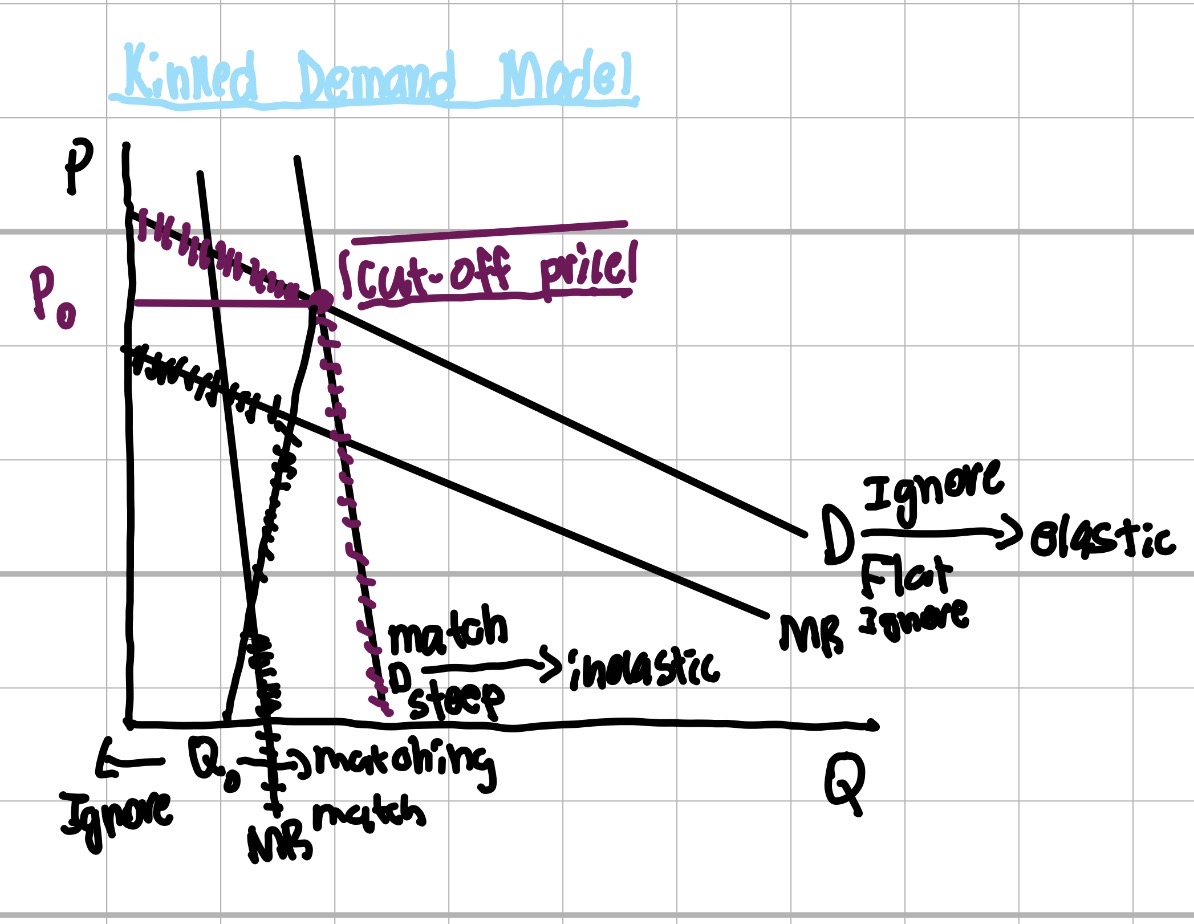

Kinked Demand Model

firms choose not collude because they want to compete

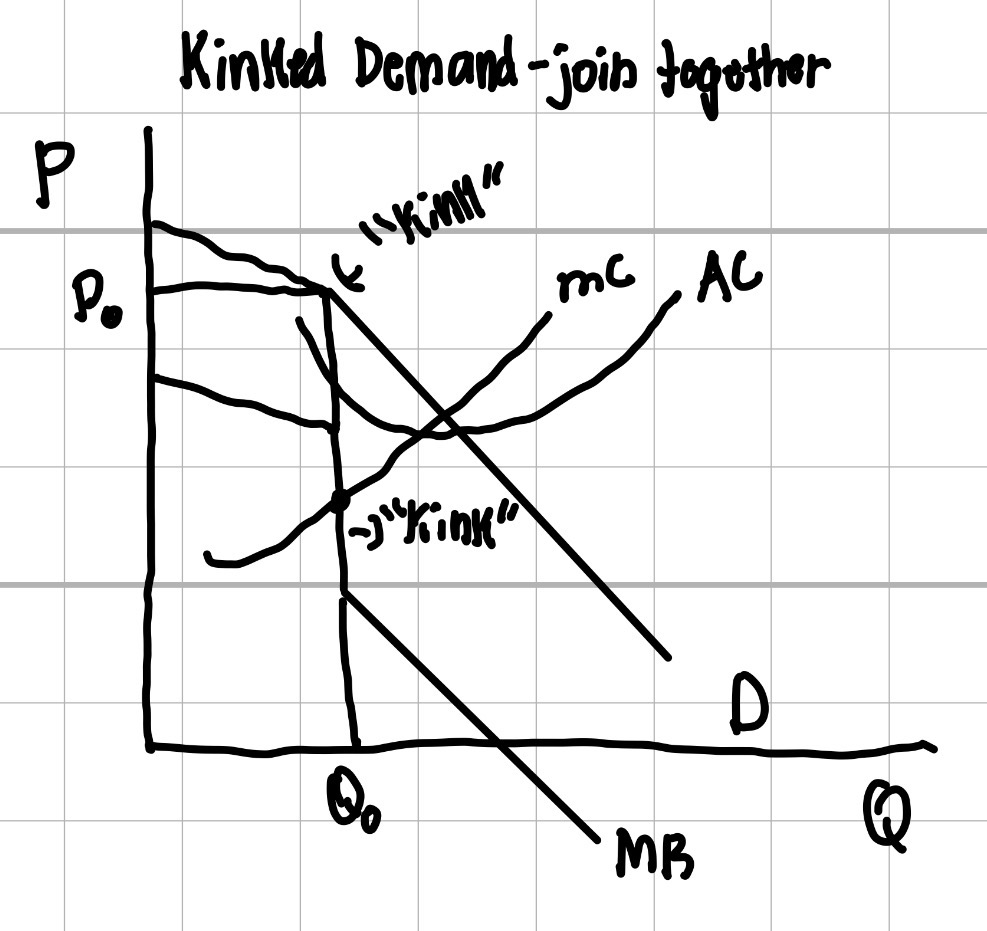

Kinked Demand-join together

Price Leadership and tacit collusion in oligopoly

tacit collusion: occurs when competing firms in an oligopoly coordinate their pricing and output without any formal agreement

price leadership: the largest/dominant firm initiates price changes or product changes & all other firms follow, “mimic a monopoly”