Intro to Financial Accounting Chapter 3

1/42

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

43 Terms

Time Period Assumption (Periodicity Assumption)

Accountants divide the economic life of a business into artificial time periods. Generally a month, a quarter, or a year.

Interim Periods

Monthly or quarterly accounting time periods

Fiscal Year

Accounting time period that is one year in length.

Calendar Year

January 1 to December 31

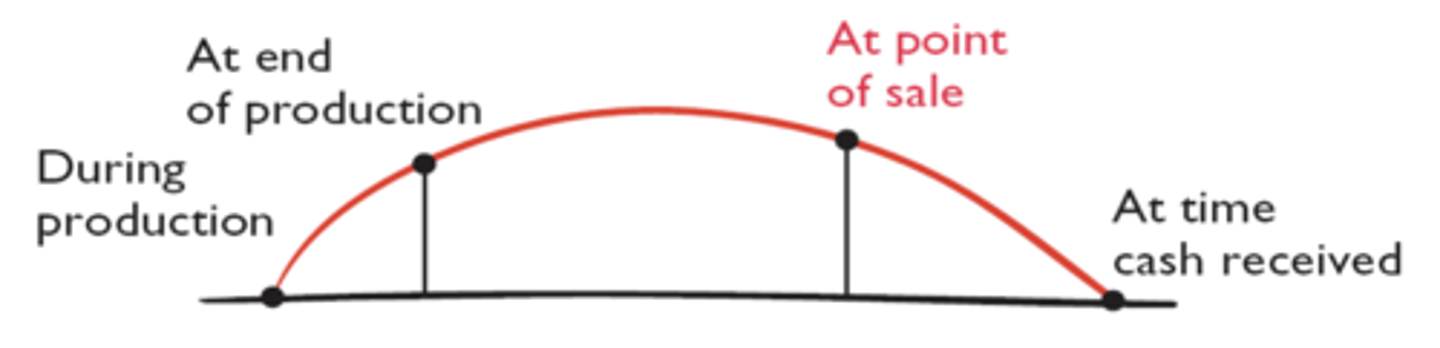

Accrual-Basis Accounting

Transactions are recorded in the periods in which the events occur. Companies recognize revenues when they perform services (rather than when they receive cash). Expenses are recognized when incurred (rather than when paid).

Cash-Basis Accounting

Revenues are recorded when cash is received. Expenses are recorded when cash is paid. Cash-basis accounting is not in accordance with generally accepted accounting principles (GAAP).

Revenue Recognition Principle

The accounting period in which the performance obligation is satisfied.

Expense Recognition Principle (Matching)

Match expenses with revenues in the period when the company makes efforts to generate those revenues.

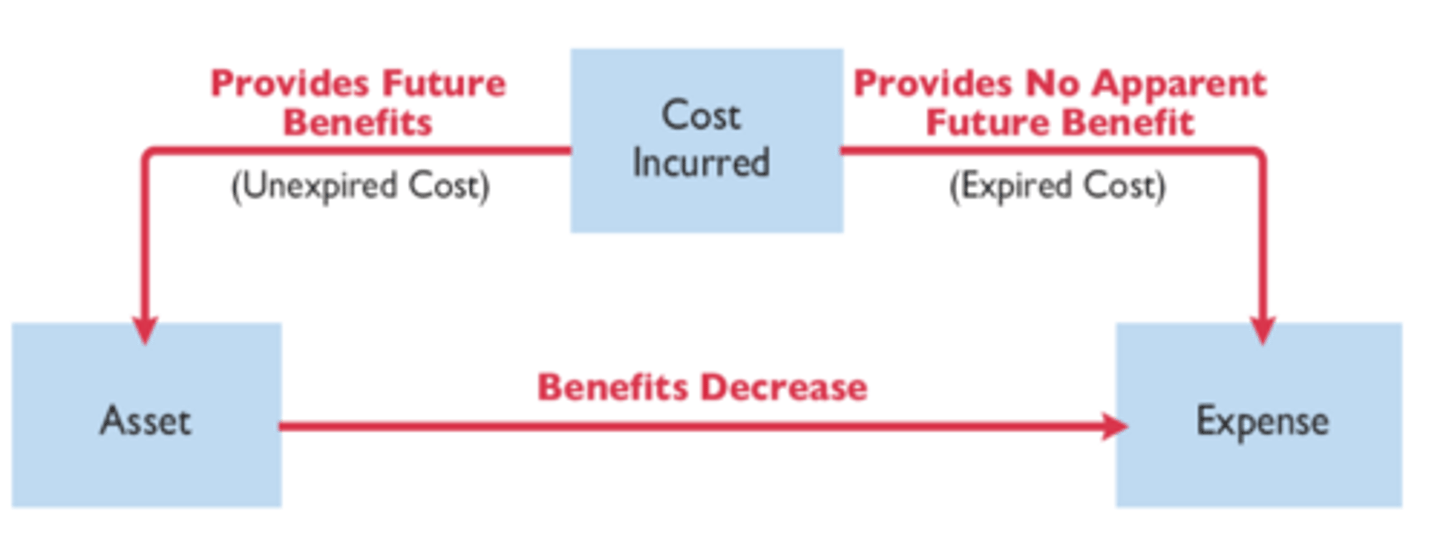

Adjusting Entries

Entries made at the end of an accounting period to ensure that the revenue recognition and expense recognition principles are followed. Includes and income statement account and one balance sheet account. DOES NOT involve cash.

Deferrals

Adjusting entries for either prepaid expenses or unearned revenues.

Accruals

Adjusting entries for either prepaid expenses or unearned revenues.

Prepaid Expenses (Deferrals)

Expenses paid in cash before they are used or consumed.

Unearned Revenues (Deferrals)

Cash received before services are performed.

Accrued Revenues

Revenues for services performed but not yet received in cash or recorded.

Accrued Expenses

Expenses incurred but not yet paid in cash or recorded.

Trial Balance (Adjusting Entries)

Each account is analyzed to determine whether it is complete and up-to-date for financial statement purposes.

Prepaid Expenses (Statements)

Payments of expenses that will benefit more than one accounting period.

Depreciation

Process of allocating the cost of an asset to expense over its useful life. Does not attempt to report the actual change in the value of the asset.

Contra Asset Account (credit).

Contra asset account (credit); accumulated depreciation

Book value

The difference between the cost of any depreciable asset and its accumulated depreciation.

Unearned Revenues (Statement)

Receipt of cash that is recorded as a liability because the service has not been performed.

Preparing the Adjusted Trial Balance

- Prepared after all adjusting entries are journalized and posted.

- Purpose is to prove the equality of debit balances and credit balances in the ledger after all adjustments.

- Is the primary basis for the preparation of financial statements.

Preparing Financial Statements

Prepared directly from the Adjusted Trial Balance. Include income statement, retained earnings statement, and balance sheet

FASB's Conceptual Framework

- Objectives of financial accounting.

- Qualitative characteristics of accounting information.

- Elements of financial statements.

- Operating guidelines (Assumptions, principles, constraints)

Objectives of financial accounting:

- To provide information that is useful to those making investment and credit decisions.

- Helpful in accessing future cash flows.

- Helpful in identifying the economic resources (assets) and the claims to those resources (liabilities).

Qualitative Characteristics of Useful Information

Relevance, faithful representation, comparability, verifiability, timeliness, and understandability

Relevance

Make a difference in a business decision. Provides information that has predictive value and confirmatory value. Accounting information must be timely.

Faithful Representation

Information accurately depicts what really happened. Informatiom must be complete, neutral, and free from error.

Comparability

Information is comparable when different companies measure and report transactions using the same accounting principles.

Consistency

Information is consistent when a company uses the same accounting principles and methods from year to year.

Verifiable

Information is verifiable if independent observers (i.e., auditors), using the same methods, obtain similar results.

Monetary Unit

Requires that only those things that can be expressed in money are included in the accounting records.

Economic Entity

States that every economic entity can be separately identified and accounted for.

Time Period

States that the life of a business can be divided into artificial time periods.

Going Concern

The business will remain in operation for the foreseeable future.

Historical Cost Principle

The price established by the exchange transaction is its "cost." Most assets follow the cost principle.

Fair Value Principle

Indicates that assets and liabilities should be reported at fair value. Fair value principle is applied in situations where assets are actively traded (i.e., investment securities).

Revenue Recognition Principle

Companies should recognize revenue in the accounting period in which it is earned:

- When the exchange takes place.

- When the earnings process is complete

Expense Recognition (Matching) Principle

Efforts (expenses) should be matched with accomplishment (revenues) whenever it is reasonable and practicable to do so.

Full Disclosure Principle

Requires that companies disclose all circumstances and events that would make a difference to financial statement users. Provided through disclosure in financial statements and notes to the financial statements.

Cost-Benefit Constraint

Accounting standard-setters weigh the cost that companies will incur to provide the information against the benefit that financial statement users will gain from having the information available.

Materiality Constraint

An item is material if its inclusion or omission would influence or change the judgement of a reasonable person.

Conservatism Constraint

When there is a choice of equally acceptable accounting alternatives, choose the alternative that is least likely to overstate assets and income.

Example: Accountants should recognize and disclose losses in the period they occur, but not gains unless they are realized.

- Accrue contingent losses from lawsuits

- Recognize impairment in value on equipment.