Module 2.1: Audit Planning & Analytical Procedures

1/43

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

Why is a good audit plan important?

Helps the auditor obtain sufficient appropriate evidence

Maintains auditor reputation

Minimizes legal liability

Helps the auditor keep costs reasonable

Maintains competitiveness (and clients)

Helps the auditor properly staff and ensure proper training & expertise

Helps the auditor maintain good client relations

What is business risk?

The risk that the business fails to achieve its objectives or execute its strategies. The risk

that it will be unable to pay its financial obligations

What is audit risk?

The risk that an auditor will issue a “clean” opinion of materially misstated financial

statements.

What is audit failure?

When the auditor issues an incorrect audit opinion because it failed to follow GAAS

What is acceptable audit risk?

the auditor’s willingness to accept that the financial statements may

be materially misstated after the audit is complete and an unmodified opinion has been

issued.

Low acceptable audit risk requires: ____, High acceptable audit risk requires:____

MORE certainty that the financial statements are NOT materially misstated

LESS certainty that the financial statements are NOT materially misstated.

What is the equation for audit assurance?

AA = 1 – AAR (acceptable audit risk)

AA ~ IR * CR * E

Relationship between Audit assurance, inherent risk, control risk, and evidence (moves from left to right) all 3 determines how much evidence will be needed

What is the risk of material misstatement?

Inherent risk x Control Risk (business controls) (IR*CR)

Inherent risk (IR) – the likelihood of misstatement (before controls),

Control risk (CR) – the effectiveness of internal controls

What does the auditor have control over?

Level of audit risk & Evidence (AA & E)

Who sets the level of audit assurance?

Set at beginning of audit at partner level

Will AA be higher for an audit of a brand-new audit client OR for an audit of a long-term client? Why?

Higher AA for new client – less trust and less familiarity

Lower acceptable audit risk

Lower AA for long term client – more trust and more familiarity

Higher acceptable audit risk

If AA is set at a relatively high level, does this mean that more or less audit evidence will be collected?

More evidence - provides greater assurance

What are residual risks? (less important for exam)

the risk of material misstatement AFTER considering the effectiveness of internal controls.

What are the four steps to initial audit planning?

Decide to accept a new client or continue with an existing client

Identify the client’s reasons for an audit

Obtain an understanding with the client

Develop the overall audit strategy

Why might an auditor reject a new client/drop an existing one?

Client lacks integrity.

Client difficult to work with.

Client in a complex industry which auditor does not adequately understand.

Clients in a risky industry rife with bankruptcies / lawsuits

If any, or all, of the above conditions exist and, assuming the client is accepted, what impact

will this have on audit assurance?

Will increase AA.

More evidence needed to overcome issues.

What is the relationship between the successor auditor and the predecessor auditor?

The new (successor) auditor is responsible for initiating communication

Help them understand if they should accept / reject the client.

Determine why the old auditor no longer the auditor.

Does the predecessor have to respond?

The old (predecessor) auditor is required to share information but…

The predecessor can respond that “no information will be provided.”

Who signs the engagement letter?

Public companies - Audit Committee

Private companies - Management

What is a related party?

an affiliated company, a principal owner of the client company, or any other

party with which the client deals, where one of the parties can influence the management or

operating policies of the other.

Why is a related party transaction not an arm’s length transaction?

Arm's Length Transaction: A transaction where the buyers and sellers acts completely independently of one another

Related Party Transaction: A transaction between two parties who share a pre-existing relationship or common control

Related party transactions are NOT illegal but…They should be disclosed in ____

FS notes

What is the level of IR associated with related party transactions?

HIGH

What are Analytical procedures?

– Evaluations of financial information through analysis of plausible relationships among

financial and nonfinancial data.

– Uses ratios and percent analysis to assess how data compares to auditor’s expectations.

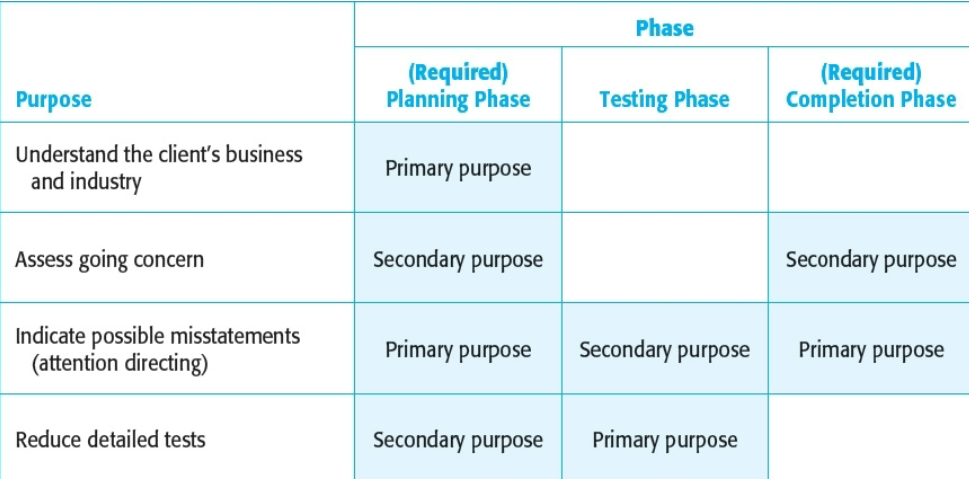

What is the purpose of Analytical procedures?

Help the auditor understand the client’s business & industry

Help the auditor to assess business risk/going concern issues

Helps the auditor to identify possible misstatements

May reduce amount of testing of account balances

Which ratios may help with assessing going concern issues?

Leverage ratios

When are analytical procedures required?

During planning and completion phases of the audit.

Analytical procedures are often done (but not required) during the testing phase of the

audit as a substantive test in support of account balances.

What is the planning phase?

Planning phase: assists in determining the nature, extent, and timing of audit procedures.

What is the completion phase?

serves as a final review for material misstatements or financialproblems.

How costly are analytical procedures and how reliable are they?

How costly are analytical procedures?

• Moderate

How reliable are analytical procedures?

• Moderate to low

What are the primary purposes of analytical procedures in the planning phase?

What are the secondary purposes?

Primary

Understand the client’s business and industry

Indicate possible misstatements

Secondary

Reduce detailed tests

Assess going concern

What are the primary purposes of analytical procedures in the completion phase?

What are the secondary purposes?

Primary

Indicate possible misstatements

Secondary

Assess going concern

What is vertical analysis?

Used to examine relations BETWEEN items WITHIN an accounting period

Emphasizes relations within each accounting period

What is horiztonal analysis?

Used to examine relations WITHIN items BETWEEN accounting periods

Emphasizes relations within a line item

What is the formula for current ratio?

Current assets / current liabilities

The allowance for obsolete inventory increased from the prior year, but the allowance as a percentage of inventory decreased from the prior year. WHY?

So if percentage based on inventory has decreases - (allowance/inventory).. and we know that allowance has increased -

that means inventory has increased more than the allowance has

Long-term debt increased from the prior year, but total interest expense decreased as a percentage of long-term debt.

The dollar amount of operating income is consistent with the prior year although the entity was more profitable on a net income basis.

The quick ratio decreased from the prior year, although the amount of cash and net account receivable is almost the same as the prior year.