MICRO Exam 3

1/79

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

80 Terms

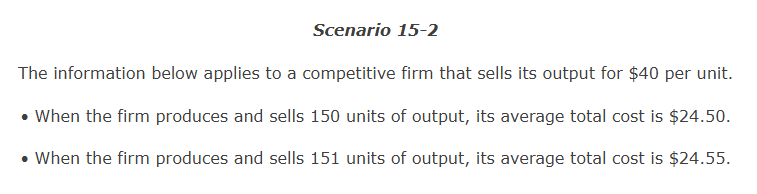

Refer to Scenario 15-2. When the firm produces 150 units of output, its total cost is

a. $3,525.75.

b. $3,675.00.

c. $3,850.25.

d. $3,450.00.

b. $3,675.00.

When fixed costs are ignored because they are irrelevant to a business's production decision, they are called

a. implicit costs.

b. sunk costs.

c. opportunity costs.

d. explicit costs.

b. sunk costs.

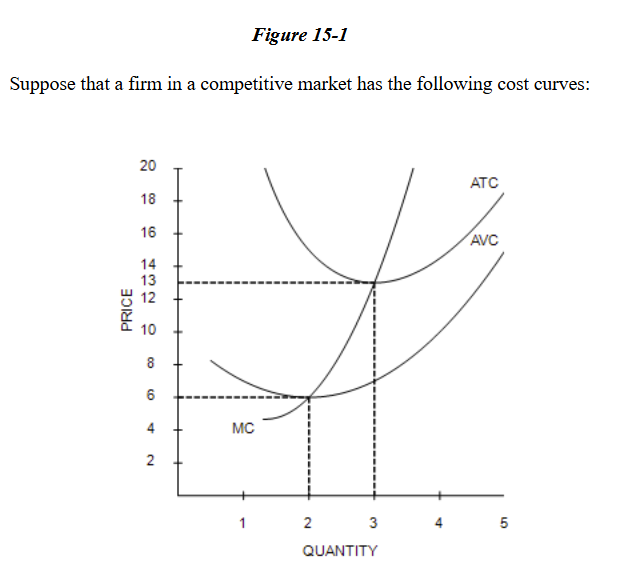

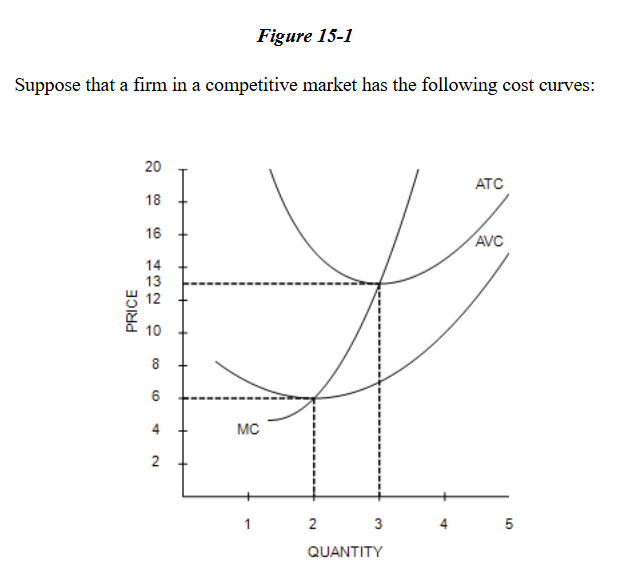

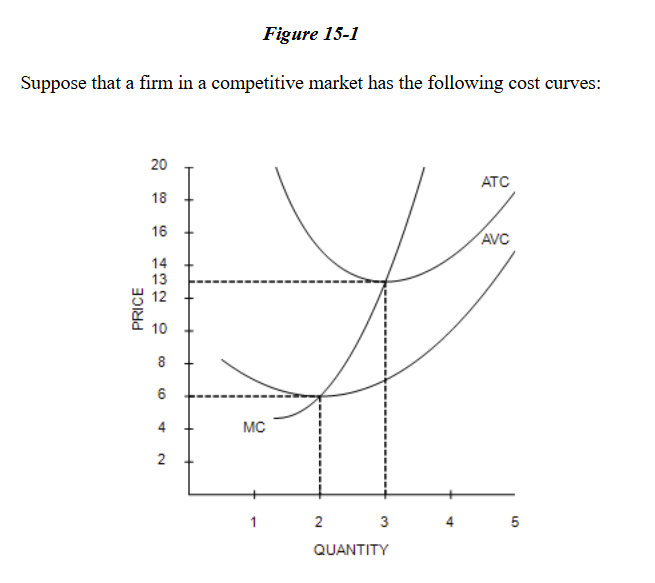

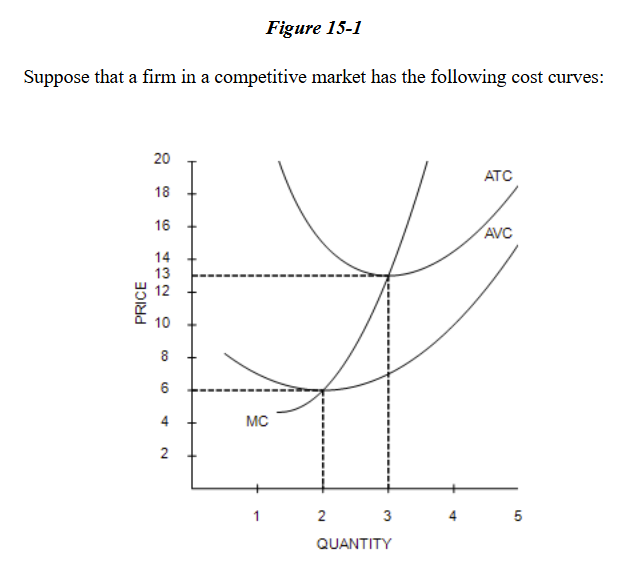

Refer to Figure 15-1. If the market price is $10, the firm will earn

a. negative economic profits in the short run but remain in business.

b. zero economic profits in the short run.

c. negative economic profits and shut down.

d. positive economic profits in the short run.

a. negative economic profits in the short run but remain in business.

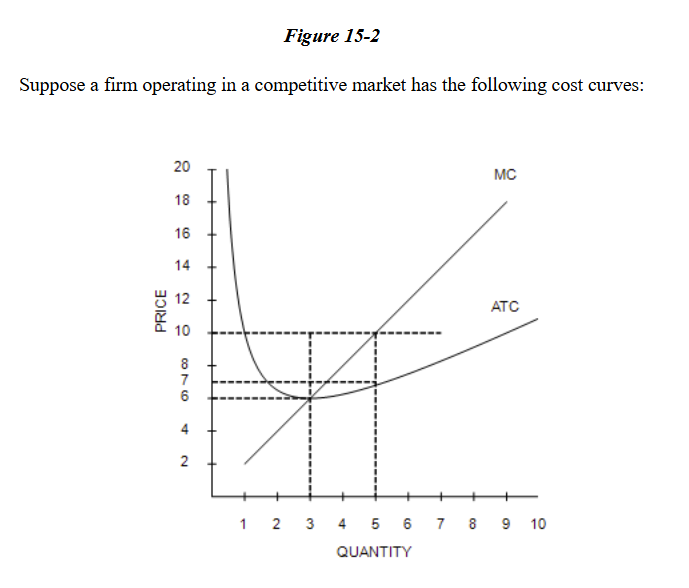

Refer to Figure 15-2. The firm will earn zero economic profit if the market price is

a. $6.

b. $0.

c. $10.

d. $7.

a. $6.

If a firm observes that the price of its product is above average variable cost, it would choose to continue to produce the good in the short run, even if that firm experiences economic losses.

a. True

b. False

a. True

A key characteristic of a competitive market is that

a. firms minimize total costs.

b. government antitrust laws regulate competition.

c. producers sell nearly identical products.

d. firms have price setting power.

c. producers sell nearly identical products.

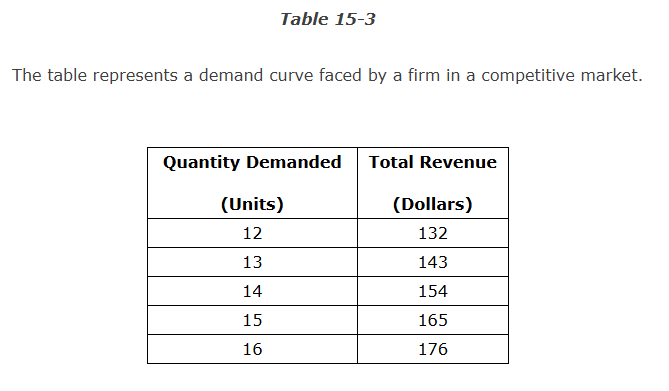

Refer to Table 15-3. For this firm, the average revenue when 14 units are produced and sold is

a. $15.

b. $13.

c. $9.

d. $11.

d. $11.

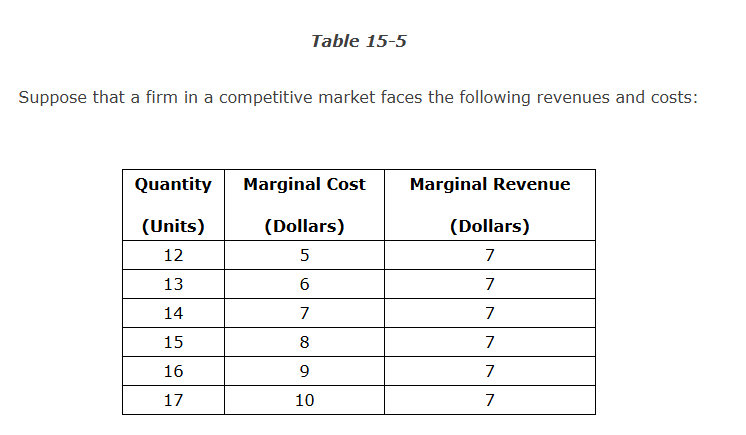

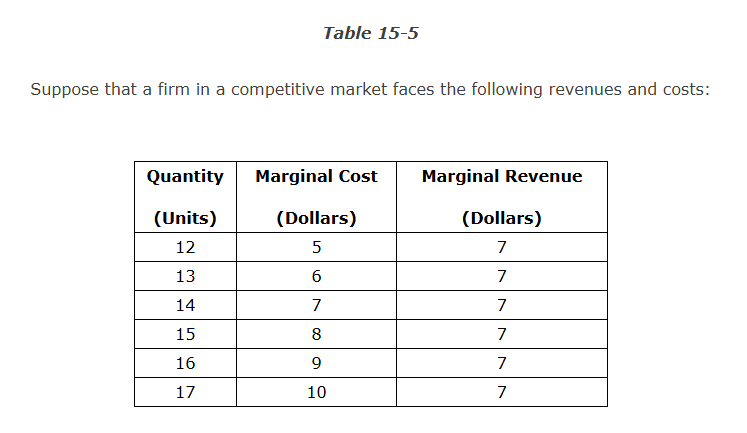

Refer to Table 15-5 . If the firm is currently producing 14 units, what would you advise the owners?

a. Decrease quantity to 13 units

b. Increase quantity to 15 units

c. Continue to operate at 14 units

d. Increase quantity to 16 units

c. Continue to operate at 14 units

Refer to Figure 15-1. The firm's short-run supply curve is its marginal cost curve above

a. $13.

b. $10.

c. $6.

d. $4.

c. $6.

Refer to Figure 15-1. If the market price falls below $6, the firm will earn

a. negative economic profits in the short run but remain in business.

b. negative economic profits in the short run and shut down.

c. zero economic profits in the short run.

d. positive economic profits in the short run.

b. negative economic profits in the short run and shut down.

Refer to Figure 15-1. The firm will earn a negative economic profit but remain in business in the short run if the market price is

a. above $13.

b. less than $13 but more than $6.

c. above $13 but less than $18.

d. less than $6.

b. less than $13 but more than $6.

Firms in a competitive market are said to be price takers because there are many sellers in the market, and the goods offered by the firms are very similar if not identical.

a. True

b. False

a. True

Refer to Table 15-5. If the firm is maximizing profit, how much profit is it earning?

a. $10

b. There is insufficient data to determine the firm's profit.

c. $0.50

d. $7.50

b. There is insufficient data to determine the firm's profit.

Ms. Joplin sells colored pencils. The colored-pencil industry is competitive. Ms. Joplin hires a business consultant to analyze her company's financial records. The consultant recommends that Ms. Joplin increase her production. The consultant must have concluded that, at her current level of production, Ms. Joplin's

a. total revenues equal her total economic costs.

b. marginal revenue exceeds her total cost.

c. marginal revenue exceeds her marginal cost.

d. marginal cost exceeds her marginal revenue.

c. marginal revenue exceeds her marginal cost.

Free entry means that

a. a firm's marginal cost is zero.

b. no legal barriers prevent a firm from entering an industry.

c. government-funded research lowers the costs of patents and other barriers to entry.

d. the government pays any entry costs for individual firms.

b. no legal barriers prevent a firm from entering an industry.

Assume a certain firm in a competitive market is producing Q = 1,000 units of output. At Q = 1,000, the firm's marginal cost equals $15 and its average total cost equals $11. The firm sells its output for $12 per unit.

Refer to Scenario 15-1 . At Q = 1,000, the firm's profits equal

a. $4,000.

b. $1,000.

c. $3,000.

d. −$200.

b. $1,000.

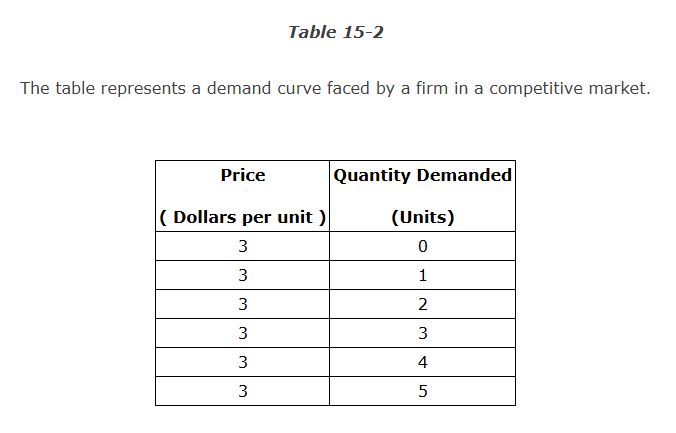

Refer to Table 15-2. For this firm, the average revenue from selling 3 units is

a. $1.

b. $12.

c. $3.

d. $4.

c. $3.

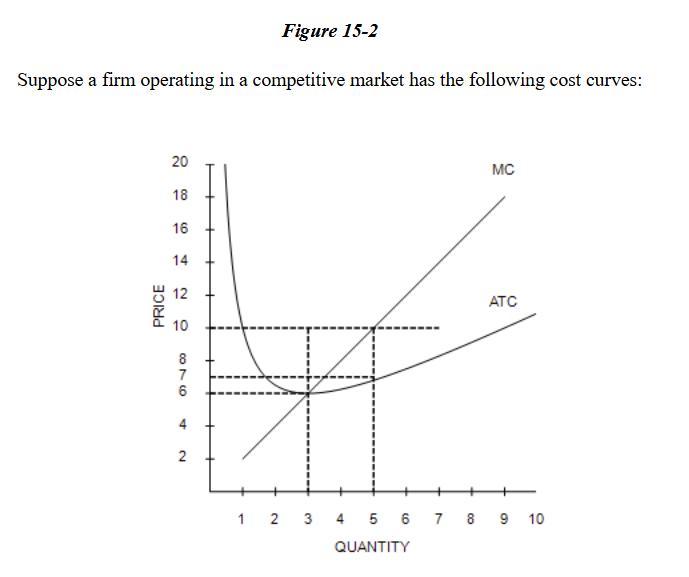

Refer to Figure 15-2. If the market price is $10, what is the firm's total revenue?

a. $50

b. $30

c. $15

d. $35

a. $50

For a firm operating in a perfectly competitive industry, marginal revenue and average revenue are equal.

a. True

b. False

a. True

A firm operating in a perfectly competitive industry will continue to operate in the short run but earn losses if the market price is less than that firm’s average total cost but greater than the firm’s average variable cost.

a. True

b. False

a. True

A monopoly can earn positive profits because it

a. can set the price it charges for its output but faces a horizontal demand curve.

b. can maintain a price such that total revenues will exceed total costs.

c. takes the market price as given and can sell unlimited quantities.

d. can sell unlimited quantities at any price it chooses.

b. can maintain a price such that total revenues will exceed total costs.

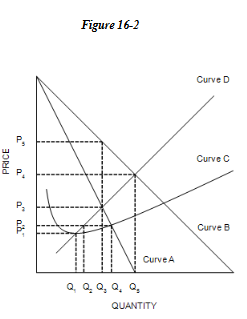

Refer to Figure 16-2. The demand curve for a monopoly firm is depicted by curve

a. C.

b. B.

c. D.

d. A.

b. B.

Which of the following is not an example of a barrier to entry?

a. Mighty Mitch's Mining Company owns a unique plot of land in Tanzania, under which lies the only large deposit of Tanzanite in the world.

b. A musician obtains a copyright for their original song.

c. A pharmaceutical company obtains a patent for a specific high blood pressure medication.

d. An entrepreneur opens a popular new restaurant.

d. An entrepreneur opens a popular new restaurant.

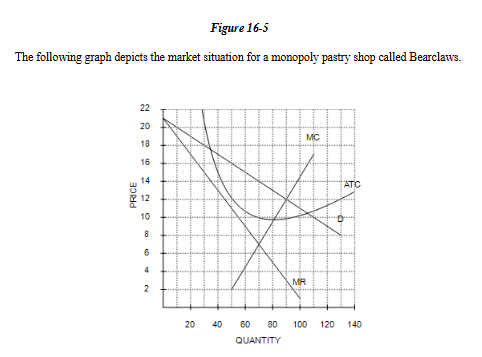

Refer to Figure 16-5. Given that Bearclaws chooses the profit-maximizing price and quantity, what profit level will it obtain?

a. $980.

b. $700.

c. $490.

d. $280.

d. $280.

If a monopolist is able to perfectly price discriminate,

a. consumer surplus and deadweight losses are transformed into monopoly profits.

b. the price effect dominates the output effect on monopoly revenue.

c. total surplus is always decreased.

d. consumer surplus is always increased.

a. consumer surplus and deadweight losses are transformed into monopoly profits.

During the life of a drug patent, the monopoly pharmaceutical firm maximizes profit by producing the quantity at which marginal revenue equals marginal cost.

a. True

b. False

a. True

A patent gives a single person or firm the exclusive right to sell some good or service forever.

a. True

b. False

b. False

Declining average total cost with increased production is one of the defining characteristics of a natural monopoly.

a. True

b. False

a. True

Since monopolists that practice price discrimination generally increase market output, compared to a monopoly that charges a single price, practicing price discrimination generally leads to a smaller deadweight loss.

a. True

b. False

a. True

The profit that a monopolist earns represents a loss to society that is measured through deadweight loss.

a. True

b. False

b. False

In order for a firm to maximize profits through price discrimination, the firm must have some market power and be able to prevent arbitrage.

a. True

b. False

a. True

Movie theatres charge different prices to different groups of people based on the differing marginal costs that exist from group to group.

a. True

b. False

b. False

The socially efficient quantity is found where the demand curve intersects the marginal cost curve.

a. True

b. False

a. True

Like competitive firms, monopolies choose to produce a quantity in which marginal revenue equals marginal cost.

a. True

b. False

a. True

Monopolists can practice price discrimination in all monopoly markets.

a. True

b. False

b. False

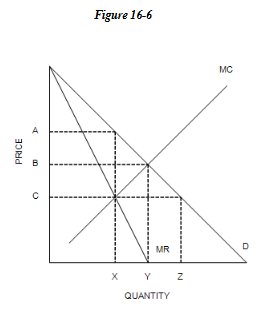

Refer to Figure 16-6. What is the socially efficient price and quantity?

a. Price = B; quantity = X

b. Price = B; quantity = Y

c. Price = A; quantity = X

d. Price = C; quantity = Y

b. Price = B; quantity = Y

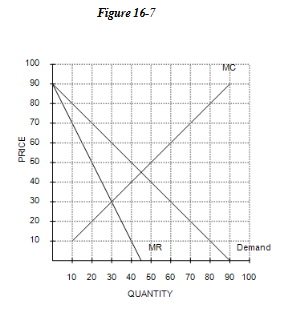

Refer to Figure 16-7. To maximize total surplus, a benevolent social planner would choose which of the following outcomes?

a. Q = 60 and P = 30

b. Q = 30 and P = 30

c. Q = 30 and P = 60

d. Q = 45 and P = 45

d. Q = 45 and P = 45

A natural monopoly occurs when

a. production requires the use of free natural resources, such as water or air.

b. there are economies of scale over the relevant range of output.

c. the product is sold in its natural state, such as water or diamonds.

d. the firm is characterized by a rising marginal cost curve.

b. there are economies of scale over the relevant range of output.

A monopoly firm maximizes its profit by producing Q = 500 units of output. At that level of output, its marginal revenue is $30, its average revenue is $60, and its average total cost is $34.

Refer to Scenario 16-1. At Q = 500, the firm's marginal cost is

a. $34.

b. less than $30.

c. greater than $34.

d. $30.

d. $30.

Which of the following is not an example of price discrimination by a firm?

a. A senior citizens' discount

b. Children's meals at a restaurant

c. Coupons in the Sunday newspaper

d. A natural gas company charging all customers a higher rate in the winter than in the summer

d. A natural gas company charging all customers a higher rate in the winter than in the summer

The commercial jetliner industry consisting of Boeing and Airbus would best be described as

a. an oligopoly.

b. a monopolistically competitive market.

c. a monopoly.

d. a perfectly competitive market.

a. an oligopoly.

A monopolistically competitive firm is currently producing 20 units of output. At this level of output, the firm is charging the highest price it can at $20, has marginal revenue equal to $12, has marginal cost equal to $12, and has average total cost equal to $18. From this information we can infer that

a. firms are likely to leave this market in the long run.

b. the firm is earning zero profit.

c. the profits of the firm are negative.

d. the firm is currently maximizing its profit.

d. the firm is currently maximizing its profit.

Which of the following statements is not correct?

a. Monopolistic competition is different from oligopoly because each seller in monopolistic competition is small relative to the market, whereas each seller can affect the actions of other sellers in an oligopoly.

b. Monopolistic competition is different from monopoly because monopolistic competition is characterized by free entry, whereas monopoly is characterized by barriers to entry.

c. Both monopolistic competition and perfect competition are characterized by product differentiation.

d. Both monopolistic competition and oligopoly fall in between the more extreme market structures of competition and monopoly.

c. Both monopolistic competition and perfect competition are characterized by product differentiation.

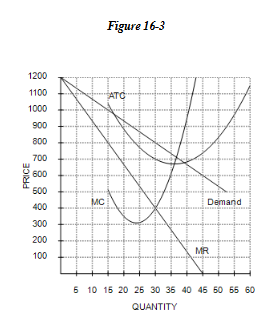

Refer to Figure 16-3. At the profit-maximizing, or loss-minimizing, output level, how many units of output will the firm in this figure produce?

a. 30

b. 20

c. This firm will choose not to produce.

d. 40

a. 30

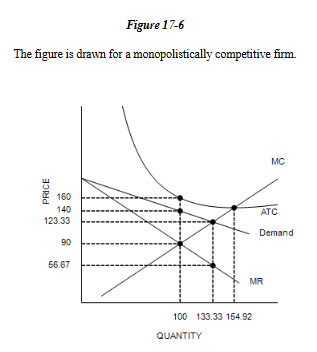

Refer to Figure 17-6. In response to the situation represented by the figure, we would expect

a. the demand for this firm's product to decrease, assuming this firm does not exit.

b. new firms to enter the market.

c. this firm's profit to remain the same.

d. some of the firms that are currently in the market to exit.

d. some of the firms that are currently in the market to exit.

A monopolistically competitive market is characterized by barriers to entry.

a. True

b. False

b. False

Monopolistically competitive firms, like monopoly firms, maximize their profits by charging a price that exceeds marginal cost.

a. True

b. False

a. True

Oligopoly is characterized by a few sellers offering similar products, whereas monopolistic competition is characterized by many sellers offering differentiated products.

a. True

b. False

a. True

In the long run, monopolistically competitive firms produce where demand equals marginal cost.

a. True

b. False

b. False

The product-variety externality states the benefits to consumers from the introduction of a new product.

a. True

b. False

a. True

The business-stealing externality states that entry of a new firm imposes a cost on existing firms because they lose customers.

a. True

b. False

a. True

In a monopolistically competitive market, the number of firms adjusts until economic profits are driven to zero.

a. True

b. False

a. True

In the long run, monopolistically competitive firms produce where demand equals average total cost.

a. True

b. False

a. True

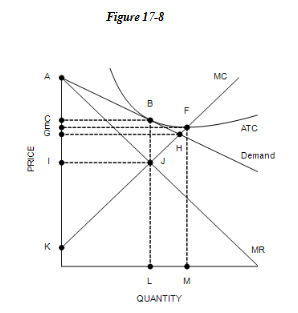

Refer to Figure 17-8. Which of the following best describes the profit-maximizing outcome for the firm depicted here?

a. This firm is incurring a short-run loss, but will earn zero profit in the long run.

b. This firm is earning zero profit in the short run, but will earn a positive profit in the long run.

c. This firm is in long-run equilibrium and will continue to earn zero profit.

d. This firm is earning a short-run profit, but will earn zero profit in the long run.

c. This firm is in long-run equilibrium and will continue to earn zero profit.

Refer to Figure 17-6. In order to maximize its profit, the firm will choose to produce

a. 154.92 units of output.

b. 100 units of output.

c. between 100 and 133.33 units of output.

d. 133.33 units of output.

b. 100 units of output.

Monopolistic competition is considered inefficient because

a. output is excessive.

b. barriers to entry limit the number of firms in the market.

c. price exceeds marginal cost.

d. long-run profits are positive.

c. price exceeds marginal cost.

Which of the following is not a key feature of monopolistic competition?

a. Differentiated products among firms in the market

b. Positive economic profits for firms in the long run

c. Excess capacity

d. A markup of price over marginal cost

b. Positive economic profits for firms in the long run

For a monopolistically competitive firm,

a. at the profit-maximizing quantity of output, price equals the minimum of average total cost.

b. at the profit-maximizing quantity of output, price equals marginal cost.

c. at the profit-maximizing quantity of output, marginal revenue equals marginal cost.

d. marginal revenue and price are the same.

c. at the profit-maximizing quantity of output, marginal revenue equals marginal cost.

Which of the following statements is correct?

a. Monopolistic competition is similar to monopoly because both market structures are characterized by firms being price makers rather than price takers.

b. Monopolistic competition is similar to perfect competition because both market structures are characterized by differentiated products.

c. Monopolistic competition is similar to perfect competition because both market structures are characterized by perfectly elastic demand curves facing each firm.

d. Monopolistic competition is similar to oligopoly because both market structures are characterized by strategic interaction between firms in the market.

a. Monopolistic competition is similar to monopoly because both market structures are characterized by firms being price makers rather than price takers.

The two types of imperfectly competitive markets are

a. monopolistic competition and oligopoly.

b. monopoly and monopolistic competition.

c. monopolistic competition and cartels.

d. monopoly and oligopoly.

a. monopolistic competition and oligopoly.

When all firms choose their best strategy given the strategies that all the other firms have chosen, the result is a Nash equilibrium.

a. True

b. False

a. True

A tit-for-tat strategy, in a repeated game, is one in which a player starts by cooperating and then does whatever the other player did last time.

a. True

b. False

a. True

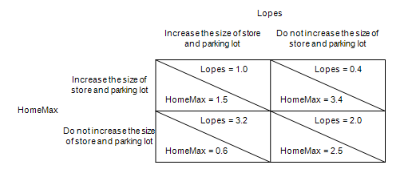

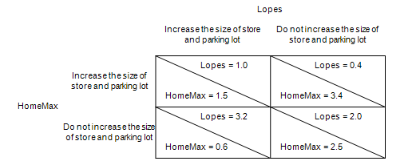

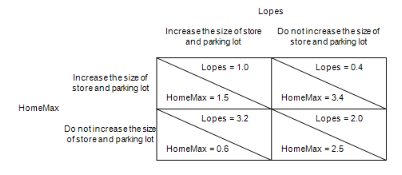

Two home-improvement stores (Lopes and HomeMax) in a growing urban area are interested in expanding their market share. Both are interested in expanding the size of their store and parking lot to accommodate potential growth in their customer base. The following game depicts the strategic outcomes that result from the game. Increases in annual profits (in millions of dollars) of the two home-improvement stores are shown in the following figure.

Refer to Table 18-6 . Pursuing its own best interest, Lopes will

a. increase the size of its store and parking lot only if HomeMax also increases the size of its store and parking lot.

b. increase the size of its store and parking lot regardless of the decision made by HomeMax.

c. not increase the size of its store and parking lot regardless of the decision made by HomeMax.

d. increase the size of its store and parking lot only if HomeMax does not increase the size of its store and parking lot.

b. increase the size of its store and parking lot regardless of the decision made by HomeMax.

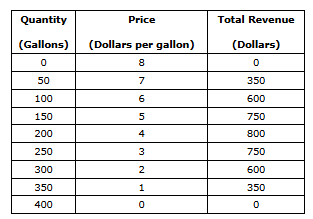

The table shows the town of Driveaway's demand schedule for gasoline. Assume the town's gasoline seller(s) incurs a cost of $2 for each gallon sold, with no fixed cost.

Refer to Table 18-5. If there are exactly five sellers of gasoline in Driveaway and if they collude, then which of the following outcomes is most likely?

a. Each seller will sell 30 gallons and charge a price of $4.

b. Each seller will sell 30 gallons and charge a price of $5.

c. Each seller will sell 40 gallons and charge a price of $4.

d. Each seller will sell 50 gallons and charge a price of $3.

b. Each seller will sell 30 gallons and charge a price of $5.

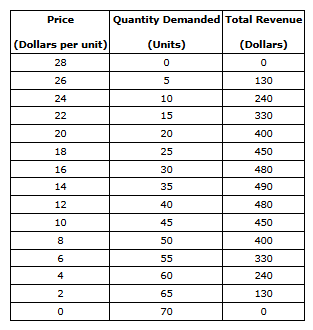

Only two firms, ABC and XYZ, sell a particular product. The following table shows the demand curve for their product. Each firm has the same constant marginal cost of $8 and zero fixed cost.

Refer to Table 18-4. If ABC and XYZ operate to jointly maximize profits, then what quantity is sold?

a. 30

b. 35

c. 25

d. 40

c. 25

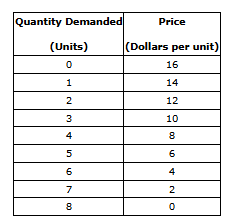

The table shows the demand schedule for a particular product.

Refer to Table 18-3. Suppose the market for this product is served by two firms that have formed a cartel. If the marginal cost of production is $4 and each firm incurs a fixed cost of $6, the combined profit of the cartel will be

a. $12

b. $32

c. $6

d. $24

c. $6

Which of the following examples illustrates an oligopoly market?

a. A farmers' market with many individuals selling sweet corn and tomatoes

b. A city with two firms that are licensed to sell school uniforms for the local schools

c. A city whose electrical service is provided by one electric co-operative

d. A city with many independently owned hair styling salons

b. A city with two firms that are licensed to sell school uniforms for the local schools

Two home-improvement stores (Lopes and HomeMax) in a growing urban area are interested in expanding their market share. Both are interested in expanding the size of their store and parking lot to accommodate potential growth in their customer base. The following game depicts the strategic outcomes that result from the game. Increases in annual profits (in millions of dollars) of the two home-improvement stores are shown in the following figure.

Refer to Table 18-6. If both stores follow a dominant strategy, Lopes's annual profit will grow by

a. $3.2 million.

b. $1.0 million.

c. $0.4 million.

d. $2.0 million.

b. $1.0 million.

Two home-improvement stores (Lopes and HomeMax) in a growing urban area are interested in expanding their market share. Both are interested in expanding the size of their store and parking lot to accommodate potential growth in their customer base. The following game depicts the strategic outcomes that result from the game. Increases in annual profits (in millions of dollars) of the two home-improvement stores are shown in the following figure.

Refer to Table 18-6. When this game reaches a Nash equilibrium, annual profit will grow by

a. $0.6 million for HomeMax and by $3.2 million for Lopes.

b. $1.5 million for HomeMax and by $1.0 million for Lopes.

c. $3.4 million for HomeMax and by $0.4 million for Lopes.

d. $2.5 million for HomeMax and by $2.0 million for Lopes.

b. $1.5 million for HomeMax and by $1.0 million for Lopes.

If firms in an oligopoly agree to produce according to the monopoly outcome, they will produce the same level of output as they would produce in a Nash equilibrium.

a. True

b. False

b. False

A group of firms that collude is called a cartel.

a. True

b. False

a. True

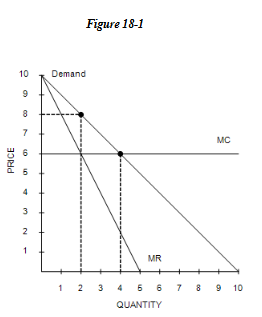

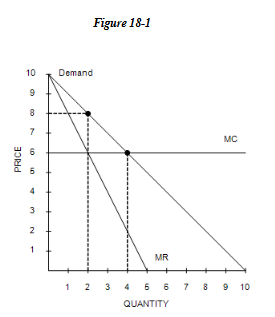

Refer to Figure 18-1. Suppose this market is served by two firms who each face the marginal cost curve shown in the diagram. The marginal revenue curve that a monopolist would face in this market is also shown. If the firms are able to collude successfully,

a. the total output will be 2 units and the price will be $8.00 per unit.

b. there will be no deadweight loss.

c. the total output will be 2 units and the price will be $6.00 per unit.

d. the total output will be 4 units and the price will be $6.00 per unit.

a. the total output will be 2 units and the price will be $8.00 per unit.

Refer to Figure 18-1. Suppose this market is served by two firms who each face the marginal cost curve shown in the diagram and have zero fixed cost. The marginal revenue curve that a monopolist would face in this market is also shown. If the firms are able to collude successfully, each firm should earn a profit equal to

a. $2.

b. $6.

c. $4.

d. $1.

a. $2.

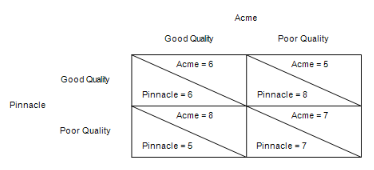

Two companies, Acme and Pinnacle, each decide whether to produce a good quality product or a poor quality product. In the figure, the dollar amounts are payoffs and they represent annual profits (in millions of dollars) for the two companies.

Refer to Table 18-7. If this game is played only once, then the most likely outcome is that

a. both firms produce a poor quality product.

b. Acme produces a good quality product and Pinnacle produces a poor quality product.

c. both firms produce a good quality product.

d. Acme produces a poor quality product and Pinnacle produces a good quality product.

c. both firms produce a good quality product.

Nadia and Maddie are two college roommates who both prefer a clean common space in their dorm room, but neither enjoys cleaning. The roommates must each make a decision to either clean or not clean the dorm room's common space. The following table shows the payoffs for this situation, where the higher a player's payoff number, the better off that player is.

Refer to Table 18-9. If Maddie chooses to clean, then Nadia will

a. not clean and Maddie's payoff will be 7.

b. not clean and Maddie's payoff will be 10.

c. clean and Maddie's payoff will be 30.

d. clean and Maddie's payoff will be 50.

a. not clean and Maddie's payoff will be 7.

The essence of an oligopolistic market is that there are only a few sellers.

a. True

b. False

a. True

Cartels are difficult to maintain because

a. the monopoly output is very difficult to determine.

b. costs to the firms in a cartel are continually rising.

c. the number of firms is always large.

d. each firm has an incentive to deviate from its agreed output level.

d. each firm has an incentive to deviate from its agreed output level.

Two companies, Acme and Pinnacle, each decide whether to produce a good quality product or a poor quality product. In the figure, the dollar amounts are payoffs and they represent annual profits (in millions of dollars) for the two companies.

Refer to Table 18-7. The more frequently this game is played, the more likely it is that

a. one firm will experience an increase in profits and the other will experience a decrease in profits.

b. both firms will produce a poor quality product.

c. both firms will produce a good quality product.

d. both firms experience a reduction in profits compared to the Nash equilibrium outcome.

b. both firms will produce a poor quality product.

Which of the following statements about oligopolies is not correct?

a. Oligopolistic firms are interdependent in a way that competitive firms are not.

b. An oligopolistic market has only a few sellers.

c. The actions of any one seller can have a large impact on the profits of all other sellers.

d. Unlike monopolies and monopolistically competitive markets, oligopolies prices do not exceed their marginal costs.

d. Unlike monopolies and monopolistically competitive markets, oligopolies prices do not exceed their marginal costs.

In which of the following markets are strategic interactions among firms most likely to occur?

a. The market for tennis balls

b. Markets to which patent and copyright laws apply

c. The market for piano lessons

d. The market for corn

a. The market for tennis balls