L8 Management (variance VMOH & sale)

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

23 Terms

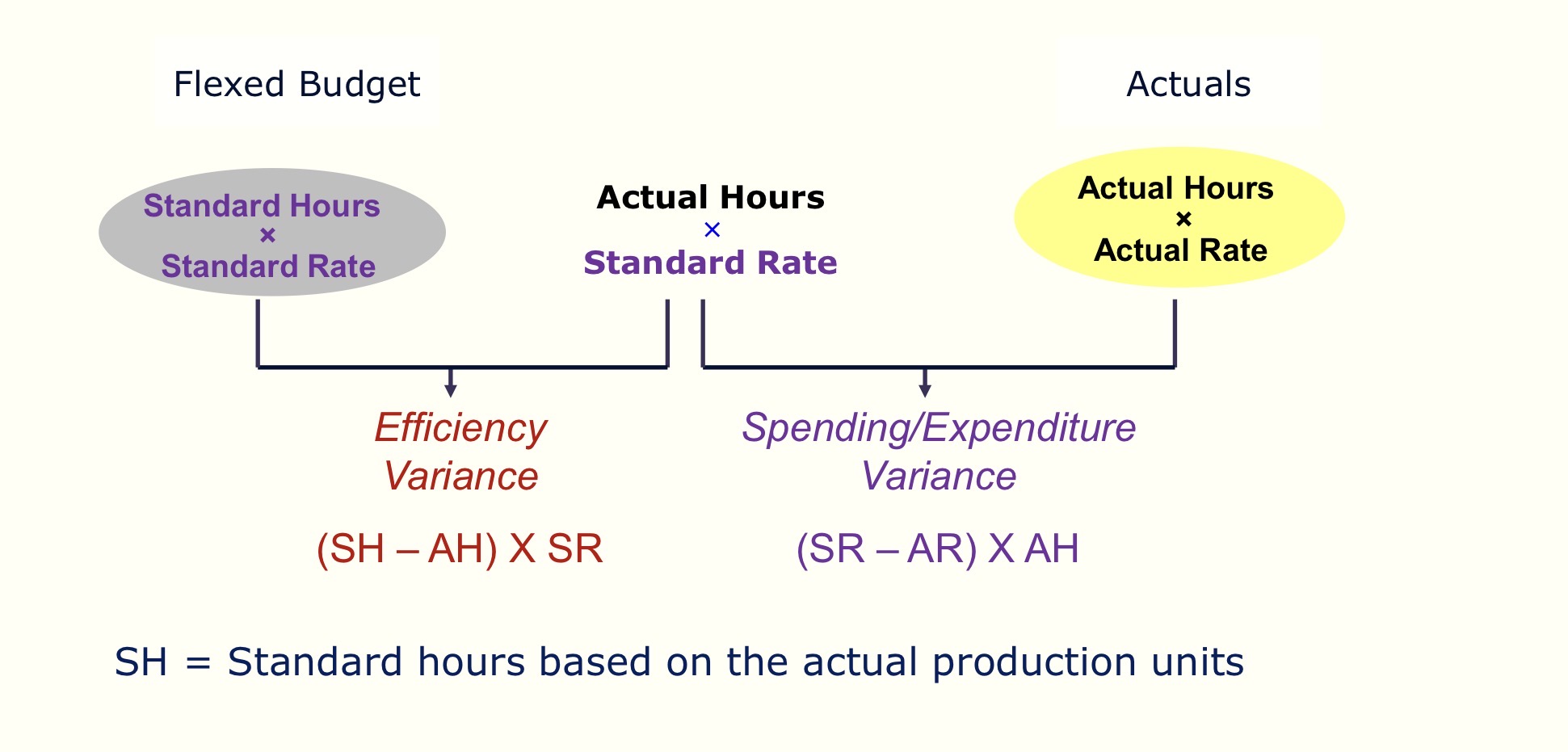

What are the two types of variances regarding VMOH?

Efficiency variance: quantity

Spending/ expenditure variance: price

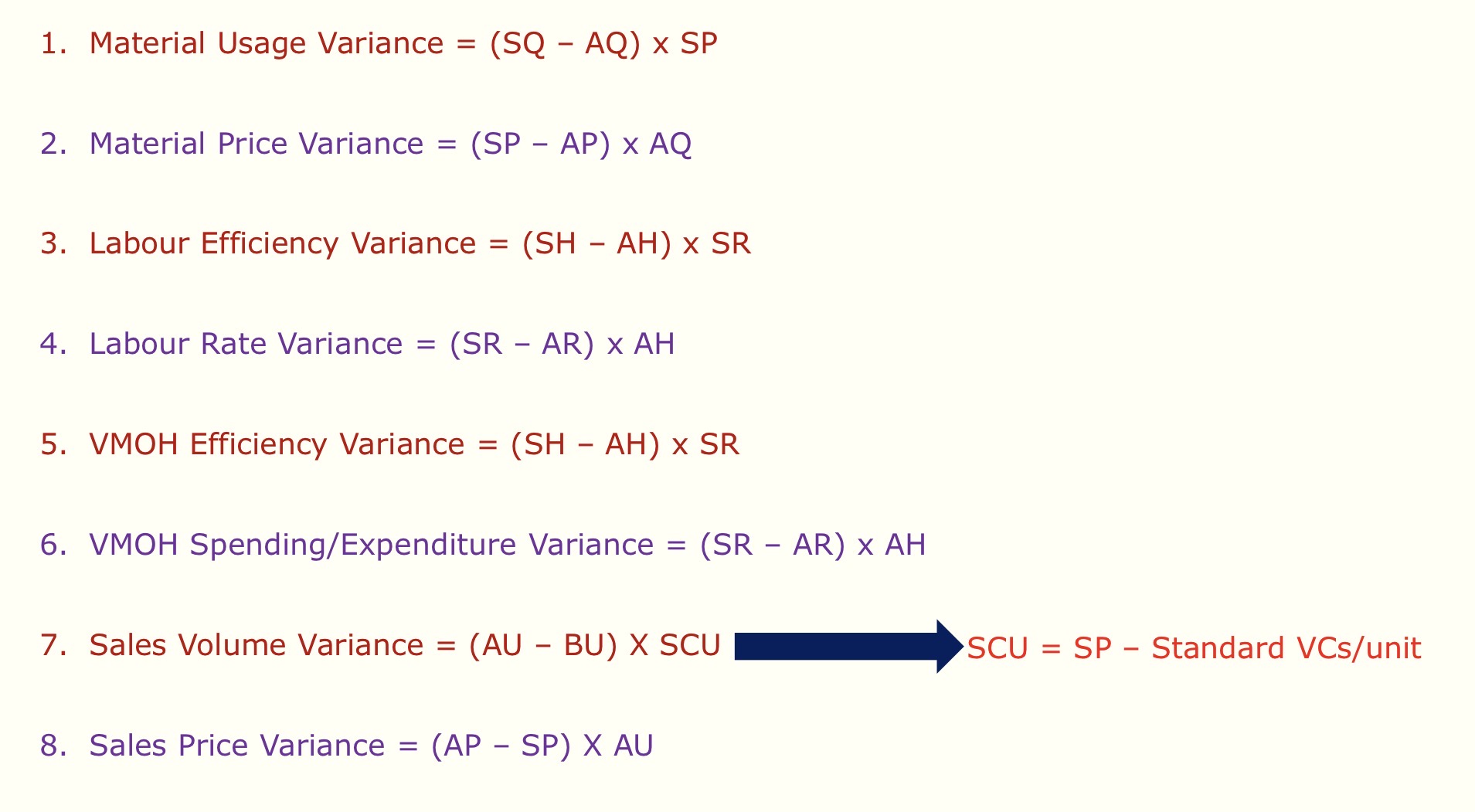

How do you find efficiency variance?

(SH - AH) x SR

How do you find spending variance?

(SR - AR) x AH

What is the diagram to represent efficiency and spending variance

NOTE: Standard hours based on total production units, not per unit/hour

How do you find total VMOH variance

Efficiency variance + spending variance

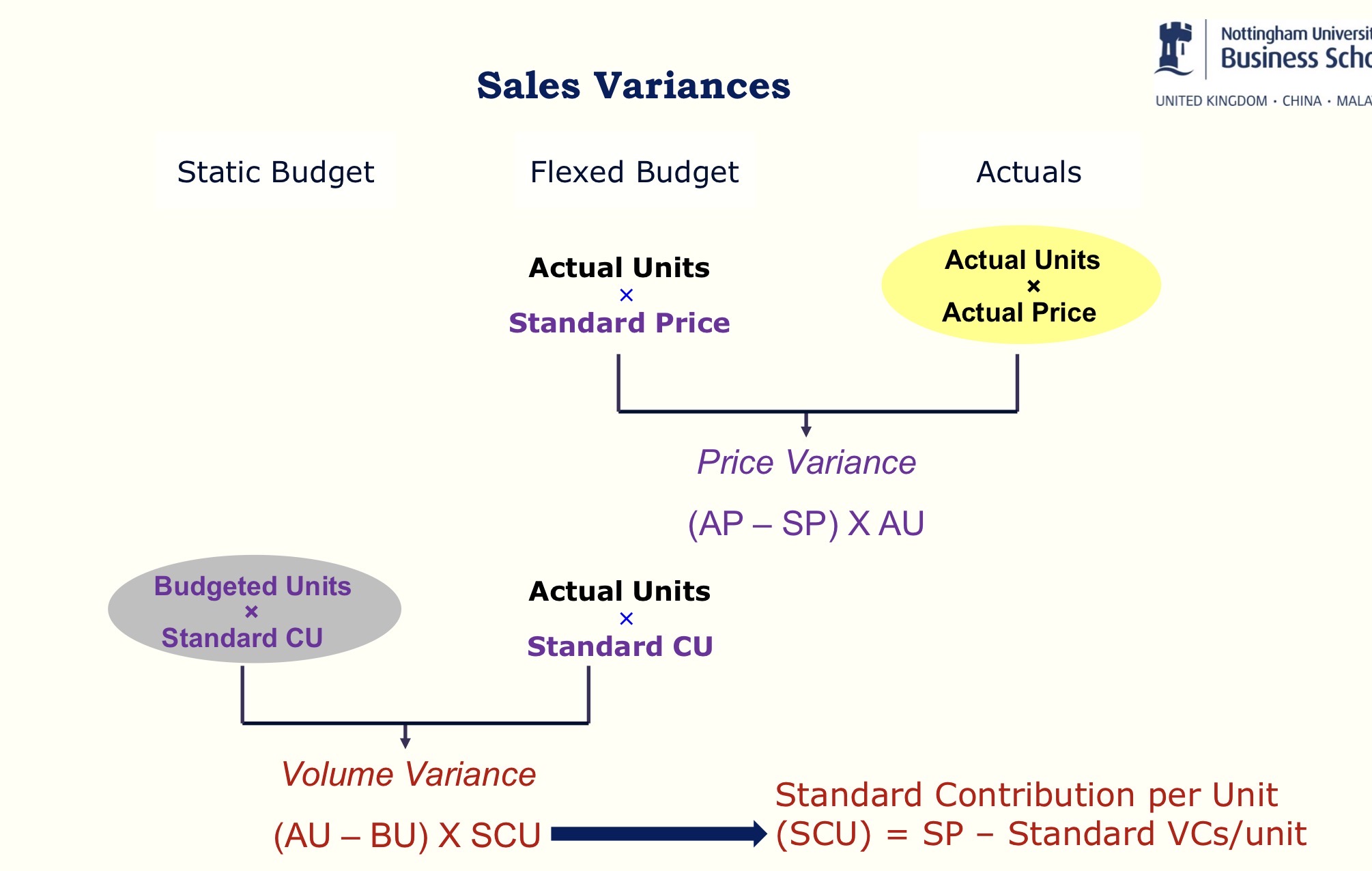

How do you find sales price variance?

Difference between Flexed budget and Actuals budget

(AP - SP) x AU

(U = units)

What does sales price variance show?

The effect different selling prices have on PROFIT

How do you find sales volume variance?

Difference between static budget and flexed budget

(AU - SU) x SCU

SCU = standard contribution per unit

How do you determine if sales variance is favourable or unfavourable?

Actual > Standard / budgeted → F

Actual < Standard / budgeted → U

NOTE; this is different to with costs, write as Standard < Actual etc

How do you fid the standard contribution per unit (SCU)?

SCU = SP - Standard VCs/unit

SP = Standard selling prices

VC = standard variable costs

What diagram relates sales price variance and sales volume variance?

NOTE;

Top row = difference in sales revenue in budgets

Bottom row = difference in contribution in budgets

What are ALL of the variance formulas?

Note: first 6 all cost variance, standard first. Last two are sales variance, actua first)

(S_ - A_)

Vs

(A_ - S_)

What is SP?

CAREFUL:

In cost analysis: SP = Standard purchase price

In sales analysis SP = Standard selling price

What is the reconciliation report?

Report including all variances, helps management clearly see

Describe what this report looks like, what is it showing?

Note favourable variance in favourable column, likewise for unfavourable

How do you calculate material price variance in reconciliation?

Based on AQ used

(SP - AP) X AQ USED

[Rather than AQ purchased]

How do you find budgeted contribution?

BU x SCU

What is management by exception?

Identifying unfavourable variances, like people underperforming

What are the advantages of standard costing?

Management by exception

Better info for planning & decision making

Improved cost control

Can lead to reduction in production cost

What are the limitations of standard costing?

Time consuming, little value given to time to prepare (some for budgeting)

Variances can’t be seen in isolation → can be misinterpreted

Emphasising standards may exclude other important objectives

Standard costs reports may not be timely (done at end of period)

Focusing on negative variances may negatively impact employee morale.

Why can’t variances be seen in isolation?

Cause there can be external reasons for favourable / unfavourable variances.

E.g. favourable material price variance (paying less than expected), could be due to buying low quality materials or from negotiation - don’t know.

What does this mean: “Emphasising standards may exclude other important objectives”

E.g. Standard material usage could be 4kg, once workers achieve this might just continue doing that

However, it could be possible to reduce waste even further and use 3.8kg of material for one unit. Should instead encourage improvement

Why is material price variance usually calculated when materials are purchased/received rather than when they are used?

Timely evaluation of purchasing decisions

Inventory is stored at STANDARD COST:

Do raw materials inventory + material price variance = actual value