Econ First Assessment Notecards

1/132

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

133 Terms

Economics

the study of the allocation of scarce resources among alternative and competing.

Goal: use resources where highest valued.

Rational-Actor Paradigm

People tend to act rationally, optimally, and self-interestedly.

at the time decision is made, not in retrospect

explains behavior when incentives change

suggests methods to change behavior

Policy Efficiency

not wasteful socially

does not mean desirable to each individual

want policies to improve efficiency

does not touch on distribution of wealth

Business Efficiency

not wasteful of resources

maximizing output for a given number of inputs

maximizing inputs for a given number of outputs

inefficiency is to be exploited

Economic Theory

a general principle that enables us to understand and predict the economic choices that people make

Economic Model

abstract world focused on a narrow set of relationships

leaves out irrelevant factors to question at hand

purpose is to understand relationships of interest

Utility

satisfaction from consuming a good or service

Fundamental Assumption of Economics

People are utility maximizers

Scarcity

Condition where our wants exceed what we can produce

Economic Cost

Accounting Cost + Opportunity Cost

Accounting Cost

(Explicit)

Dollar cost on your books

Opportunity Cost

(Implicit)

What you would have made in the best thing you didn’t do

Economic Profit

Total Revenue - Accounting Cost - Opportunity Cost

Total Revenue - Economic Cost

What is capitalism’s coordinating mechanism?

Price system

Thomas Mun background

1571-1641

Wealthy merchant

Director of East India company

Thomas Mun view

Mercantilism

What is mercantilism?

gold is wealth, gold is limited

so wealth is limited

become wealthy by acquiring gold

export more than you import

government encourages exports and not imports

“zero sum game”

trade isn’t even, one always gains more

England’s Treasure by Foreign Trade (1664)

wrote for mercantilist view on trade

written by Thomas Mun

Adam Smith background

1723 - 1790

born in Kirkcaldy, Scotland

known as fumbling, bumbling bachelor father of economics

became famous for “The Theory of Moral Sentiments”

“An Inquiry into the Nature and Causes of the Wealth of Nations”

Adam Smith view

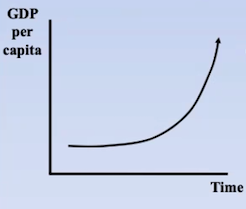

Wealth (National Standard of Living) = Goods + Services

Division of Labor / Specialization (limited by market)

Gains from Trade

trade because both better off

gain something from trade that’s valued more than the money

Invisible Hand Doctrine

Role of Government / Tax Policies / Externalities

Subsistence Theory of Wages X

Banking Regulation

Utility (Self-Interest)

Diamond-Water Paradox X

Monopoly

Rent Seeking

Price Fixing

Free Trade

Absolute Advantage

Antitrust

What is Invisible Hand Doctrine?

in a decentralized, free market economy, individuals pursuing their own self-interest will tend to benefit the economy as a whole

Thomas Robert Malthus background

1766 - 1834

godson of David Hume

best friends with David Ricardo - Intellectual adversaries

Thomas Malthus view

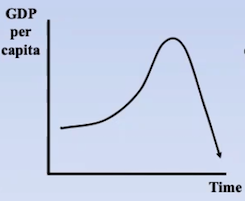

Law of Diminishing Returns (1815)

Population growth grows 2.5% / yr, doubles in 28 years

food production growing at decreasing rate

doomed unless economic choices at work, those who adapt best will survive

Malthusian “struggle for existence” inspires Darwin

"An Essay on the Principles of Population”

Cost-benefit analysis

Comparative Advantage

What is Labor Theory of Value?

value of an output is equal to the sum of its labor inputs

Karl Heinrich Marx background

rejected Jewish ancestry, debate over whether anti semitic

Religion “… opium of the people”

drank himself out of university

unwashed slob - “the Moor”

developed severe boils - Carbuncles

strong believer in Hegelian method - dialectic

life always in flux, things are always changing

any idea has opposite, they will do battle, change will come from it “synthesis”

"The Communist Manifesto” (1848)

“Das Kapital” (1867)

“From each according to his ability, to each according to his needs!”

Critique of the Gothra Programme, 1875

Karl Marx view

Dialectical Materialism

fusing of dialectic method with materialism

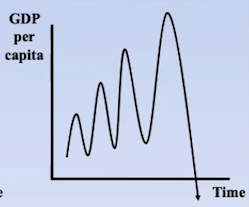

Business cycles (20 years of trough-to-trough)

Capitalism “Laws of Motion”: Unguided production — rises and slumps of higher intensity

socialism: rationally planned production

Collapse of capitalism inevitable “Iron necessity”

dependent on “Labor Theory of Value”

exploited workers

attacked perfect capitalism — perfect competition

but, capitalism was a necessary precondition for socialism

said virtually nothing about what to do after revolution

Alfred Marshall background

1842 - 1924

Teacher of John Maynard Keynes

Interested in philosophy

devoted life to economics after walking through “poorest of quarters” of cities, “looking at the faces of poor people”

focus on education to fix

Alfred Marshall view

Diagrammatic Economics

Scissors analogy for S & D

Partial Equilibrium

I only care about my market for my firm

Elasticity Theory

Theory of the Firm

Consumer Surplus

“Principles of Economics (1890)

Horizontal (Supply)

Quantity supplied at a particular price

Vertical (Supply)

Willingness to sell a little more at a particular quantity

i.e., economic cost of a marginal increase in output

Supply shifters

input prices

price/profitability of other goods

expectations of future prices

number of suppliers

technology

regulation

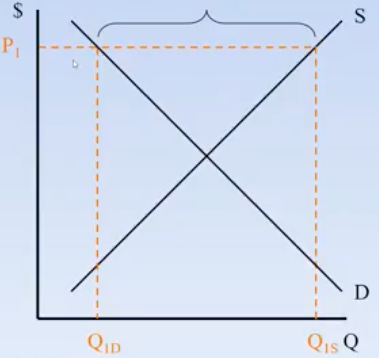

Surplus

Excess of supply over demand at a given price

Shortage

excess of demand over supply at a given price

Competitive prices signal

value and scarcity on the margin

“demand, willingness to pay” “supply” “of one more, of one extra unit”

Marginal Analysis

examines the change in one variable with respect to a small change in another

Why do economists care about marginal analysis?

prices determined on the margin

most economic decisions are marginal

Consumer surplus

excess of what consumers are willing to pay over what they have to pay for a good

net value to consumers (i.e., utility received but not paid for)

Producer surplus

excess of what sellers receive over the minimum they require (i.e., economic cost) to produce a particular quantity

net value to the company

Social Welfare

excess of consumer willingness to pay over the minimum producers require for a particular quantity

sum of consumer and producer surplus

Deadweight Loss (Welfare Loss, Inefficiency)

loss in social welfare due to market inefficiency

DWLs are wasteful of resources

Who became famous for “The Theory of Moral Sentiments” and “An Inquiry Into the Nature and Causes of the Wealth of Nations”

Adam Smith

Who said Wealth = Goods + Services

Adam Smith

Who said both parties gain from trade?

Adam Smith

Who was famous for “The Communist Manifesto” and “Das Kapital”

Karl Marx

Who wrote “The Essay on the Principles of Population”

Thomas Malthus

Elasticity

Measures the sensitivity of one variable to small changes in another

invariant to units of measure

affected by slope, but not slope

Formula for price elasticity of demand

% change in quantity / % change in price OR

(change in quantity / quantity) / (change in price / price)

Formula for Arc Price Elasticity of Demand (two prices and two quantities)

| ((Q2 - Q1) / AVG (Q1 and Q2)) / ((P2 - P1) / AVG (P1 and P2))

Pricing tradeoff assumes you are maximizing what?

Total Revenue

Pricing is

tradeoff between revenue and variable costs

With respect to elasticity, the goal of business is to

make its demand as inelastic (vertical) as possible

Determinants of Elasticity

number of close substitutes

proportion of budget (related to price)

time period to adjust

individual brand or industry aggregate

Formula for Cross Price Elasticity of Demand

% change in quantity of X / % change in price of Y OR

(change in quantity of X / quantity of X) / (change in price of Y / price of Y)

Economic definition of a firm

institution specializing in the production of goods and services for others

Why do firms exist?

specialization is productive

firms and markets are complements

variable input

varies with output over given time period

fixed input

constant with respect to output over given time period

Short run (SR)

time period in which at least one input is fixed

when you can’t reasonably expand all of your inputs

Long Run (LR)

time period in which all inputs are variable (i.e., can be reasonably adjusted

In class, what is assumed for labor and capital in short run?

labor is variable and capital is fixed

In class, what is assumed for labor and capital in long run?

labor and capital are variable

Total fixed cost (TFC) formula

R x K

r = rental rate (price) of capital

k = quantity of capital (fixed input)

Average fixed cost (AFC) formula

TFC / Q

Total variable cost (TVC) formula

w = wage rate (price of labor)

L = quantity of labor (variable input)

Average variable cost (AVC) formula

TVC / Q

Total cost (TC) formula

TFC + TVC

Average Total Cost (ATC) formula

AFC + AVC

(TFC / Q) + (TVC / Q)

Marginal Cost (MC) formula

change in total cost / change in quantity

change in TVC / change in quantity

Sunk costs

portion of fixed costs that cannot be recovered

Decision making mistakes

considering irrelevant costs (fixed/sunk)

ignoring relevant costs (opportunity)

Marginal Product of Labor (MPL)

extra output from employing an additional laborer

Marginal Product of Labor (MPL) formula

change in quantity / change in labor

Average Product of Labor (APL)

average output per laborer

Average Product of Labor (APL) formula

quantity / labor

Law of Diminishing Returns

when equal increments of a variable input are successively added to a fixed input, the extra output will eventually diminish due to unbalanced growth

Point of Diminishing Returns

the output level where marginal cost is minimized

the worker where marginal product is maximized

the point beyond which every business must go to maximize profits

Increasing Returns to Scale (IRS, Economies of Scale)

if you increase all inputs by X%, output increases by more than X%

Constant Returns to Scale (CRS)

if you increase all inputs by X%, output increases by exactly X%

Decreasing Returns to Scale (DCS), Diseconomies of Scale)

if you increase all inputs by X%, output increases by less than X%

Returns to scale is a what type of concept?

Long-run

Minimum Efficient Scale (MES)

the smallest production level or scale at which average costs are minimized

the smallest output level of CRS

“Top Two Principles” (Elasticity, Production, Costs)

with respect to elasticity, the goal of business is to make its demand as inelastic (vertical) as possible

when making a decision, consider only the costs and benefits that vary with the consequence of the decision

ignore irrelevant costs (fixed and sunk costs)

consider relevant hidden costs (opportunity costs)

Who was famous for Das Kapital (1867)?

Karl Marx

What year was Das Kapital made?

1867

Who was famous for The Principles of Economics (1890)?

Alfred Marshall

What year was The Principles of Economics made?

1890

Who was famous for An Inquiry into the Nature and Causes of the Wealth of Nations (1776)?

Adam Smith

When was An Inquiry into the Nature and Causes of the Wealth of Nations made?

1776

Whose view does the graph represent?

Karl Marx

Whose view does the graph represent?

Thomas Malthus

Whose view does the graph represent?

Adam Smith

normal good

a product where an increase in income raises its sales

inferior good

an increase in income causes a reduction in spending

Oligopoly Assumptions

Large number of buyers and a few sellers

firms are price makers

some barriers to entry

some close substitutes

company interaction is strategic

strategic interdependence in decision-making

all others same as perfect competition

Why do oligopolies exist?

economies of scale

large capital requirements

steel, airplanes, aluminum, pharmaceuticals

large advertising requirements

soft drinks, beer, pharmaceuticals

network effects

credit cards, social media, video games, phones

patents, reputation, etc

magnitude of these barriers affects real-world market structure

Collusion

when a group of firms behaves as if they were a single firm

Cooperation on competitive investments like joint venture is

Per Se Illegal

Inherently illegal “without elaborate inquiry as to the precise harm they have caused or the business excuse for their use”

Price Fixing Methods

High output prices

bid-ask spreads

vitamins

CDs

High margins

Low discounts

university financial aid

Low input prices

NCAA

tech company hiring

Allocation of customers / sales volume

carbon fiber / prepreg

Price fixing

typically provides NO social benefits

unlike some monopoly situation

simply adjusts industry P and Q to monopoly level

increases DWL without any offsetting benefits

purely welfare

per se illegal under antitrust laws

can be prosecuted as a criminal offense with prison sentences for managers involved